FSLY - Fastly: Nearing A Critical Inflection Point

2023-06-26 07:15:28 ET

Summary

- Fastly, an edge cloud computing platform, is approaching an inflection point of profitability.

- FSLY is operating in a growing addressable market, and the company continues to grow its customers, especially in the Enterprise market.

- Despite being free cash flow negative, Fastly has an aggressive plan to achieve FCF profitability by FY 2024, making it a promising recovery investment in the content delivery network sector.

Fastly ( FSLY ) is an edge cloud computing platform whose shares have been in a long-term downtrend. Although Fastly's valuation soared during the pandemic, the firm has seen a moderation of its top line growth as well as struggled with achieving profitability. However, Fastly is nearing an inflection point (EBITDA profitability) which could result in investors rediscovering this beaten-down tech company. The company's valuation is also much more attractive after a near-80% downside revaluation and the risk profile looks increasingly favorable!

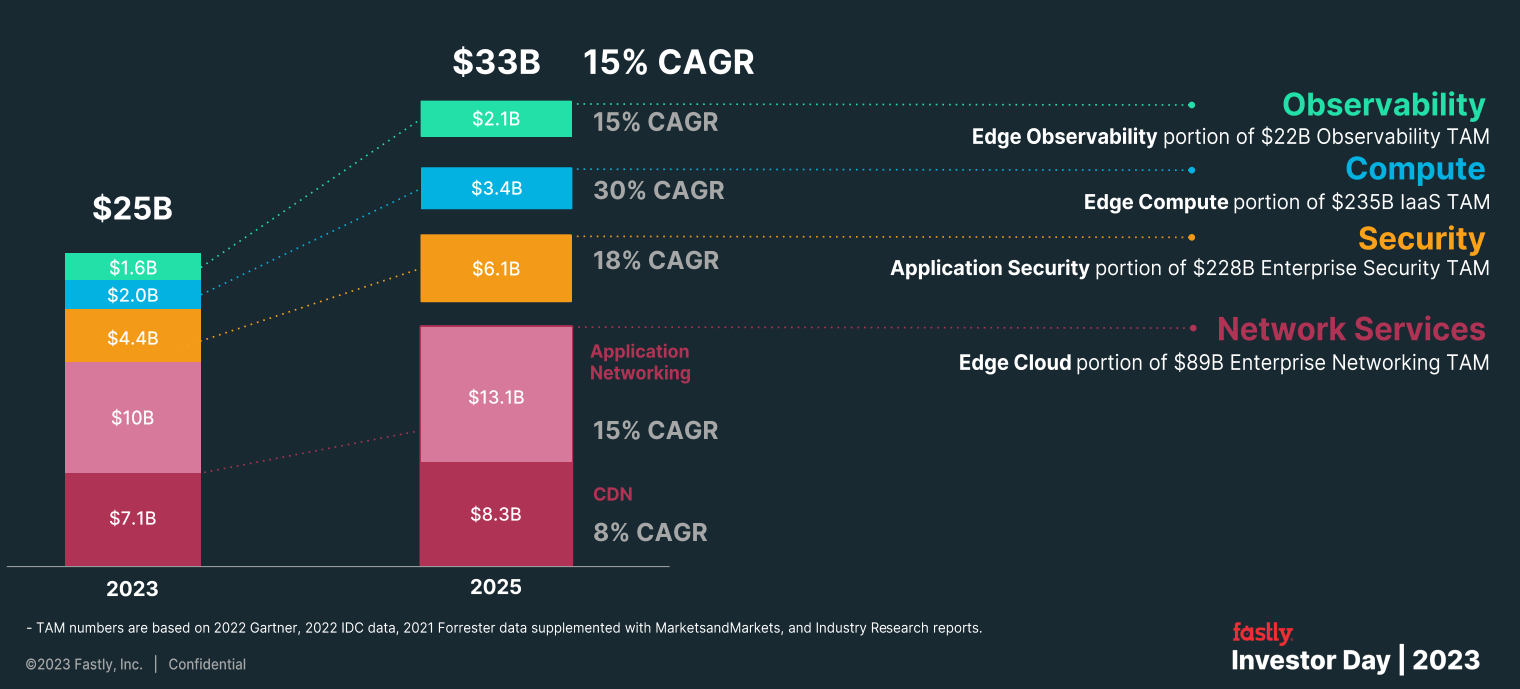

Growing TAM and footprint in the Enterprise market

Fastly is a leading edge cloud computing platform that offers its customers content delivery network and security solutions. With Fastly's core product offering, companies can scale their digital transformations in a fast-changing market. The total addressable market for Fastly's products and services is expected to grow from $25B in FY 2023 to $33B in FY 2025 which calculates to an average annual growth rate of approximately 15%. The biggest growth opportunity for Fastly is in the edge computing market which is expected to grow at twice the overall CAGR -- at 30% annually -- over the next two years.

{kind=link}

Fastly has seen a slowdown in its revenue growth over time, in part because customer acquisition growth has slowed and companies overall have cut back on spending on IT spending, driven by a desire to control costs in a high-inflation world. However, Fastly is still executing very well in the Enterprise segment which is seeing twice the customer acquisition growth (10.7% vs. 4.6%) than Fastly's overall customer growth rate. Enterprise customers typically are large companies that generate more than $100 thousand in annual recurring revenues. At the end of the first-quarter, Fastly had 3,100 customers using its platform, including 540 Enterprise customers.

| FY 2023 |

| FY 2022 |

| Fastly |

| Quarter 1 |

| Quarter 4 |

| Quarter 3 |

| Quarter 2 |

| Quarter 1 |

| Growth Y/Y |

| Total Customer Count |

| 3,100 |

| 3,062 |

| 3,039 |

| 3,025 |

| 2,965 |

| 4.6% |

| Enterprise Customer Count |

| 540 |

| 533 |

| 511 |

| 499 |

| 488 |

| 10.7% |

| Dollar-based net retention rate |

| 121% |

| 123% |

| 122% |

| 120% |

| 118% |

| 3 PP |

(Source: Author)

Fastly expresses its ability to grow revenues internally through a figure called dollar-based net expansion rate (DBNER). This rate is a financial metric that measures the growth and revenue retention of a company's existing customer base. A DBNER rate of 121% -- Fastly's dollar-based net expansion rate in the most recent quarter -- means that a firm has grown its revenue base, from the same customer pool, by 21% year over year. Fastly's DBNER figure increased 3 PP year over year and the company is still doing a good job growing revenues organically: the higher the DBNER number, the better a company is doing regarding customer retention and upsells.

EBITDA and free cash flow profitability would be an inflection point for Fastly...

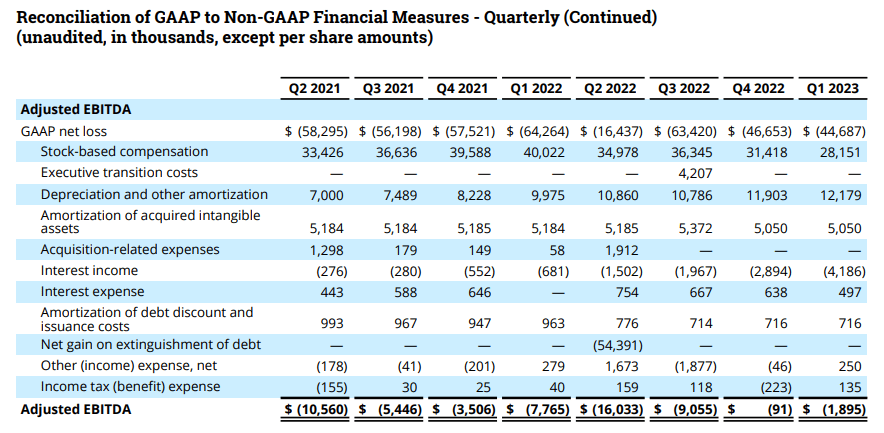

Like so many cloud-focused companies, Fastly is not profitable, but the company continues to grow its customer base, especially in the profitable Enterprise market, and Fastly is slowing approaching profitability, based off of adjusted EBITDA. The cloud-based company reported a $1.9M EBITDA loss for the first-quarter, but drastically narrowed losses compared to the year-earlier period. In Q4'22, Fastly came very close to positive adjusted EBITDA and I believe Fastly has a reasonably good chance to achieve EBITDA profitability in FY 2024.

{kind=link}

Fastly is also not yet profitable on a free cash flow basis. Fastly achieved negative free cash flow of $26.5M in the most recent quarter, but the overall free cash flow picture definitely needs to be improved: Fastly has consistently been FCF-negative with quarterly free cash flow losses ranging between $27M and $61M in the last five quarters.

| Fastly |

| FY 2023 |

| FY 2022 |

| $'000 |

| Quarter 1 |

| Quarter 4 |

| Quarter 3 |

| Quarter 2 |

| Quarter 1 |

| Cash flow from operations |

| ($8,861) |

| ($12,128) |

| ($27,634) |

| ($16,680) |

| ($13,190) |

| Purchases of P&E |

| ($3,494) |

| ($8,529) |

| ($2,631) |

| ($6,428) |

| ($2,387) |

| Proceeds from P&E sales |

| $22 |

| $126 |

| $125 |

| $241 |

| $0 |

| Capitalized internal-use software |

| ($4,209) |

| ($4,290) |

| ($5,120) |

| ($4,926) |

| ($3,810) |

| Repayments of finance lease liabilities |

| ($8,645) |

| ($4,427) |

| ($7,076) |

| ($3,870) |

| ($7,159) |

| Advance payments for purchase of P&E |

| $0 |

| ($10,923) |

| ($1,964) |

| ($29,310) |

| $0 |

| Free Cash Flow |

| ($25,187) |

| ($40,171) |

| ($44,300) |

| ($60,973) |

| ($26,546) |

(Source: Author)

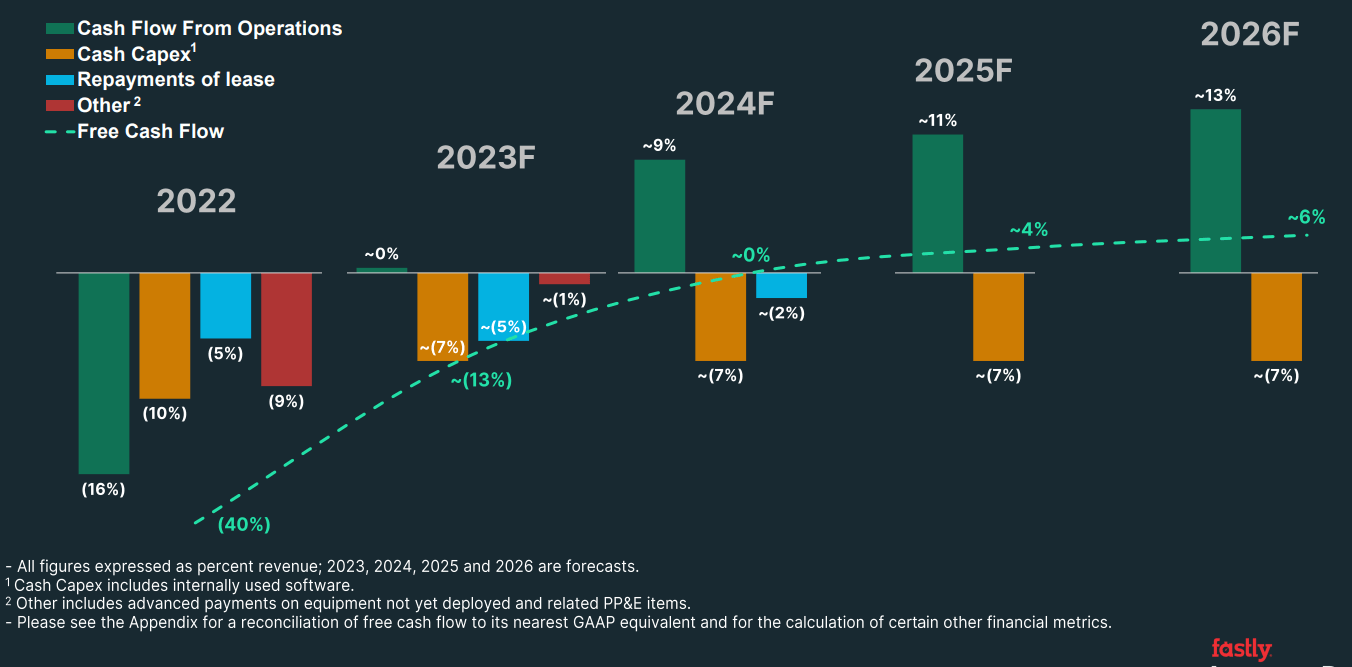

While Fastly is still free cash flow negative, the firm's management has laid out an aggressive plan to drive the company to FCF profitability by FY 2024… driven by aggressive operating cost cuts, product innovation and strong customer retention/monetization. If Fastly finally achieves FCF profitability next year, I can see shares of the company revalue sharply higher.

{kind=link}

Fastly's outlook for FY 2023 and analyst expectations

Fastly expects $495-505M in annual revenues for its current fiscal year which implies a year over year growth rate of 16%. In FY 2022, Fastly grew its top line 22%. The moderation of top line growth is due to companies slowing their IT spending in a high-inflation world, a trend that has affected other companies in the cloud market as well.

Source: Fastly

Analysts expect Fastly to hit its revenue target of approximately $500M, at the mid-point, and revenue estimates have risen sharply in 2023. Consensus top line projections call for 15-16% annual growth in each of the next three years.

Fastly compared to rivals

Fastly's market cap has declined by 75% in the last three years, although shares did initially benefit from the pandemic-induced boom in cloud company valuations. I believe the large draw-down in Fastly's valuation combined with the company's double-digit revenue growth and clear path to free cash flow profitability make Fastly an interesting rebound investment in the edge computing space.

Shares of Fastly are currently valued at 3.4X forward revenues which is on about the same level as the valuation multiplier for Akamai Technologies ( AKAM ), a key rival of Fastly in the content delivery network sector. Other companies like Cloudflare ( NET ) achieve much higher valuation multipliers than both Fastly and Akamai Technologies. Although this is due to Cloudflare's expected growth being twice as high as Fastly's (around 30% annually), I believe Fastly's valuation has upside potential.

Risks with companies like Fastly

The biggest risk, in my opinion, for Fastly is that the firm has not yet achieved profitability, despite scaling its footprint in the Enterprise market in the last few years. Fastly has also seen a significant deceleration of its top line growth after the pandemic which is a key driver of Fastly's massive valuation loss since 2020. What would change my mind about Fastly is if the company failed to achieve its FCF target in FY 2024.

Final thoughts

In my opinion, Fastly is a promising recovery investment for investors that focus on cloud-based growth companies. While it is true that Fastly has seen a moderation of its revenue growth in recent years, the company is still growing revenues at double-digit rates annually and continues to achieve strong growth in the Enterprise market. Fastly is also rapidly approaching an inflection point -- free cash flow profitability (projected for FY 2024) -- which, once achieved, could result in a major revaluation of Fastly's shares. For those reasons, I believe that Fastly has considerable rebound potential after a near-80% decline in the company's share price!

For further details see:

Fastly: Nearing A Critical Inflection Point