EXPE - Expedia: Cracks Are Emerging But At Least The Stock Is Cheap

2023-08-15 09:13:30 ET

Summary

- Expedia's Q2 earnings disappointed, causing shares to drop over 10%.

- Bookings trends are not meeting expectations, possibly due to the rollout of Expedia's new loyalty program One Key.

- However, margins are expanding, thanks to the company deferring marketing spend. This has led to superb earnings growth.

- Expedia stock is trading at very cheap P/E multiples, making it an opportune short-term buy.

Earnings season has been fairly punishing so far to any company reporting less-than-perfect results, and for companies that faced a high bar of expectations going into earnings, a slip-up was almost guaranteed. Such is the case for Expedia ( EXPE ), the global travel platform that had high expectations riding on record summer travel demand.

Since reporting Q2 earnings, shares of Expedia are down more than 10% (initially having fallen more than 20% after the results first dropped). Year to date, the stock is still up 26% - though that's barely above the S&P 500, and pales significantly below its larger competitor Booking.com which is up more than 50% on the year.

Expedia's risks are offset by a cheap price

New risks have emerged for Expedia. We'll get into the specifics of Q2 results in the next section, but in brief: bookings trends may not be playing out as we expected heading into a reportedly hot travel season. Expedia's bookings dipped sequentially from Q1 to Q2, which is abnormal seasonality. Part of this is driven by Vrbo, the Airbnb competitor that saw soft bookings trends as customers opted for shorter-term stays in more urban destinations.

But part of the weakness may also be due to the rollout of One Key, Expedia's new loyalty program encompassing all its brands that essentially offers a 2% rebate for booking through an Expedia site. Expedia likes to tout that it is the only OTA with a universal loyalty program, but customers may not see that to be the case: as I noted on my prior article on Expedia, a Hotels.com user used to earn "Stamps" that basically equated to a 10% rebate, and now under the One Key program that earnings rate has been materially slashed.

Plus: travel portals through banking sites like Chase ( JPM ) and Citi ( C ) often offer between 5-10 credit card points for booking through their travel portals instead of through third parties. Softer hotel bookings for Expedia may not be a reflection of the market, but customers voting with their dollars.

In spite of these risks, I do remain cautiously bullish on Expedia, which is primarily a valuation-driven argument. The good news is that Expedia is raising its profitability margins, and even though bookings are decelerating, they are still near record levels - which is allowing the company to pump out impressive profitability.

It's worth noting that Expedia trades at a meaningfully lower P/E multiple versus the more reliable Booking:

Here, in my view, are the core bullish arguments in favor of Expedia:

- Red-hot travel demand- After a quiet COVID season, travelers are catching up on lost vacations. Picking up on strong end-customer demand, airlines and hotels have also raised rates, which benefits Booking's commission model.

- Work from anywhere- Airbnb ( ABNB ) has cited this as a benefit to its growth in stays: now that many companies have allowed remote-work from anywhere, many travelers are opting to stay in vacation destinations for extended chunks of time, bringing their work laptops with them. This new "format" for travel has increased wallet share and spending on overall travel.

- Vrbo is Expedia's answer to Airbnb- Whether customers want to stay in a hotel or book a vacation rental home (both formats of stays, we now universally agree, are two entirely different types of vacations, with the former generally offering more creature comforts and the latter a more authentic, local experience), Expedia has the right option for its customers' preferences.

- One Key may help to unify Expedia's brands- Outside of its namesake site, Expedia is also home to Orbitz, Vrbo, Hotels.com, Hotwire, HomeAway, Egencia, and a number of other brands. The company's plan to unify all of its rewards programs under "One Key" this year will hopefully help to maximize the group's marketing spend and boost its following.

All in all, it's worth buying Expedia on the recent dip, but this stock needs constant monitoring. I don't view Expedia as a buy-and-hold play: if the stock manages to eke up to a ~14x P/E multiple (implying a $132 price target ), I'd take profits and run.

Q2 download

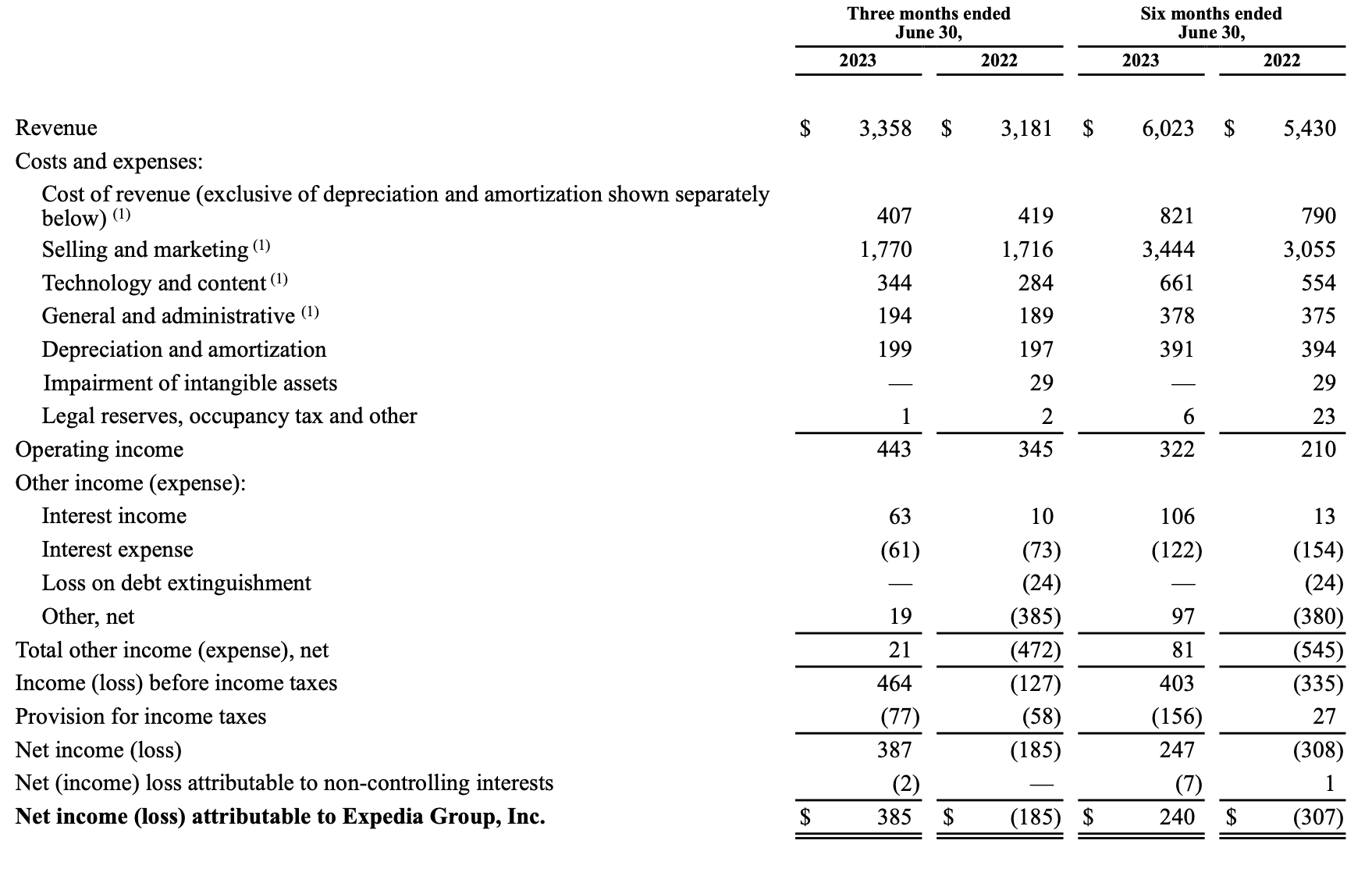

Let's now go through Expedia's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Expedia's revenue grew only 5.5% y/y to $3.36 billion in Q2, missing Wall Street's expectations of $3.37 billion and decelerating versus 18% y/y growth in Q1.

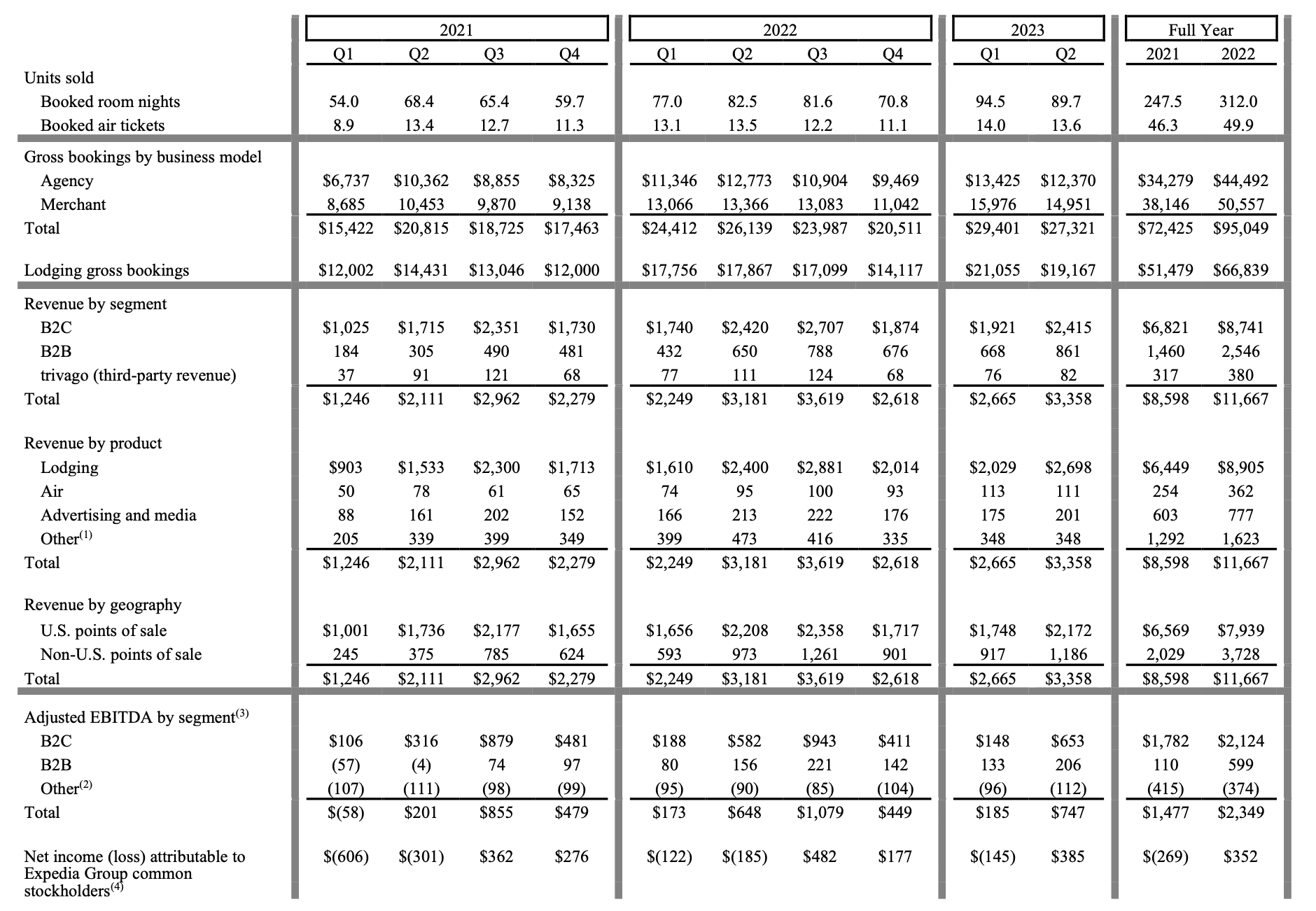

The chart below shows Expedia's key metrics over time. Note that booked room nights grew 9% y/y to 89.7 million, but declined sequentially versus Q1: which is atypical seasonality of the past two years.

{kind=link}

Similarly, air tickets also declined sequentially versus Q1. And even in Expedia's smallest segment, car rentals, the company noted softening rental rates due to higher inventory levels.

Softness across the board, however, may be due to Expedia's decision to pull back on marketing in the second quarter and save the spend for Q3, where travel demand peaks. Here is some helpful commentary from CEO Peter Kern's prepared remarks on the Q2 earnings call, detailing the end-market trends Expedia is experiencing:

We are particularly pleased that we were able to meet our second quarter financial goals while electing to move some marketing spend from Q2 to Q3, where we believe it can be better spent in support of the launch of one key and our accelerated growth in the back half of the year.

Industry trends have remained broadly consistent with the first quarter. And North America and Europe has remained stable with stronger growth in APAC and Latin America. Travelers worldwide continue to favor shorter stays in urban locations versus longer trips in sun and ski destinations. As far as pricing, both hotel and vacation rental ADRs are holding up year-over-year, while international cross-border airfares are stable. U.S. domestic airfares have seen some declines as capacity increases [...]

As we continue to move from a purely transaction, room-night-focused world to one in which we focus on customers and lifetime value, we have been able to build a bigger, more valuable base of these high ROI travelers. Our focus on acquiring and retaining loyalty members and app users to drive this strategy continues to show good results. This quarter active loyalty members continue to hit new highs and were up 15% year-over-year in our core brands, and the percentage of bookings coming through our apps was up 300 basis points sequentially versus the first quarter. We know that members with the app have the best economics, which is why we have been so focused on growing this segment of customers."

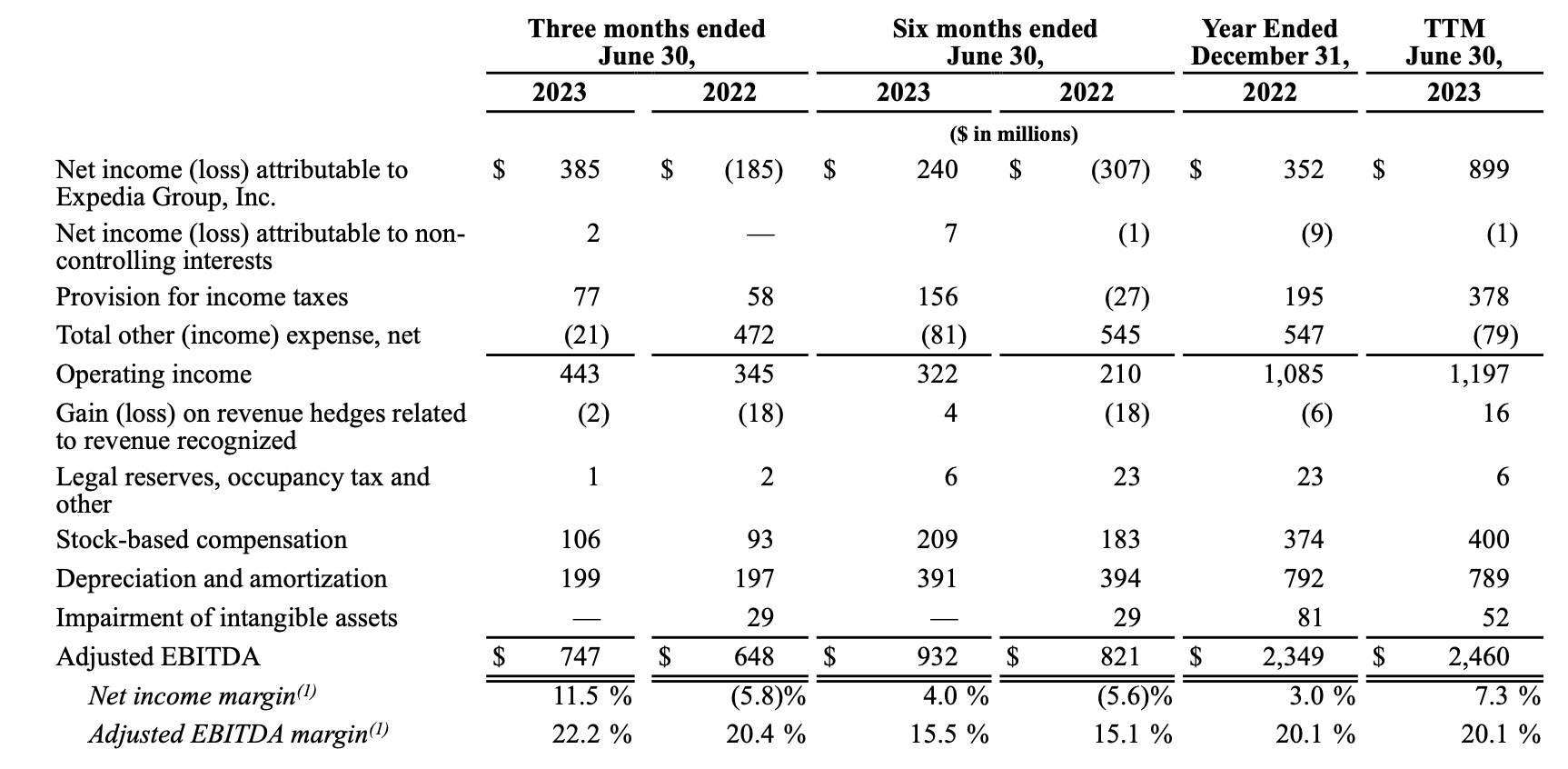

We have seen the benefit of deferred marketing spend show up in earnings. Expedia's adjusted EBITDA grew 15% y/y to $747 million, and represented a 22.2% margin - 180bps better than the year-ago quarter.

{kind=link}

Pro forma EPS also soared 47% y/y to $2.89, well ahead of Wall Street's more modest expectations of $2.36.

Key takeaways

Needless to say, Expedia is not a risk-free investment: however, buying into the stock at a cheap <12x P/E ratio (well below the S&P 500) is an appealing proposal. Buy strategically here, but don't get greedy and settle for quicker gains.

For further details see:

Expedia: Cracks Are Emerging, But At Least The Stock Is Cheap