FSLY - Fastly: Danger Ahead

2023-04-27 05:19:26 ET

Summary

- Fastly's stock has appreciated tremendously in 2023.

- However, the company is having trouble outrunning its operating costs.

- We believe that cost along with a lack of long-term customer commitments spells potential trouble ahead for the company.

What Goes Up

In the heady days of the zero-interest rate [ZIRP] environment, growth trajectory was a primary target among investors, with profits and cash flow often sitting a few rungs down the ladder of importance. 2022, of course, changed much of this thinking. As the Federal Reserve ramped up interest rates at a fever pace, companies which failed to generate returns on capital rapidly fell out of vogue.

Sometimes, this was warranted. After all, the marketplace is supposed to - supposed to - punish bad business models and reward good ones. Today we will examine a company that we believe offers a competitive service, but is yet unprofitable and whose stock, we believe, is likely to experience more pain ahead - Fastly ( FSLY ). Let's dive in.

Background

Fastly provides a number of services including Content Delivery Networks [CDNs], load balancing for website traffic, and image optimization. The company labels itself as part of the burgeoning Infrastructure as a Service [IAAS] field, which provides the framework for developers to deliver content to consumers.

Specifically, Fastly focuses on delivering these services through edge cloud computing. Today, an enormous amount of data is stored in physical servers at data centers located around the world. The time it can take to retrieve information from these centers can result - due to traffic volume, physical distance, et cetera - in a higher degree of latency than developers want or consumers expect. Edge cloud computing aims to counteract this problem by moving portions of the actual computing out of the data centers and to the devices or locations where end users actually are.

As an example, Fastly has published on its website several case studies of its products in action, including how the company was able to assist publishing giant Gannett ( GCI ) with reducing latency on its websites. This is particularly important for a company like Gannett, which needs breaking stories and accompanying images or video to load quickly, lest impatient browsers leave to read the story elsewhere. This service certainly seems important given the exponential rate at which data is growing around the world, along with data congestion.

Core Issues

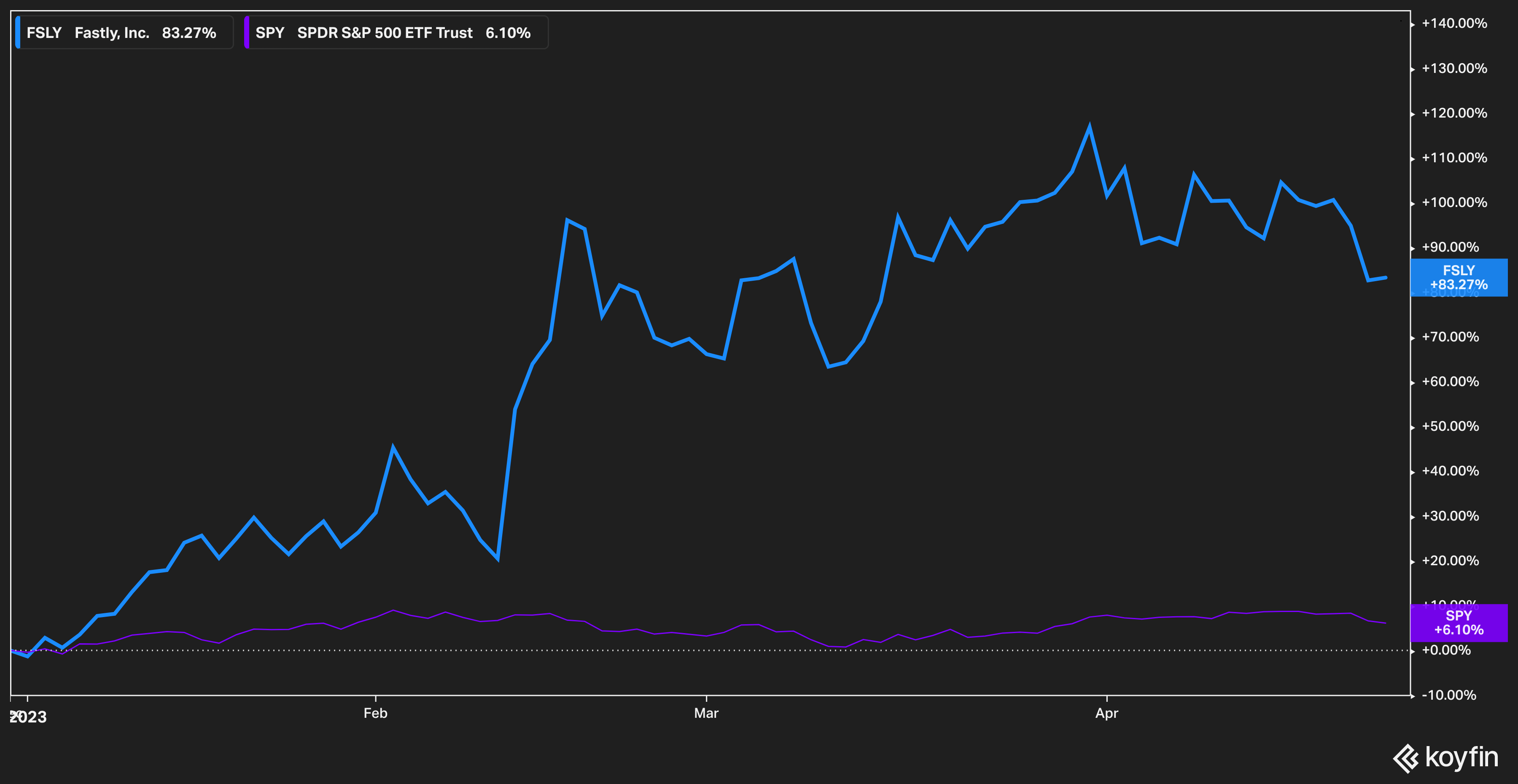

For all the utility of its service, however, Fastly possesses many of the pitfalls associated with high-flying, ZIRP-era, profitless growth companies. Investors, however, may be forgiven for overlooking these facts since the stock has been on a tear in 2023, nearly doubling this year alone.

{kind=link}

We believe that the recent rally is likely to run out of steam, however. Let's take a look at the company's income statement going back to 2020.

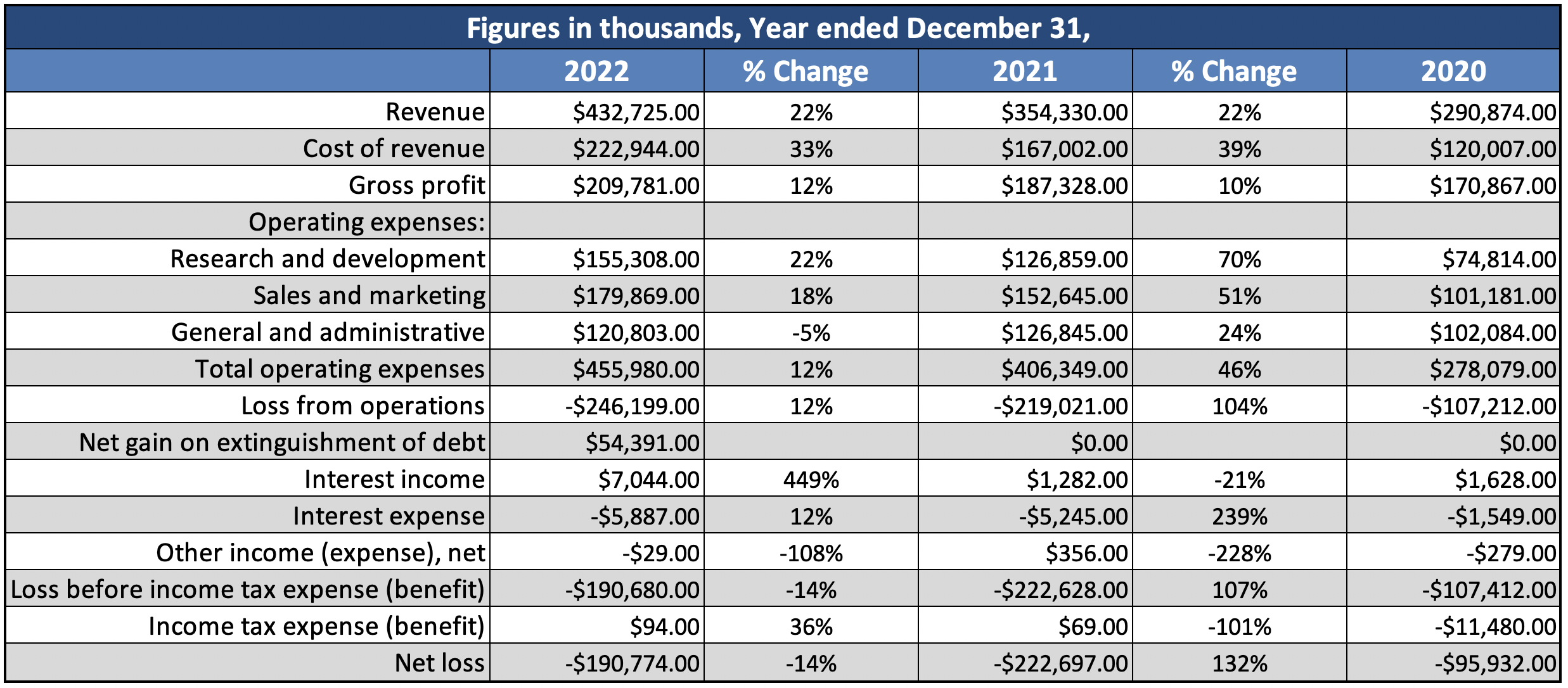

{kind=link}

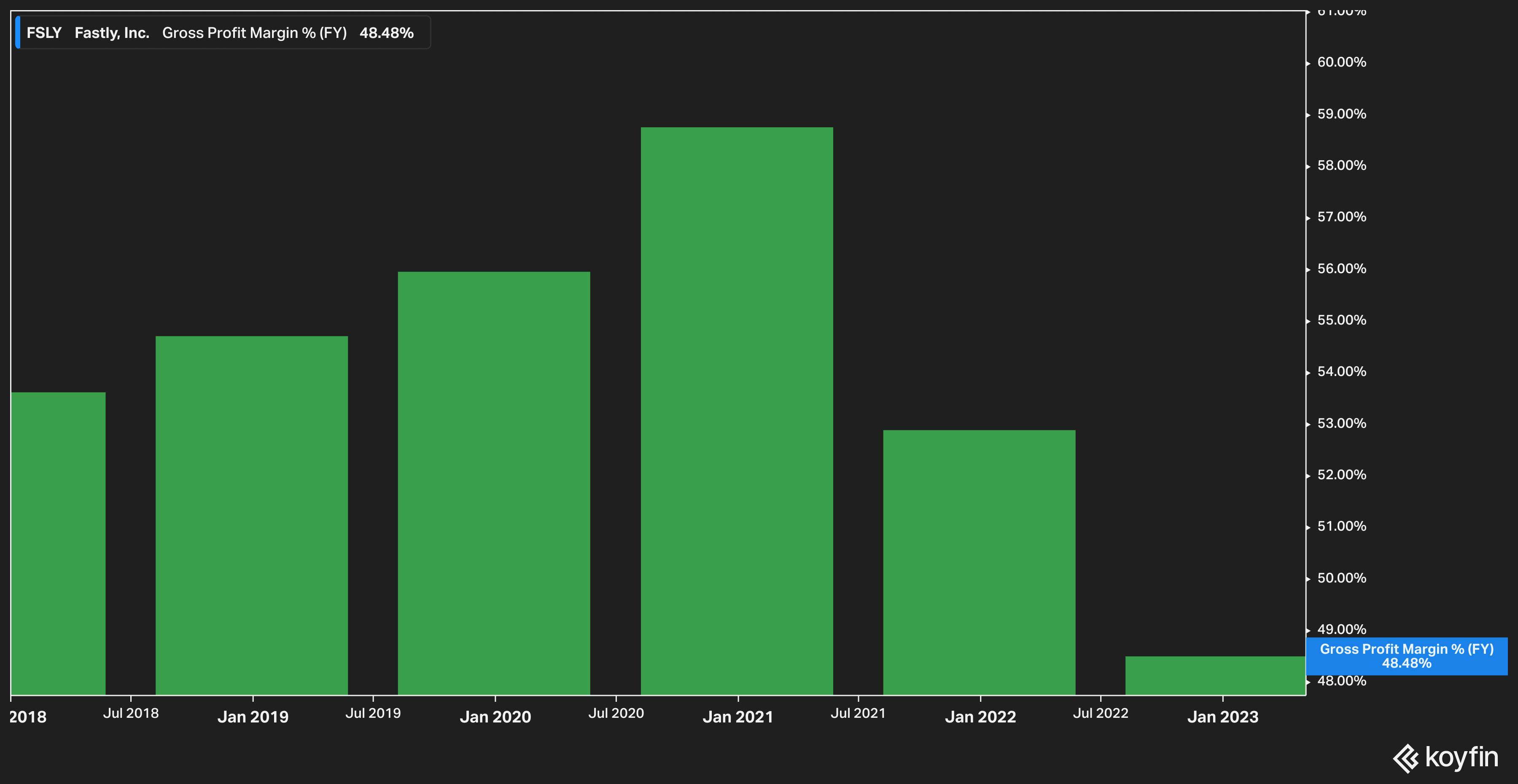

Revenue growth has been steady over the last two years at 22% (management has guided to expect 16% growth in 2023), but cost of revenue has outpaced it. Management noted in the most recent conference call that by the end of 2023 they expect to have gross margins pushing 60% by the end of 2023. This is good to hear, especially since CEO Todd Nightingale has been on the job for less than a year, but for investors 60% gross margins are really just a return to where Fastly has previously operated.

{kind=link}

Indeed, the gross margin posted in 2022 is the lowest in the company's history, and it is during this time with lower gross margins that the stock has rallied significantly, which is cause of concern for us.

Operating expenses, as well, remain stubbornly high - higher than even top line revenue. We find it particularly questionable that the company is investing so much in Research and Development (the line item was up 22% in 2022) at a time when interest rates are going up and the broader market sentiment is that management teams should be focused on achieving profitability.

Sales and Marketing expenses similarly grew 18% year over year. This cash outlay - $179 million dollars in 2022 against $432 million of revenue - is quite simply unsustainable in our view. To state the line item differently, Fastly had to spend $0.41 to generate a dollar of revenue. We believe that the company must get its customer acquisition costs under control before profitability is likely to be achieved.

Customer Concentration & Commitment

Part of the pain of having to spend so much on customer acquisition is that Fastly's sales cycle is long and unpredictable. In that vein, consider the company's own comments from its most recent 10K .

The timing of our sales with our enterprise customers and related revenue recognition is difficult to predict because of the length and unpredictability of the sales cycle for these customers. In addition, for our enterprise customers, the lengthy sales cycle for the evaluation and implementation of our products may also cause us to experience a delay between expenses for such sales efforts and the generation of corresponding revenue. The length of our sales cycle for these customers, from initial evaluation to payment, can range from several months to well over a year and can vary substantially from customer to customer. Similarly, the onboarding and ramping process with new enterprise customers, or with existing customers that are moving additional traffic onto our platform, can take several months.

Readers may be tempted to write off this disclosure as it only applies to enterprise customers, but for Fastly this could be a significant risk. Customer concentration risk at Fastly has been elevated for some time, and it seems to be getting worse. To this end, disclosed on page 24 of Fastly's 10K is the following:

Our 10 largest customers generated an aggregate of 35% and 33% of our revenue in the trailing 12 months ended December 31, 2022 and 2021, respectively. Our 5 largest customers generated an aggregate of 26% and 22% of our revenue in the trailing 12 months ended December 31, 2022 and 2021, respectively.

Now, to spend $0.41 per dollar of revenue generated would be one thing if (if!) the revenue generated were recurring and consistent, which is the lens through which many investors approach software companies generally. After all, if a company depends on large, enterprise clients for so much of its revenue, it would make sense to ensure that customers agreed to service contracts spanning several years.

Fastly, however, does not have long-term contracts with its customers. The company states that "most of our customers, including some of our largest enterprise customers, do not have long-term contractual financial commitments to us. In addition, most of our current customer contracts are only one year in duration and these customers may not use our platform in a subsequent year."

These combined issues - spending significant amounts of money to secure clients who do not sign commitments (if they sign one at all) greater than one year in duration - set off alarm bells in our ears.

Bulls Say...

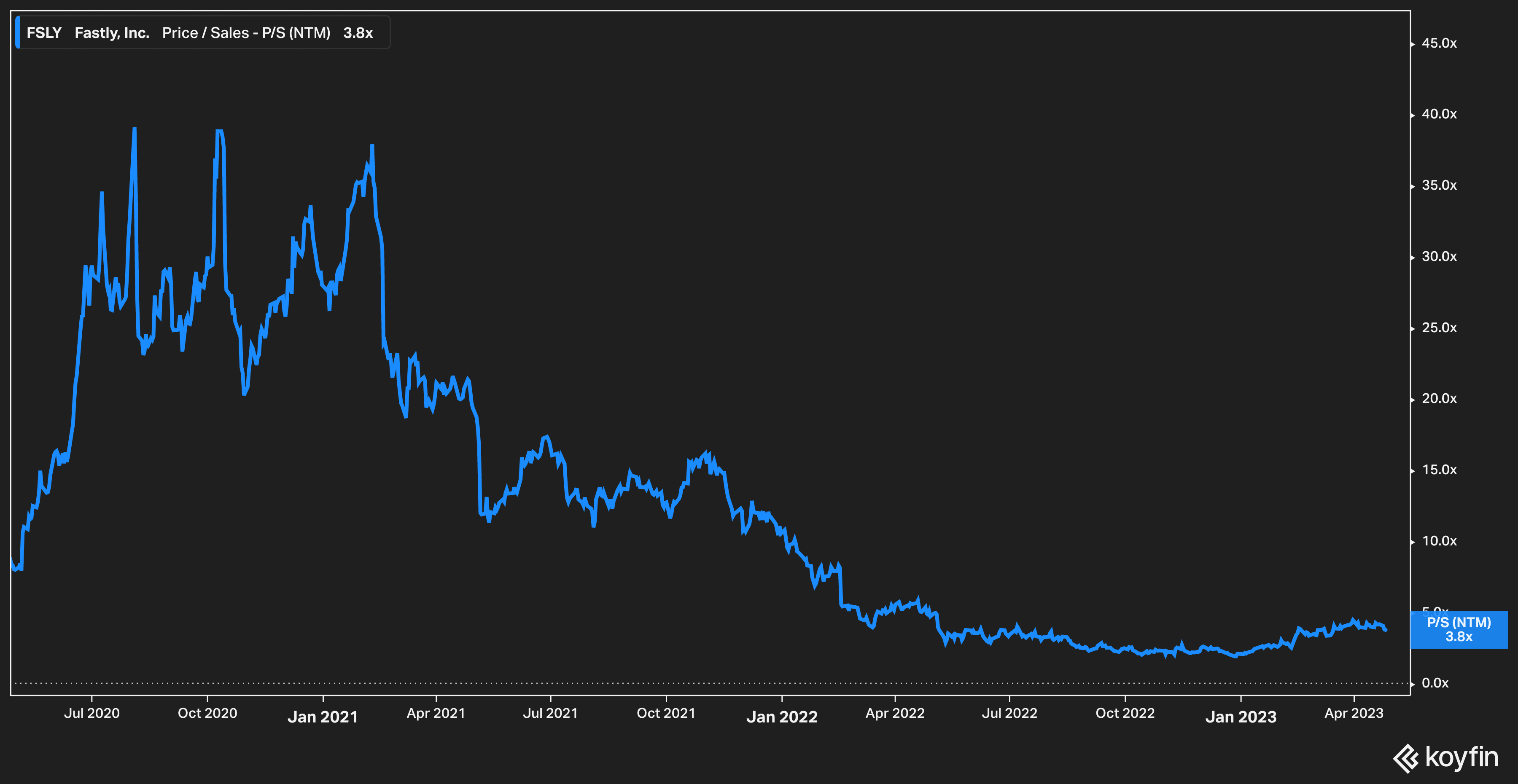

On the valuation front, bulls will likely point out that the company's price-to-sales has been falling for some time.

{kind=link}

Given that the stock once traded in the 30x range and today can be bought for less than 4x forward sales estimates, bulls believe that the valuation today is much more rational for an entry point. We take issue with this principally because, as we've shown above, the company's cost structure seems unsustainable. Therefore, we find it difficult to ascribe a true value to a metric like price-to-sales for Fastly.

Bulls are also likely to say that Fastly's business itself is solid - that it is a leader in a nascent industry set to burst onto the scene.

We are inclined to agree. Edge computing, we think, is likely to find quite a bit of traction among developers in the coming years. We just aren't sure how much market share Fastly will be able to capture. This is because Fastly, despite how intriguing the businesses is, in our view possesses very little in terms of a competitive moat. There is feasibly very little stopping a hyperscale cloud provider from branching into edge computing or acquiring a competitor to materially disrupt the business landscape (the company discusses these possibilities and some of its principal competitors on page 24 of its 2022 10K).

For example, consider the case study with Gannett referenced earlier. While it seems undeniable that Fastly provided a value-add service to Gannett, it also seems incredibly plausible that Gannett could develop (or may already have) a relationship with a hyperscale cloud provider such as Amazon's ( AMZN ) AWS or Google Cloud ( GOOG )( GOOGL ). Should either of these two giants decide to muscle into Fastly's business, it seems that there would be little to stop them.

The Bottom Line

Shares of Fastly have experienced a strong rally to start 2023, but we believe the sustainability of that rally is tenuous. Given that the company has a limited technological moat, high sales and marketing expenses, and very little in the way of customer stickiness as far as long-term commitments go, we remain on the sidelines when it comes to Fastly.

For further details see:

Fastly: Danger Ahead