FSLY - Fastly: Attractively Priced Amid Solid Turnaround

2023-09-05 12:44:43 ET

Summary

- Fastly, Inc. stock is reasonably priced at around 6x forward sales, making it an appealing entry point for investors.

- Fastly is strategically positioned to play a pivotal role in the AI-driven future, leveraging AI technology to deliver fast, safe, and engaging user experiences.

- While revenue growth rates may not be exceptional, Fastly's focus on profitability and cash flow positivity is evident, despite challenges related to its balance sheet. The stock is attractively priced.

Investment Thesis

Fastly, Inc. ( FSLY ) is attractively priced while undergoing a solid turnaround. As you'll read, an investment in Fastly is not blemish-free. There are different considerations that keep me wary.

Perhaps the most weighty is the pace of its customer adoption curve. That being said, I believe this consideration is already reflected in its valuation.

Therefore, I continue to be bullish on this stock and believe that paying 6x forward sales is an attractive point for new investors to get involved with this stock.

Rapid Recap

In my previous bullish analysis titled "Resurging As A Promising Investment Opportunity," I plainly described this opportunity as such

Yes, [Fastly's] aren't the revenue growth rates that are congruent with a fast-growing business, but at the same time, I don't believe that anyone looking at Fastly today is expecting much from Fastly either.

Author's performance

I stand by those comments. Few investors getting involved with Fastly have high expectations for this business. And therein lies its opportunity.

Why Fastly? Why Now?

Fastly is a company that operates as a content delivery network ("CDN"), and its main job is to make the Internet faster. They have a special cloud-based infrastructure that helps businesses speed up the delivery of their content over the internet. The way they do this is by storing copies of websites and other online content closer to where people are trying to access them. So, when you visit a website or use an app, instead of that information having to travel a long way across the internet to reach you, Fastly's technology brings it to you from a nearby location. This means you get to see web pages, videos, and other online stuff quicker because it doesn't have to travel as far. Big websites, like those of media companies or online stores, use Fastly to make sure their content loads fast and works reliably for all their users.

In simple terms, Fastly is like a super-fast mail delivery service for the Internet. It takes websites and content and brings them closer to you so that everything loads and works smoothly, especially when lots of people are trying to access it at the same time. This helps websites run better, and it makes your online experience faster and more enjoyable.

One noteworthy aspect of Fastly's recent direction has been its embrace of AI technology. The company describes its commitment to leveraging AI through its edge cloud infrastructure, positioning itself to play a pivotal role in the AI-driven future. Fastly showcases its ability to run AI inference on its platform, with a vision for generative learning models predominantly running in the central cloud. This forward-looking AI strategy is expected to have a transformative impact across various industries.

In particular, Fastly illustrates how AI could revolutionize sectors like e-commerce, media, and high-tech, bringing about low-latency, personalized, and accurate recommendations, sentiment analysis, computer vision applications, and more. Fastly's promise to deliver fast, safe, and engaging AI-powered user experiences captures the essence of its strategic vision.

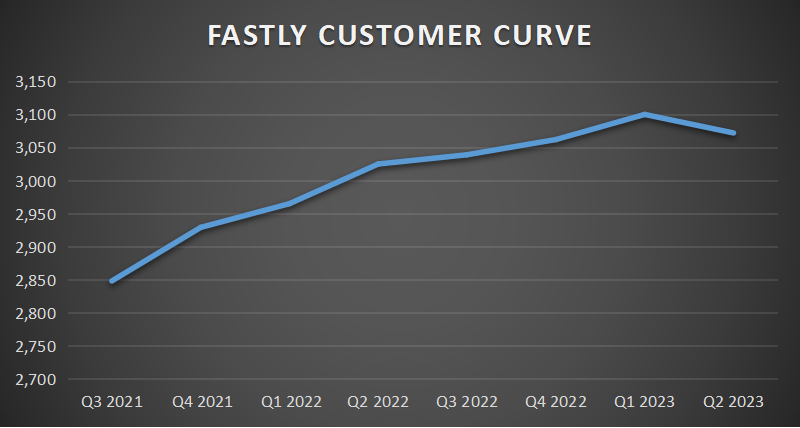

One negative consideration that surfaced from this last set of results is reflected in the following chart.

{kind=link}

Anyone who follows my work will know that I'm obsessed with customer curves. A strong increase in total customers, irrespective of the revenue growth rate, and the business will do well. And vice versa. Accordingly, I'm keeping a watchful eye on this progress in the following quarters and leave myself open to changing my mind from my bullish rating here.

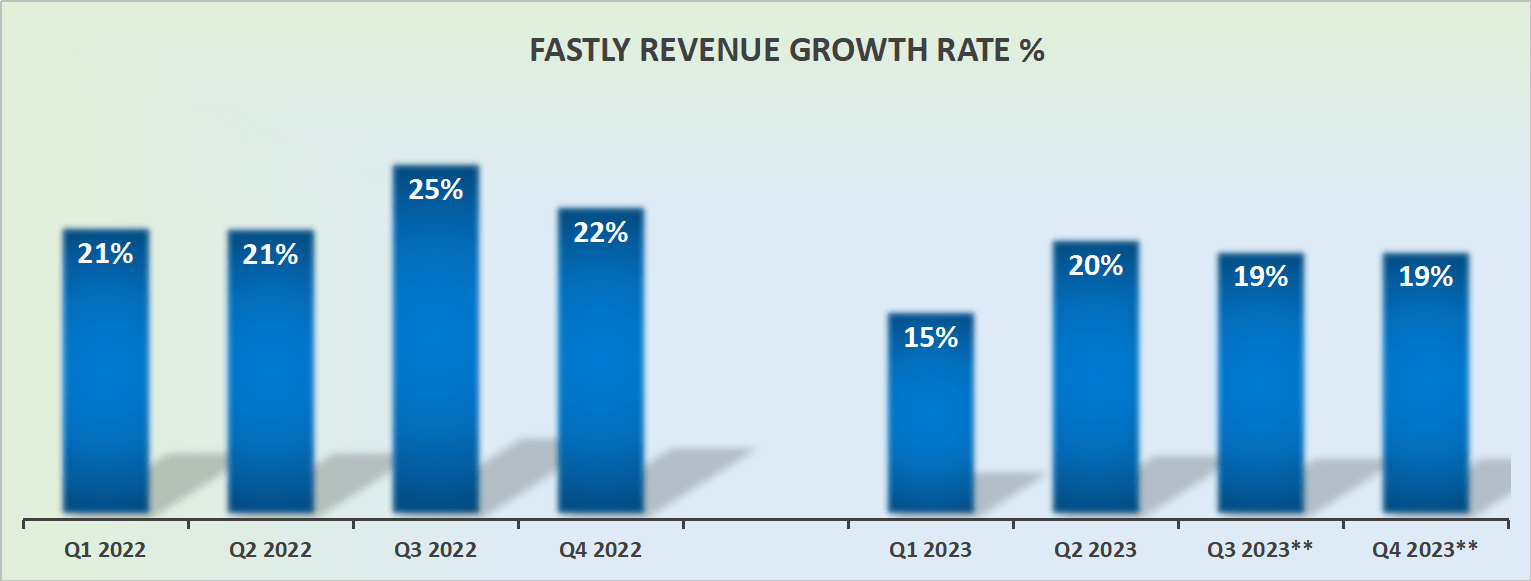

Revenue Growth Rates Ticking Along

{kind=link}

As I've already made clear, Fastly is no longer a fast-growing business. And that's OK too . Why?

Because with less quarterly growth, Fastly can turn more of its focus on improving its profitability. And that's one aspect of this investment thesis that sorely needs attention and substantial improvement.

Profitability Profile Continues to Weigh on Fastly

As I noted in the previous analysis, the bear case facing Fastly is that this business hasn't succeeded in making its business strongly profitable.

As a consequence, Fastly's balance sheet is the Achilles heel of this investment thesis. Fastly is unprofitable on a GAAP and non-GAAP basis, but it does succeed in being cash flow positive, which I believe is the single most important measure of the sustainability of a business, albeit Fastly is barely cash flow positive.

That being said, Fastly ended Q2 2023 with a net neutral balance sheet. This is a fancy term for when the cash and debt roughly balance each other. This means that although Fastly does carry approximately $470 million of debt, it also has approximately $470 million of cash and equivalents, which will in time be used to pay off its debt.

Case in point, during Q2, Fastly repurchased $236 million in convertible debt at a 17% discount to par value. In other words, Fastly is working towards tackling its balance sheet and improving it. However, because Fastly still has a significant amount of debt, it will be unable to leverage its balance sheet further with additional borrowings and make a bid for a substantial and meaningful acquisition.

FSLY Stock Valuation -- A Fair Entry Point

Fastly's multiple has compressed significantly in 2022. And now, despite financial conditions starting to ease up, Fastly multiple is still down from its highs.

In sum, I don't believe that paying 6x for Fastly is a rich multiple. Yes, the investment thesis is evidently not blemish-free. And there's still a lot of progress to be made, for instance in improving its profitability profile. But altogether, I believe this stock provides an attractive risk-reward opportunity.

The Bottom Line

Fastly, Inc. has undergone a solid turnaround, but certain considerations have left me with lingering doubts. The pace of its customer adoption curve remains a significant concern, albeit one that appears to be priced into its valuation. Despite these uncertainties, I find myself leaning toward a bullish perspective on this stock. Paying 6x forward sales seems like an enticing entry point for new investors, especially given that few have high expectations for Fastly at the moment.

The recent highlight of Fastly's AI initiatives adds an exciting dimension to its potential. By running AI inference on its platform and envisioning generative learning models in the central cloud, Fastly positions itself at the forefront of the AI-driven future. One noteworthy aspect is Fastly's emphasis on AI's transformative power, which could drive growth and innovation in various sectors.

While doubts linger, the attractive risk-reward opportunity makes a compelling case for considering Fastly as an investment.

For further details see:

Fastly: Attractively Priced Amid Solid Turnaround