VTSI - Finding The Value In VirTra Inc.

2023-03-20 08:30:00 ET

Summary

- VirTra doesn’t screen well. Margins have declined over the years, it currently trades at a high trailing earnings multiple and has recently been very capital intensive.

- But I think the business is at an inflection point as operating leverage from recent investments could kick in as revenue growth ramps.

- This could be an especially good opportunity as the stock has declined quite a bit over the past few months.

- In this article, I’ll go into more detail on this potential operating leverage and the potential risks of an investment in the stock.

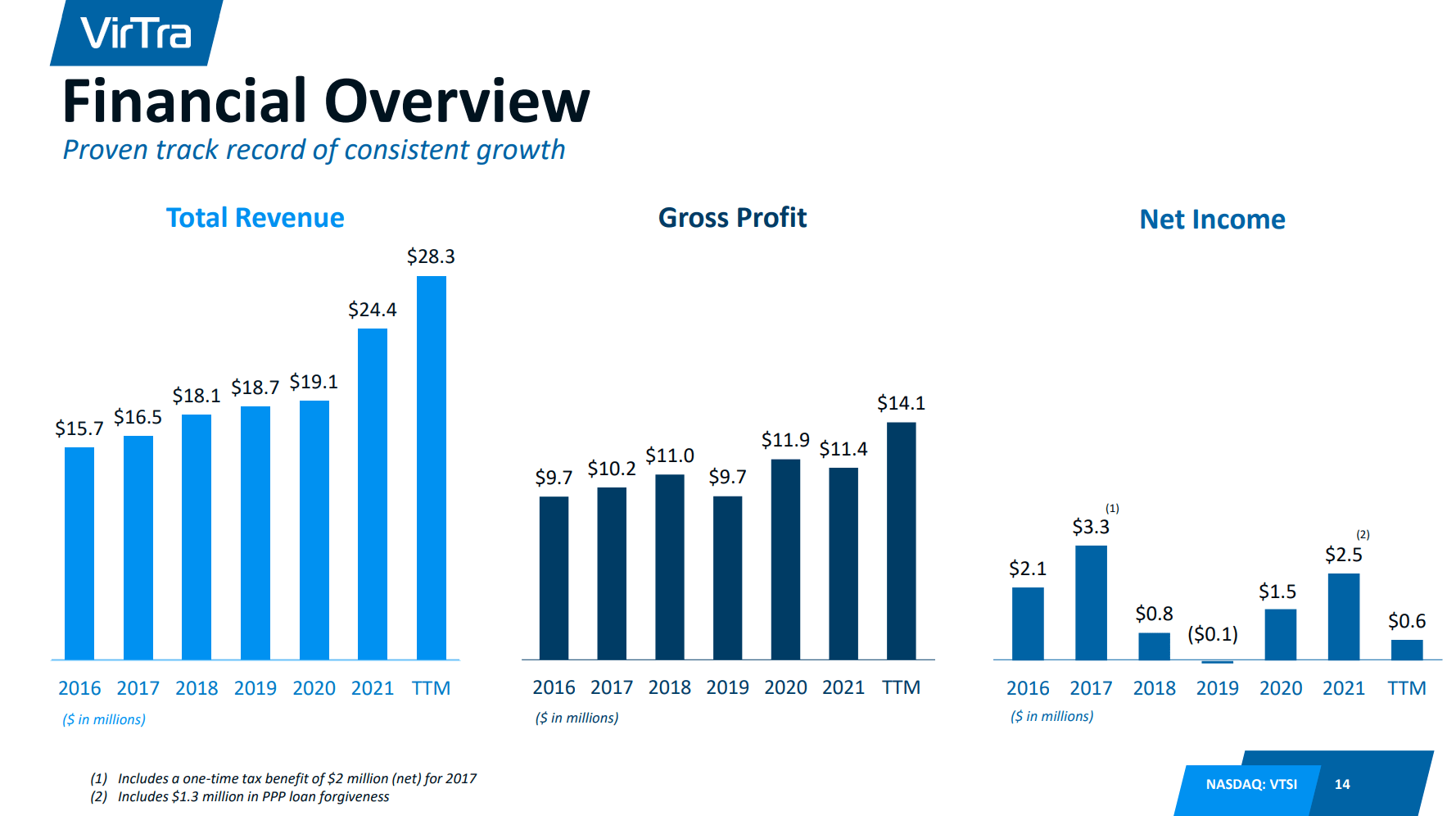

VirTra, Inc. ( VTSI ) is in an interesting spot. The stock doesn’t screen well. Margins have declined over the past few years, it currently trades a high trailing earnings multiple, it has recently been very capital intensive, the share count rose quite a bit in 2021 due to a large capital raise, and the financials are lumpy as seen from the slide below.

Financial Overview from VirTra Investor Presentation (VirTra Investor Presentation)

{kind=link}

But I think the business could be at an inflection point. They are at the start of a big push to grow the military segment, led by co-CEO John Givens. They recently opened a facility in Orlando which, from the most recent earnings call , “will serve as an extension of our R&D efforts, customer service, and as a demonstration and meeting site for our prospective [military] customers.” And in 2021, they completed the purchase of land and office space in Arizona to help scale all aspects of the business from administrative work to R&D.

What all of this means is that this could be a turning point for the business. Operating leverage from all of the new facilities could kick in as revenue growth rises. This would lead to high growth in earnings and, if capex falls to levels seen from before the Arizona land and office investment, high growth in free cash flow.

This is especially an opportunity because the stock just about at a 52 week low. This operating leverage would lead to more investor interest as it would screen better on a trailing 12 months basis and from there, the stock could rise from higher earnings and multiple expansion. In this article, I’ll go into more detail on this potential operating leverage and the risks of an investment in VirTra stock.

Where Will the Growth Come From?

Management is clearly banking on high growth for a long period of time from the military segment. From the most recent earnings call, co-CEO Bob Ferris emphasized this as he said, “keep in mind, we still see massive upside in the military market for our shareholders, especially given VirTra’s technological leadership position with de-escalation and small arms training. We are increasingly convinced we can expand our military simulation market share through efforts spearheaded by John Givens”.

For the nine months ended September 2022, revenue grew 24%. This was the case even with a 20% year over year revenue decline in the third quarter due to unbilled sales not being recognized. As these are recognized in the fourth quarter and beyond, and as the military segment grows with the start of the Department of Defense fiscal year 2024, revenue growth should continue at a high clip.

The main caveat for this incremental revenue growth, is that it needs to be at a relatively high gross margin. From 2013-2020, gross margin stayed within the 55%-65% range. In 2021, gross margin dipped down to 32% in Q4 but has been about 50% for the past few quarters. I will go into more details on my financial calculations below, but the stock works from here if gross margin settles in at 50%.

Tailwinds

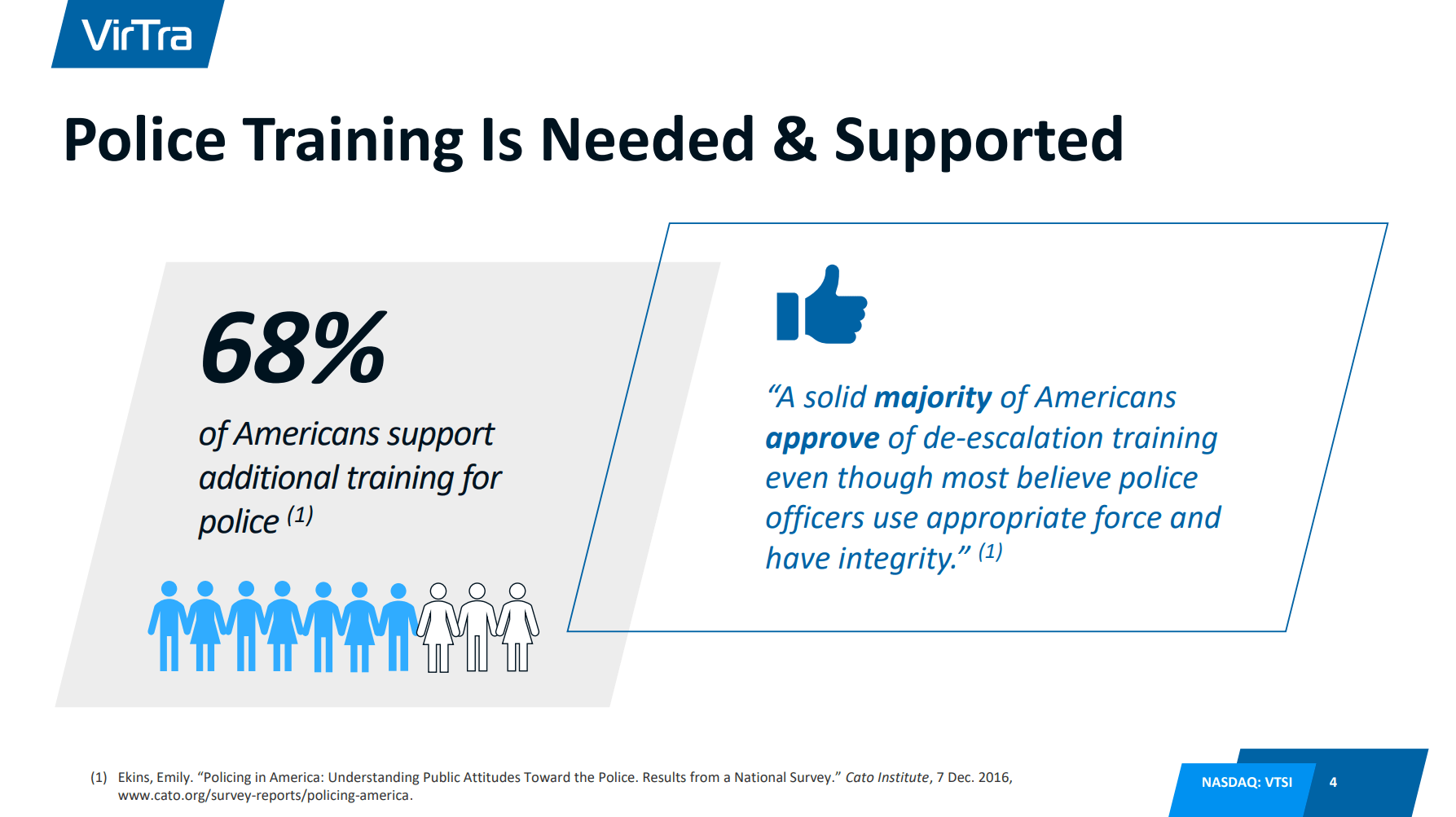

On top of VirTra’s long term track record of growth, there are tailwinds for the industries they operate in. There is widespread support for increased police training, as training in the U.S. normally lasts weeks while training in other countries lasts months. This support should bolster further sales growth in the law enforcement segment going forward.

Slide from VirTra Investor Presentation (VirTra Investor Presentation)

{kind=link}

In addition to more spending on law enforcement training, military spending around the world is on the rise. The White House recently released its proposed defense budget for fiscal year 2024. It calls for an increase of $26 billion and $100 billion over FY 2023 and FY 2022 respectively. This is clearly driven by increased awareness for military spend due to the war in Ukraine and from increased geopolitical pressure from China. Just as the support for increased police will help bolster sales in the law enforcement segment, this increased military spending will provide a tailwind for VirTra’s military segment.

Expenses and Capital Expenditures

Operating expenses have ballooned over the past few quarters due to the expansion of the Orlando facility which was built to support military and general market objectives. Total operating expenses for the trailing 12 month period were $13.2 million compared to $10 million in the trailing 12 months prior. This 30% increase in expenses came with 24% growth in lower gross margin revenue. This is not a recipe for earnings growth.

In addition to the increased operating expenses, capex increased quite a bit in 2021 due to the purchase of land and office space in Arizona. VirTra has historically been a relatively capital light business with capex being a low single digit percentage of revenue but more recently, capex has been a low double digit percentage of revenue. Once again, this increased capex along with lower margin revenue growth has not been a recipe for growth in free cash flow.

I will go into more details below but for the stock to work operating expenses need to grow at its pace from years prior, and capex needs to decline to a low single digit percentage of revenue. These factors, along with relatively higher gross margin incremental revenue growth will showcase the imbedded operating leverage.

Financials

From 2013-2021, revenue growth averaged 12% and in that same period, gross margin averaged 58%. However revenue grew 24% in the 9 months ended September 2022 with a gross margin of 55%. For my estimates, I will assume revenue grows 18% per year (middle point between 12% and 24%) from here and that gross margin settles in at 50%.

Operating expenses grew an average of 8% per year from 2013-2021. I will assume growth in operating expenses returns to this average as the Orlando and Arizona facilities are completed.

(all figures in thousands)

| CY 2022 |

| CY 2023 |

| CY 2024 |

| Revenue |

| $28,297 |

| $33,391 |

| $39,401 |

| Gross Margin |

| 50% |

| 50% |

| 50% |

| Gross Profit |

| $14,148 |

| $16,695 |

| $19,700 |

| Operating Expenses |

| $13,288 |

| $14,352 |

| $15,500 |

| Operating Income |

| $860 |

| $2,343 |

| $4,200 |

| Tax Rate |

| 21% |

| 21% |

| 21% |

| Net Income |

| $3,318 |

With these assumptions, operating income in CY 2024 would be $4.2 million. Assuming a 21% tax rate, net income would be $3.3 million. VirTra’s current market cap is $43 million so this would put the stock at about 11x CY 2024 net income.

Determining a fair earning multiple is difficult here because of the lumpy investment schedule that has led to lumpy ROIC numbers. In the past, ROIC has been high as it was an asset and capital light business. For example, in 2016 VirTra earned $2.1 million of operating income with invested capital (I’m determining this by adding net working capital and PPE) of about $7.5 million for an ROIC of 28%. A high growth business with a 28% ROIC clearly demands a high earnings multiple. But the facts have changed.

The business seems to be hoarding quite a bit of cash and PPE is much higher due to the Arizona land and office space investment, so the latest quarterly report shows invested capital of $40 million. With that figure, even with operating income of $4.2 million as I’m estimating for in 2024, ROIC would be 10%. Once again this screens poorly as it no longer looks like the asset light, high ROIC business it once was.

However beneath the surface I believe this is a high ROIC business and returns on incrementally invested capital (ROIIC) going forward should be high as the operating leverage story plays out. This is why, along with the high expected growth going forward, I think a 20x earnings multiple is reasonable.

With a 20x net income multiple, the market cap would be $66 million or 50% higher than the current market cap by the end of 2024. On top of this, the operating leverage from the Arizona and Orlando facilities should continue to facilitate earnings growth beyond 2024.

Risks

The main issues in my thesis are obviously revenue growth slowing and operating expense growth remaining elevated. Between these two I’m more concerned about the operating expenses. The company has a strong history of revenue growth and the tailwinds I described above make me confident the growth will continue. However, management hasn’t provided many details on expenses and capex going forward. It’s up to shareholders to trust that growth in these costs will fall due to the facilities being finished because if growth in expenses do not fall, earnings will not rise and the stock will likely continue to fall.

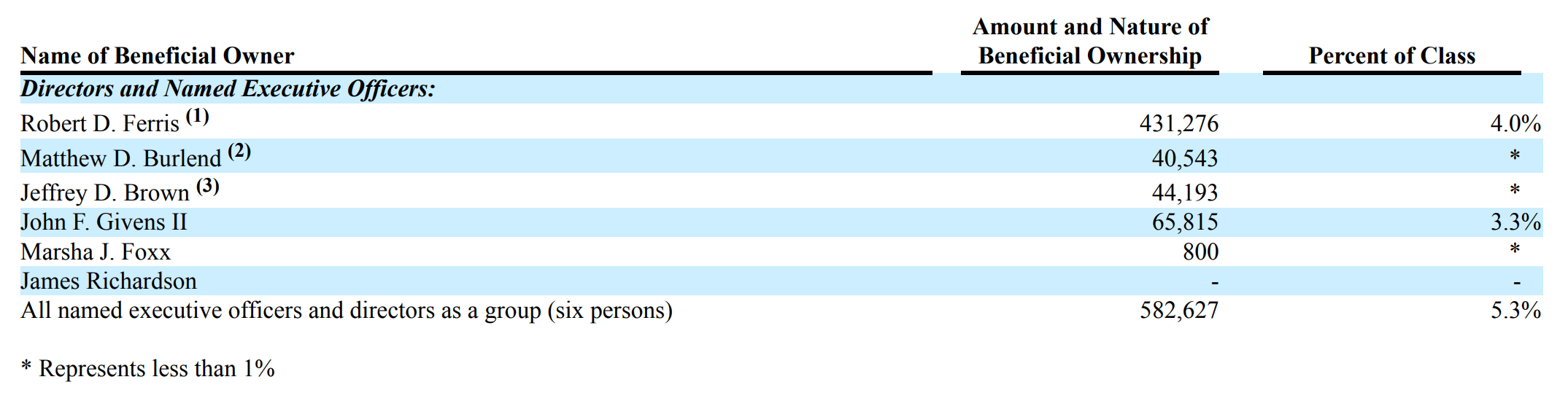

It’s not entirely easy to fully trust management that doesn’t have much skin in the game. The co-CEOs own less than 10% of the business and the board owns a negligible amount. Despite this being a micro-cap stock, the largest shareholders are institutional owners. With micro-caps, C-suite and board ownership is a very important factor to consider. It’s also important to consider how executives and the board acquired shares. Was it through stock awards or was it through open market purchases? In this case, much of the ownership is through stock awards.

Stock Ownership of VirTra Executives and Directors (VirTra FY Year 2021 10-K)

{kind=link}

However, the bright spot is that there is a stock bonus for the co-CEOs that vests depending on net income. Stock will vest for them if trailing 12 months net income as of August 2023 is $3 million. For the next year, stock will vest if net income for the trailing 12 months ending August 2024 is $3.5 million. This would ideally be determined by earnings per share, but this still creates an incentive to keep track of costs. And note that this trailing 12 months ending August 2024 target is above my calendar year 2024 net income target of $3.3 million. Obviously the stock is even more of a buy if this target is hit, but this makes me more confident about my 2024 net income target.

Final Thoughts

I believe VirTra is at an inflection point. Revenue should continue to grow due to industry and market tailwinds, while expenses and capex growth should slow as the Arizona and Orlando investments are completed. This should lead to operating leverage and earnings growth for years to come.

For further details see:

Finding The Value In VirTra, Inc.