FSLY - Fastly: Another Quarter Same Issues

2023-11-02 11:21:06 ET

Summary

- Fastly's third quarter results suggest ongoing issues, despite an expectation of an improved demand environment.

- Customer concentration, weak customer growth and a lack of operating leverage are ongoing concerns for Fastly.

- Fastly's stock now appears fully valued and could come under pressure if growth falls from current levels or margins fail to improve.

Earlier in the year I suggested that the market was too negative on Fastly's ( FSLY ) prospects as pandemic related demand headwinds were moving into the rearview mirror. While Fastly's stock has moved significantly higher since then, it remains a company with serious issues and third quarter results suggest that these issues are not going away. This is concerning as the demand environment is supposed to be improving and Fastly has been actively working to improve its gross profit margins and accelerate customer acquisition over the past year.

Market

Market commentary on the third quarter earnings call was surprisingly pessimistic. Customers are still tightening their budgets, which is contributing to vendor consolidation. Fastly believes that this is a positive though, as its position as a performance leader tends to result in share gains. Some deals are also taking longer to close as they are receiving more scrutiny. Fastly saw several key deals slip out of the third quarter, although this was not material. These types of observations have been common across software companies over the last 12 months, but there has been a growing consensus that conditions were improving. Fastly's results and guidance suggest that headwinds are ongoing.

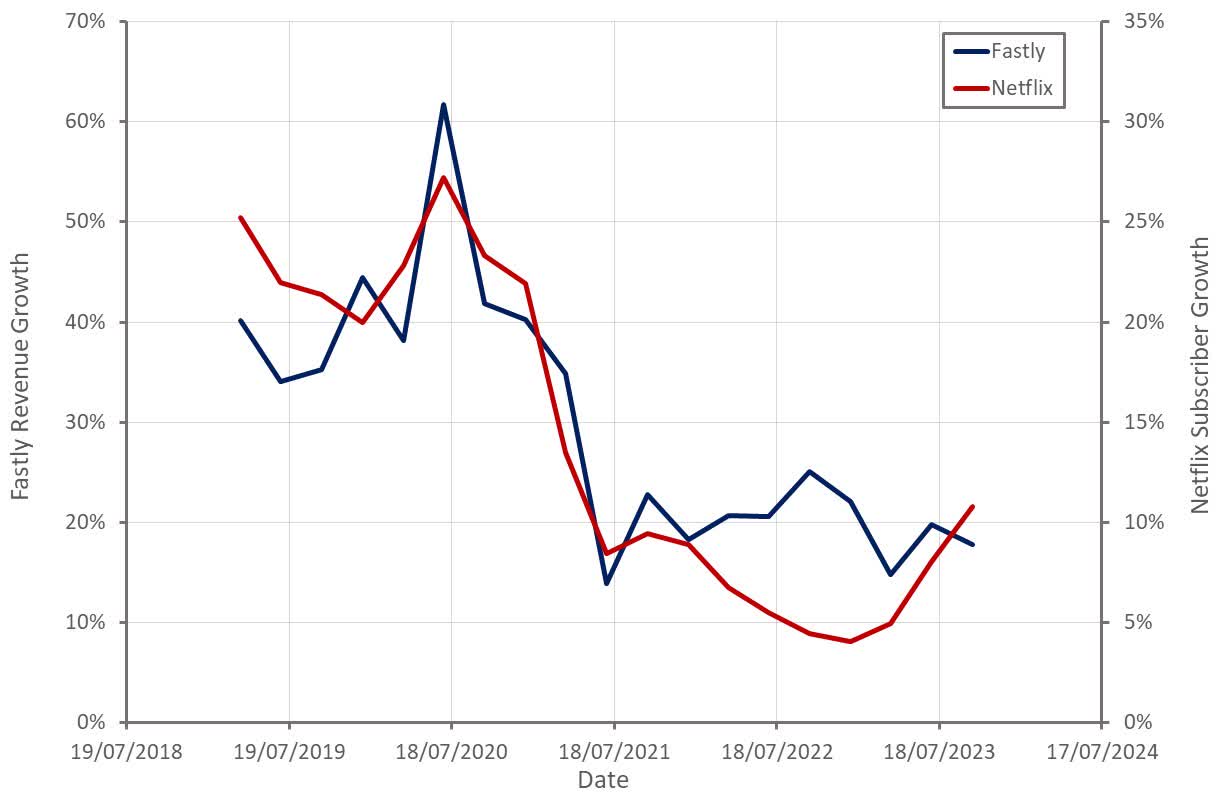

This is somewhat surprising given a return to more normal internet traffic growth in the wake of the pandemic, particularly in areas where Fastly has exposure, like media and ecommerce. The reacceleration in Netflix’s ( NFLX ) business is suggestive of the headwinds that continue to plague Fastly. Netflix subscriber growth should be indicative of broader video-on-demand traffic trends. Video on-demand is a key market for Fastly as performance is paramount to customers. While Netflix’s growth is picking up, Fastly’s growth still appears to be falling off.

{kind=link}

Figure 1: Fastly Revenue Growth and Netflix Subscriber Growth (source: Created by author using data from company reports)

Fastly

Fastly's product portfolio has expanded over the past few years, but the platform still appears to only really appeal to large companies with high performance requirements. Delivery remains the backbone of Fastly's business, although its security business is growing rapidly. Fastly's compute product doesn't appear to have gained much traction so far.

Fastly has stated that its customers are still experimenting with compute. Cost has been a roadblock to adoption in this area, as indicated by the fact that when Fastly launched the package with fixed pricing it saw a significant increase in customers using its compute service. The deployment of AI is expected to be a tailwind for edge networks, but Fastly thinks that any material revenue is still 12-15 months away, with benefits primarily accruing to its compute business.

Fastly’s security business is largely focused on web application security. The company now has a DDoS solution and a bot protection service that is currently in beta. Given the focus of Fastly's business, a narrow security portfolio is not a large issue, but it may limit mass adoption of the platform.

Fastly is also introducing products in areas like edge observability, DNS management (through its Domainr acquisition) and edge databases. These types of products support the delivery, security and compute businesses, but Fastly appears to be behind peers in many of these areas.

On the sales and marketing side, Fastly is trying to broaden adoption of its platform, which should help to support growth and improve margins. Fastly’s high-performance CDN has led to a strong position in media and entertainment, ecommerce and high-tech, and the company is now trying to drive growth in verticals like brick-and-mortar retail, travel, leisure and healthcare. A more diversified traffic load should lead to more consistent network and compute demand and hence better infrastructure utilization.

Fastly hopes to increase adoption through recent changes to its pricing structure. This initiative was started around a year ago, and Fastly believes it is having an impact. Packaging deals are growing rapidly and a substantial number of these are platform wins involving multiple product lines.

Fastly is also ramping its channel partnerships to help it reach more customers. Between June and now, Fastly increased its number of partners from 33 to 55. Partner revenue contribution has also grown more than 50% in 2023 YTD, compared to all of 2022. In particular, Fastly’s partner program is ramping internationally.

Financial Analysis

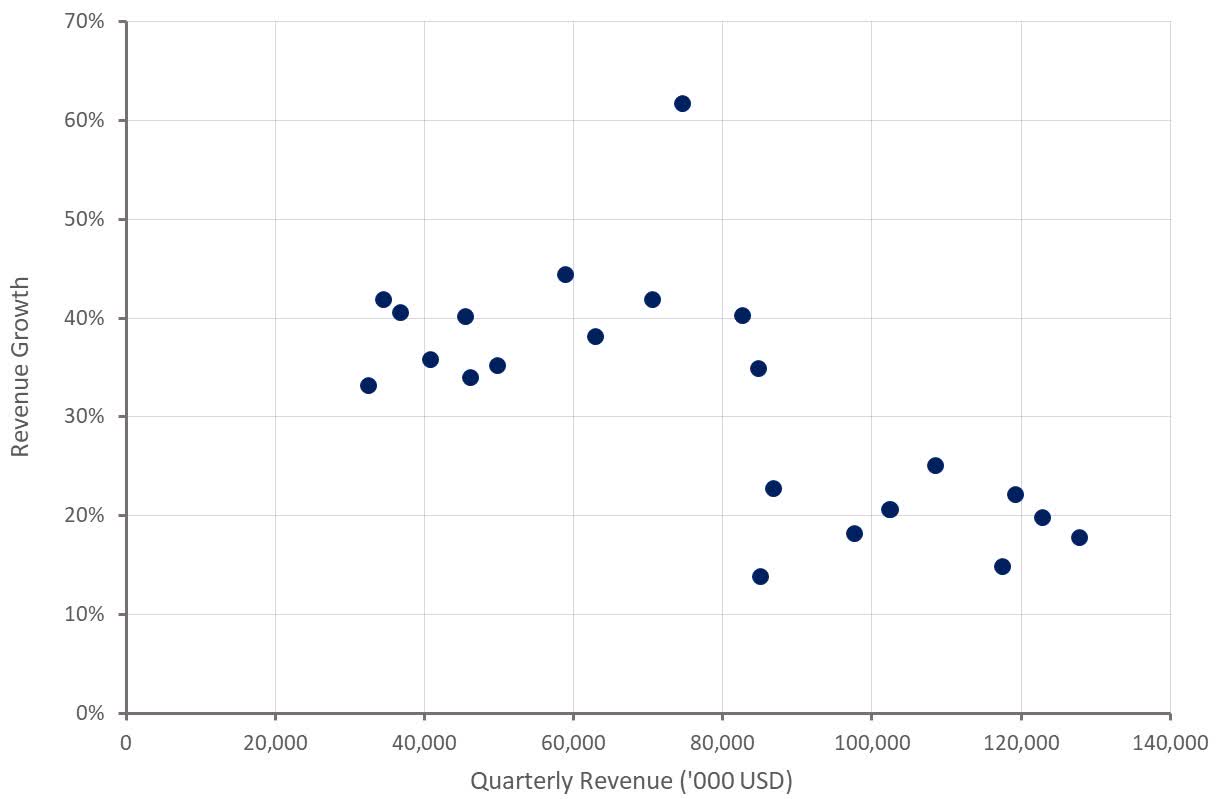

Revenue increased 18% YoY in the third quarter to 127.8 million USD, with growth driven by international traffic and expansion within existing customers. Fastly believes that CDN market growth is around 8% , with the company gaining market share over time due to the performance and ease of use of its products. Vendor consolidation has also been a tailwind for Fastly recently. One of Fastly’s larger customers consolidated its CDN providers from five down to two in the first quarter. While this is a positive, vendor consolidation also contributed to increased pricing pressure in the first half of the year.

Security continues to be an area of strength for Fastly, with Signal Sciences contributing 14% of total revenue in the third quarter and increasing revenue 33% YoY.

Fourth quarter revenue is expected to be 137-141 million USD , a 16% YoY increase at the midpoint. While this guidance is likely conservative, Fastly's revenue growth should ideally be accelerating back into the 20-25% range. Particularly as the company is gaining share within existing customers, actively trying to expand its customer base and cross selling security and compute.

{kind=link}

Figure 2: Fastly Revenue Growth (source: Created by author using data from Fastly)

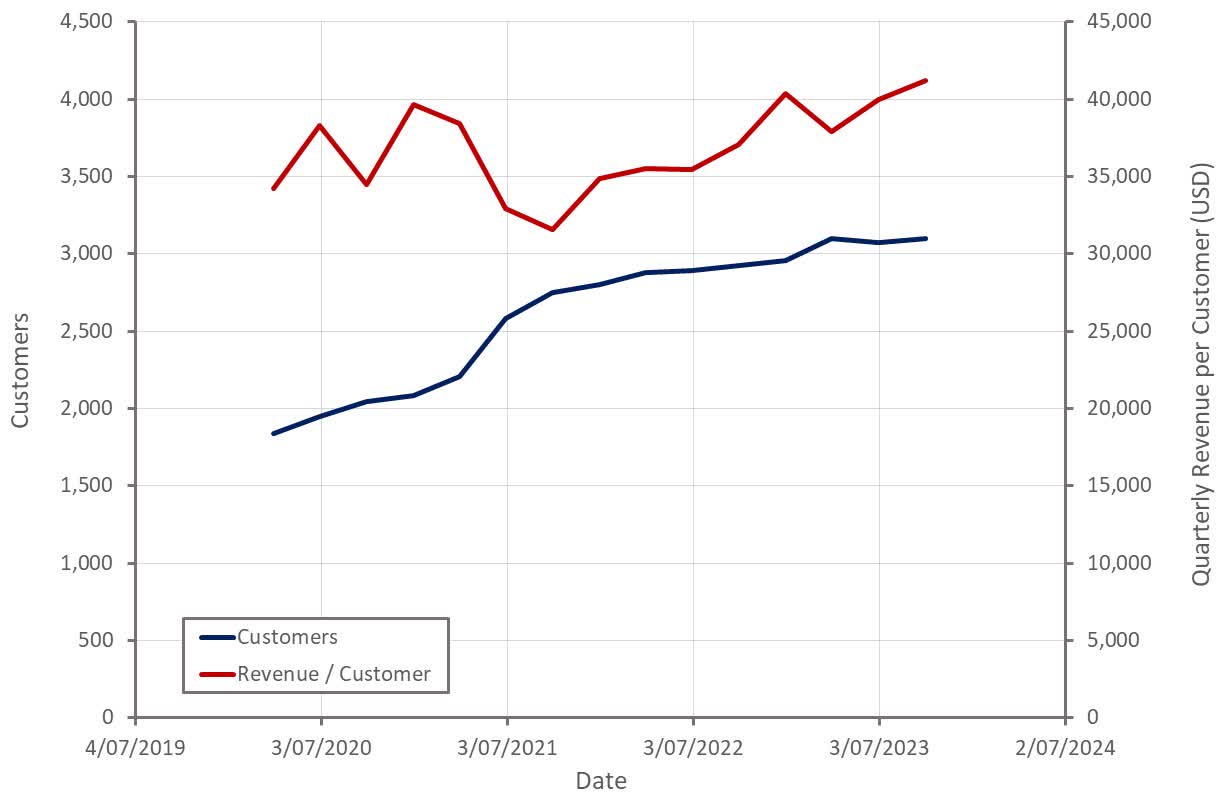

Fastly’s customer count increased by 30 in the third quarter to 3,102. I have long suggested that narrow adoption of its platform was both inherent to Fastly’s strategy and a competitive disadvantage. Fastly is trying to change this, but the third quarter again suggested that progress has been limited.

Marketing is currently focused on new logo acquisition and Fastly’s salesforce is being specifically compensated for new logo acquisition. Fastly has also introduced a new pricing structure which aims to reduce friction and increase adoption of its platform amongst smaller customers.

Fastly had 547 enterprise customers in the third quarter, a sequential decrease of four. This decrease is the result of Fastly’s new enterprise customer count methodology and weaker consumption during the quarter. Using the prior methodology, Fastly’s enterprise customer count increased by 10, which is still relatively weak.

Customer concentration continues to be an issue for Fastly, and if anything, this problem has increased over the past few quarters. Enterprise customers accounted for 92% of total revenue on an annualized basis in the third quarter. Fastly’s top 10 customers currently contribute 40% of total revenue, with one customer accounting for 12% of revenue.

NRR was down slightly in the third quarter to 114%. DBNER was 120% in the third quarter, also down sequentially. Enterprise customer average spend was up 11% YoY. Fastly has suggested that expansion is being driven by wallet share gains (in part due to cross-sell) and increased traffic. Fastly’s customer success team is being incentivized to promote cross-product adoption and platform unification is making this easier.

{kind=link}

Figure 3: Fastly Customers (source: Created by author using data from Fastly)

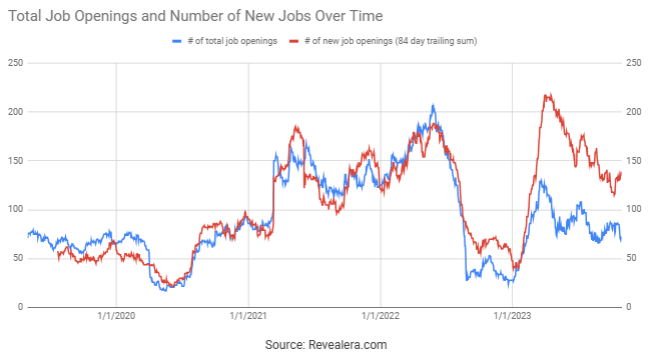

Fastly's job openings also suggest that growth is likely to remain soft going forward, as the number of job openings is down significantly since earlier in the year. The lack of operating leverage in the business over the past few quarters also suggests that growth has been softer than management anticipated.

{kind=link}

Figure 4: Fastly Job Openings (source: Revealera.com)

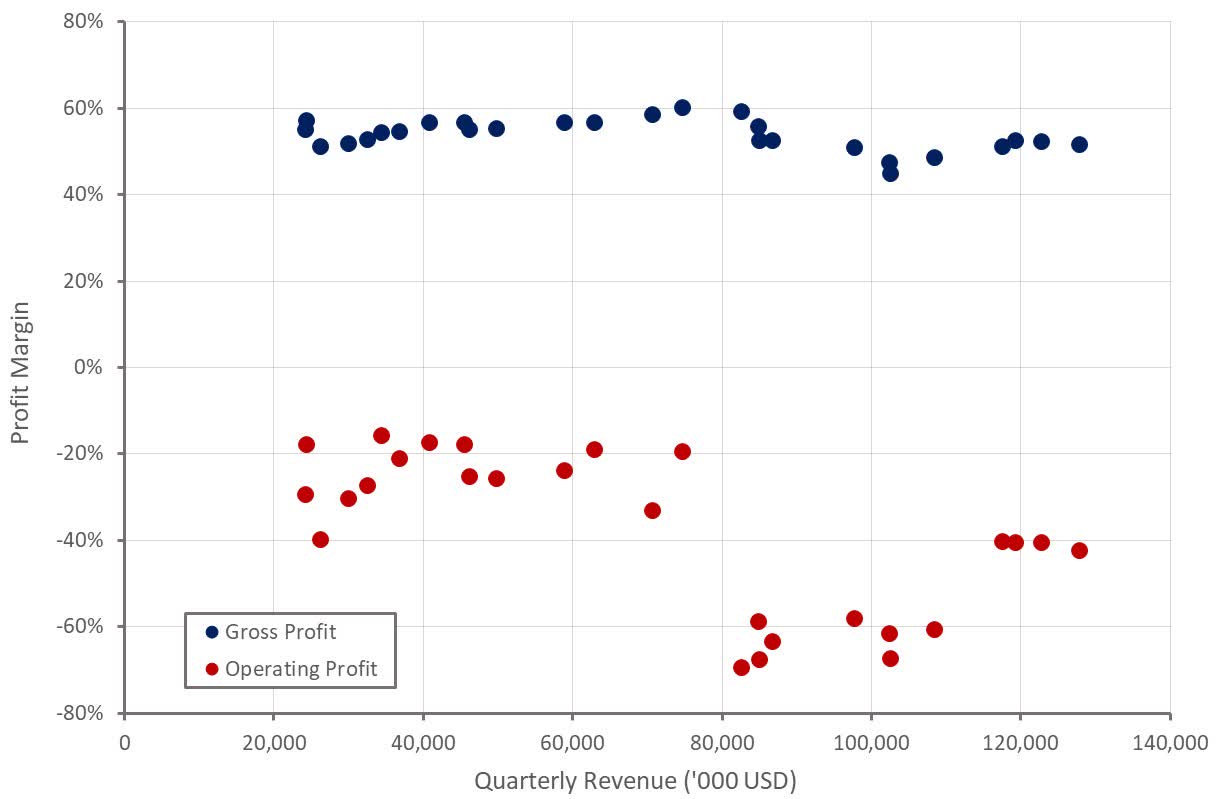

Fastly's gross profit margin was 55.9% in the third quarter. Margins were supposed to move higher as utilization of Fastly's infrastructure improved, but this process has stalled over the past year. This is more damning given that Signal Sciences' rapid growth should be a structural tailwind for margins.

Gross profit margin improvement appears to have stalled due to a combination of pricing pressure and a shift in traffic mix across geographies. Fastly has gained a lot of traffic over the past few quarters in regions where it previously had a limited presence. This has been the result of both vendor consolidation and large multinational customers successfully expanding into new regions. While this has supported growth, it has also undermined gross profit margins as Fastly’s cost structure in these regions has been high. The increase in traffic allows Fastly to peer more and negotiate better pricing on bandwidth though. Margins are therefore expected to improve but this may take time. Fastly continues to suggest that CDN margins could eventually move upwards of 60% , irrespective of higher margin value added services. This looks a long way off at the moment.

Operating expenses were 84 million USD in the third quarter, with the YoY decline driven by cost discipline. Increased sales and marketing spend in the third quarter was attributed to one-time events and fees. The lack of operating leverage in Fastly's business should be a cause of concern for investors. R&D spend can be explained by investments in expanding the company's product portfolio, but elevated sales and marketing spend isn't justified by the company's weak growth. Fastly is now trying to leverage channel partners to increase sales efficiency, particularly as the company tries to reach more into the mid-market.

{kind=link}

Figure 5: Fastly Profit Margins (source: Created by author using data from Fastly)

Valuation

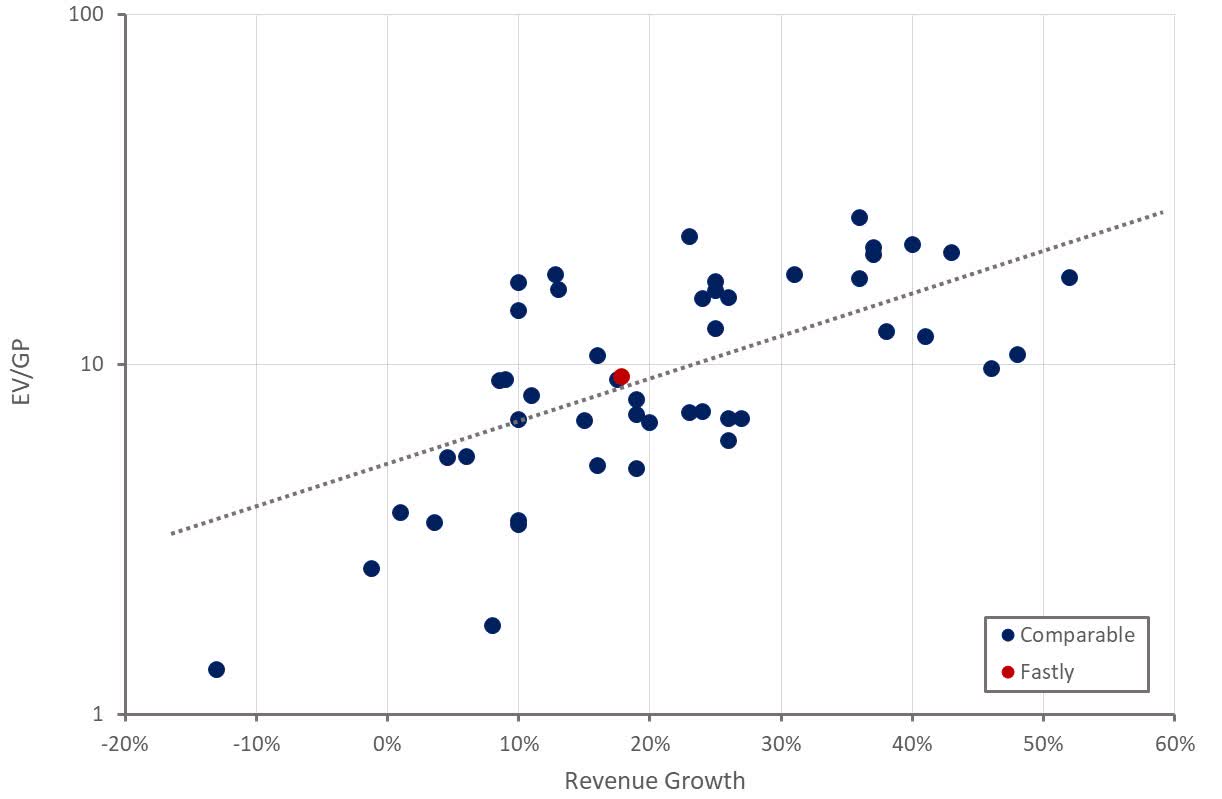

Based on its current growth rate and profitability, Fastly appears to be valued broadly in line with comparable companies. Based on a discounted cash flow analysis I estimate that Fastly's stock is worth approximately 12 USD per share. Given Fastly’s relatively large losses, and lack of progress towards profitability, I wouldn’t consider an investment in the company though, regardless of valuation.

While Fastly's stock responded positively to third quarter earnings, there were many areas of concern. Fastly needs to find a way to increase its customer count and generate more operating leverage. If growth decelerates further going forward, Fastly's stock is likely to come under pressure again.

{kind=link}

Figure 6: Fastly Relative Valuation (source: Created by author using data from Seeking Alpha)

For further details see:

Fastly: Another Quarter, Same Issues