ET - FEI's Discount To NAV And Top Holding Make It Attractive

2023-09-18 20:50:21 ET

Summary

- First Trust MLP and Energy Income Fund Common is an attractive alternative to the Alerian MLP ETF for income-oriented investors who want high yield without K-1s.

- FEI's top holdings are generally very solid stocks.

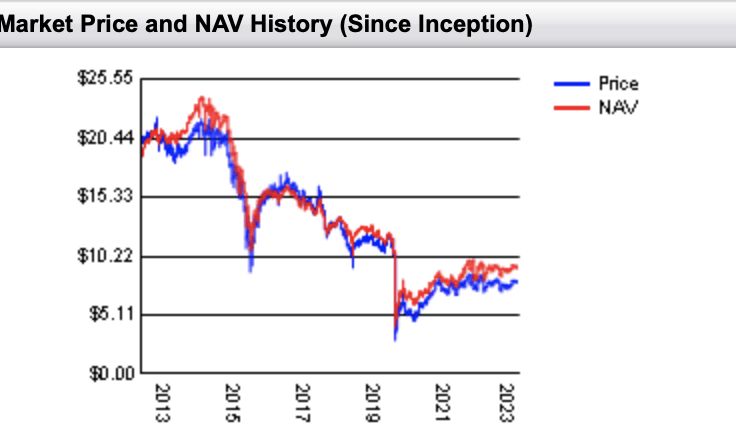

- FEI currently trades at a 13% discount to its NAV, making it an attractive option.

For income-oriented investors that like the high yield of master limited partnerships (MLPs), but hate the idea of K-1s, another option outside the Alerian MLP ETF ( AMLP ) is the First Trust MLP and Energy Income Fund Common ( FEI ).

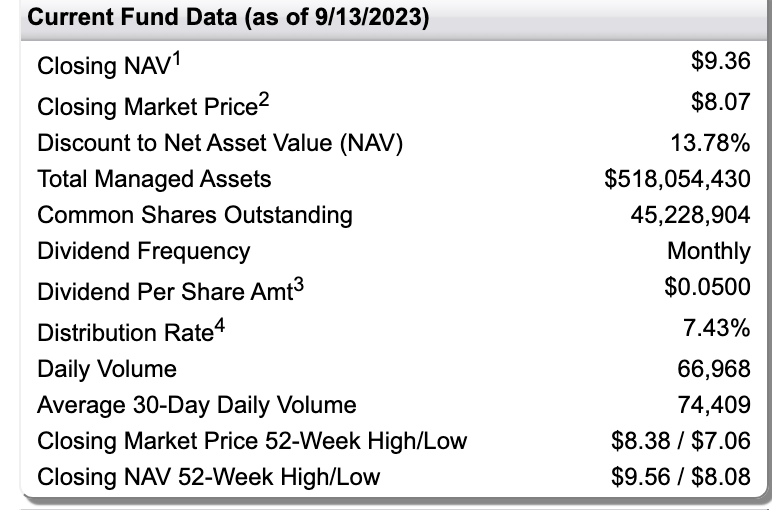

The closed-end fund [CEF] currently has a yield of about 7.4%

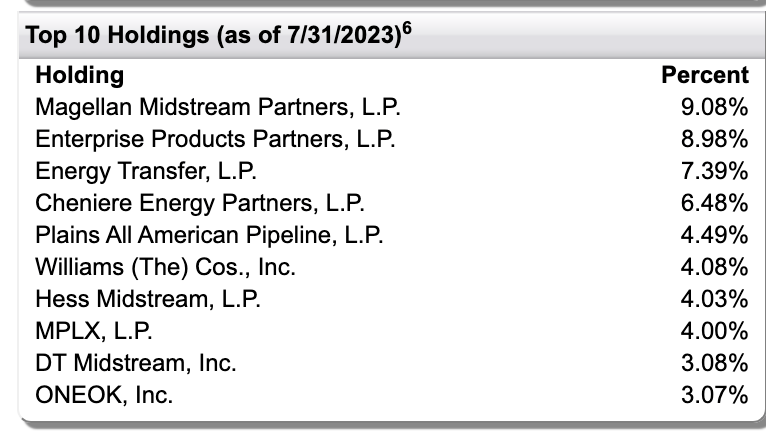

To judge the CEF, let’s look briefly at its top-5 holdings, which make up over a third of its portfolio and thus will drive the CEF's performance.

{kind=link}

Magellan Midstream ( MMP ) - 9.08%

Coming in hot as its top holding in MMP, which is in the process of being acquired by ONEOK ( OKE ). OKE is the CEF’s 10 th largest holding with a 3.07% weighting.

In June , I wrote that long-term investors should vote against the MMP-OKE deal due to the tax consequences. Since then, the company has undergone a full-court press to try to convince investors to vote for the deal.

In an interview with Seeking Alpha, CEO Aaron Milford said: "So if you're an investor, you owe the taxes anyway; the question is, do you want the premium in the deal? Because you're better off. Do you want $45 after the tax-free deal, or would you prefer $55 now with the upside of the pro forma because what I think is misunderstood is that this transaction is not creating these taxes; these taxes exist in either scenario, and anytime a unit holder wants to sell a unit, they're going to pay taxes."

That is certainly true, but MMP is also forcing its investors to pay a large tax bill now and all at once if the deal goes through. That’s not ideal for many investors, many of whom would prefer just to continue to collect the distribution.

MMP has become bond-like, as it wasn’t finding many growth projects and instead was focusing more on capital allocation. However, it was enjoying a nice boost from its tariffs that are tied to inflation.

As for OKE, the company set to acquire MMP, I’m largely neutral on the stock, as I think there are better buys in the space. More of my thoughts on OKE can be found here .

Enterprise Products Partners ( EPD ) - 8.98%

If I were building my own midstream CEF, EPD is the first stock I’d look to add. Quite simply, it has been the best-run company in the space for over two decades. While many companies in the space have run into market or leverage issues in the past during weak energy environments, EPD is on track to increase its distribution for the 25 th straight year in 2023.

I consider EPD to have some of the best assets in the sector, and while some midstream companies are having trouble finding growth projects, the company has a strong backlog. At the same time, EPD has a strong balance sheet with only 3.0x leverage and a distribution coverage ratio of 1.8x last quarter.

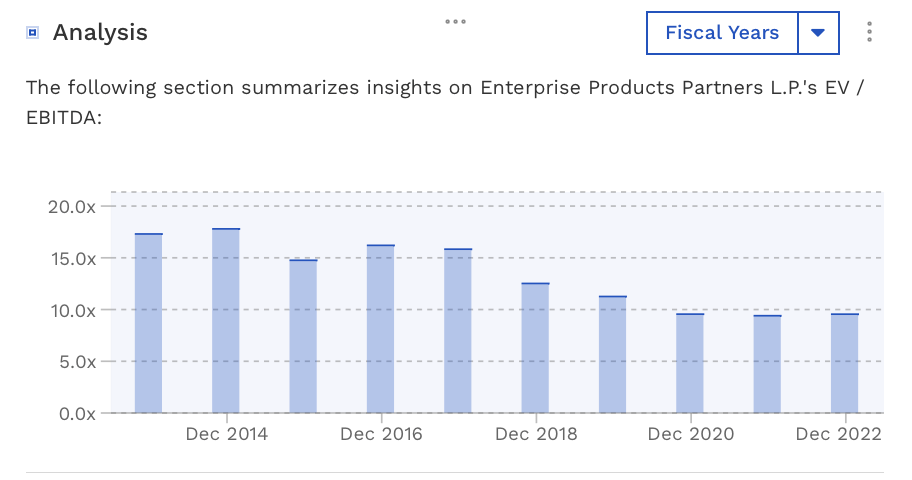

The stock currently trades at 9x 2024 EBITDA estimates. While that is higher than many midstream stocks, the premium is deserved given its track record, and it is still below where the stock has traded historically pre-Covid.

EPD Historical EV/EBITDA Multiple (FinBox)

{kind=link}

Energy Transfer ( ET ) - 7.39%

ET is the best value in the midstream space in my view. Trading at just 7.4x 2024 adjusted EBITDA, investors get what I view as the best midstream assets in the entire sector.

So, if ET has the best assets in the sector, why is it among the cheapest stocks in the space, you may ask. That boils down to founder Kelcy Warren, who previously used the GP to take advantage of its ETP limited partner unitholders by aggressively growing the ETP distribution while it was in the high-split IDRs and using LP units to fund growth. A private preferred offering to shield his interest during ETE’s botched takeover of Williams ( WMB ) back in 2016 only cemented his reputation.

However, since the ETE-ETP merger to form ET in 2018, these past conflicts of interest are no longer present.

Still, investors have a long memory and have been reluctant to re-rate ET to a more appropriate peer level. I think the Warren discount should eventually fade as he’s been on good behavior for over 5 years now, and that the company deserves to trade at a much higher multiple. The company is one of the world’s largest energy arbitrageurs and has a lot of growth still left in front of it.

It is perhaps my favorite midstream stock currently.

Cheniere Energy Partners (CQP) - 6.48%

CQP owns and operates the Sabine Pass LNG Terminal in Cameron Parish, Louisiana, one of the largest LNG production facilities in the world. Cheniere Energy ( LNG ) owns 48.6% of CQP, as well as its general partner and incentive distribution rights (IDRs).

CQP has a pretty steady business, with about 85% of its total product capacity contracted out through long-term agreements. The stock is a play on the growing LNG market, and the company is in the process of looking to expand the Sabine Pass facility.

That said, I prefer an investment in Cheniere Energy over CQP as the MLP is not associated with all of Cheniere’s growth projects and it is one of the few MLPs that still have IDRs, which are currently in the high splits.

You can find more of my thoughts on CQP here , and more on Cheniere Energy here .

Plains All American Pipeline (PAA) - 4.49%

PAA is a liquids-focused midstream operator, whose assets consist of gathering, intra-basin, and long-haul pipelines, as well as associated storage assets. Its crude segment represents over 80% of its EBITDA, with the Permian accounting for about 60% of the segment's EBITDA.

The company previously overbuilt capacity in the Permian, which while a mistake, now gives it the opportunity to take advantage of Permian growth as its underutilized pipelines get filled. This has been fueling growth for the company, while also keeping its CapEx down. As its pipelines and others in the Permian start to get filled - balancing out pipeline supply-demand dynamics - it should also lead to increased tariff rates down the road.

PAA is trading at under 8x 2024 EBITDA; has low leverage of 3.2x; and a coverage ratio of over 2x. I like PAA, which I rate a “Buy,” and have more coverage on the stock here .

{kind=link}

Sector-Focused Closed-End Fund

As a midstream sector-focused CEF, FEI has a pretty narrow focus. While most midstream companies don't have a lot of direct energy price exposure, they do tend to have volume exposure, which can be impacted by prices. However, it is notable that many companies in the space have seen volumes hold up well when natural gas volumes plunged last year, as there is still a lot of demand pull for natural gas. FEI tends to have most of its exposure in crude and natural gas pipeline companies.

The MLP structure along with the prospects of the midstream companies have improved over the past several years, as the companies have become more disciplined and improved their balance sheets. Most have eliminated incentive distribution rights (IDRs), which acted as a transfer of value to the GP on distribution increases, and companies today scrutinize returns on projects much more closely. However, the stock prices of midstream have generally not reflected this change for the better and trade below pre-pandemic valuations.

Given the strength of the individual stocks in the CEF's top 10, the current distribution is sustainable and should continue to rise.

Conclusion

While I like picking individual stocks, I think FEI is a good option that has many of the top midstream options out there. The CEF is a little more diverse than AMLP and also includes some non-MLP midstream stocks such as WMB and OKE.

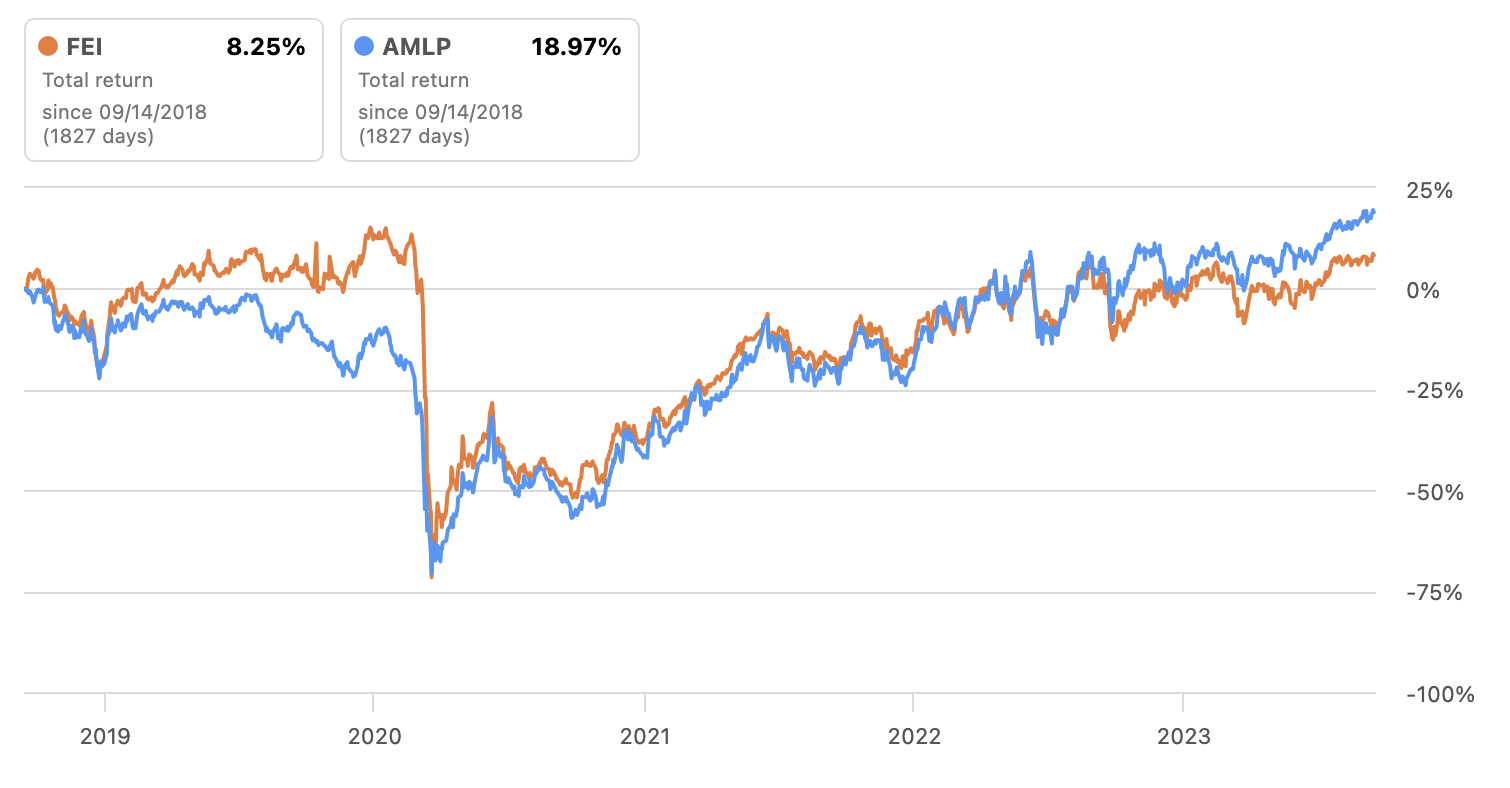

One of the most notable things about FEI is that currently the CEF trades at an over 13% discount to its NAV. That’s a pretty sizable discount and really takes away any concern with the potential tax consequences from the MMP-OKE merger. It’s also worth noting that FEI does use a minimal amount of leverage which can juice its performance. While the AMLP has outperformed FEI, a large part of that seems to be from the recent discount to NAV the CEF has seen over the past year plus.

{kind=link}

{kind=link}

Overall, while I like picking individual stocks, I think FEI looks attractive given its portfolio and current discount to NAV. You’re getting some top midstream names as top holdings and get to avoid K-1s. As such, I think the CEF is “Buy.”

For further details see:

FEI's Discount To NAV And Top Holding Make It Attractive