FSLY - Fastly: Strong Q2 But Now Expensive (Rating Downgrade)

2023-08-05 08:25:17 ET

Summary

- Fastly reported a Q2'23 revenue re-acceleration and beat its own guidance due to strong performance in the Enterprise segment.

- Fastly further achieved positive adjusted EBITDA and raised its top line guidance for FY 2023.

- Customer monetization also improved with Fastly's DBNER figure rebounding 2 PP to 123%.

- Shares soared 23% on Thursday and shares are now expensive. I'd wait for a correction before starting a new position.

Fastly ( FSLY )’s shares soared more than 23% after the cloud edge computing firm presented better than expected second-quarter results on Thursday and submitted a raised revenue outlook for FY 2023. With investor optimism soaring and shares becoming overbought in the short term, I am down-grading FSLY to hold. I previously rated the company a buy due to rapidly growing customer accounts and because the firm was moving towards EBITDA profitability. I consider FSLY to be a high-risk, high-reward investment in the cloud edge computing market and, given the strong increase in pricing after Q2’23 results, I believe investors should maybe wait for a correction before buying shares in the company!

Fastly beat on revenues and earnings

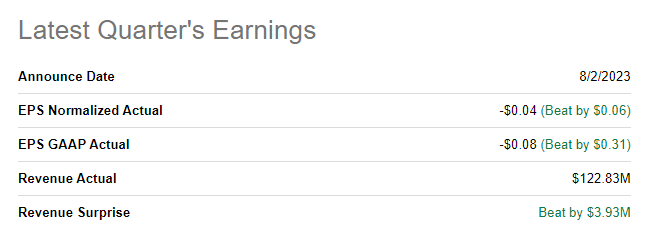

Fastly reported a top and bottom line beat for the second-quarter which, together with a raised guidance for FY 2023, helped reinvigorate investor optimism about the company’s growth prospects in its cloud edge computing market. Fastly reported an adjusted loss of $(0.04) per-share, which beat the consensus estimate by $0.06 per-share, on revenues of $122.8M... which also beat estimates (as well as Fastly's guidance).

{kind=link}

Strong Q2 results and milestone achievement of positive adjusted EBITDA

Fastly’s second-quarter earnings sheet was solid and the company reported a number of achievements in Q2’23.

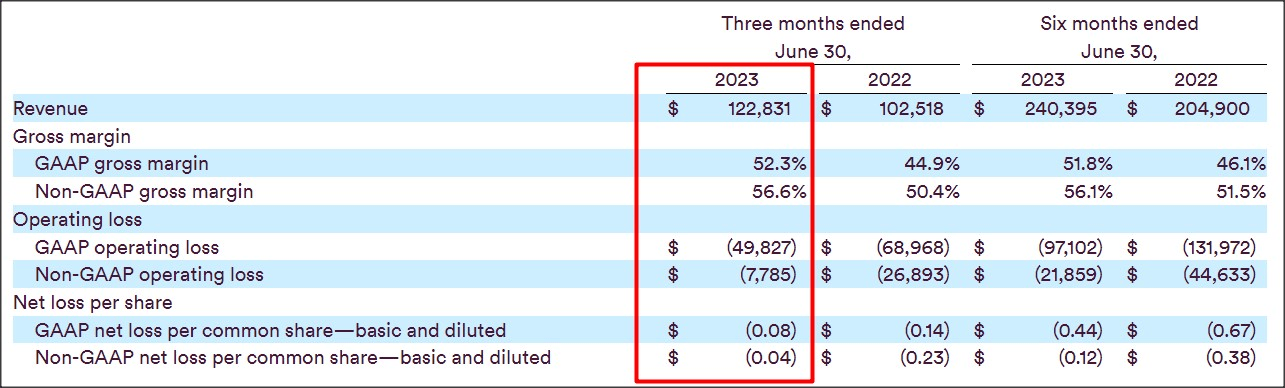

First, Fastly generated 20% year over year top line growth in the second-quarter, reaching record revenues of $122.8M and beating its own guidance. In Q1’23, Fastly guided for a revenue range of $117-120M and the company's second-quarter revenues came in 2.8M above guidance. Additionally, Fastly saw a re-acceleration of its top line growth in Q2’23 after the cloud firm saw only 15% growth in Q1’23. This growth has been driven by an increase in enterprise customers as well as improving customer monetization.

{kind=link}

Improving customer monetization, driven by Enterprise

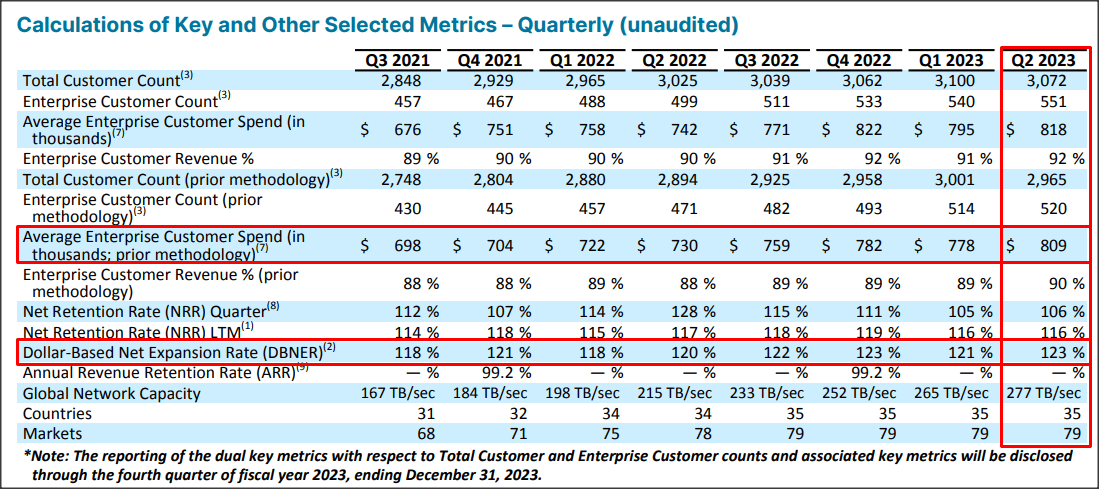

The really positive news for me was that the company saw an uptick in its dollar-based net expansion rate (DBNER)... which measures customer monetization success. The DBNER figure measures to what extent existing companies are ramping up their product spend from one reporting to the next. In Q2'23, Fastly's customers spent 23% more on Fastly's products and services than in the previous year, meaning the DBNER figure increased 2 PP quarter over quarter. This growth is chiefly driven by Fastly's enterprise segment which has seen customer growth (10% Y/Y) and increasing enterprise spend (11% Y/Y).

{kind=link}

Free cash flow

In my last work on Fastly I indicated that the company has a free cash flow problem in the sense that it did not generate positive FCF in any quarter in the last five quarters… a trend that unfortunately continued in Q2’23. Fastly generated $25.2M in negative free cash flow in the second-quarter, which was only slightly below last year’s free cash flow loss of $26.5M. However, Fastly confirmed on its investor day that it expects to achieve free cash flow breakeven in FY 2024 ( Source ).

{kind=link}

Fastly raises FY 2023 guidance and finally achieves positive EBITDA

Given Fastly’s revenue momentum and re-acceleration of growth in the second-quarter, the company felt confident enough to raise its top line outlook for FY 2023. Fastly now expects $500-510M in revenues in the current fiscal year which compares against a prior forecast of $495-505M. Fastly now also expects a narrower non-GAAP operating loss of $(49)-(43)M compared to earlier guidance of $(53)-(47)M.

Source: Fastly

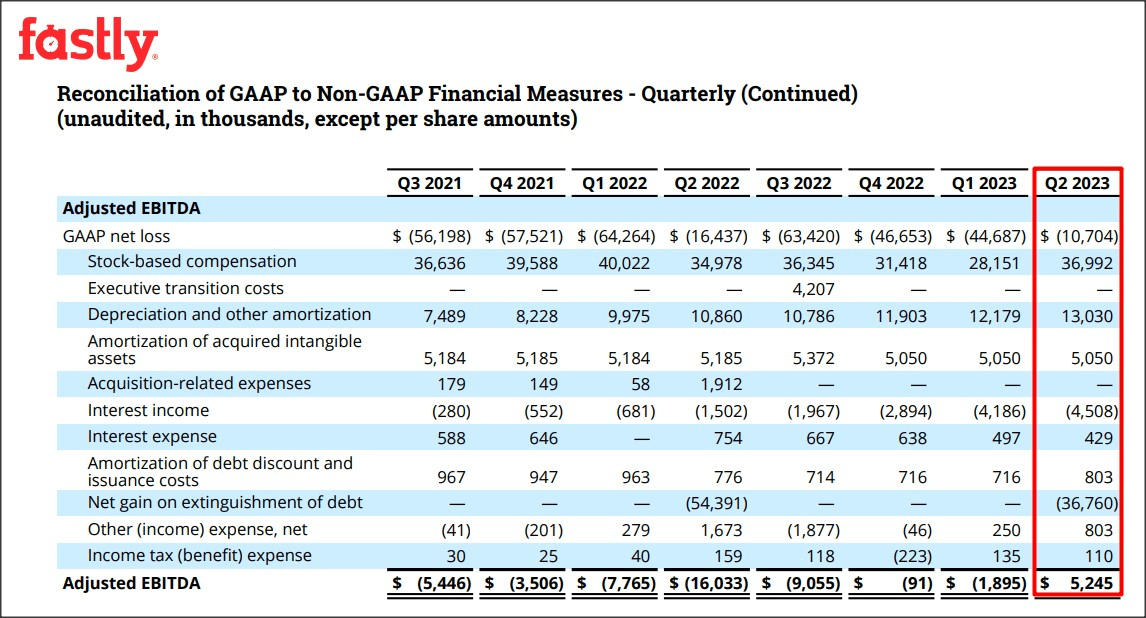

An improving earnings picture is what I believe could drive Fastly’s upside revaluation in the longer term. Lower losses will chiefly be driven by an improving cost structure as well as continual momentum in the enterprise segment. In the second-quarter Fastly already achieved a major milestone: it reported positive adjusted EBITDA (of $5.2M) which likely explains the rapid improvement of investor sentiment on Thursday.

{kind=link}

Fastly’s valuation

Given the improved revenue outlook and EBITDA situation for Fastly, I would expect analysts to upgrade Fastly's revenue estimates for FY 2024 in the near-term. Analysts currently expect $584M in revenues next year, implying 16% growth. The company's guidance for FY 2023 implies a revenue growth rate of 17% Y/Y.

Fastly is not expensive and cloud companies typically don't tend to be. Fastly is valued at 4.5X FY 2024 revenues, showing a 32% increase since I last took a look at the company in June. Given that Fastly is trading well above its 1-year average P/S ratio of 2.8X, I believe a rating down-grade is warranted and I would look to engage at the $16-17 support level.

Risks with Fastly

I see two big risks with Fastly at the moment, although the overall earnings picture has improved. First, Fastly is not yet profitable on a GAAP basis and free cash flow remains negative. If Fastly fails to achieve FCF profitability in FY 2024, investors may not react kindly to such a development. Second, Fastly’s monetization success is chiefly measured by its dollar-based net expansion rate. A drop below 120% is what I would consider to be a warning sign that the monetization situation is deteriorating.

Closing thoughts

Fastly reported a solid earnings sheet for the second-quarter that included a re-accelerating top line, driven by gains in the enterprise market, a raised guidance for FY 2023, positive adjusted EBITDA and a rebound in the DBNER figure. On the other hand, the company’s valuation has increased significantly lately which I believe translates into an unattractive risk profile for those investors that have not yet build a position in the cloud edge company. I am rating Fastly as a hold now and would recommend investors interested in FSLY to wait for a correction before engaging!

For further details see:

Fastly: Strong Q2, But Now Expensive (Rating Downgrade)