FSLY - Fastly: A Contrarian Bet

2023-03-23 11:12:30 ET

Summary

- Fastly has been left for dead, with the stock down more than 80% from its highs.

- Fastly's investment thesis is not without blemishes. For one, it carries more than 35% of its market cap as convertibles on its balance sheet.

- On top of that, Fastly's operations are focused on a concentrated few customers.

- However, Fastly today is working to cut back on excess costs and reach EBITDA breakeven in the coming year.

Investment Thesis

Fastly ( FSLY ) is a content delivery platform. With its stock down more than 80% from its highs, this means that everyone has lost their enthusiasm for this stock. I know this. You know this. And management knows this.

That's why during its recent Q4 earnings call , management stated the term "efficiency" more than 15 times. Could 2023 be Fastly's year of efficiency?

Fastly wants investors to get on board with its vision that it can dramatically improve its profitability profile in the next twelve months.

Given the lack of passion investors have for its shares today, I believe that this is an attractive contrarian bet.

Fastly's Story is About to Change

Fastly is a network infrastructure company. Fastly provides the technology to speedily distribute digital content. For certain companies, faster-loading websites reduce user friction, which ultimately drives revenue.

There are several problems facing Fastly's story.

- There's the obvious consideration that its growth rates are nowhere near in line with those of a fast-growing company.

- There's also the fact that its business model is highly concentrated around a few key customers. More specifically, its 5 largest customers generated 26% of its revenues. So you can understand that Fastly will not have any pricing power in that case.

- Also, Fastly has about $735 million worth of convertible debt on its balance sheet, roughly equal to 37% of its market cap. Given that Fastly's cash and equivalents position is approximately $510 million, there's a shortfall, which adds yet another complication for investors to be mindful of.

All that being said, for their part, Fastly is aware of those factors and is rapidly moving its business towards controlling costs and managing its spend to get the business close to breakeven even in the coming two years.

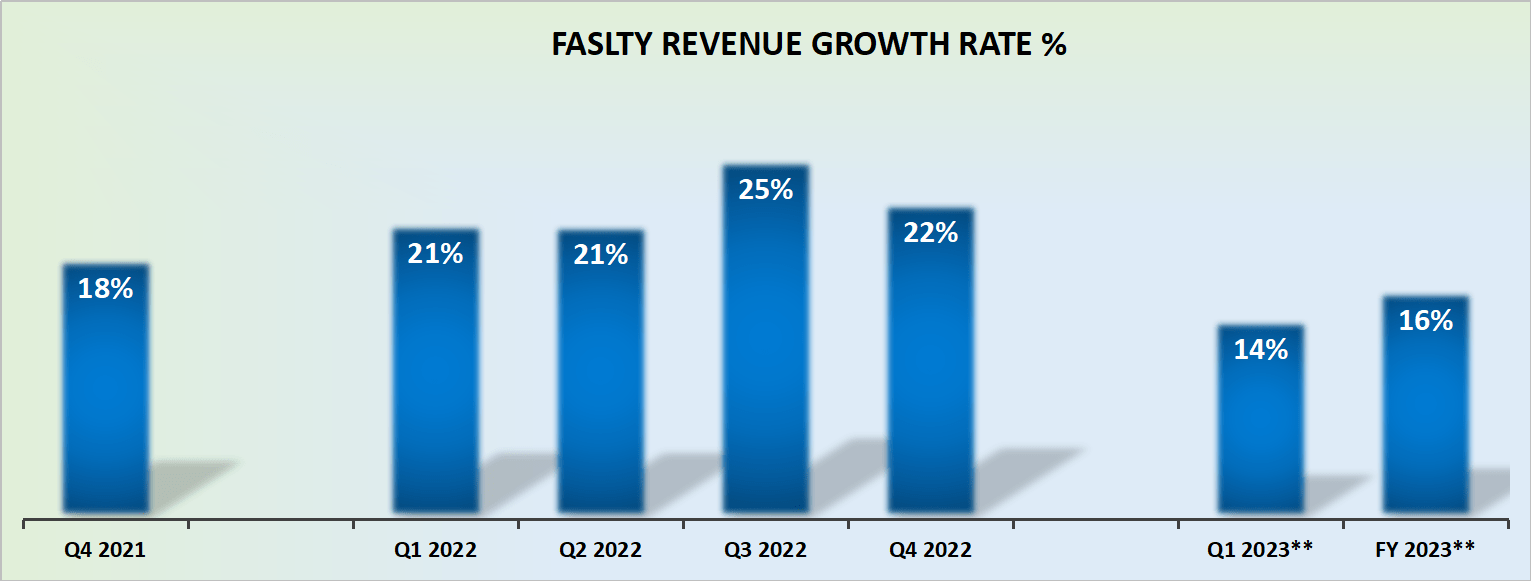

Revenue Growth Rates Lose Steam

{kind=link}

The thing with high-tech businesses is that you are either growing rapidly or you are dying. And companies that are growing at under 20% CAGR and are unprofitable are very unappetizing to investors.

This consideration led all "growth" investors to exit the stock. Meaning that the investors that are left are now unlikely to sell.

At this juncture you'll say, I get all this Michael, so, why is this a contrarian bet? Here's why.

Where the Bull Case Can be Found

Fastly spent significant time on the earnings call, highlighting that it's on the path towards breakeven over the next 12 months. Here's a quote

[W]e expect to continue to see accretion and improvement in our gross margins. We expect that to continue beyond 2023 and our efforts to drive leverage and operating expenses, once or just the efficiency, things we've spoken about, will continue to bring down, OpEx as a percent of revenues. So that's generally the trajectory that gives us high confidence in getting to that breakeven point.

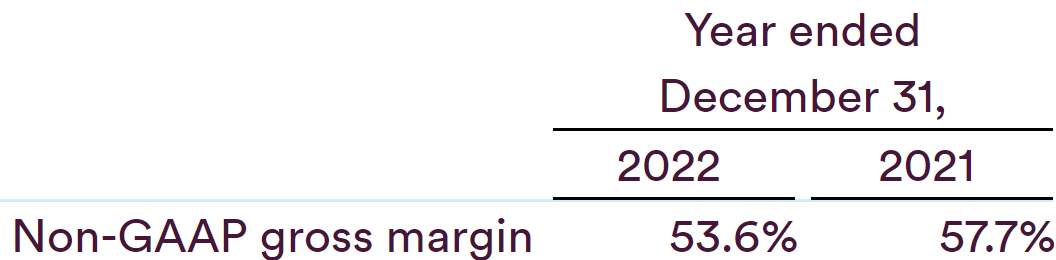

Simply put, Fastly's message is that its cost structure will improve significantly this year. More specifically, Fastly will be able to get its non-GAAP gross margins "within striking distance" of 60% for 2023.

Also, recall that FSLY's operations are seasonal, as customers increase their usage when they need more capacity during busy periods, especially in Q4 of each year.

Consequently, it's important to think about the year as a whole, rather than just looking at Q4 and extrapolating.

{kind=link}

As you can see above, if FSLY does indeed end up "within striking distance" of 60% gross margins , that would be a small improvement from 2021 but a massive improvement from 2022.

Its guided 60% non-GAAP gross margin would come just shy of the peak in 2020. However, recall that in 2020 its share price was also at least 600% higher than it is today.

The Bottom Line

Fastly is in the process of turning around its operations. My thesis points to a change in narrative. Today, few investors would seriously consider FSLY. Indeed, there's very little in its fundamentals that one can point to in order to substantiate a position in this stock.

But I believe that if one looks ahead over the next twelve months, to the time when Fastly's message will be around reporting positive EBITDA, at that time investors will be repricing FSLY higher than it is today.

In sum, for now, its stock is still attractively priced relative to its potential over the next 12 months.

For further details see:

Fastly: A Contrarian Bet