FSLY - Fastly: Don't Get Too Excited

2023-08-04 09:09:13 ET

Summary

- Fastly's second quarter results were far less impressive than the market reaction would suggest.

- Growth is stable but low, and Fastly is still a long way away from achieving profitability on a GAAP basis.

- The recent share price surge is more the result of demand headwinds easing and sentiment towards the stock improving than Fastly's prospects fundamentally changing.

- Fastly's valuation now looks more in line with market, which probably suggests upside is limited, particularly given that margins will deteriorate signifycantly in the third quarter.

Despite the extremely positive share price reaction, Fastly’s ( FSLY ) second quarter results were only average. Growth has been fairly stable over the past two years and it has yet to show a consistent trend higher. Margins and cash flows improved but this was largely on the back of one-time benefits. Sentiment towards the stock had become overly negative, which I pointed out earlier in the year, and the stock price runup in recent months has been due more to improving sentiment than fundamentals. This will make further gains more difficult going forward as expectations are higher and Fastly is still the same company it has always been.

Fastly believes its platform strategy is leading to strong cross-selling activity, although this is hard to see in the company's financials. Security continues to be an area of strength, particularly in next-gen WAF technology. This strength is coming both from sales to existing customers and new logo wins.

Fastly is also reportedly seeing momentum in its compute and observability businesses. Management has suggested that customers with large personalization requirements, like ecommerce and retail, tend to be more interested in the compute offering. The compute business is expected to be a margin tailwind as it grows in importance.

Fastly suggested on the second quarter earnings call that AI inference workloads could be a tailwind for its edge cloud. Fastly has been engaging with customers across a range of industries regarding this. For ecommerce, AI could drive greater personalization and more accurate recommendations, with inferencing at the edge allowing lower latencies. Within media, AI can be used to detect spam and flag problematic user-generated content. This is all fairly hypothetical at this point though. It is not clear that Fastly's compute business is a meaningful revenue generator yet, and Cloudflare ( NET ) appears far better positioned to capitalize on the opportunity.

At the market level, Fastly has suggested that some larger customers that have been pursuing a multi-CDN strategy are looking to consolidate. Fastly has suggested this is a positive, as its position as a performance leader should lead to market share gains. CDN is also now reportedly being purchased as part of an edge cloud solution, which Fastly believes is another tailwind.

Financial Analysis

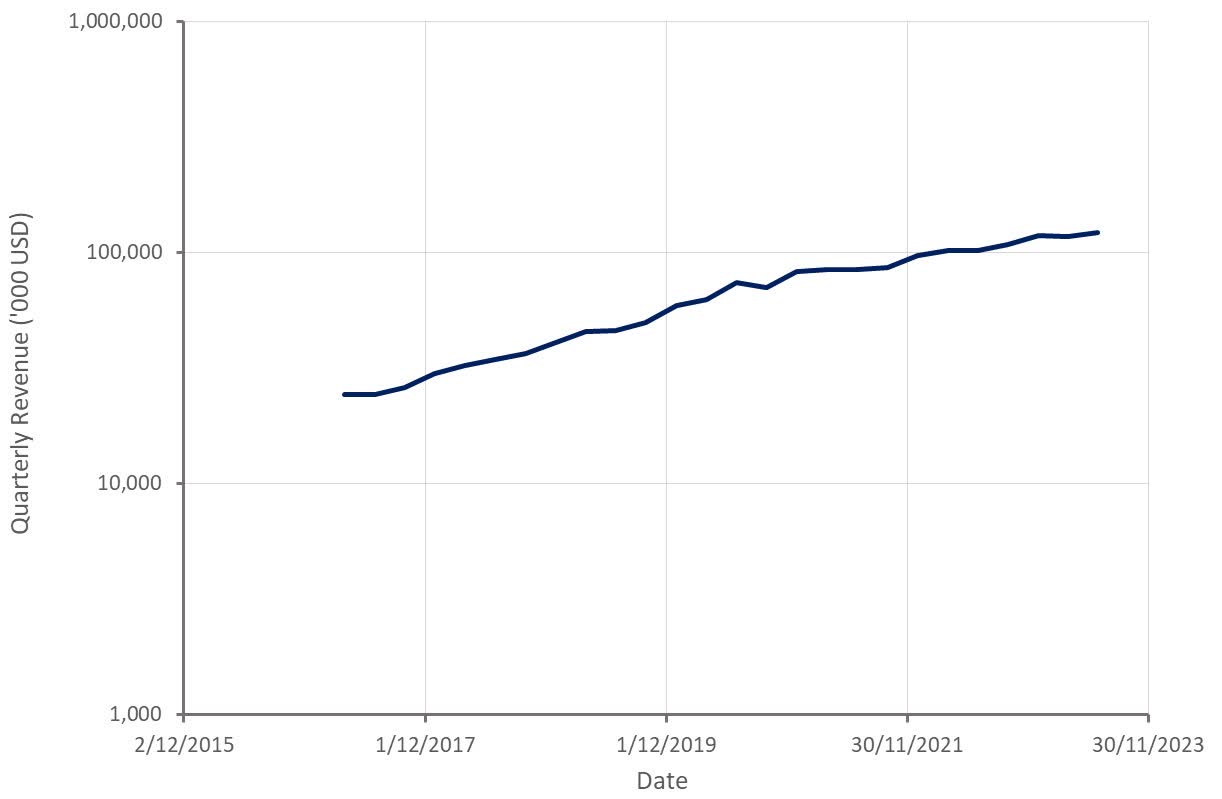

Revenue increased by 20% YoY in the second quarter, driven by enterprise customers and Signal Sciences. Revenue from Signal Sciences products increased 32% YoY and the business excluding Signal Sciences grew around 18%. This strength is also expected to carry through to the rest of the year, with Fastly guiding for 17% revenue growth in the third quarter and for the full year.

{kind=link}

Figure 1: Fastly Revenue (source: Created by author using data from Fastly)

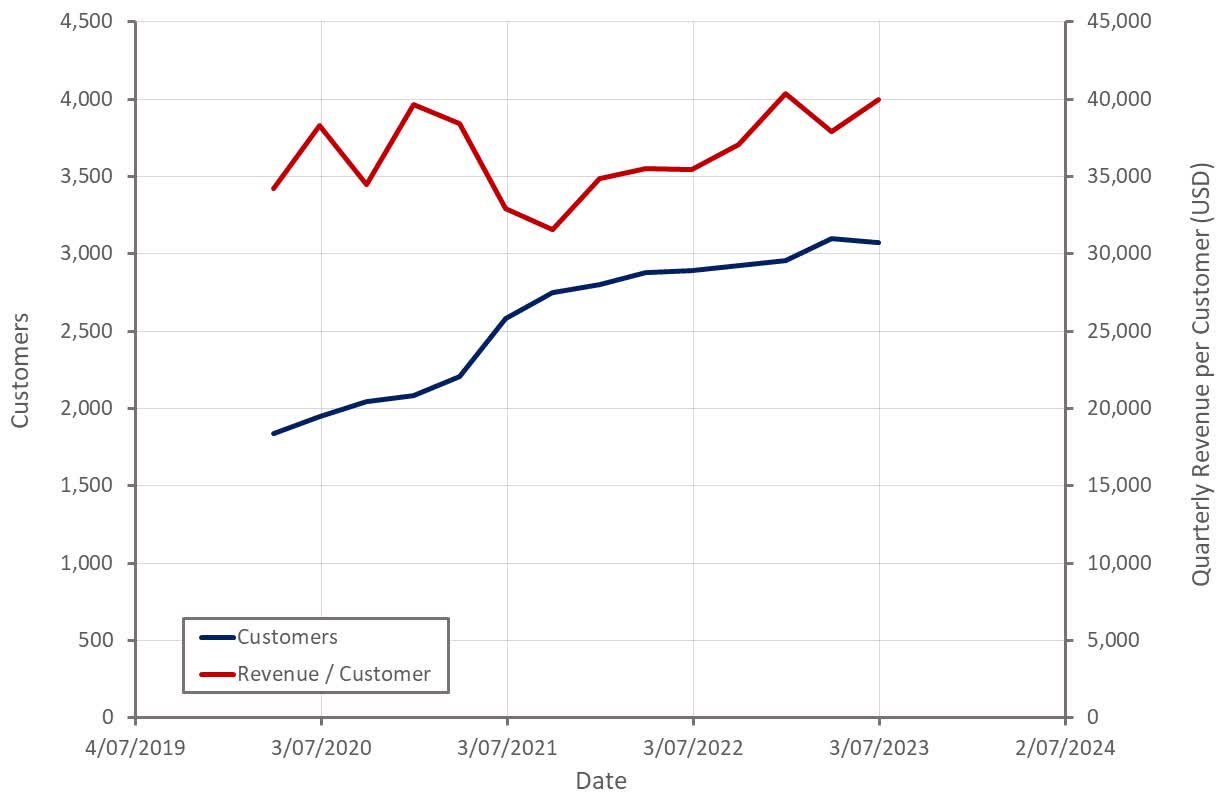

Fastly’s total customer count declined by 28 sequentially in the second quarter to 3,072. Roughly one third of this decline was attributed to customer consolidations and most of the other customers reportedly had relatively small ARRs. Fastly’s enterprise customer count increased by roughly 10% YoY. Fastly has an ongoing problem with attracting new customers that shouldn’t be downplayed though. The company’s focus is clearly on large customers with high performance requirements, but this strategy will only take the company so far. A wider customer base will ultimately be needed to continue driving growth, and scale is an important determinant of margins.

Fastly recently introduced new pricing and packages for its portfolio, including flat-rate pricing and tiered packages. This is supposed to make it easier for customers of all sizes to adopt Fastly’s platform, and customer reception has reportedly been favorable.

Fastly’s net retention rate was 116% in the second quarter and appears to have stabilized. Fastly has stated that expansion is being driven by traffic growth and cross-sell opportunities with low customer churn. While it is a positive that Fastly’s NRR has stopped declining, the current figure is hardly strong. Cross-sell opportunities from Signal Sciences, along with the introduction of products like edge compute and observability, should be driving significant expansion. A soft demand environment may largely be responsible for this, but investors should look for signs of increased expansion going forward.

Fastly has been working on platform unification and simplifying its sales motion to support cross-sell opportunities. Management has stated that an increasing proportion of their large deals are platform wins, with customers adopting multiple solutions.

Enterprise customers accounted for 92% of Fastly’s revenue in the second quarter, with average spend increasing 10% YoY. Fastly’s top 10 customers accounted for 37% of revenues in the second quarter, indicating that customer concentration remains a problem.

{kind=link}

Figure 2: Fastly Customers (source: Created by author using data from Fastly)

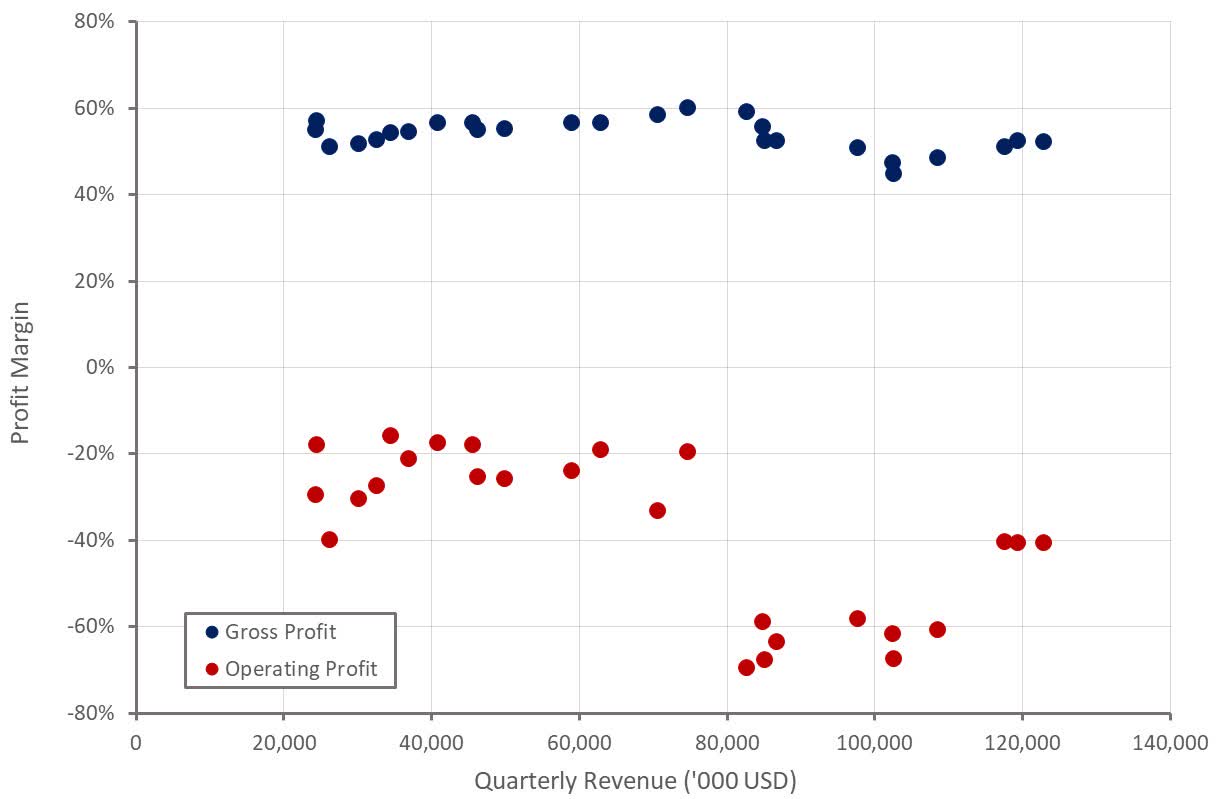

Fastly’s gross profit margin was roughly 52% in the second quarter and has now been fairly flat over the past three quarters. Gross profit margins have improved by around 7% over the past 12 months as Fastly has focused on its fixed costs and improving network utilization. Margins remain well below the COVID peaks and pre-COVID levels though, despite the addition of higher margin businesses like security, observability and compute.

It seems likely that pricing is a contributor to this problem, with Fastly stating that there were price declines in the second quarter as a result of winning additional delivery traffic from a major customer. Pricing is expected to resume its normal trajectory in the second half, with reductions in bandwidth cost and ongoing network optimization offsetting price declines.

Fastly recently onboarded traffic that is expected to adversely impact bandwidth costs though. Traffic that fluctuates over the course of the day and has significant peaks tends to result in lower utilization and higher costs. As a result, gross margins are expected to decline by roughly 1% in the third quarter.

{kind=link}

Figure 3: Fastly Profit Margins (source: Created by author using data from Fastly)

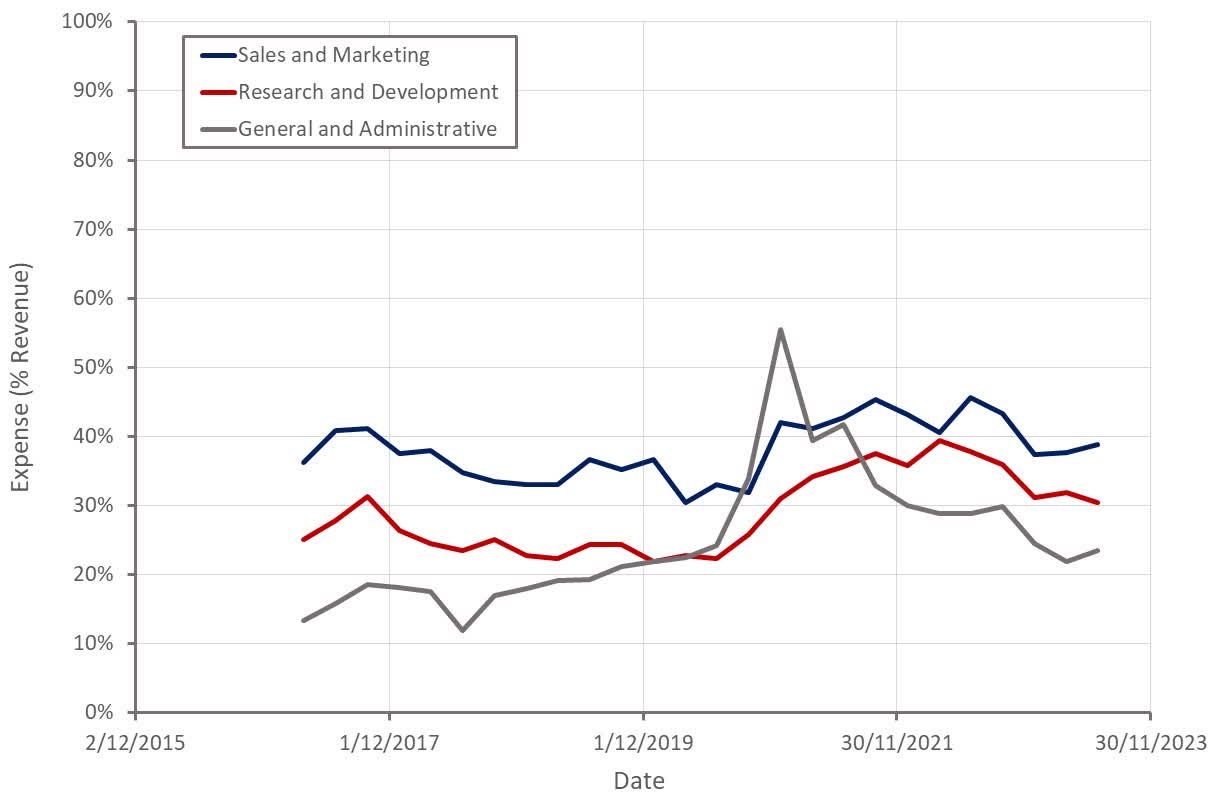

Operating expenses totaled 77 million USD in the second quarter, although they were artificially depressed for a number of reasons. The timing of marketing expenses and an increase in capitalization of internal-use software accounted for around a 3 million USD reduction, and Fastly recognized a 3.4 million USD G&A benefit due to a tax refund. As a result, Fastly’s third quarter operating loss is expected to increase by around 8 million USD.

{kind=link}

Figure 4: Fastly Operating Expenses (source: Created by author using data from Fastly)

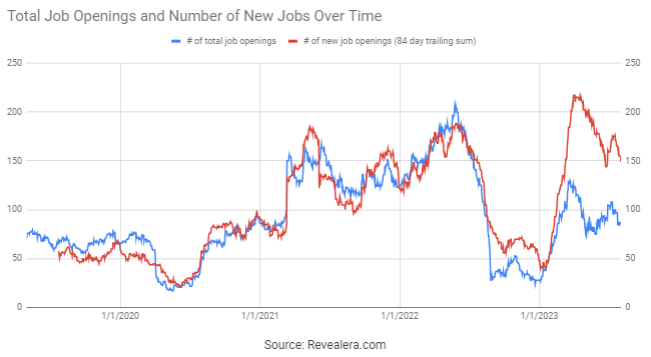

Job openings at Fastly were an early indicator that market sentiment towards the company was far too negative earlier in the year. While hiring remains solid, the number of job openings is no longer increasing, which could suggest that growth is unlikely to continue accelerating. Continued growth along with modest hiring should be supportive of margins though.

{kind=link}

Figure 5: Fastly Job Openings (source: Revealera.com)

Fastly’s free cash flow in the second quarter was 7.8 million USD , driven by an improvement in working capital and higher operating margins. Cash flows are expected to turn negative again in the third quarter though, driven by working capital requirements and lower operating margins.

Fastly still has a large amount of cash on the balance sheet and used some of this in the second quarter to repurchase convertible debt at a discount, resulting in a 36.8 million USD net gain.

Conclusion

Fastly's modest beat and raise in the second quarter, along with some one-time margin tailwinds, resulted in a 20% plus share price gain, which is indicative of how negative sentiment has been. The stock no longer looks heavily undervalued though and performance expectations going forward will be much higher.

Fastly has been an investor favorite in the past and could begin to exhibit some momentum based on the share price move over the past six months. Despite this, Fastly is still a company with modest growth, large losses and a niche value proposition and it is not clear that the stock has much more upside.

{kind=link}

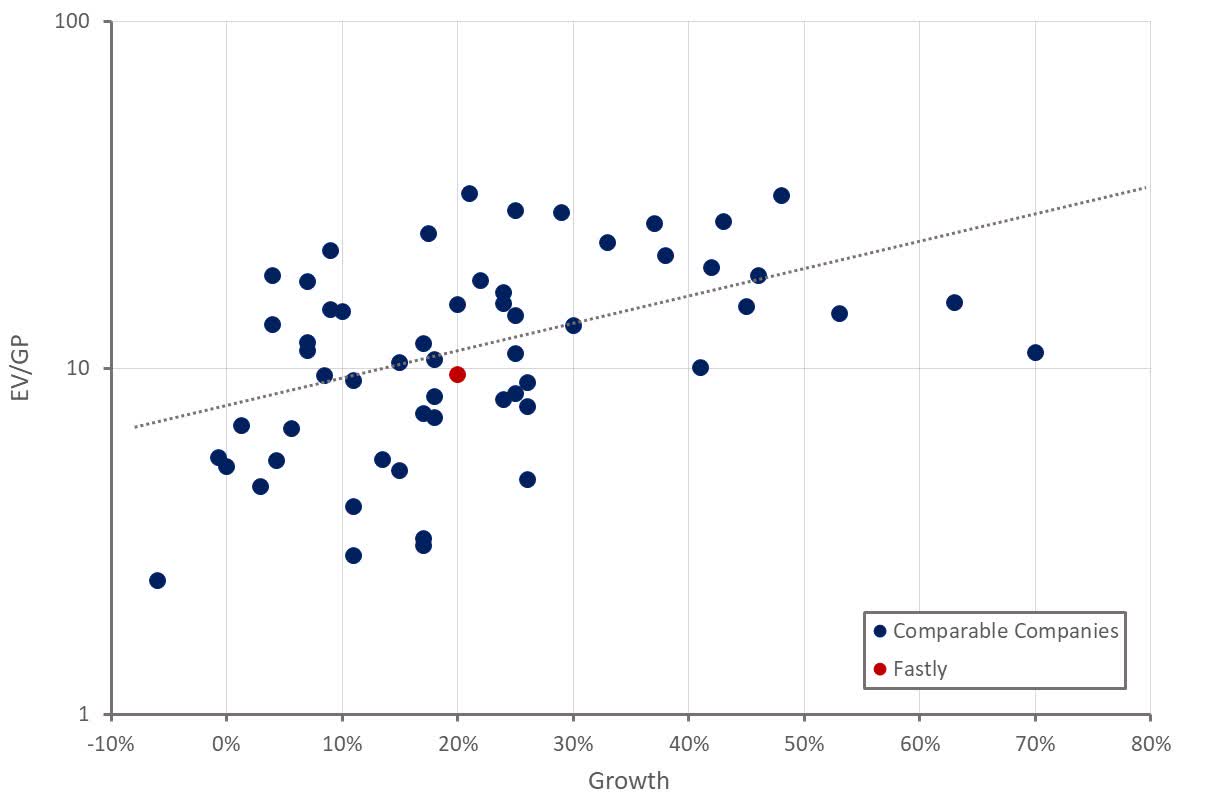

Figure 6: Fastly Relative Valuation (source: Fastly Relative Valuation)

For further details see:

Fastly: Don't Get Too Excited