XOM - Exxon Has Huge Production Upside For 2024

2023-11-17 10:21:11 ET

Summary

- Exxon Mobil and Pioneer Natural Resources announced a $59.5 billion merger, expected to close in 1H24, which will significantly increase Exxon's production volumes and revenue by 16% and 30%, respectively.

- Exxon reported strong Q3'23 results, with a focus on developing assets in Guyana and the Permian Delaware Basin.

- Exxon increased their quarterly distribution by 4% to $0.95/share and suggested 2024's share buyback program will be similar to 2023's $17.5b program.

It has been about a month since Exxon Mobil ( XOM ) and Pioneer Natural Resources ( PXD ) announced their $59.5b merger. This highly accretive merger is expected to close sometime in 1h24 and will significantly bolster Exxon’s upstream daily production volumes by 16% and total upstream revenue by 30% as well as provide margin-expanding operating efficiencies. In this report I will walk you through my analysis of Exxon’s current operations, my expectations as a combined firm, and my forward-looking FY24 estimates for the firm. Given the value added from the merger as well as Exxon’s robust shareholder returns, I provide the firm with a BUY rating priced at $107.55/share for a FY24 EV/EBITDA of 5.50x.

Operations

Exxon reported a strong q3’23 on the back of low liquids inventory and strong demand. Natural gas, on the other hand, experienced a continued price decline as inventory levels remained in the top half of the 10-year range. Refining margins were strong driven by low inventories while chemical margins weakened as a result of higher capacity and feed costs outpacing demand. Exxon CEO Darren Woods outlined in their q3’23 earnings call that the firm is actively refocusing production to cater more heavily towards liquids production from sub-65% liquids to 85% total (70% liquids, 15% LNG). This initiative will involve reducing exposure to dry gas production.

Exxon is making significant strides in developing their Guyana assets and with production at Payara coming online November 14, 2023, management is expecting production capacity to reach 560mboe/d. Payara (220mboe/d) is Exxon’s third offshore oil development on the Stabroek Block with the other two being Liza 1 (120mboe/d) and Liza Unity (220mboe/d). Upon further development of the block, Exxon anticipates production to reach 1.2mmboe/d by the end of 2027. Further production of their fourth and fifth projects, Yellowtail and Uaru, are expected to each produce 250mboe/d. As referenced in my article covering Hess and Chevron, Exxon owns 45% interest in the Stabroek Block with Hess owning 30%, and CNOOC Petroleum owning the remaining 25% interest. Given this breakdown, production attributable to Exxon will be 252mboe/d.

Domestically, Exxon continues to focus on developing short-cycled wells in the Permian Delaware Basin. Total production in this basin sums to 274mboe/d, or 250mbbl/d of crude and 400mcf/d of natural gas. Accordingly, Exxon runs 17 rigs in the Permian basin with six frac crews. For their ESG strategy, all of their rigs are electrified and one frac crew is fully electrified and is actively securing electricity for the remaining crews.

Downstream Operations

Exxon has a large downstream footprint that accounts for 65% of net earnings using TTM figures for q3’23. The downstream chemicals segment may be facing a painful 2024 as polymers production remains high with slightly suppressed demand ( please read my article on LyondellBasell (LYB) for further industry analysis). On the flipside, refined products such as aviation fuel have balanced out the lower realized gasoline prices. Long-term, Exxon is aiming to bolster earnings across their downstream segments by $10b through 2027 by implementing strategic projects and through structural cost reductions. Much of the mix includes renewable fuels and biofuels with 12 projects under development. Since 2019, Exxon has reduced their refinery footprint from 18 to 13 with 85% of refining capacity integrated with their chemicals segment. The firm is in the process of increasing capacity integration to reach 90%. In addition to building out performance chemicals, the firm is focusing heavily in developing advanced recycling feed capacity with 12 projects under development globally. Chemicals is expected to account for $3.5b of the 2027 earnings growth. $1.5b earnings growth will derive from specialty products.

Transport

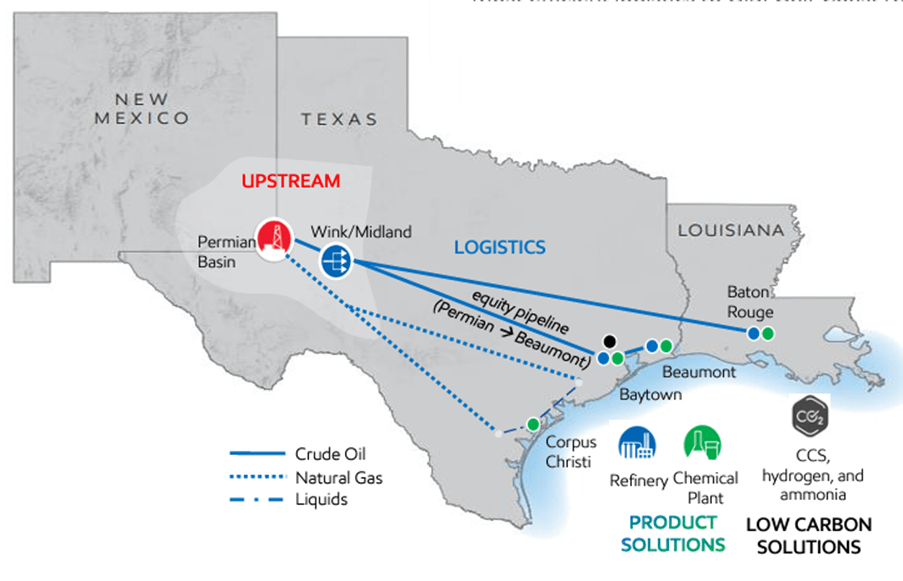

To tie it all together, Exxon has a significant footprint of equity ownership in intrastate pipelines from the Permian to the US Gulf Coast, including the 650mile, 1mmbbl/d capacity self-operated Wink to Webster Pipeline System.

{kind=link}

M&A

Exxon closed the acquisition of Denbury on November 2, 2023, in a transaction valued at $4.9b in an all-stock deal. This acquisition was designed to bolster Exxon’s long-term decarbonization strategy as the firm acquired 1,300miles of CO2 pipeline network in the US with access to 15 CO2 injection sites with capacity of 100mm metric tons of CO2 sequestering per year. In addition to these operations, the acquisition also included 46mboe/d of production with 200mmboe of reserves across Denbury’s Gulf Coast and Rocky Mountain operations.

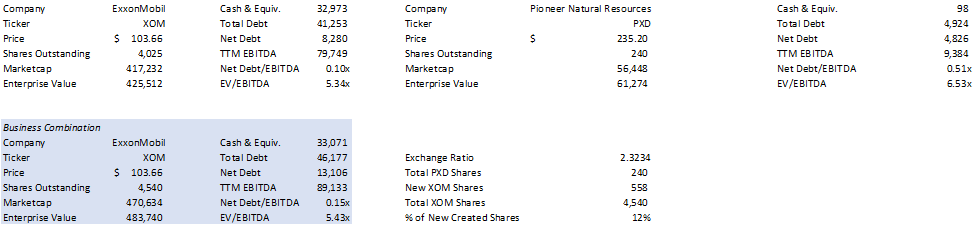

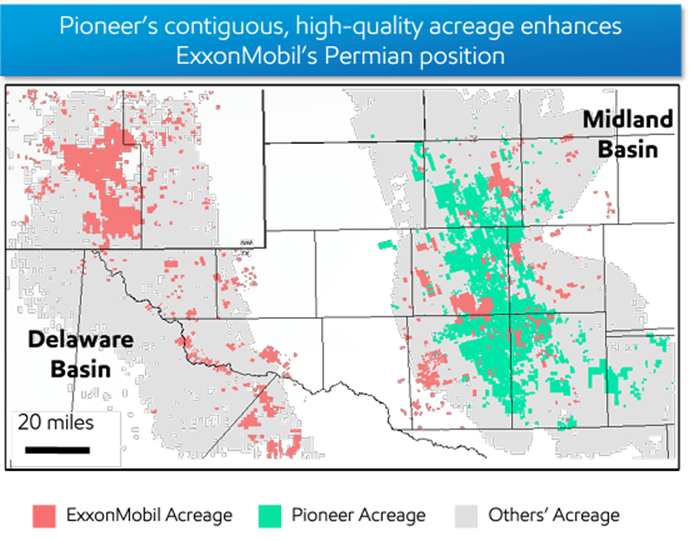

Pioneer Natural Resources was the latest announced merger by Exxon for a value of $59.5b in an all-stock transaction, dated October 11, 2023. Each PXD shareholder will receive 2.3234 shares of XOM at the close of the deal. The acquisition will double Exxon’s Permian footprint, creating the largest tier-1 domestic oil reserve to date. The merger includes 850,000 net acres in the Midland Basin, combining Exxon’s 570,000 net acres in the Delaware and Midland Basins for a total undeveloped reserve of 16mmboe. Exxon anticipated production volumes to double to 1.3mmboe/d based on 2023 figures and expects to increase production to 2mmboe/d by 2027. Combining the properties will allow Exxon to drill longer lateral wells, suggesting up to 4 miles, resulting in fewer wells for larger production volumes.

Pioneer’s assets are some of the highest quality assets in the Permian Basin, producing 78% liquids of the 721boe/d produced in q3’23.

{kind=link}

Considering the financial position, Pioneer will be highly accretive to Exxon’s financial position with their strong operating performance. Pioneer will add nearly 30% to Exxon’s upstream revenue and increase daily production by 16%. Considering margins, Pioneer’s EBITDA will contribute 11% to the combined firm’s EBITDA and increase Exxon’s margin from 22% to 24%. Considering the estimated first year synergies of $1b run rate along with the estimated $2b run rate over the course of the next decade, margin effects should be expansionary and bolster Exxon’s realized value. This is expected to be achieved with $1.3b in additional revenue from the increased 1mmboe/d in production and $700mm in 15% development cost reductions. Exxon plans to save on development costs by bringing their cube development strategy with an anticipated 30-50% higher NPV as a result.

{kind=link}

As of FY22, Pioneer’s assets were valued at $38,392mm using the standard PV10 analysis.

{kind=link}

It will be tough seeing Pioneer leaving the public markets as an independent company. They were one of the first firms to put their foot down in managing production volumes as well as one of the first firms in the industry to implement the fixed plus variable dividend policy based on free cash flow. YTD, the firm has paid out $2,527mm in dividends with 67% of the dividend being comprised of the variable rate.

{kind=link}

Considering the business combination based on q3’23 figures, the combined company will have an enterprise value of $488b for a combined TTM EV/EBITDA of 5.48x using TTM figures. Do note, the combined firm’s share count includes both shares issued to PXD shareholders and nets out the remaining $4.4b buybacks remaining for FY23.

Reserves

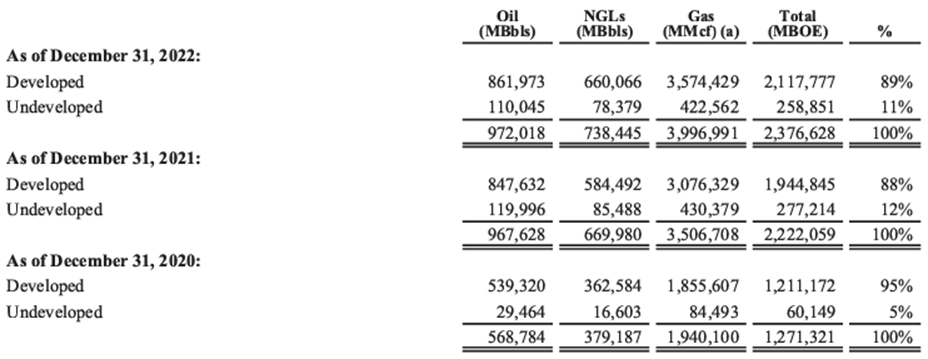

As of FY22, Exxon has a total of 17.7Bboe of proved reserves, 37% (6.6Bboe) of which are undeveloped. During the year, Exxon invested $12.1b in exploration and added 1.4Bboe of proved undeveloped reserves to their book as the firm further explored and increased discoveries in the US and Guyana. Guyana currently has an estimated 11Bboe of reserves with 4.95Bboe attributable to Exxon’s 45% share.

Domestically, the acquisition of Pioneer Natural Resources will increase acreage by 856,000 net acres, bolstering Exxon’s 570,000 net acres across the Delaware and Midland Basins for a combined reserve of 16Bboe, 75% of which are liquids. As of FY22, 65% of Exxon’s proved reserves were liquids with 40% specific to oil. Based on their MD&A and q3’23 earnings call, Exxon is going to be refocusing their production away from dry gas and into more liquids-rich basins. Given that the firm has eliminated all gas flaring in the Permian Basin, pulling back on dry gas production may relieve gas storage and allow prices to reverse course higher. Given the consolidation occurring across the industry, this strategy may be utilized by others as acreage is combined and OPEX is reduced.

{kind=link}

Looking Forward

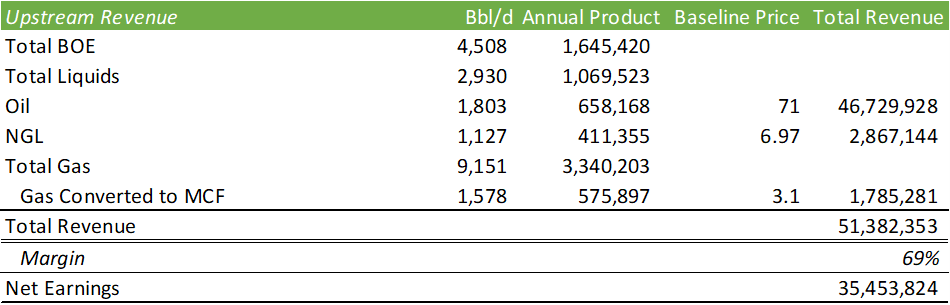

Given how diverse Exxon’s operations are, it will be challenging to perfectly model their future operating estimates. By cherry-picking upstream data and baking in constant values in energy, refining, and chemicals, we can somewhat come up with an estimate of what 2024 is going to look like. My baseline presumption is that petrochemicals isn’t set to recover for another year out as global production appears to remain at a standstill. Assuming Exxon retains Pioneer’s 721mboe/d production as well as adding Exxon’s 45% share of the 220mboe/d addition in Guyana, we can expect daily production for FY24 to be ballpark 4,508mboe/d, holding all else equal. Assuming a constant $71/bbl crude oil and $3.10/mcf based on CME futures pricing and a constant net margin of 69% (TTMq3’23 margin), we can come up with $51b in total upstream revenue. This assumes Exxon’s historical breakdown of 65% liquids production, 40% of total production being oil, and the remainder being gas.

{kind=link}

Holding all else equal, we can expect total revenue to come to $365b, net earnings of $54b, and EBITDA of $88b, assuming the merger’s accretive EBITDA margin of 24%. Though this would be a slight pullback from the combined company’s TTMq3’23 EBITDA, the average price per barrel is anticipated to be lower throughout 2024, as reported by CME Group, when compared to 2023 prices. Of course, these figures may change as economic developments are updated throughout the next year, whether we experience a global economic turnaround, debottlenecking in the polymers space, or an oil price-spiking event. These figures are just the baseline based on the present information.

Shareholder Value

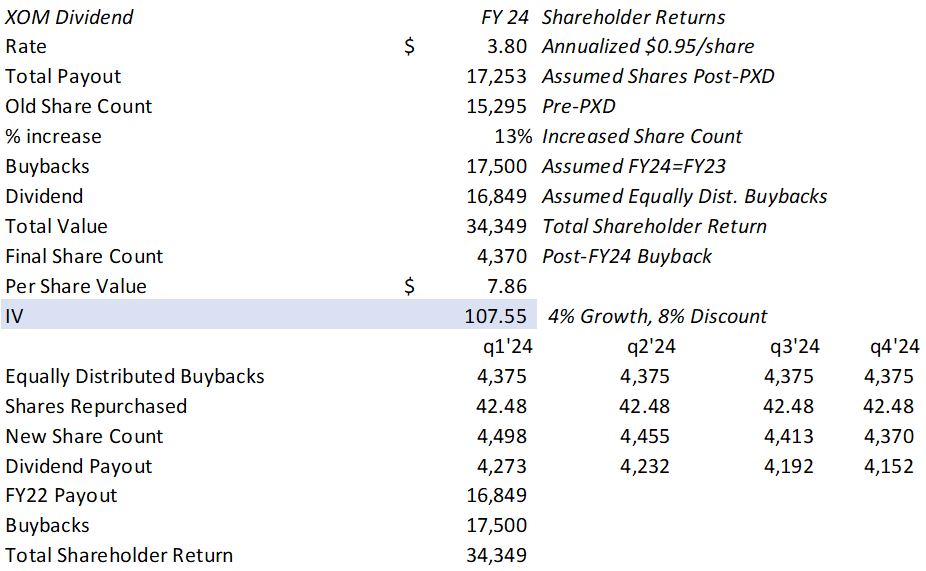

Exxon increased their quarterly dividend by 4% to $0.95/share at the end of q3’23. The firm also announced that they are on track to completing their $17.5b share repurchase program by the end of the fiscal year with the expectations of a similar program going into 2024.

Including the new share count of 4,370mm shares outstanding, as a result of the XOM/PXD and annualizing their increased dividend of $0.95/share, Exxon is expected to pay out $17,253mm in dividends in FY24 (holding constant shares outstanding and not accounting for buybacks). This would be a 14% increase in dividends issued using the new share count. Assuming the firm repurchases $17,500mm shares throughout FY24 in equal amounts throughout the quarter and using the share price of $103/share, this figure will look closer to $16,849mm, assuming no additional stock issuances through acquisition are made. With these presumptions, the total shareholder return between both dividends and buybacks will result in $34,349mm returned to shareholders (not including any discount rate).

{kind=link}

Considering the massive amount of shareholder value Exxon brings to the table, I provide XOM a BUY recommendation with a price target of $107.55/share for a forward EV/EBITDA of 5.50x. Because the deal value is now known, PXD shares will trace XOM shares until conversion and purchasing one or the other shouldn’t make a significant difference. The only pending argument is whether the deal is blocked by antitrust. My money is on the deal goes through and the combined firm realizes their exceptional production synergies in the Permian Basin.

For further details see:

Exxon Has Huge Production Upside For 2024