GRBK - Finding Faith In Real Estate: My Journey Back With Green Brick Partners

2023-08-18 18:05:54 ET

Summary

- Green Brick Partners is a real estate company tied to homebuilding and land improvement in the Dallas-Fort Worth and Atlanta areas.

- The company has reported strong Q2 2023 key data, including increased home deliveries and orders, a decrease in cancellation rates, and a decrease in construction cycle duration.

- Despite uncertainties in the real estate market, Green Brick's historically high margins, declining raw material prices, and ability to withstand a recession make it an attractive investment opportunity.

Stay away from stocks related to the real estate market. This was one of my personal guidelines for 2023. Too many uncertainties: the possible arrival of a recession, the unique condition of the market between minimal inventory and sky-high interest rates, and the volatility in the commodities market, to name a few. Between the stocks that were heavily sold in 2022 and soaring tech, I thought I could resist any temptation from the real estate sector.

Until I analyzed Green Brick Partners ( GRBK ). For those unfamiliar with the company, it is entirely tied to homebuilding and land improvement, with the heart of its operations in the DFW (Dallas-Fort Worth) and Atlanta areas.

I began my analysis tainted by skepticism and concluded it with a strong injection of enthusiasm. In this analysis, I explain why, despite the stock's rally, I believe there is still plenty of room to invest.

Q2 2023 Key Data

Green Brick Partners released their second-quarter 2023 results on August 2nd. Here are the most important figures, but I want to stress that my analysis does not rely - like none of my analyses - on a 90-day period. It might just be helpful for those already following the stock to stay updated. The most relevant financial data are:

- Revenue of $454.4 million from residential units, with a gross profit of $142.9 million and a net income of $75.3 million;

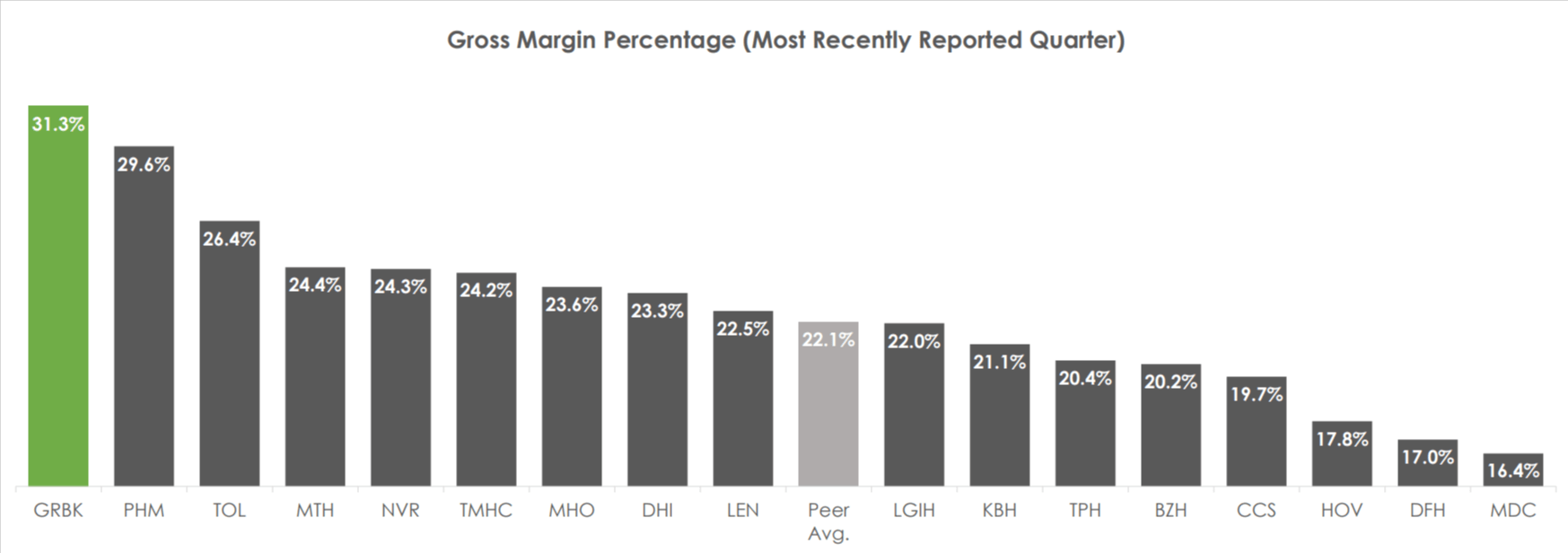

- The gross margin linked to homebuilding was 31.30%, slightly down (100 bps) compared to the same period in 2022;

- Free cash flow of $1.19 per share;

- Total liabilities of $553.4 million, of which $227.8 million are current liabilities;

- $209.6 million in cash and short-term investments, an increase of $32.3 million from the previous quarter;

- Inventory value stands at $1.404 billion, a slight increase from the $1.369 billion in Q2 '22 and the $1.373 billion in Q1 '23;

- The debt/total capital ratio as of June 30th was 22.9%.

Overall, the company maintains one of the best margins in the industry, as reported in the accompanying slide of the quarterly data presentation.

{kind=link}

Regarding company business updates, the most important points to highlight are:

- 783 new homes were delivered in the second quarter;

- Orders for new homes increased by 50.8% compared to the same period last year (822 vs 545) and by 64.8% in the first six months of 2023 compared to the same period last year (1,889 vs 1,146);

- The average price of the backlog increased by 1.7%;

- The cancellation rate dropped from 11.4% to 7.4%, indicating a strong improvement in the company's sales ability;

- The company completed the development of over 2,000 plots in the first half of the year and expects to end the year with 6,100 finished plots;

- The construction cycle duration has decreased by 47 days compared to the end of 2022.

It is truly challenging to find a single point to criticize the solidity of these results. Not just in absolute terms but also compared to the data published by other American builders this past quarter.

Real Estate Market Conditions

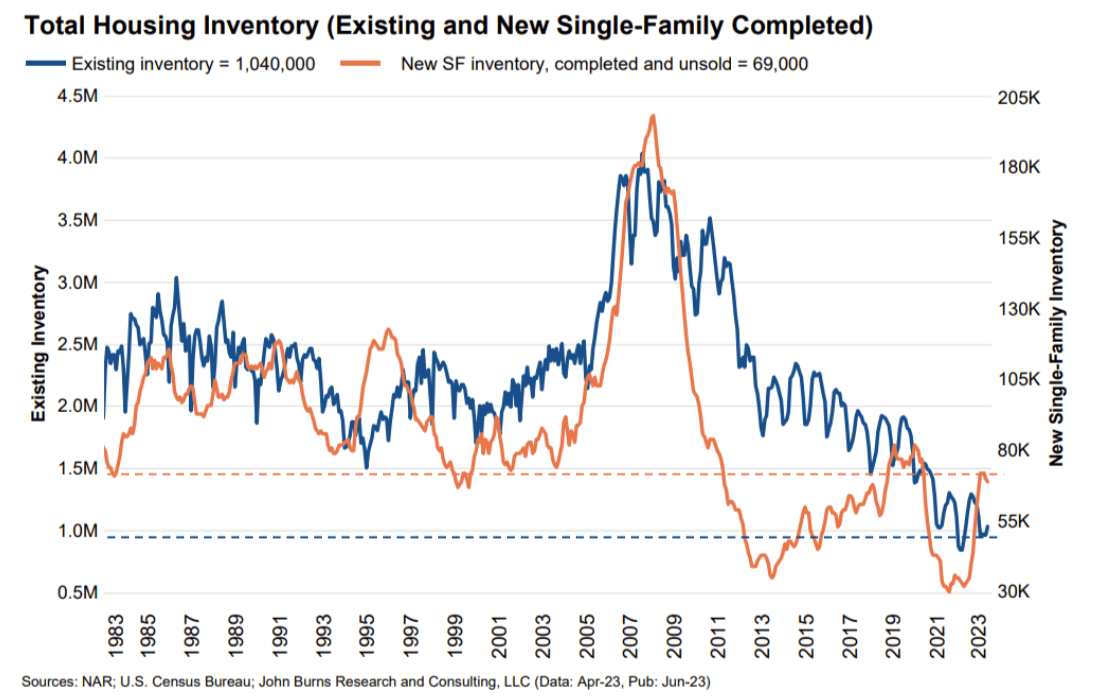

Contrary to expectations, the rise in interest rates has not yet caused a significant contraction in prices. Homeowners who took out a mortgage during the pandemic or earlier, benefiting from better rates than those currently available, are not selling their properties. Consequently, inventory is at historical lows, and buyers have to look at the new home market.

Q2 Investors Presentation - Data from NAR, U.S. Census Bureau

{kind=link}

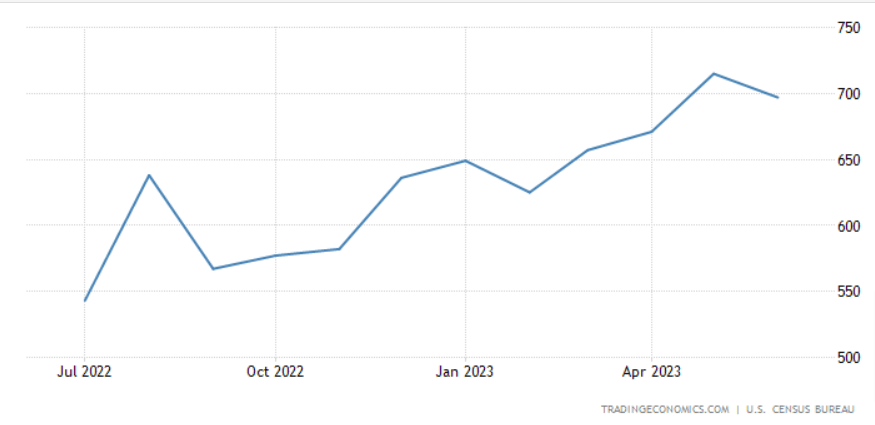

Undoubtedly, this context is benefiting property developers, who are able to achieve higher margins on sales. Specifically for Green Brick, the company has "indirectly" raised the average selling price in 2023: although the listing prices have slightly decreased compared to Q2 '22, the company has ceased to offer long-term rate buy-downs as incentives for buyers. Regardless of how this is accounted for in the financials, this measure has the same effect as a price increase. Looking specifically at the Dallas market, this year Green Brick has reported a reduction in incentives in 70-80% of communities.

New home sales (Trading Economics - Data from U.S. Census Buraeu)

{kind=link}

Focus on Atlanta and DFW

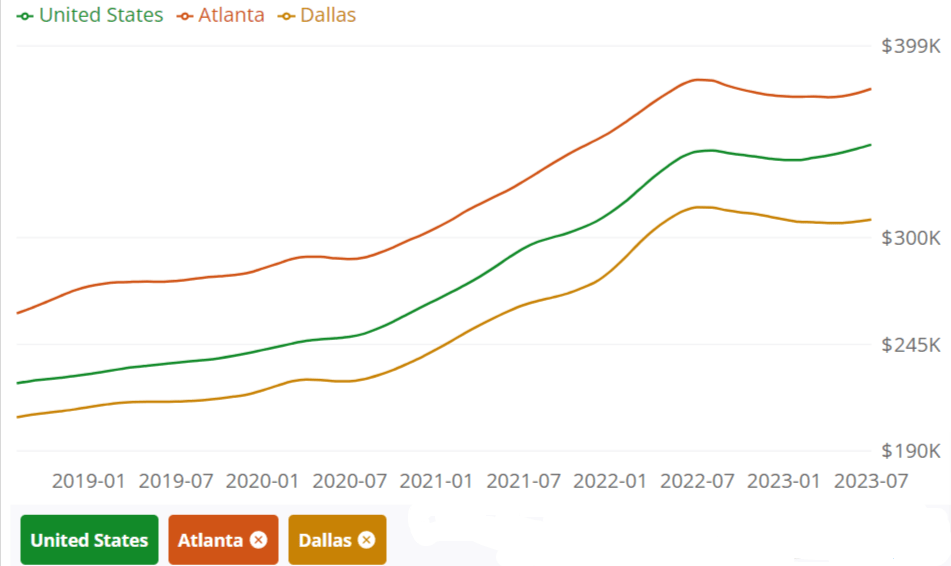

The reason for such positive results is not because the markets they operate in have been particularly better than the national average in recent years. In fact, looking at Zillow's data, Atlanta and Dallas-Fort Worth seem to have merely followed the general trend of the American real estate market.

{kind=link}

They are undoubtedly two great markets because of the major employers operating in these areas. For DFW, it's certainly worth mentioning Southwest Airlines (LUV), Topgolf, McKesson (MCK), Toyota North America, Texas Instruments (TXN), Jacobs Engineering (J), Exxon Mobile (XOM), and American Airlines (AAL), among others. For Atlanta, companies like Coca-Cola (KO), Delta (DAL), Home Depot (HD), UPS (UPS), Georgia-Pacific, Mercedes-Benz USA, Porsche North America, Chick-fil-A, and Southern Company (SO) can be cited, among many others.

The presence of a diversified economic fabric and strong employers ensures that these two cities aren't exposed to the collapse of a single industry, like San Francisco with tech or Detroit with the automotive industry. Therefore, beyond short-term cycles, one can expect the real estate market in Atlanta and DFW to remain strong in the long term.

Market conditions matter, but they aren't everything

The fact that Green Brick Partners' results have soared in the past two years is also certainly due to extremely reduced inventory, maintained high prices, and scarce existing home sales. For this reason, I find it nonsensical to analyze the company with a DCF model: there have been too many recently changing variables and too much unpredictability in real estate market cycles to make really solid assumptions.

Instead, I invite you to consider this: the current P/B ratio is 1.95, meaning half the stock price is justified by the company's liquidation value. At the same time, the TTM net income stands at $268.5 million, against a market capitalization of $2.22 billion. Considering the profitability of the core business and the value of the company's assets, it won't take long before the investment pays for itself.

In particular, I find it crucial that Green Brick is in a position to withstand any changes in the real estate market. The reasons behind this statement are listed below, showing clearly that market conditions are not the only reason for such positive results in recent years.

Historically high margins

The table below shows that although Green Brick has had particularly high margins in recent years, its profitability has always been high historically (Data from Seeking Alpha).

| Year |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM |

| Revenue |

| 291.1 |

| 391 |

| 458.3 |

| 623.6 |

| 791.7 |

| 976 |

| 1,402.90 |

| 1,757.80 |

| 1,747.40 |

| Gross profit |

| 62.3 |

| 87.8 |

| 118.6 |

| 154.3 |

| 169.2 |

| 234.6 |

| 362.1 |

| 523 |

| 513.3 |

| Operating income |

| 32.3 |

| 49.1 |

| 60.1 |

| 74.3 |

| 71.4 |

| 122.5 |

| 227.8 |

| 359.1 |

| 330.3 |

| Gross profit margin |

| 21.40% |

| 22.46% |

| 25.88% |

| 24.74% |

| 21.37% |

| 24.04% |

| 25.81% |

| 29.75% |

| 29.38% |

| Operating margin |

| 11.10% |

| 12.56% |

| 13.11% |

| 11.91% |

| 9.02% |

| 12.55% |

| 16.24% |

| 20.43% |

| 18.90% |

From this data, it's evident that the margin on homebuilding has long exceeded 20% and has increased over the years due to economies of scale. Moreover, Green Brick has refined its current business model over time, maximizing achievable margins through a series of key decisions:

- Fully independent lot development;

- Choice of infill or infill-adjacent lots;

- An increasingly stronger focus on the pricier and more desirable areas of Atlanta and DFW;

- A mix increasingly geared towards middle-upper and upper-class clients.

Although focusing on independent lot development might slow the company's growth, the fruits of this decision are now being seen: margins have increased over time not only due to market prices but also thanks to greater bargaining power, economies of scale, and expertise acquired over the years.

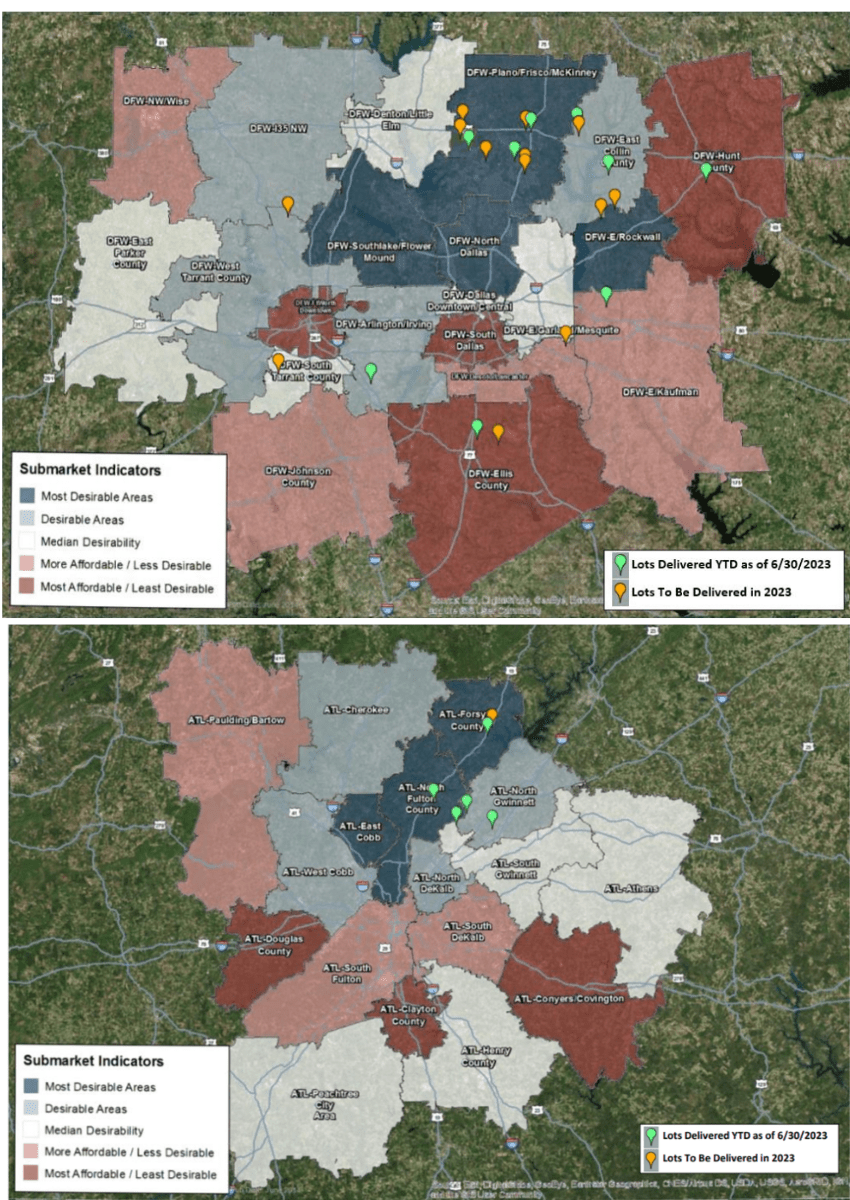

Areas of DFW and Atlanta where Green Brick is conducting operations (Q2 '23 Investors Presentations)

{kind=link}

Declining Raw Material Prices

Although 2021-22 was a great biennium for Green Brick' margins, it was also marked by high prices for raw materials. Between March and today, the prices of wood, steel, and cement have significantly decreased. Unfortunately, statistics on the impact of these costs as a percentage of the total are not available, but it's clear that Green Brick will benefit in the upcoming quarters.

In case of Recession, Green Brick is Ready

Let's assume the worst-case scenario: a recession, a significant decline in property values (-10/15%), and low market demand. In this context, I would be wary of holding the shares of a residential REIT operating with a classic 1:2 leverage or those of an even more indebted builder. Fortunately, Green Brick has been extremely cautious over the years and can now benefit from it: interest rates are high but the debt is not high, and the financial leverage is so low that even in a crisis, Green Brick would easily survive in my opinion.

In the meantime, it would remain the third-largest builder in two of the most industrialized cities in the United States, with the possibility of conducting acquisitions at discounted prices, both of individual assets and other builders. Times would be tough, but the company has all the means to emerge stronger.

How I will play this

Green Brick has found a winning formula to operate with high margins in almost any market context, aiming to grow sustainably over time through autonomous lot development and low debt. It has increasingly defined its target market, and today, despite the stock rally, I believe there are still all the conditions to open a position.

The only significant risk is a real meltdown of the real estate market, with a correction similar to that of 2008. It should be said that, in that case, the problem would be the entire stock market and not just Green Brick. Even in a period when I wanted to stay away from the real estate market, this company convinced me to re-enter it.

I plan to build my position gradually since prices in the Dallas and Atlanta areas are beginning to decline. I think this will generate some panic and will lead especially those who have benefited from the rally so far to realize their profits. For this reason, I will invest 10% of the total capital I want to invest in Green Brick every month, dollar-cost averaging in an unpredictable period for interest rates. This makes me even more confident about my position. And of course, having this investment ongoing, I will periodically update my analysis.

For further details see:

Finding Faith In Real Estate: My Journey Back With Green Brick Partners