FCNCA - First Citizens BancShares: Limited Upside Potential In 2024 (Rating Downgrade)

2024-01-08 20:20:10 ET

Summary

- The expected 2024 Fed pivot poses an NIM and earnings challenge for First Citizens.

- The Federal Reserve's decision to end its tightening policy and lower interest rates in 2024 poses risks for First Citizens and other regional banks.

- Growing pressure on First Citizens' net interest margin is a major concern. Shares now also trade at a premium to book value.

First Citizens BancShares ( FCNCA ) has seen a strong share price upside revaluation in 2023, in part due to a recovery in the broader regional banking market and because the bank acquired Silicon Valley Bank's deposits earlier this year. However, I believe that additional earnings and net interest margin upside is harder to achieve going forward now that the Federal Reserve is set to end its tightening policy. With the federal fund rate set to decline in 2024, I believe the risk profile is no longer as attractive as it was at the outset of the regional banking crisis in the first-quarter. Since shares have now also revalued up to book value and First Citizens trades at a 3% premium to book value, I am comfortable changing my rating to hold!

Previous rating

I acquired a small number of shares of First Citizens during the summer months as I ramped up my exposure to battered regional banks. The reason why I bought into First Citizens chiefly related to the general overreaction and panic in the regional banking market after Silicon Valley Bank failed. I believe that further revaluation upside is not only limited, but that downside risks have increased in the context of the Federal Reserve seeking a number of rate cuts in FY 2024. Therefore, I am downgrading First Citizens from buy to hold.

First Citizens acquired SVB's deposits during the crisis

First Citizens acquired failed Silicon Valley Bank after the regional bank was forced to sell assets in a bid to shore up its liquidity. The Federal Reserve ultimately stepped in, provided emergency liquidity and essentially bailed out the regional banking market. Many regional banks have lost deposits during this time, but the situation started to drastically improve in the second-quarter which is when deposits started to return to smaller banks. In the case of First Citizens, the banks' deposit base has grown significantly, however, due to the acquisition of SVB's deposits. The bank ended the third-quarter with $146.2B in deposits on its balance sheet, showing an increase of 63% since the end of FY 2022.

First Citizens

Growing pressure on First Citizen’s net interest margin should be expected

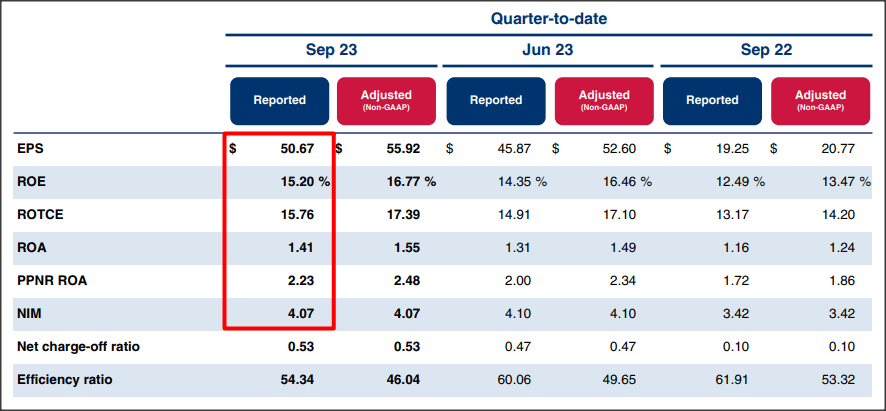

Going forward, growing pressure on First Citizens’ net interest margin is a major concern for me and the driving cause behind me changing my rating to hold. Although First Citizens reported strong Q3'23 results with an impressive return on equity of 15% and strong net interest margins after the integration of SVB's deposits, I believe that the Federal Reserve has changed the game here, not just for First Citizens, but for other regional banks as well.

{kind=link}

The Federal Reserve at this point has guided for three rate cuts in 2024 , but we may see more or less action on the interest rate front depending on how well the U.S. economy is holding up. The U.S. economy generated 216,000 jobs in December, widely crushing consensus estimates of 170,000 jobs.

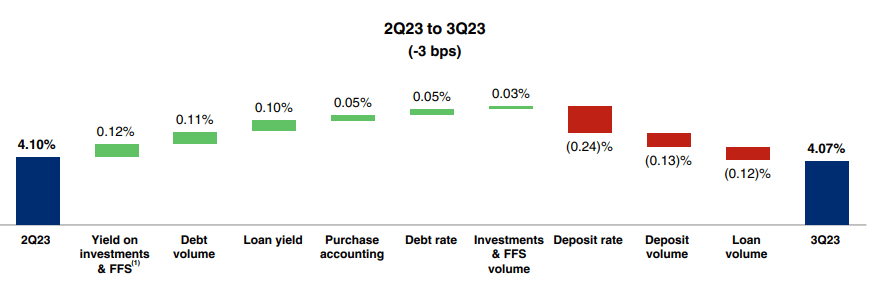

First Citizens achieved a net interest margin of 4.07% in Q3’23, showing a decline of 0.03 PP quarter over quarter. With a cyclical correction in terms of interest rates now apparently set to be initiated by the Federal Reserve, chances are for a slide in the bank’s net interest margin, and lower bank profitability overall, over the course of this year.

{kind=link}

First Citizens’ valuation

First Citizens has seen a strong share price revaluation to the upside since the bank announced the acquisition of SVB's deposits. Part of the reason why banks generally recovered in the second quarter is because deposits flowed back to the regional banking market after the Federal Reserve provided emergency liquidity to depository institutions in the first-quarter.

This measure has proven to be extraordinarily effective and can be credited for the quick and sharp rebound in bank valuations in 2023. Now, shares of First Citizens are valued at price-to-book ratio of 1.03X which contrasts with a P/B ratio of 0.90X when I first bought into the regional bank in the second-quarter. Most regional banks now trade at P/B ratios above 1.0X and I have sold most of my bank holdings, especially those that now trade at a premium to book value, including U.S. Bancorp ( USB ), Fifth Third Bank ( FITB ) and PNC Financial ( PNC ).

The main change here for me is the Fed's pivot with regard to interest rates which make banks generally less attractive for me as growth investments during a down-turn period in interest rates. I consider shares of First Citizens to be fairly valued at around $1,343 per-share since this is the regional bank’s last disclosed per-share book value.

Risks with First Citizens

There is no guarantee that the Federal Reserve will lower interest rates quickly in 2024 which means there is a reasonable chance that rate cuts could be delayed if the U.S. economy performs well. The U.S. economy just added 216,000 jobs in December, indicating that the Federal Reserve may not be in a hurry to lower the federal fund rate. This would obviously benefit the bank’s net interest income margin.

Final thoughts

I made a decent profit on my investment in First Citizens, but given the headwinds that can be expected from the Federal Reserve this year, I don’t see many good reasons to remain invested at the current time. Since shares are now also trading at a premium to book value, as small as this premium may be, I believe the risk profile is no longer as attractive as it was back in March or in June 2023. Given the limited upside potential that I see in FY 2024, I am rating shares as a hold!

For further details see:

First Citizens BancShares: Limited Upside Potential In 2024 (Rating Downgrade)