FSLY - Fastly: To Old Highs With New CEO?

2023-07-17 17:50:00 ET

Summary

- Once an obscure company, Fastly gained widespread attention during the pandemic but suffered a steep decline.

- The appointment of Todd Nightingale as CEO sparked a transformation, leading to a rise in share prices and the unveiling of ambitious long-term plans at its Investors Day.

- With regard to some key metrics indicating accelerating growth in the upcoming quarters and potential breakeven in free cash flow by 2026, a compelling investment case arises.

- Valuation suggests there's still upside potential, but more positive surprises might be needed for an attractive long-term investment.

Before 2020, Fastly ( FSLY ) was a relatively unknown company that gained significant media attention due to the expected push toward digitalization brought on by the COVID-19 pandemic. However, despite high market expectations and claims, the company was unable to meet them, resulting in a rapid decline in its share price.

The sell-off was not just due to a shift in market sentiment, but also due to internal problems such as poor management, rising losses, and weak growth rates. In September 2022, Todd Nightingale was appointed as the new CEO, resulting in a rise in share prices and a presentation of concrete plans and goals at the Investors Day. However, the question remains whether this is enough to sustain long-term interest from investors.

Fastly's business model can essentially be summarized as follows:

Fastly is a cutting-edge technology company that has become a vital player in the digital landscape. As a content delivery network (CDN) provider, Fastly enables businesses to deliver their digital content to users with unparalleled speed, reliability, and security. Utilizing their innovative edge cloud platform, Fastly optimizes the performance of websites, applications, and streaming services by caching and distributing content closer to end-users worldwide.

Renowned for its real-time capabilities and intelligent edge computing solutions, Fastly has rapidly established itself as a critical partner for organizations seeking to enhance user experiences and maintain seamless online operations. With a reputation for pushing the boundaries of web delivery, Fastly continues to reshape the internet landscape, empowering businesses to thrive in the fast-paced digital era.

If you only look at the share price, the era of ex-Ceo Joshua Bixby can only be described as a roller coaster ride. Immediately after his arrival, the share price multiplied by several 100%, only to slide back to the original level and even below within a year.

In the end, the share price was even 50% below its initial level. As an example, I believe one can show the development of GAAP earnings to illustrate the apparent dissatisfaction of investors.

Data from Fastly Earnings Statements, figure from author

{kind=link}

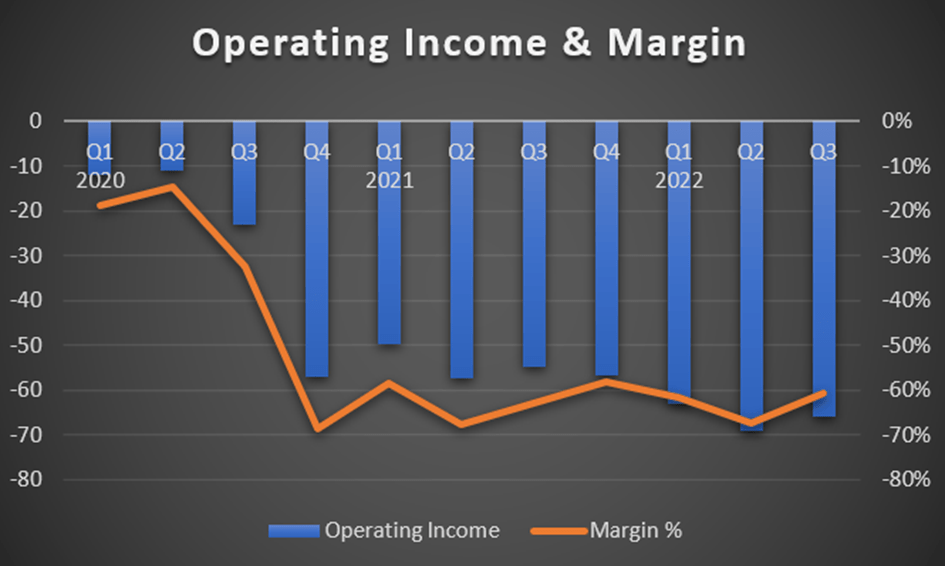

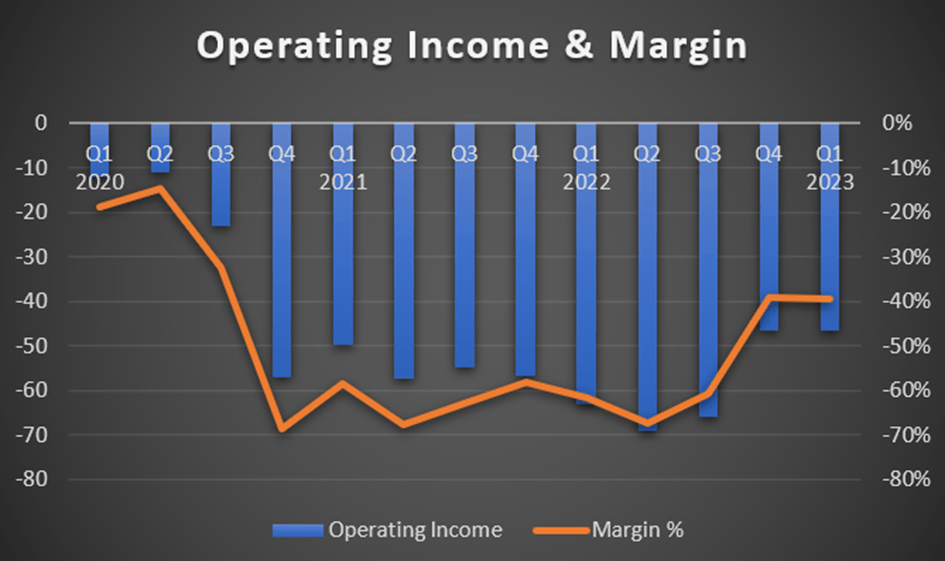

Almost exactly at the same time as Todd Nightingale took over, the share price stopped its downward trend and even built up a nice momentum in 2023 so far.

Within two quarters, the company has already managed to improve the operating margin by 20 percentage points.

Data from Fastly Earnings Statements, figure from author

{kind=link}

At -40%, it is of course still very disastrous, but at least you get the feeling that they are now trying to get a grip on costs and pursue the long-term goal of profitability.

But how sustainable is this development? To find out, we first have to take a closer look at the company's key operating figures.

Financial Summary - Still many question marks

The company's revenue increased by 15% year-over-year to $117.5 million. This number was the weakest growth rate since Q2 2021 which was only so low at that time due to the direct comparison to the strong Q2 2020. In Q4 2022, the annual growth rate was still 22%, to that extent a significant decline in growth can be seen here. As already shown, the operating loss of -$46.5 million is still miles away from break-even but still represents a significant improvement compared to the previous year's figure of -$63 million.

This was achieved thanks to an increase in gross margin of 400 bps to 51.3% and significant cutbacks in G&A and R&D. A primary driver here was also the reduction in stock-based compensation by 30% from $40 million to $28 million. However, even after the cost reductions and various adjustments, the non-GAAP margin remains at -12% and does not indicate a timely break-even.

The outlook for the full year was left unchanged, which could almost be considered a surprise after the Bixby era. On average, revenue is expected to increase by 15.7% to $500 million with a non-GAAP margin of -10%. This at least induces further cost optimizations in the year even if growth remains weak.

Looking at the key performance numbers, one can at least see that some relevant trends are still intact. The Dollar-Based Net Expansion Rate has stabilized at 120% for several quarters, indicating that Fastly's existing customers have spent on average 20% more than in the previous year.

Data from Fastly Earnings Statements, figure from author

This speaks to satisfied existing customers who continue to drive growth post-acquisition. The growth rate of enterprise customers has also held reasonably steady at 12% for several quarters.

Overall, Fastly now has 514 enterprise customers out of 3001 total customers. Average Enterprise customer spending is up 8% to $778,000. Sequentially, however, this was a small decline. The next few quarters will have to show how the trend plays out here.

Somewhat disappointing, on the other hand, is the trend in total customers, which has been growing sequentially at only 1% for some time, indicating that non-enterprise customers do not prefer Fastly's offerings or generally perceive the offerings of enterprise customers as more attractive.

Overall, these are not numbers where a potential growth investor would want to jump in immediately. On the other hand, the numbers are still okay for a turnaround candidate and leave some room for speculation. At the last Investors Day, Fastly presented its new medium-term strategy for the next few years, which looks quite interesting.

Fastly's medium-term path - Ambitious but not far-fetched

Unlike the old target of $1 billion in revenue by 2025 which the old CEO held on to until 2022 (As a reminder, Fastly is aiming for just $500 million in 2023), instead of continuing to focus on just one metric and everything being purely about growth, a compromise between growth and profitability is now to be achieved. On the one hand, the company wants to break even in terms of operating profit soon by further expanding the gross margin and reducing operating costs.

Fastly Investors Day 2023

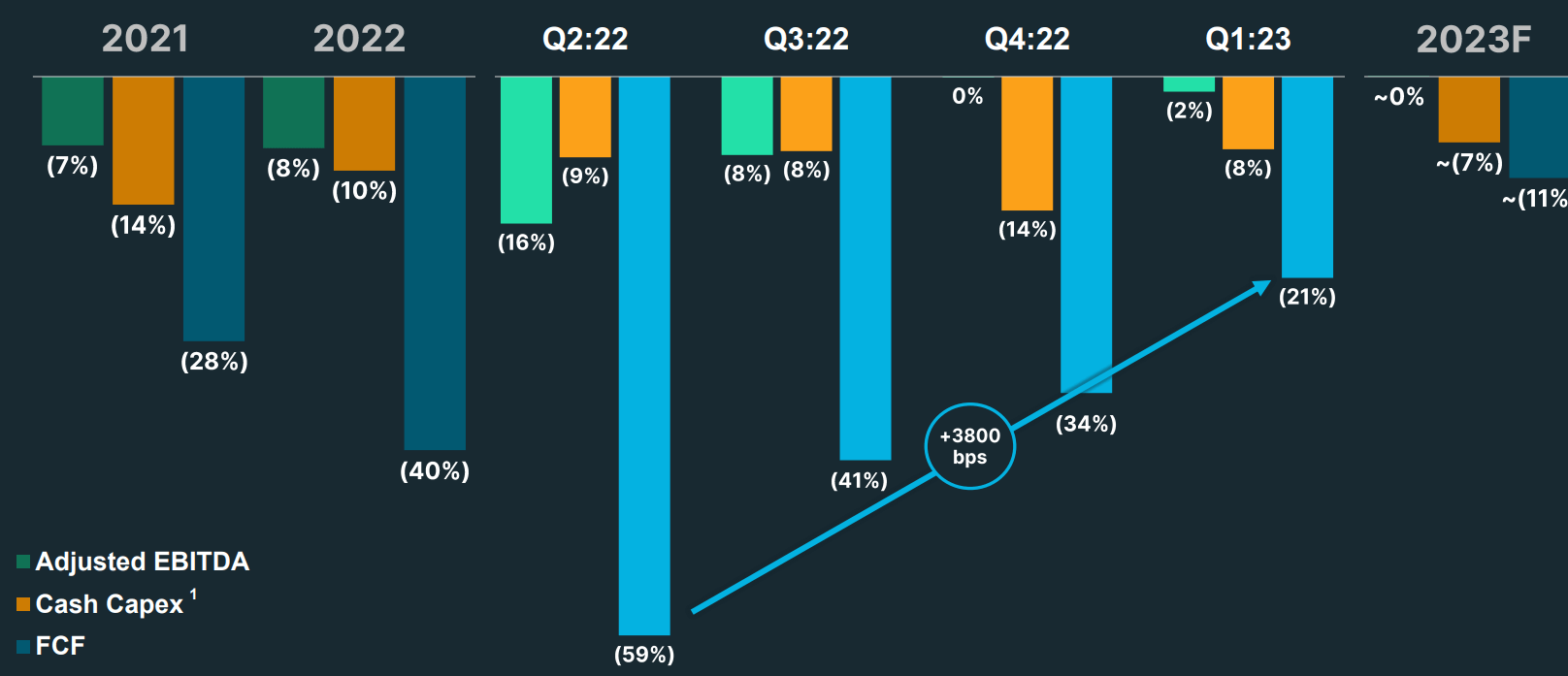

By 2026, the company aims to achieve a gross margin of 65% (currently 54% over the last four quarters). Furthermore, the management emphasizes that there is savings potential in CAPEX and that these are to be reduced from 14% and 10% of sales to 7% in the coming years and maintained. 2023 is now planned with break-even in operating cash flow as well as in Adjusted EBITDA.

{kind=link}

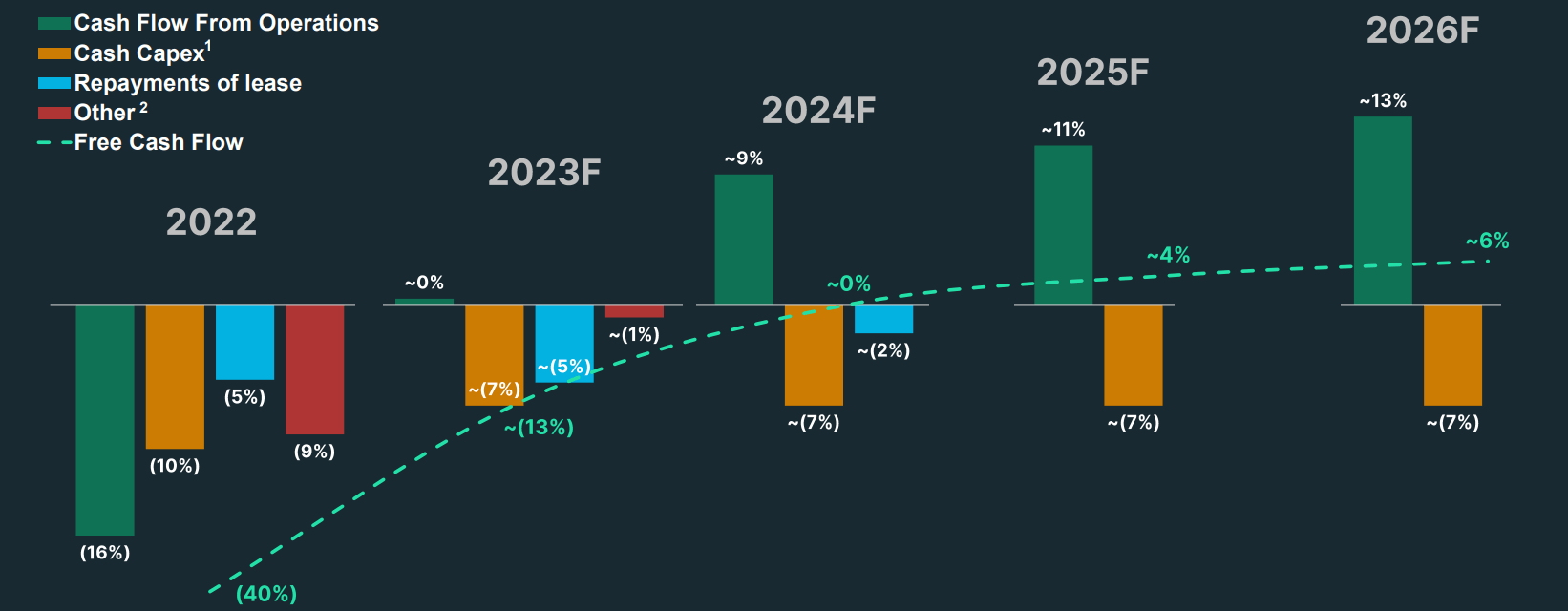

This would be a massive improvement, especially in operating cash flow, after the margin was still -16% in 2022. As early as 2024, management would like even free cash flow to reach breakeven. That would be very impressive and certainly, an undertaking that investors would have considered impossible a year ago because of a free cash flow margin of -40%. In 2026, the free cash flow margin should then be 6%.

{kind=link}

To achieve this, however, more than cost reductions are necessary, growth is just as important to achieve economies of scale. Here, the company sets a target of $800-900 million by 2026, which is admittedly a very wide range. On average, however, this results in a CAGR of 20% from 2024-2026, and would thus indicate a revival of growth rates. But where will the growth come from?

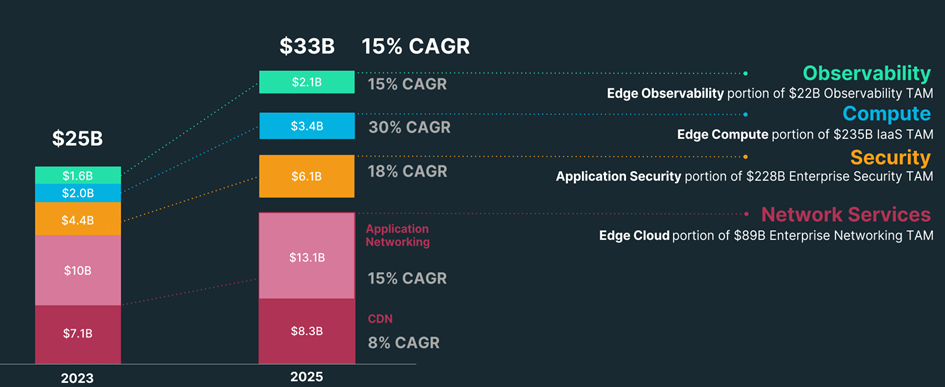

Fastly plans to increasingly differentiate itself from the rather low-growth CDN business and strives to enter new markets with higher growth rates.

{kind=link}

All four of Fastly's target markets currently add up to a total addressable market of $25 billion and are estimated to grow by an average of 15% annually. The compute sector in particular is growing at an above-average rate of 30%, and the company sees itself strongly positioned here with its own Cloud Edge.

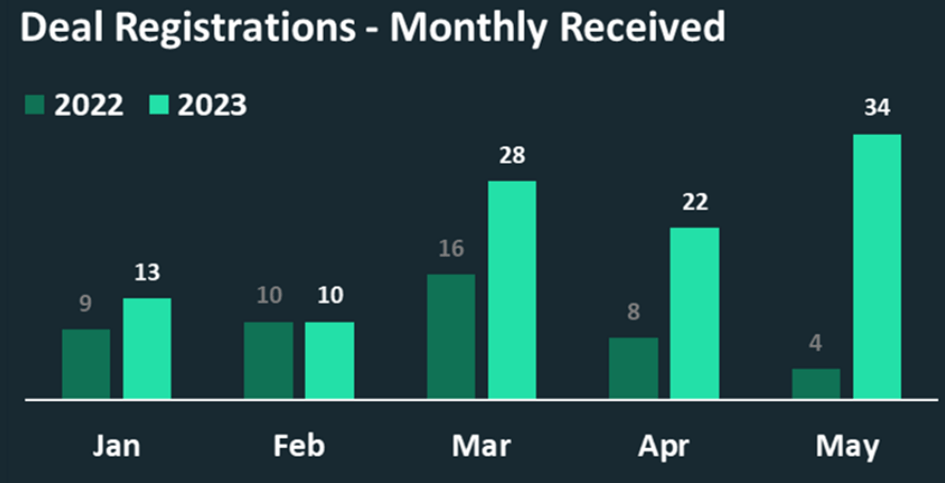

The company does not only refer to potential growth rates but can also present some key figures which support the thesis that growth is accelerating again. For example, there are deal registrations, which have been massively above the previous month's figures, especially in the last few months.

{kind=link}

This does not mean that these are all new customers, but at least it shows a strong increase in interest in Fastly's services. It also speaks for a strong marketing and sales strategy, even though costs have been cut in recent quarters.

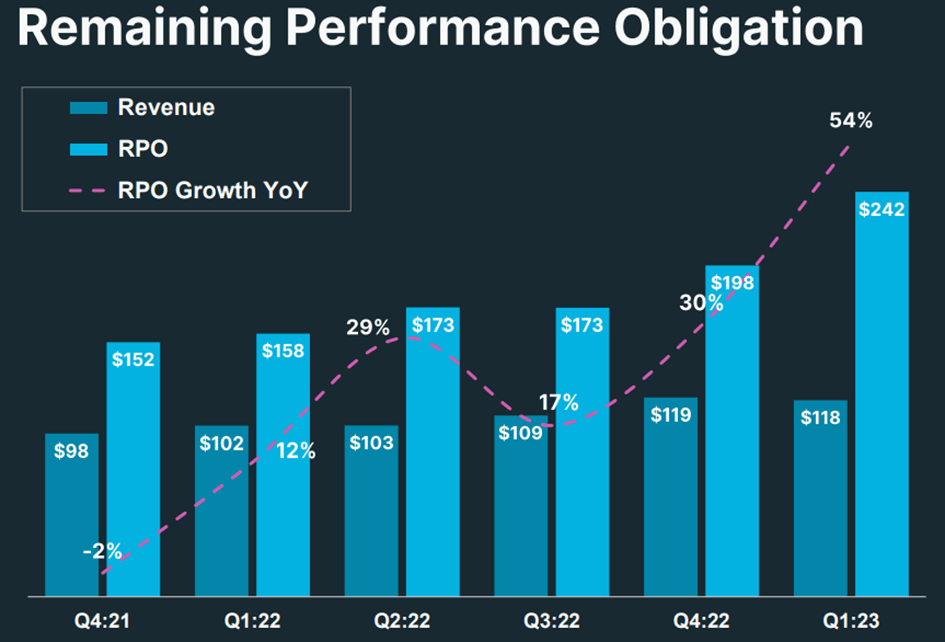

Another reason for some optimism is the recent development of RPO. This very relevant metric for software companies, which is composed of deferred revenue and order backlog, is usually not published by Fastly.

{kind=link}

This had its reasons, as the RPO growth in Q4 2021, for example, was negative. However, in the last two quarters, the growth has accelerated massively, reaching an impressive $242 million in Q1 2023, representing 54% growth. Deferred revenue was $26.8 million in the last quarter, putting the order backlog at $215.2 million. This should not be overstated at first, due to the high fluctuations in the last quarters but it strengthens the thesis of resurgent growth and thus feeds a hope that has not been present at Fastly for a while.

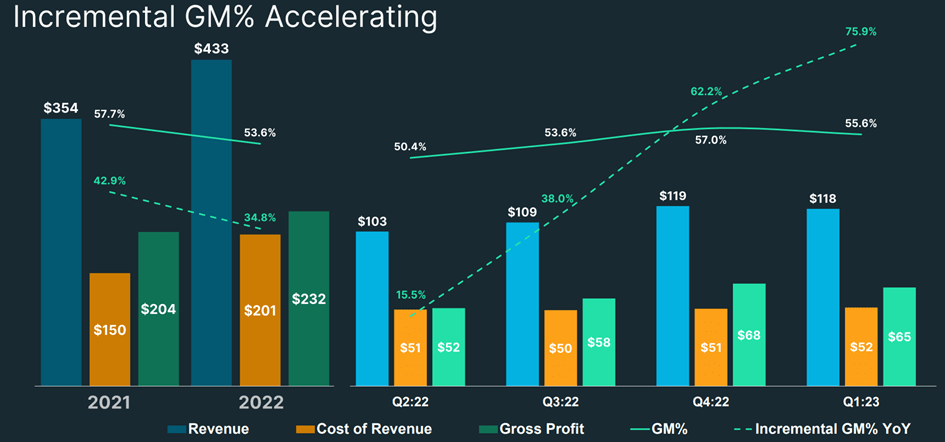

Finally, the development of the Incremental Gross Margin gives reason to believe that the Gross Margin can indeed be increased significantly in the future and that Fastly will finally reach a certain level of scalability. Incremental Gross Margin refers to the additional gross margin that a company generates by selling an additional unit of a product or service. If this is above the Gross Margin, it indicates that a company is better managing its direct costs while achieving attractive selling prices.

{kind=link}

At Fastly, this Incremental Gross Margin was quite significantly below the total Gross Margin before Todd Nightingale took over, which would have been a big warning sign (15% in Q2 2022). It appears that management was trying to push customer growth through low selling prices without regard to costs. Under Nightingale, Fastly achieved an Incremental Gross Margin of 75.9% in Q1, which is very impressive for this short time.

Accordingly, Fastly currently appears to be building momentum in its core business that has not been seen since 2020. Against this backdrop, the management's ambitious targets seem realistic and there is a certain chance that Fastly can achieve a turnaround. But to what extent does this also mean a win for shareholders? How much is already priced in?

Valuation

A valuation based on conventional ratios is almost impossible for Fastly, as they are currently neither EBITDA, EBIT, or cash flow positive, which is why only EV/Sales remains as a ratio. The problem with this metric is the high room for interpretation. With a current value of 5.3, one could argue that it is just a quarter of Cloudflare ( NET ) and thus should be considered favorable.

However, one could also argue that Cloudflare is operating at growth rates beyond 30%, should become GAAP profitable this year, and is not a turnaround case. However, since these considerations are not very helpful when looking at Fastly, I will use a discounted cash flow model.

To do so, I make the following assumptions.

- Revenues grow 19% annually from 2023-2026, and 15% annually through 2031.

- Gross margin increases to 65% by 2026 and can be increased to 70% by 2031.

- OPEX fall to 58% of sales by 2026, and 50% by 2031.

- CAPEX remains at 7% of sales.

- Amortization slowly decreasing to 10% of sales.

- Tax rate 22.

- WACC 11.

- Terminal growth rate 3%.

The assumptions up to 2026 are essentially in line with management's targets. The estimates up to 2031 build on these. The WACC of 11% reflects the increased risk compared to comparable stocks. The assumptions result in a price target of $24, which represents a 40% premium to the current price.

Thus, while Fastly still has potential at the current price level, it is not excessive when measured against the expected volatility. The next few quarters will be decisive in determining whether the momentum will be maintained and whether a major turnaround is indeed imminent.

The bottom line

Overall, I believe the new CEO has made impressive progress in turning Fastly around and restructuring the company within just two quarters. Despite cutting costs, indicators are pointing towards increased growth and capable management. While the goal of breaking even on free cash flow by 2025 with 20% growth is ambitious, it is also realistic. However, the stock has already been in a good run and there are still some uncertainties in financial measures.

Based on the analysis of free cash flow, there is still potential for increases in the share price, but it may require several higher growth rates for a complete turnaround. Currently, due to Fastly's strong key figures, I rate the company as a buy for the moment. There is potential for positive surprises in the upcoming quarters, making it a promising investment. In the medium term, the company needs to demonstrate that the current demand trends are sustainable and can revive the Fastly brand.

For further details see:

Fastly: To Old Highs With New CEO?