FSLY - Fastly: Cloud Growth At A Rich Price

2023-11-13 19:57:13 ET

Summary

- Fastly's shares soared 16% after reporting better-than-expected Q3 results.

- The company beat estimates on both the top and bottom lines.

- Fastly's customer account growth and revenue growth have been slowing, but the company issued a strong outlook for Q4.

- Free cash flow profitability could be an inflection point for Fastly. However, shares of the cloud edge computing company remain highly valued.

Shares of content delivery network provider Fastly ( FSLY ) soared 16% after the company presented better than expected results for the third-quarter at the beginning of November. The edge cloud platform managed to grow its top line in the double-digits again and free cash flow losses, on a year over year basis, narrowed. In my opinion, the achievement of free cash flow profitability could be an inflection point for Fastly. The company raised its FY 2023 revenue forecast, but shares of Fastly remain expensive after they have doubled their valuation this year. As a result, I continue to rate the cloud edge computing platform as a hold.

Previous rating

I rated Fastly a hold in August due to valuation concerns: Strong Q2, But Now Expensive (Rating Downgrade) . In the third-quarter, the cloud edge computing company reported a slowdown in revenue and customer account growth, but the firm nonetheless managed to narrow its free cash flow losses. All factors considered (including the raised guidance for FY 2023), I will continue to rate Fastly a hold.

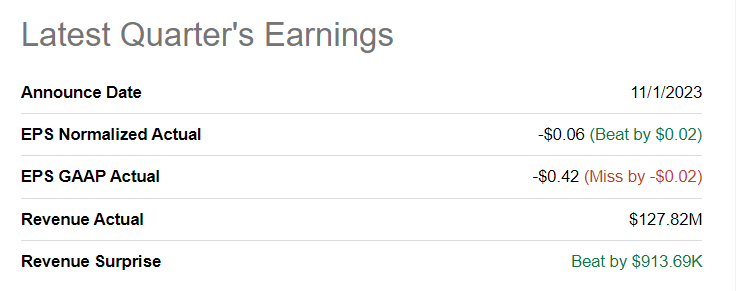

Fastly beats estimates for Q3’23

Fastly beat estimates on both the top and bottom line for the third-quarter: Fastly reported an adjusted loss of $0.06 per-share, which surpassed the average prediction by $0.02 per-share. Revenues came in at $127.8M and were $914k higher than expected.

{kind=link}

Source: Seeking Alpha

Double-digit top line growth, but slowing customer acquisition

Fastly’s revenues rose 18% year over year to $127.8M although the firm's top line growth continued to moderate in the third-quarter… a trend that started back during the pandemic. While the edge cloud computing company’s revenues were up 18% Y/Y in the last quarter, they rose 20% in Q2’23 and 25% in Q3’22.

Fastly ended the third-quarter with 3,102 customer accounts in its portfolio, including 547 enterprise accounts, which tend to be the most lucrative for Fastly. Unfortunately, Fastly lost 4 enterprise accounts in the last quarter, the first such decline in the last year. In total, enterprise accounts are still up 7% year over year, but growth is clearly slowing: enterprise customers grew at a 10% Y/Y rate in Q2’23 and 11% Y/Y in Q1'23. The decline in the customer acquisition growth rate is driven by market saturation and companies optimizing their IT spending.

Fastly's dollar-based net retention rate declined 3 PP quarter over quarter to 120%, but remained overall solid. The dollar-based net retention rate is a key performance metric for cloud companies that measures how well companies are managing, engaging and upselling customers. As such, the dollar-based net retention rate quantifies to what degree existing customers are ramping up their product-spend from one reporting period to the next. The average (unweighted) dollar-based net retention rate for Fastly in the last year was 122%, so Fastly dropped slightly below this average in the third-quarter.

| FY 2023 |

| FY 2022 |

| Fastly |

| Quarter 3 |

| Quarter 2 |

| Quarter 1 |

| Quarter 4 |

| Quarter 3 |

| Growth Y/Y |

| Total Customer Count |

| 3,102 |

| 3,072 |

| 3,100 |

| 3,062 |

| 3,039 |

| 2.1% |

| Enterprise Customer Count |

| 547 |

| 551 |

| 540 |

| 533 |

| 511 |

| 7.0% |

| Dollar-based Net Retention Rate |

| 120% |

| 123% |

| 121% |

| 123% |

| 122% |

| (2) PP |

(Source: Author)

Strong outlook for the fourth-quarter

Fastly guided for total revenues of $505-509M for the current fiscal year which represents an increase, at the mid-point, of $2M compared to the previous revenue guidance range of $500-510M. The low-end of Fastly's FY 2023 guidance was raised by $5M.

{kind=link}

Source: Fastly

Free cash flow is still negative, but the trend is favorable

Fastly achieved positive adjusted EBITDA in Q3'23, but is still not consistently profitable on a free cash flow basis which is something, in my opinion, that is holding the stock back.

Fastly generated negative free cash flow of $19.7M in the third-quarter on revenues of $127.8M. However, free cash flow losses have narrowed significantly over the course of the last year and the trend is favorable. In the second-quarter, the content delivery network actually managed to report a positive free cash flow of $7.8M. The achievement of consistent free cash flow profitability would likely be a favorable catalyst for Fastly’s shares and a major inflection point for the business.

| Fastly |

| FY 2023 |

| FY 2022 |

| $'000 |

| Quarter 3 |

| Quarter 2 |

| Quarter 1 |

| Quarter 4 |

| Quarter 3 |

| Cash flow from operations |

| ($8,390) |

| $24,990 |

| ($8,861) |

| ($12,128) |

| ($27,634) |

| Capital Expenditures |

| ($11,304) |

| ($17,237) |

| ($16,326) |

| ($17,120) |

| ($14,702) |

| Advance Payment for PPE |

| $0 |

| $0 |

| $0 |

| ($10,923) |

| ($1,964) |

| Free Cash Flow |

| ($19,694) |

| $7,753 |

| ($25,187) |

| ($40,171) |

| ($44,300) |

(Source: Author)

Fastly’s valuation

Cloud companies are trading at elevated revenue multipliers because they are valued based off of their expected future top line potential. Many software companies in the cloud space are not yet profitable (like Fastly), but have a strong revenue trajectory and are moving towards positive operating income and free cash flow.

The edge cloud platform is currently valued at a price-to-revenue ratio of 3.7X and slightly trading above its 1-year average P/S ratio of 3.3X. Valuations for competitors such as Akamai ( AKAM ) and Cloudflare ( NET ) are high as well, with the P/S ratio for Cloudflare being especially massive at 12.8X. However, Cloudflare is the highest valued company as the market expects the strongest top line growth for the firm: analysts expect 32% revenue growth for Cloudflare this year while Fastly is projected to achieve 17% growth. Since shares of Fastly have already doubled this year and the market has a tendency to overreact to Fastly's guidance raises, I believe a hold rating is prudent.

Risks with Fastly

If Fastly wants to see a higher valuation, it must address its cash burn. The company continues to add clients on a consolidated basis and the dollar-based net retention rate looks good as well, but Fastly must translate this momentum in positive free cash flow or investors are going to lose their patience with the stock. The biggest commercial risk that I see with Fastly is a potential deceleration of growth in the enterprise market which then may also translate to a weakening dollar-based net retention rate.

Final thoughts

Fastly reported a decent third-quarter that showed continual double-digit top line growth, but the cloud edge computing firm also lost some enterprise customers and we saw a small 3 PP dip in the dollar-based net retention rate which can be understood as a measure to quantify customer monetization. On the positive side, Fastly is moving closer to free cash flow profitability as FCF losses narrowed compared to the year-earlier period. However, the valuation remains stretched and it may take Fastly a while to drive its business to FCF profitability. The raised guidance for FY 2023 was positive as well, but I will stick to my hold rating.

For further details see:

Fastly: Cloud Growth At A Rich Price