FSLY - Fastly: More Room To Run

2023-12-17 22:43:12 ET

Summary

- Fastly is an undervalued small-cap growth stock with room to grow in 2024.

- The company has strong sales momentum and is benefiting from increased internet traffic and usage.

- FSLY is seeing tremendous momentum with channel partners, extending its sales reach.

- At just over ~4x 2024 revenue, Fastly still has room to run higher.

A market rally is coming in 2024, but I don't necessarily think a rising tide will lift all boats. This year's rally has largely focused on the safety of large-cap names, but there are a number of undervalued small-cap growth stocks that I think have plenty of room to run in 2024.

Despite more than doubling year to date, Fastly ( FSLY ) is one of those stocks that I think has plenty of room to march higher. This CDN company, which is the bridge between internet users and website owners, has benefited from strong traffic/usage and excellent sales momentum.

I last wrote a bullish note on Fastly in September, when the stock was trading closer to $23 per share. Since then, the company has dropped on little news, outside of Q3 earnings (which were well-received) and the resignation of the company's chief revenue officer, which may have some short-term impact on the sales team's headcount churn but doesn't distract from the long-term growth potential of this company.

All in all, I remain quite bullish on Fastly, especially as the company has initiated a number of catalysts to drive outperformance in 2024. Among them is strong momentum in the partner channel. Fastly continues to be a smaller player relative to legacy vendors like Akamai ( AKAM ), and its sharp expansion of its reseller partners will allow the company to extend its sales muscle far beyond what its sales force is capable of achieving on its own. High-profile clients are also continuing to choose Fastly and signal to other companies the quality of its CDN network (a recent major win in Q3 was Wendy's ( WEN ), the fast-food giant).

As a refresher to investors who are just getting caught up on Fastly, here is my full long-term bull case for the stock:

- Fastly's usage-based business model opens the door to tremendous growth - Fastly, alongside other software/technology peers like Twilio ( TWLO ), was among the companies that could fully take advantage of the pandemic and the increase in internet traffic that came with it. Because Fastly's pricing is based on volumes of content delivered, as the underlying customers continue to grow their websites and traffic, Fastly's revenue will also grow proportionally. Fastly's dollar-based revenue retention rates recently clocked in the ~120% range, which is an enviable target vis-a-vis other tech growth stars.

- Greater customer diversification - 2020 caused a big disruption for Fastly when it lost its biggest customer, TikTok. Since then, however, Fastly has proven its "horizontal" nature by landing customers of various industries, and the fact that it is still growing revenue in the mid-20s proves that it has reduced its reliance on single large customers. The company now has a base of approximately 3,000 total customers, with about ~500 enterprise customers between them.

- Best of breed - Though CDN is not a new technology category, with companies like Cloudflare ( NET ) and Akamai preceding Fastly by several years (and in Akamai's case, decades), Fastly is one of the most highly regarded CDN vendors. Fastly's addition of Signal Sciences and its web application firewall (WAF) tools also flesh out Fastly's offering. The company was also recently recognized as a Challenger by the influential Gartner Magic Quadrant reviewers.

- Economies of scale - As Fastly grows, it achieves economies of scale on its CDN network. It has already started to pare down hardware spend in an effort to improve gross margins. Capex spend as a percentage of revenue is also expected to continue trending downward. As Fastly's existing customer base continues to boost usage, margins will continue to expand.

With the company's post-September correction (whereas most other tech companies have rallied since then), I also find Fastly's valuation to be incrementally more appealing. At current share prices near $19, Fastly trades at a market cap of $2.45 billion. After we net off the $460.7 million of cash and $472.8 million of debt on Fastly's most recent balance sheet, the company's resulting enterprise value is $2.46 billion.

Meanwhile, for next fiscal year FY24, Wall Street analysts are now expecting Fastly to generate $584.9 million in revenue, representing 15% y/y growth. This puts Fastly's valuation multiple at 4.2x EV/FY24 revenue.

Directionally, I still think Fastly is well-positioned for double-digit gains in FY24, though I'm de-risking my price target down to $24 (from a prior $27), representing 5.2x EV/FY24 revenue and ~26% upside from current levels.

Stay long here and buy Fastly while it's on a recovery path back toward September highs.

Q3 download

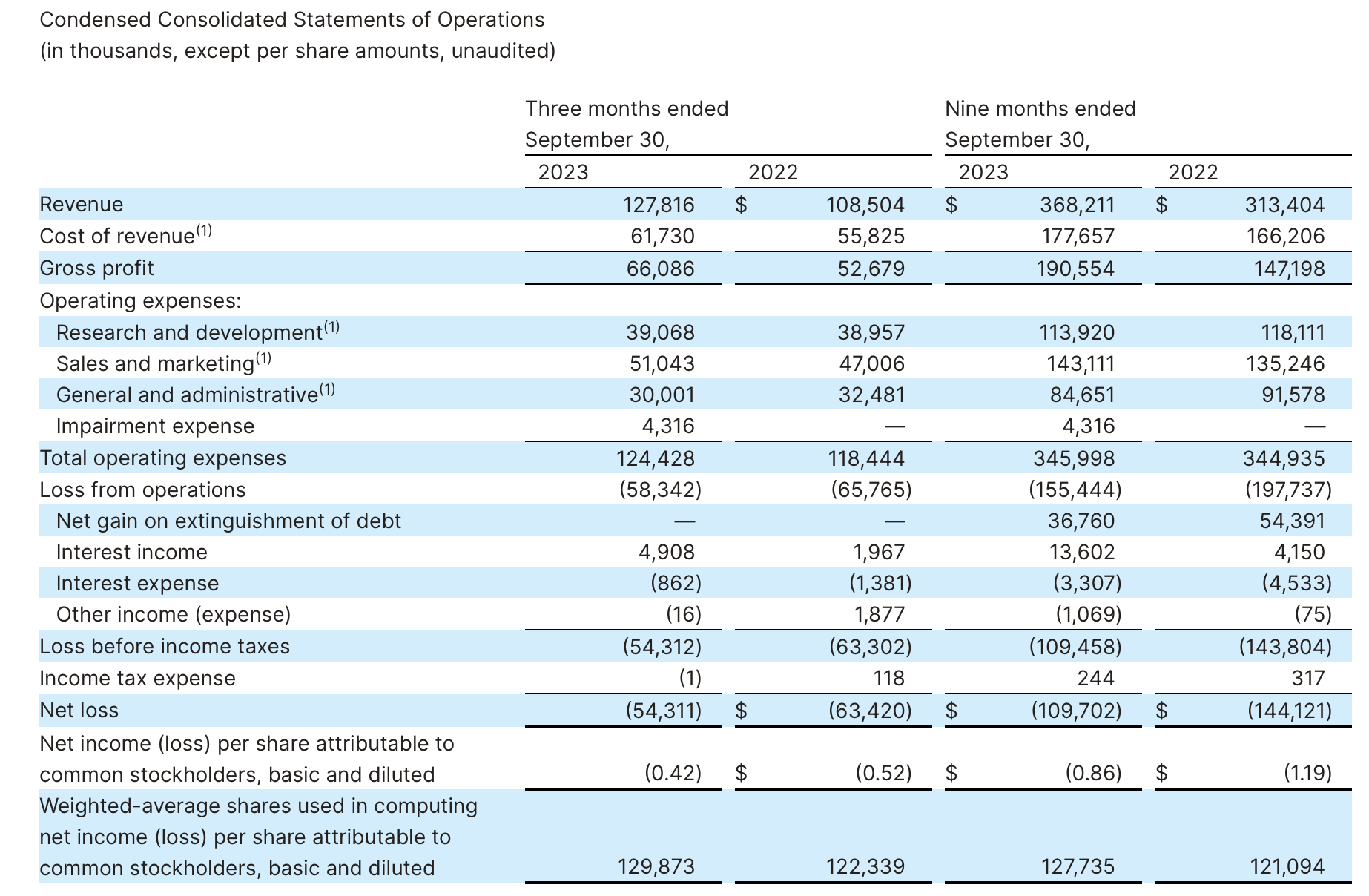

Let's now go through Fastly's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

Fastly Q3 results (Fastly Q3 earnings release)

{kind=link}

Fastly's revenue grew 18% y/y to $127.8 million in the quarter, beating Wall Street's expectations of $126.9 million (+17% y/y) by a one-point margin. Revenue growth did decelerate, however, from 20% y/y growth in Q2.

Management is still pointing to an overhang from macro-related budget constraints as holding back the company's growth rates. In spite of this, existing customers are continuing to expand their spend - which is a testament to both customer satisfaction as well as Fastly's own cross-sell momentum. The company also noted a higher-than-expected surge in international traffic (good for growth, but a slight headwind to gross margins).

Dollar-based net retention rates in the quarter were still elevated at 120% (indicating 20% net upsell), three points lower sequentially versus 123% in Q2.

As previously noted, channel partner expansion has been a key driver for Fastly's go-to-market strategy going forward. Per CEO Todd Nightingale's remarks on the Q3 earnings call :

Moving on to our channel partner development, we are seeing great progress here. Our 2023 deal registration is already triple that of 2022. You'll recall that during our Investor Day in late June, Brett shared with you that we had 33 partners globally engaged. Today that number totals 55. Our revenue contribution has grown more than 50% in 2023 year-to-date, when compared to all of 2022.

And we expect to see this trend continue into 2024. So far, I'm pleased with the progress we're making in 2023. And this is reflected in our updated projections for the year. We raised our annual guidance for both revenue and operating margin and we'll strive to find ways to outperform that guidance through strong innovation velocity, strategically lowering the friction of our go to market efforts and streamlining our employee experience."

The company added 30 net-new customers in the quarter, bringing its total to over 3,100 customers. Note that Q3 saw many more customer adds than just 11 added in Q2.

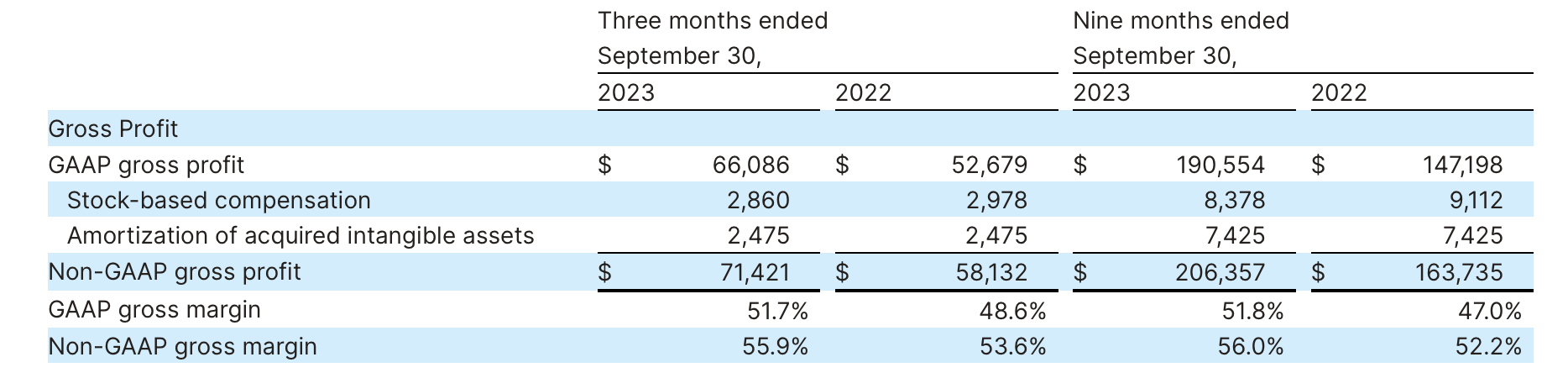

From a margin standpoint, economies of scale have driven the company's pro forma gross margins to 55.9%, up 230bps y/y.

Fastly pro forma gross margins (Fastly Q3 earnings release)

{kind=link}

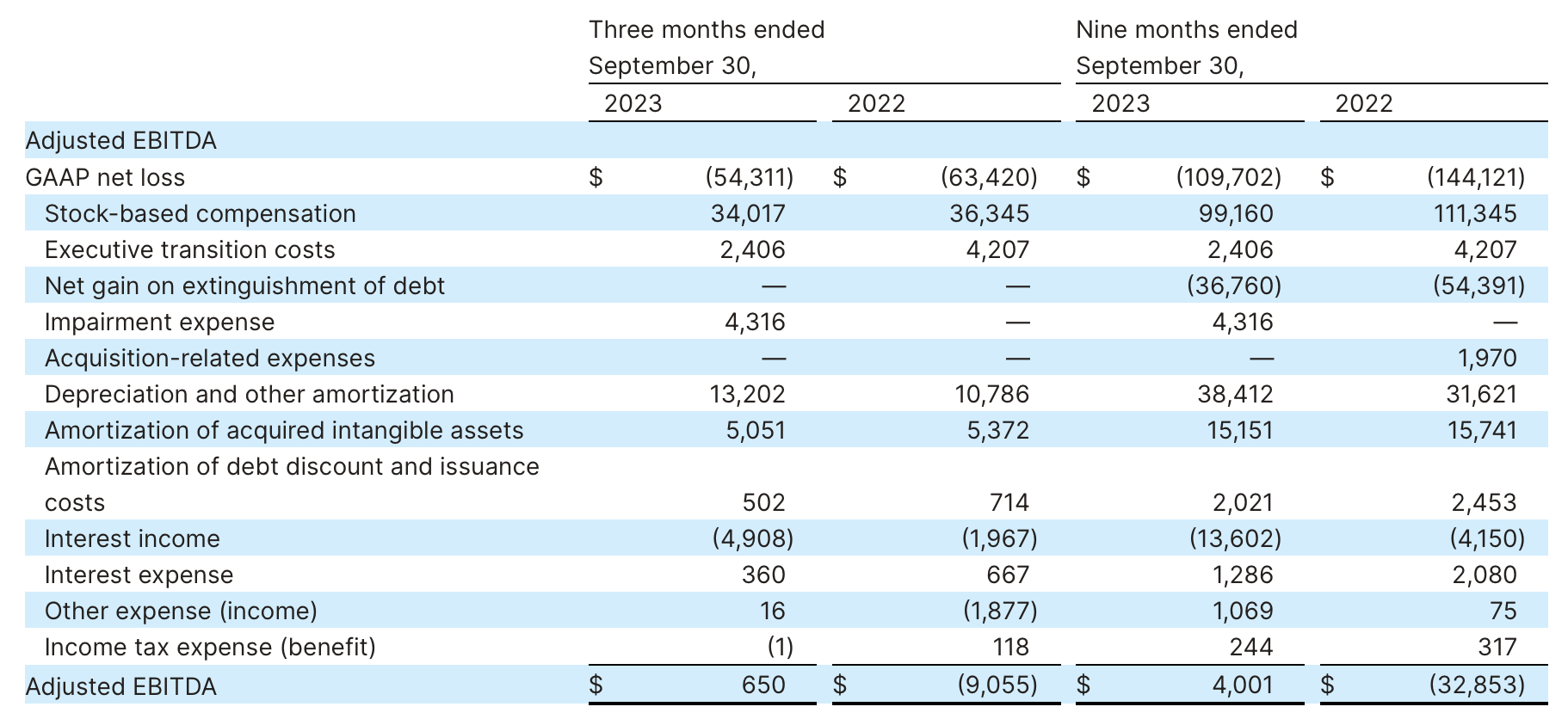

And though Fastly has not done any high-profile layoffs like many of its tech peers have, the company has still done a good job at reining in opex to boost its bottom line. As shown in the chart below, adjusted EBITDA was roughly flat in the quarter (a 1% margin) versus an -8% loss margin in the year-ago quarter.

Fastly adjusted EBITDA (Fastly Q3 earnings release)

{kind=link}

This was Fastly's second quarter of adjusted EBITDA profitability, which the company notes should be a regular occurrence going forward due to the combination of gross margin expansion and opex leverage on a growing top line.

Key takeaways

In my view, there's more room for Fastly to slide higher as it continues to execute a strong growth plan amid a large and greenfield addressable market. Its expanding wallet share, as evidenced through high dollar-based net retention rates, should continue to drive top-line growth for the company that requires little incremental cost investment, boosting its path toward profit expansion. Stay long here as Fastly rebounds.

For further details see:

Fastly: More Room To Run