FSLY - Fastly: Turnaround With Solid Enterprise Customer Growth

Summary

- Fastly is a leading CDN provider which operates a fast footprint of data center services across the globe.

- The company reported strong results for fourth quarter 2022 as it beat both revenue and earnings growth estimates.

- Its stock is undervalued intrinsically, relative to historic multiples and relative to its competitor Cloudflare.

- Fastly has continued to grow its enterprise customer base, which will likely increase retention rates and expansion opportunities for the future.

Fastly ( FSLY ) is a content delivery network [CDN] provider which enables fast and secure website/app performance across the globe. The company basically operates by storing a "cached" version of websites across a global footprint of data centers, so it can be accessed in rapid time. The business has more than 2,900 customers with many well-known brands from Reddit to Stripe and even the New York Times. Fastly also is the No. 1 rated Gartner leader in CDNs (by customer reviews) with 4.9 stars out of 5. This is much greater than competitor Akamai and Cloudflare which have 4.7 and 4.6 stars out of 5, respectively. Interestingly enough this is despite Cloudflare having a more expensive valuation on a price to sales ratio (I will discuss more on this later).

{kind=link}

CDN Provider (Gartner)

Fastly has recently reported strong results for the fourth quarter as it beat both top and bottom line growth estimates. In this post I'm going to break down its fourth quarter financials and valuation using my discounted cash flow model and forecasts.

Fourth Quarter Financials

Fastly reported strong financial results for the fourth quarter of 2022. Its revenue was $119.3 million which surpassed analyst estimates by $4.77 million and increased by a solid 22% year over year. This was driven by steady customer growth of ~5% year over year. Notable wins included the Duolingo language learning app, Civitatis, an online travel provider, a popular online grocery delivery company and many more. We can see straight away that Fastly's revenue basis is now extremely diverse across multiple industries and ~79 markets. This is a positive for stability, especially given the company lost TikTok as a major customer in 2020, which butchered the stock price at the time.

{kind=link}

Customer Wins (Q4,22 report)

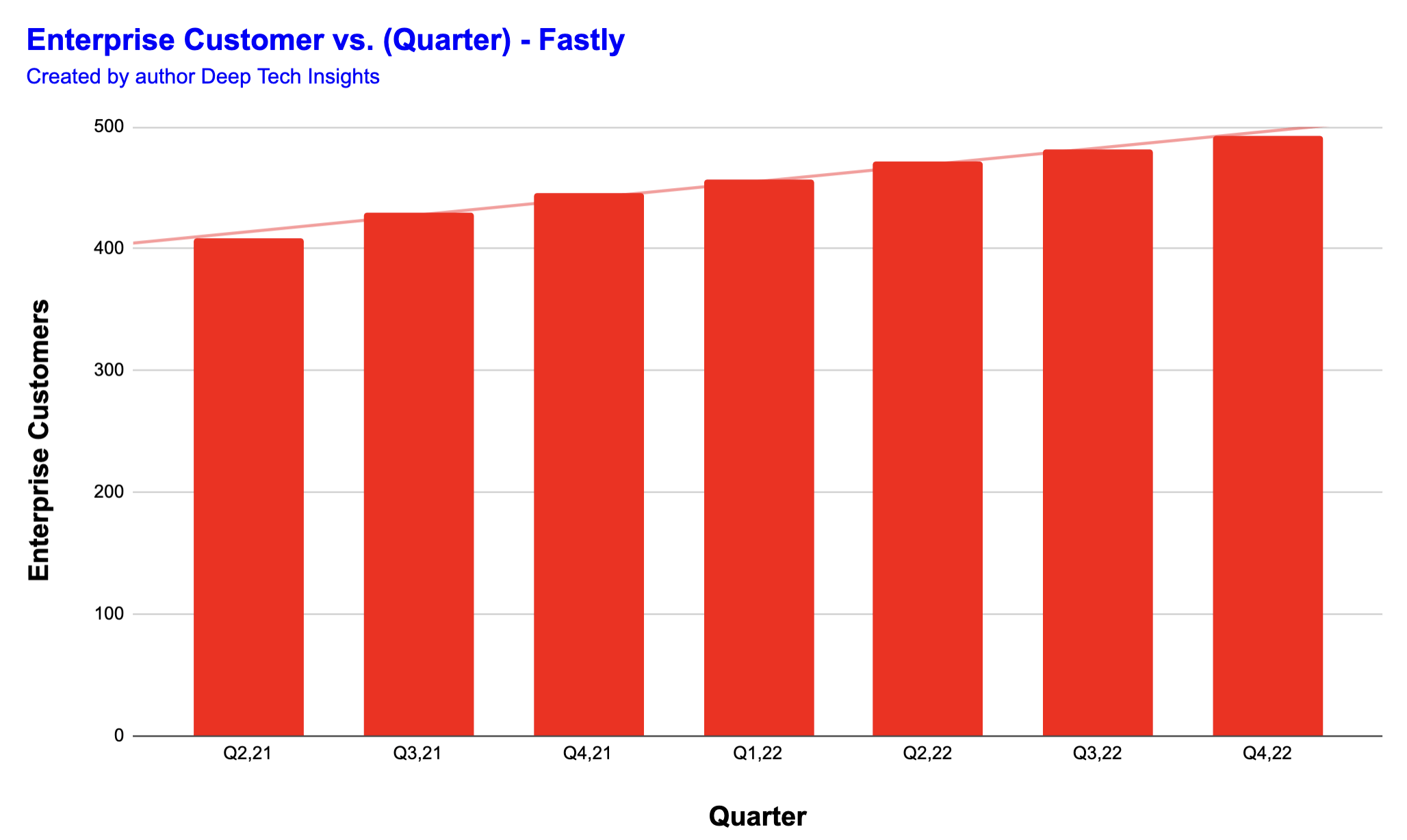

Another positive for Fastly , is I noticed its enterprise customer count has increased from 445 to 493, or 10.79% year over year. It's a major positive to see its enterprise customers growing at a faster levels than its overall customer base. This is because larger organizations (Enterprises) tend to be more "sticky" by nature with a mature, stable business. I have taken the time to create a unique chart plotting the enterprise customer growth, as Fastly hasn't provided charts in its earnings. From the light red trendline you can see this is clearly upwards.

{kind=link}

Fastly Enterprise Customers (Created by author Deep Tech Insights)

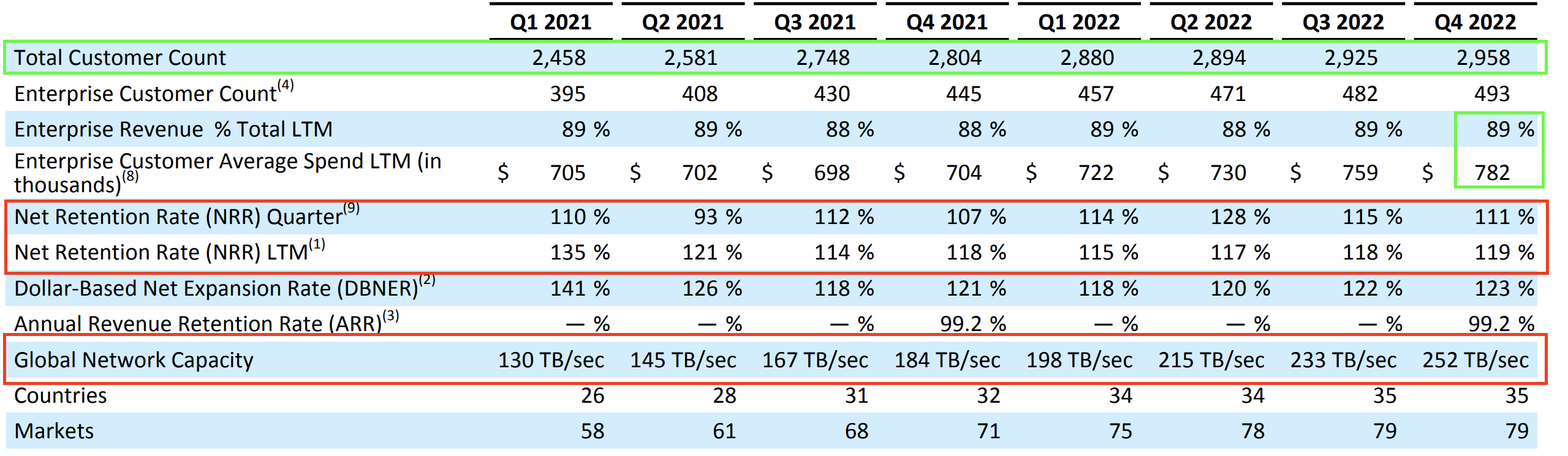

As someone who has first-hand experience working with enterprises from a "digital transformation/cloud" perspective, I know they tend to have large bureaucracy's and can be slow to change. This means they can be hard to sign up initially, but once you lock them in as a customer, high retention is expected. For example, Fastly reported an overall net dollar retention rate of 119% in the trailing 12 months, which is up 1% year over year. This means customers are staying with the company and spending more through product/bandwidth growth, even despite the "recessionary" backdrop. As its enterprise customers expand and economic conditions improve, I expect this figure to increase for its overall customer base.

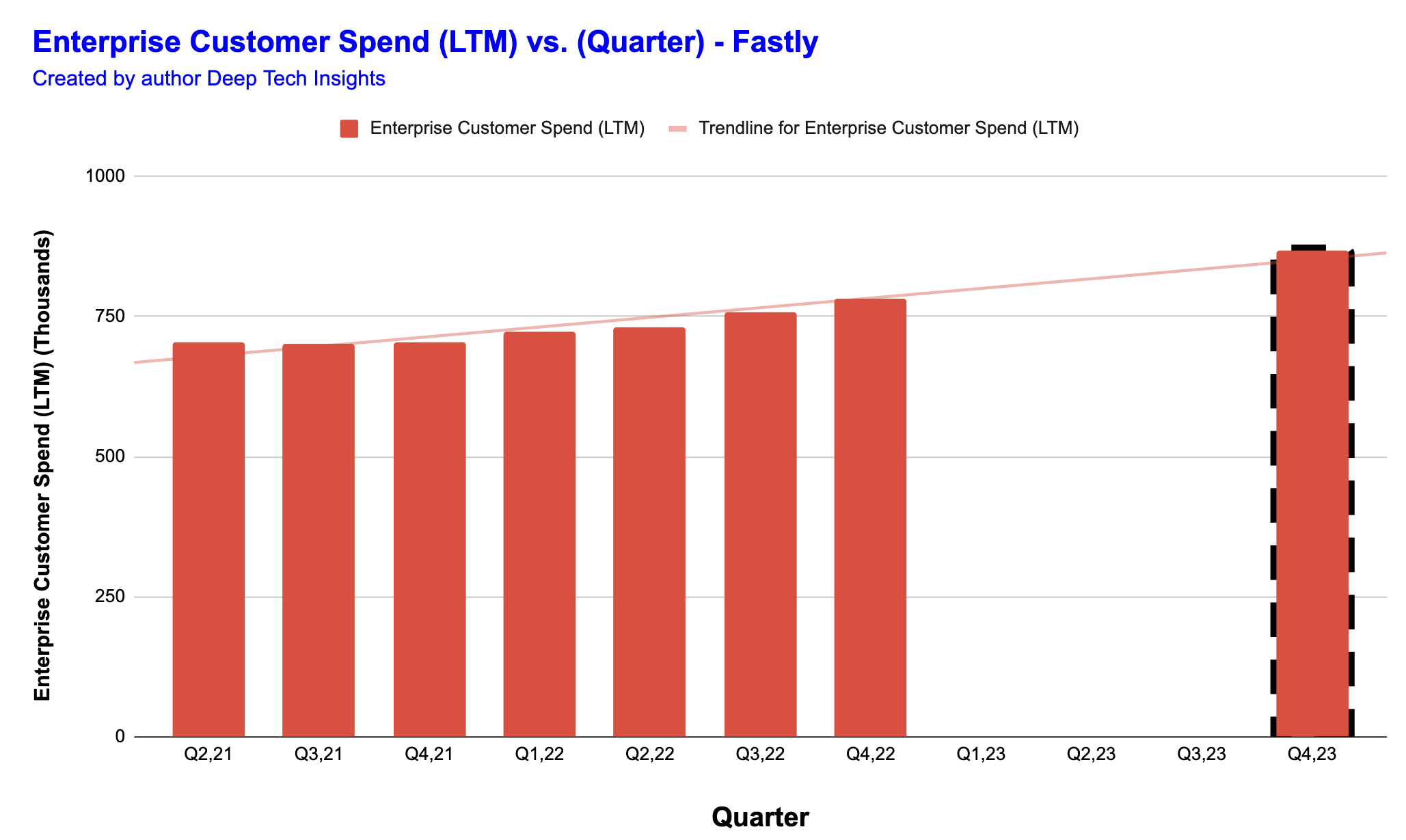

Large organizations offer vast account expansion opportunities across multiple parts of the business. For example, Fastly reported its Enterprise customer average spend (last 12 months) jumped from $704,000 in Q4,21 to $782,000 by Q4,22, or 11% year over year. For extra clarity, I have plotted a graph of the enterprise customer spend and extrapolated out the recent growth rate, but slightly lower at 10.9% year over year for my forecast (dotted line column). Utilizing this forecast I estimate 868 enterprise customers by Q4,23, as per the current trend. I will discuss more on this in the "valuation and forecasts" section.

{kind=link}

Enterprise Customer Spend (Created by author Deep Tech Insights)

Notable Product Improvements

In order for a technology/software company be successful, they must continually invest into infrastructure improvements and capacity. In this case, Cloudflare has increased its Global Network Capacity from 184 TB/Sec to 252 TB/Sec or a rapid 36.96% year over year. This is fantastic to see and should provide both peace of mind and better performance, for its customers, especially those in the enterprise which often demand strict SLA's or "Service Level Agreements."

The company also has continued to innovate on its security front and recently achieved Payment Card Industry Data Security (PCI DSS) compliance. This may seem like a small piece of news, but this is huge. PCI DSS is a standard related to the secure storage of credit card information which includes encryption, access controls, etc. Thus having compliance with this standard, means Fastly can be adopted by more e-commerce and payment companies much easier, expanding its total addressable market.

On a more technical front the company has improved its Web Application Firewall, or WAF, with automatic provisioning via Terraform. Web Application Firewalls help with the prevention of DDoS or Distributed Denial of Service attacks and are vital pieces of cybersecurity infrastructure. The integration with Terraform means cloud adaptability is much easier. Given the number of global cyber attacks increased by an eye watering 38% year over year in 2022, and cloud security is becoming vital, this was a great product improvement.

Margins and Balance Sheet

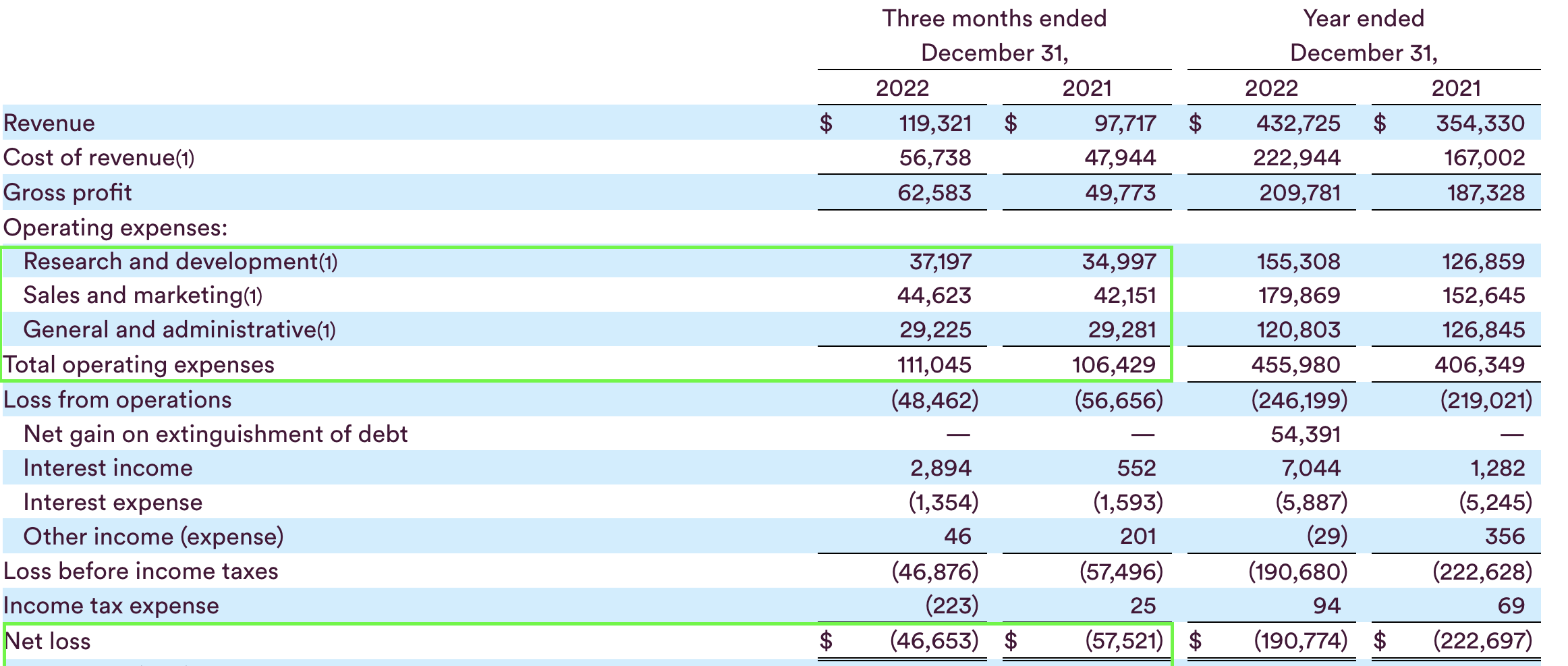

Moving onto profitability, the company reported a gross margin [GAAP] basis increase of 380 bps quarter over quarter, which was a positive sign. In addition, its GAAP operating losses have started to narrow from negative $56.65 million reported in Q4,21 to negative $48.46 million by Q4,22. This is a positive sign and indicates operating leverage as the business scales. Its operating expenses did increase slightly from $106.4 million to $111 million or 4% year over year, but revenue grew at a faster rate. In addition, its G&A expenses was slightly lower/flat, while its R&D expenses increased by ~6% year over year. I don't believe this is a bad sign, as the company must continually innovate to stay ahead of the competition and recent product improvements are testament to this. Overall EPS was negative $0.38, which beat analyst expectations by negative $0.10.

{kind=link}

Fastly expenses (Q4,22 report)

Fastly has a strong balance sheet with $518 million in cash and short-term investments. The company does have total debt of ~$833.5 million, but the majority of this ~$704 million looks to be long term debt. I believe this is manageable, especially given the company's losses are narrowing.

Valuation and Forecasts

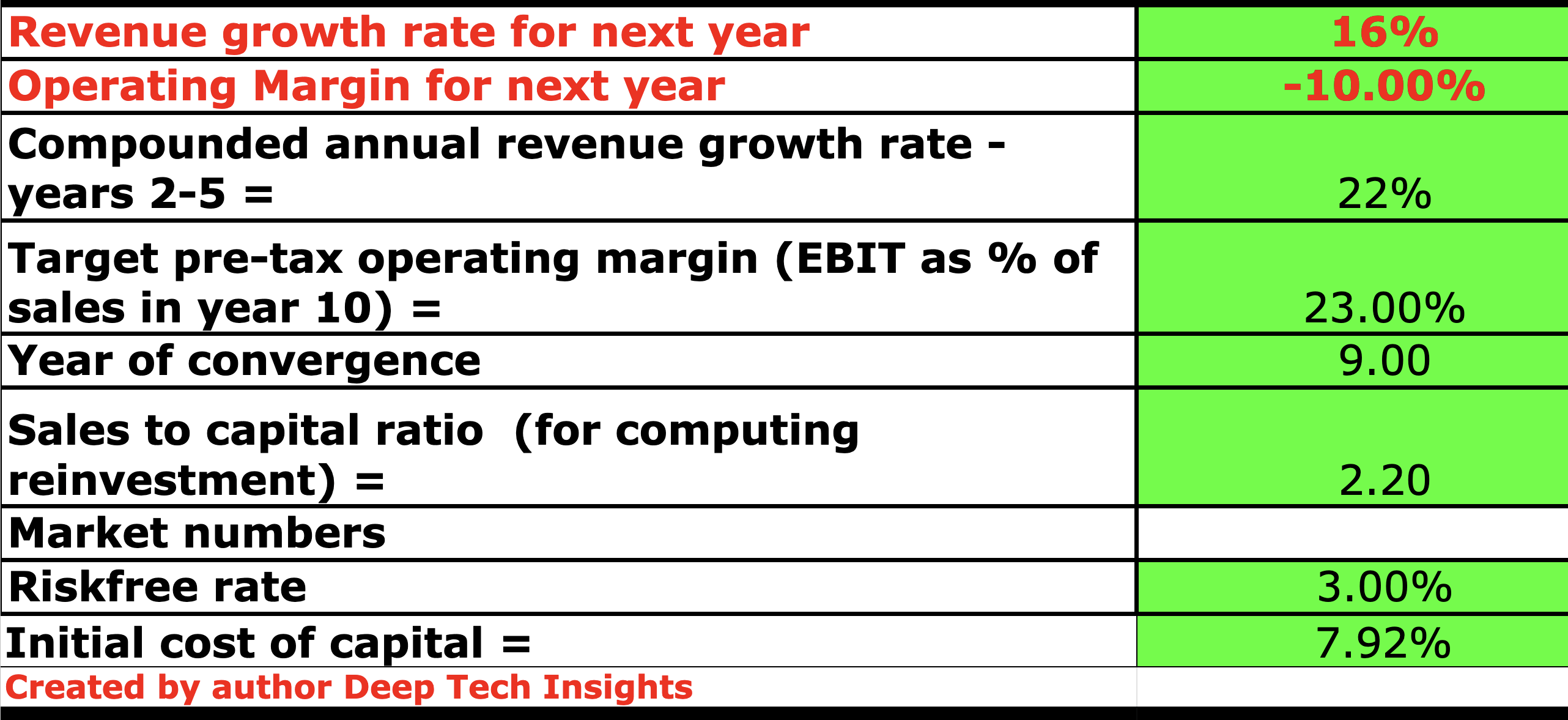

In order to value Fastly, I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 16% revenue growth for "next year," which refers to the full year of 2023. This is aligned with management guidance and I believe prudent based upon the forecasted "recession" which I will discuss more on in the "Risks" section. In years 2 to 5, I have forecast a much faster growth rate of 22% per year. This may seem optimistic, but it's in-line with the 22% growth rate reported in Q4,22 and slower than the staggering 45% revenue growth reported in 2020. I forecast this growth rate to be driven by improving economic conditions, the increasing need for Web security and performance and continued expansion into the enterprise.

{kind=link}

Fastly stock valuation 1 (Created by author Deep Tech Insights)

To increase the accuracy of my model, I have capitalized R&D expenses which has boosted net income. In addition, I have forecast a negative 10% operating margin for next year. This is based upon management's guidance at the midpoint and would represent an increase from the negative 18% reported in 2022. Management has made it a strategic priority to focus on cost efficiency and as mentioned prior its general and administrative expenses have been flat year over year. I have forecast a 23% operating margin over the next nine years. This is optimistic but based upon the average of the software industry. Given Fastly has built out its infrastructure footprint extensively and has a large enterprise customer base, with many expansion opportunities, this is not impossible.

{kind=link}

Fastly stock valuation 2 (created by author Deep Tech Insights)

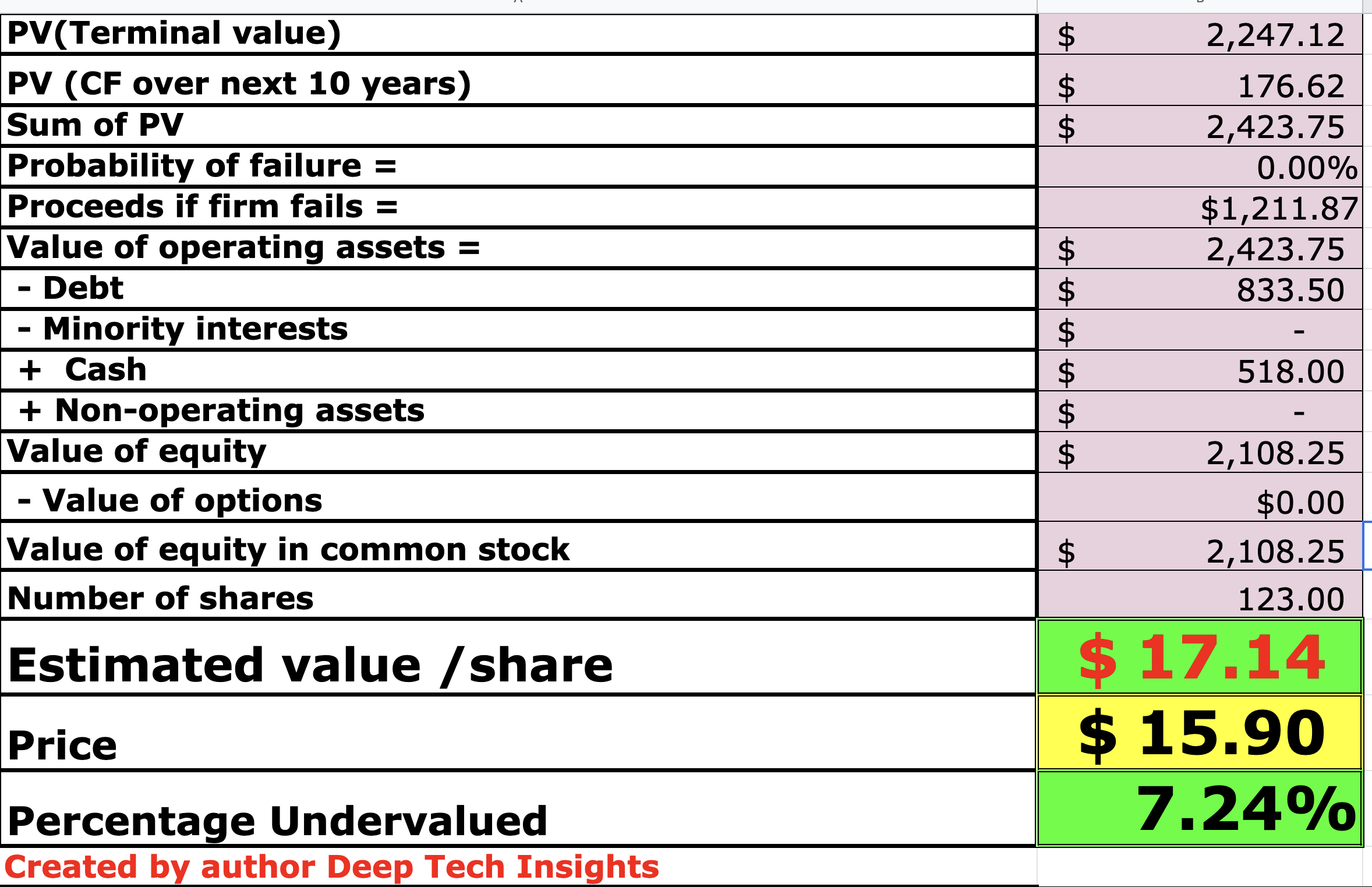

Given these factors I get a fair value of $17.14 per share, the stock is currently trading at $15.90 per share at the time of writing and thus it's ~7.24% undervalued.

As an extra datapoint, Fastly is trading at a price to sales ratio = 4.47, which is ~68% cheaper than its five-year average. The stock also is trading substantially cheaper than popular competitor Cloudflare ( NET ), which trades at a price to sales ratio = 15.94.

Risks

Recession/Lower Demand

Many analysts have forecast a recession in 2023 and we're already seeing a cyclical decline across the technology and e-commerce sectors. As Fastly charges based upon web "delivery traffic" with up to 3TB and up to 10TB packages, I believe the company will face lower demand in 2023 which I have reflected in my model forecasts.

Final Thoughts

Fastly has faced tough headwinds since its loss of TikTok as a customer in 2020. However, the company has continued to grow its core customer base with focused growth in the lucrative enterprise market. Its high retention and improving profitable is also a major positive. Given the stock is slightly undervalued in my model and trading much cheaper than competitors such as Cloudflare, while being highly rated in Gartner reviews, I believe the stock has all the ingredients of a turnaround story.

For further details see:

Fastly: Turnaround With Solid Enterprise Customer Growth