CA - First Majestic Silver: A Weak Q4 With A High-Cost Year On Deck

2024-01-22 00:39:15 ET

Summary

- First Majestic Silver missed its FY2024 silver production estimates and 2024 production is expected to decline year-over-year based on current guidance.

- Unfortunately, the 2024 outlook suggests negative free cash flow at current metals prices, and I would not be surprised to see additional share dilution in 2024.

- In this update, we'll dig into the Q4/full-year results, the company's outlook for 2024 & if the stock is finally offering enough of a margin of safety for investment.

While the S&P 500 ( SPY ) has built on its Q4 gains with a new all-time high set last week, the Silver Miners Index ( SIL ) has given up the bulk of them, down 12% year-to-date in what's typically its best month of the year from a seasonality standpoint for the precious metals. This can be attributed to underwhelming guidance from some companies like Fortuna Silver ( FSM ) and Endeavour Silver ( EXK ), and a 14% pullback in the silver price from its December highs.

Unfortunately, the sector has got no help from one of its leading producers, First Majestic Silver ( AG ), with the company reporting another year of elevated costs and lower production in 2024 after an already brutal 2023. Worse, the company missed its already downward revised 2023 guidance of ~10.9 million ounces of silver at the mid-point, partially offset by delivering into the higher end of guidance on consolidated gold production. In this update we'll dig into the Q4 and full-year results, the company's outlook for 2024, and if the stock is finally offering enough of a margin of safety from an investment standpoint.

Jerritt Canyon Operations - Company Website

{kind=link}

Q4 & FY2023 Production

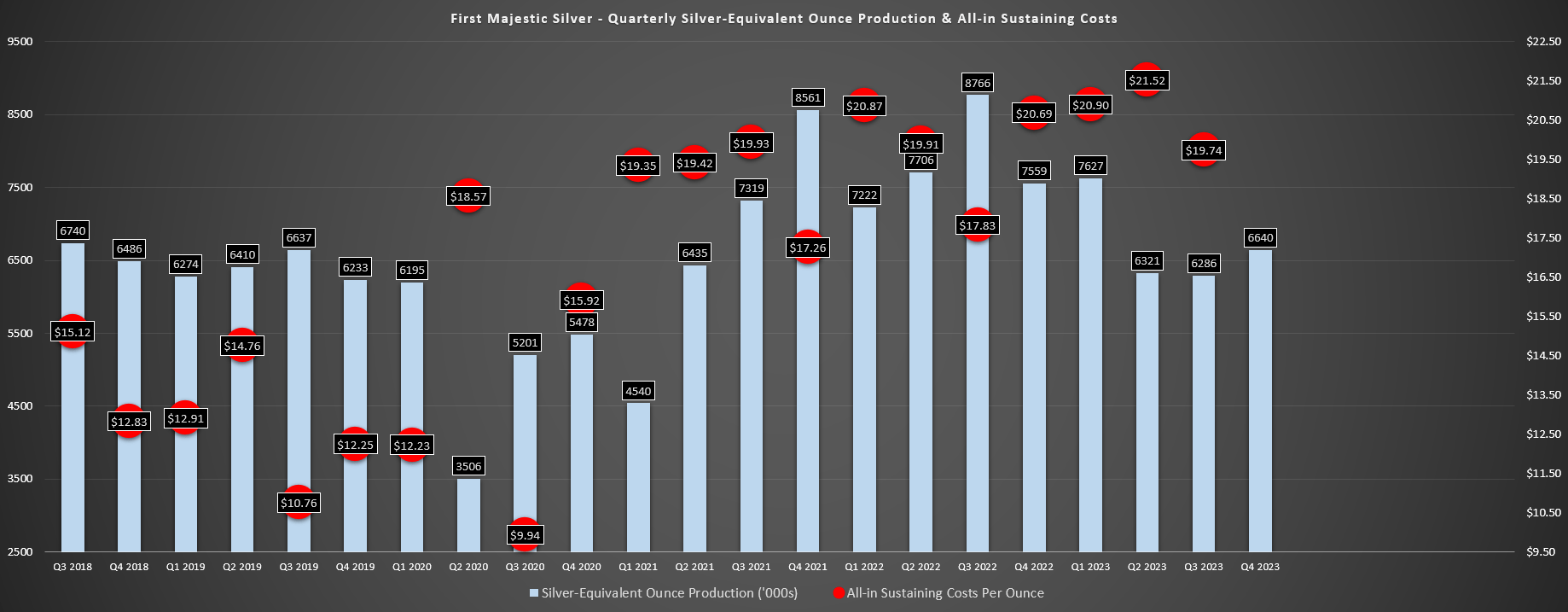

First Majestic Silver ("First Majestic") released its Q4 and FY2023 results earlier this month, reporting quarterly production of ~6.64 million silver-equivalent ounces [SEOs] made up of ~2.61 million ounces of silver and ~46,600 ounces of gold. This translated to a 9% increase in silver production but 26% decline in gold production from the year-ago period, with the lower gold production related to Jerritt Canyon moving into care & maintenance and the higher silver production driven by higher throughput and silver grades at San Dimas, offset by a much weaker Q4 from its smallest La Encantada Mine. In fact, La Encantada's production slid to a multi-year low at ~516,000 ounces, with this being the worst quarter since the temporary curtailment of operations during Q2 2020.

First Majestic Silver Quarterly SEO Production & AISC - Company Filings, Author's Chart

{kind=link}

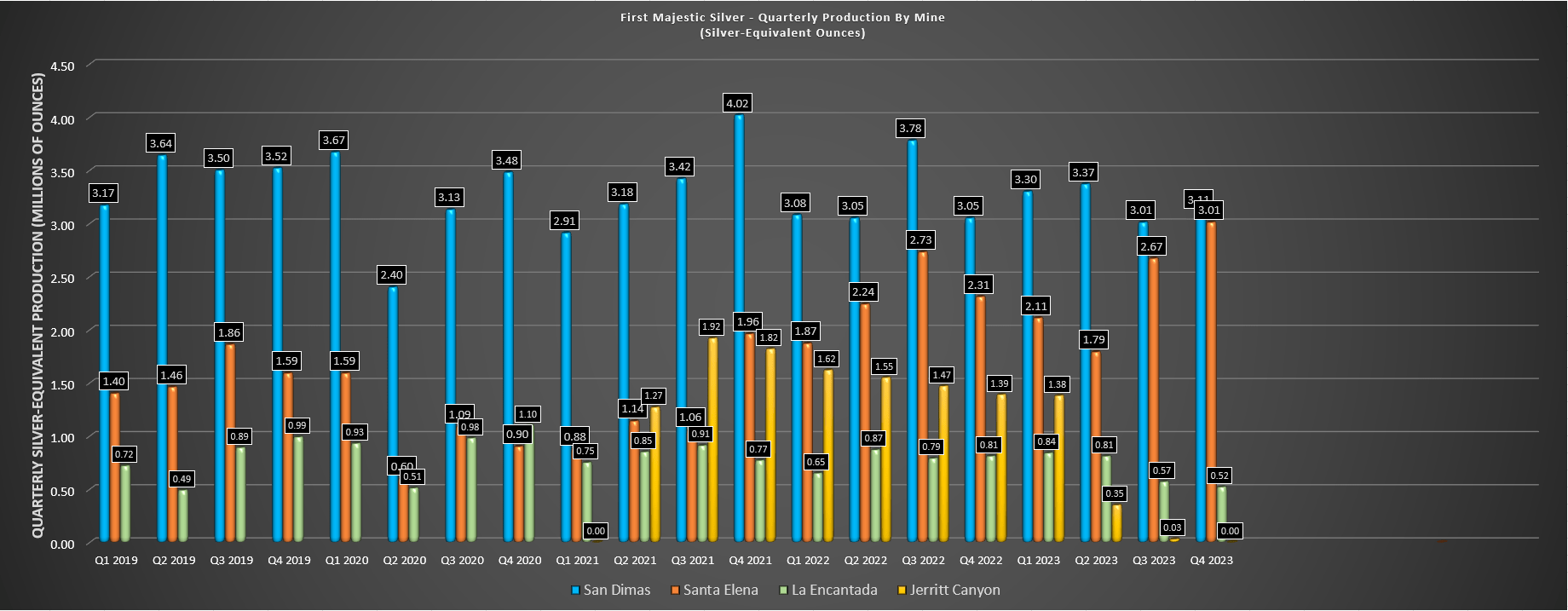

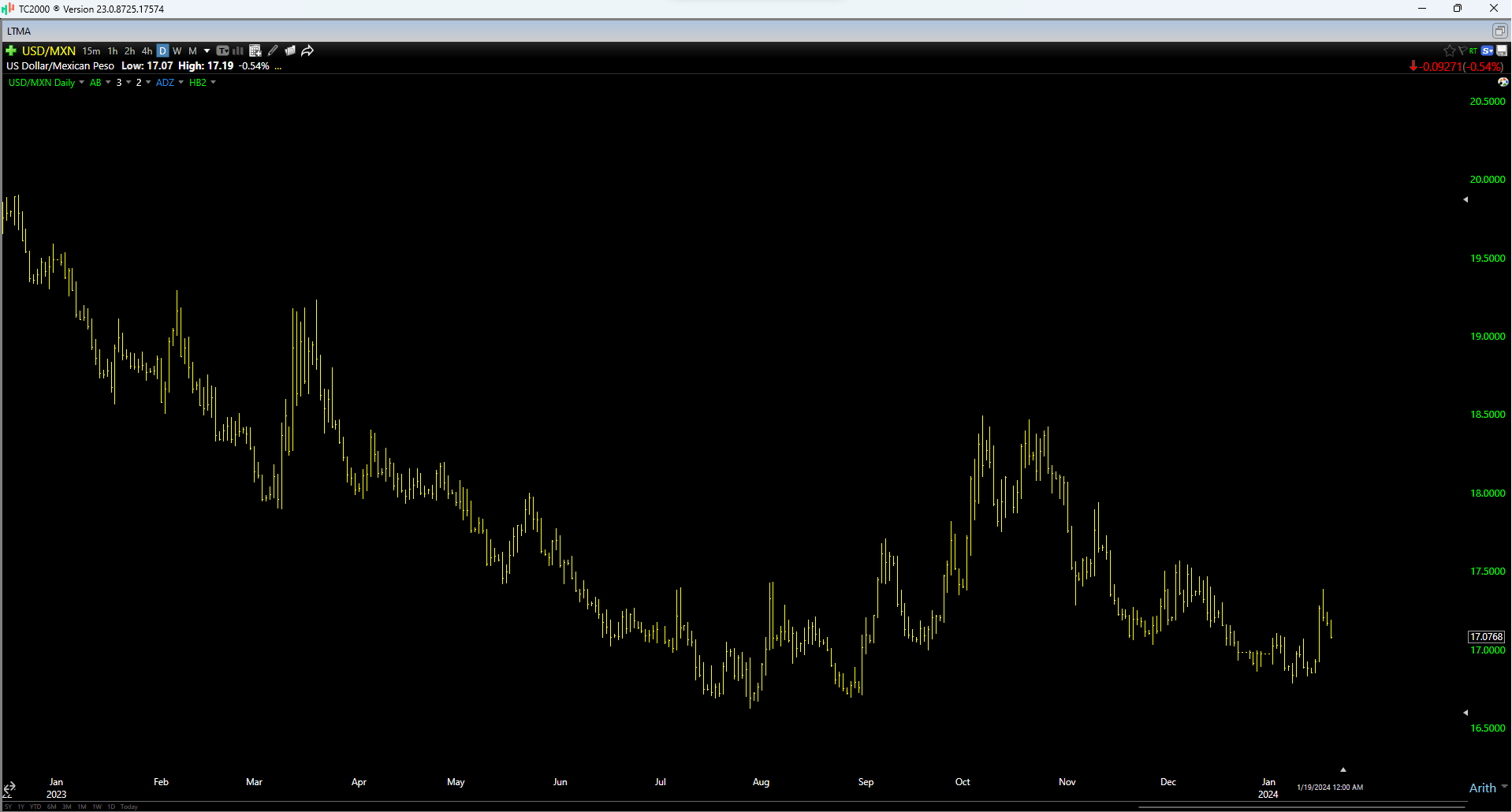

Digging into the production results a little closer, First Majestic's production at San Dimas improved slightly year-over-year to ~3.11 million SEOs, benefiting from higher silver grades (234 grams per tonne vs. 220 grams per tonne), offset by lower gold grades and lower silver recoveries. This led to the mine coming in slightly below its guidance of 12.9 to 13.7 million SEOs (actual: 12.8 million SEOs), and 2024 isn't looking much better with grades expected to decline nearly 10% at the mid-point to ~11.7 million SEOs. Worst, costs have been guided to ~$16.05/oz at the mid-point vs. ~$15.00/oz based on revised guidance in FY2023 and this is despite using an MXN/USD ratio of 18:1 vs. the current ratio of ~17:1 which continues to put a dent in margins for Mexican producers like Endeavour Silver and Fresnillo (as well as First Majestic).

First Majestic Silver Quarterly SEOs by Mine - Company Filings, Author's Chart USD/MXN Ratio - Worden

{kind=link}

{kind=link}

As for the company's Santa Elena operation, it was another solid year. Quarterly production came in at ~582,500 ounces of silver and ~28,100 ounces of gold, respectively (~3.0 million SEOs), a significant improvement from last year vs. ~20,100 ounces of gold and ~142,000 ounces of silver in Q4 2022. The increase in production can be attributed to higher gold grades from Ermitano and higher throughput rates (2,540 tonnes per day vs. 2,350 tonnes per day), as well as higher silver grades of 106 grams per tonne and significantly better recovery rates (73% vs. 52%) with the dual-circuit plant. This helped the operation to pick up slack across the portfolio, especially with Jerritt Canyon no longer online, and the company remains quite bullish on this asset with the view that it could potentially catch up to San Dimas from a production standpoint. That said, costs will be higher here as well in 2024, with costs guided for ~$17.25/oz at the high end vs. ~$16.00/oz for FY2023.

Ermitano Quarterly SEO Production - Company Filings, Author's Chart

{kind=link}

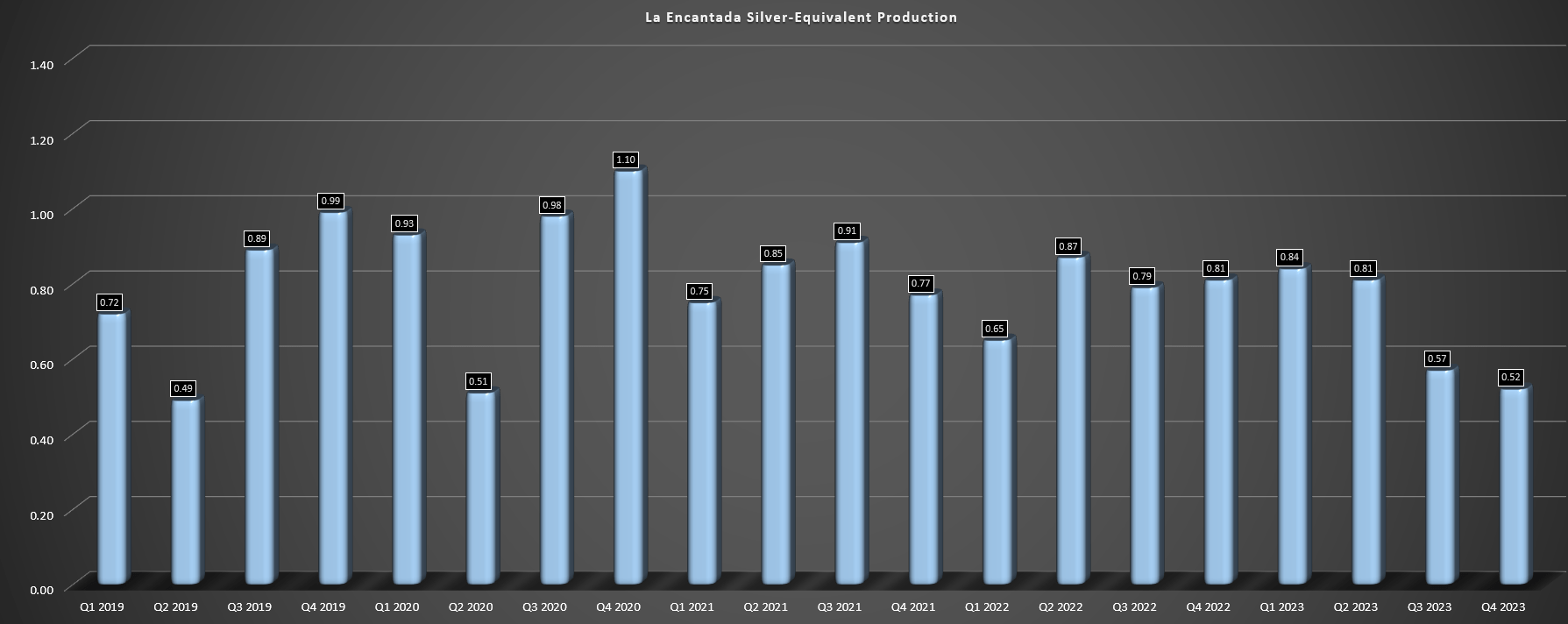

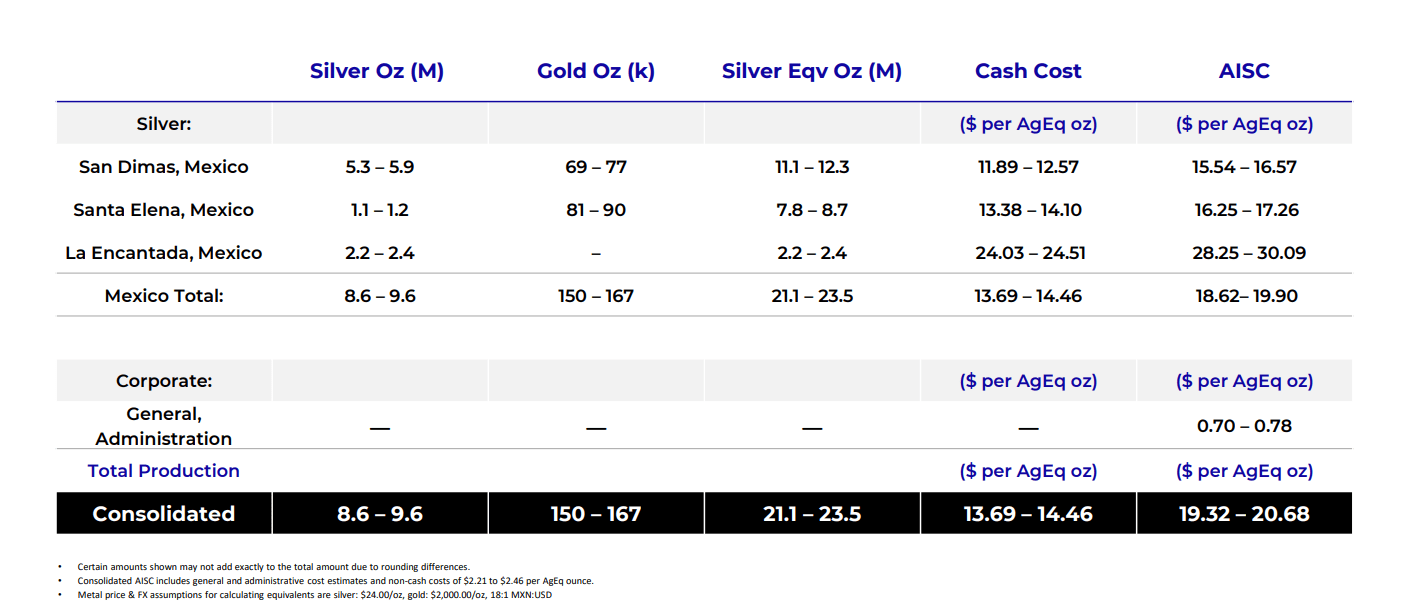

Unfortunately, the better performance at Santa Elena was overshadowed by a brutal second half for La Encantada, which produced just ~516,000 ounces in Q4 and ~0.52 million SEOs, with H2 production of ~1.1 million SEOs plunging relative to the ~1.6 million SEOs produced in H2 2022. The company noted that production was affected by the collapse of one of its wells (impacting water availability), but that production would normalize once construction of the replacement well is complete. However, First Majestic has shared that severe drought conditions affected existing water wells and, while three exploration and production holes drilled to source additional, they have had "limited success" . The result is that production is guided for a mere ~2.3 million SEOs at $29.17/oz at the mid-point, dragging company-wide costs.

If there're any positive takeaway from the recent news release, it's that the company appears to have guided conservatively at La Encantada, stating that while it believes an additional water source will be discovered to improve production and provide leveraged on fixed costs (which has dampened the cost outlook for next year), it provides to take a conservative approach. Hence, there looks to be some upside on production and potential improvement on costs at La Encantada. In summary, if the Mexican Peso can cool off and the company can improve the water situation at La Encantada, we could see all-in sustaining costs for the come in below the midpoint of ~$20.00/oz company-wide.

2024 Outlook

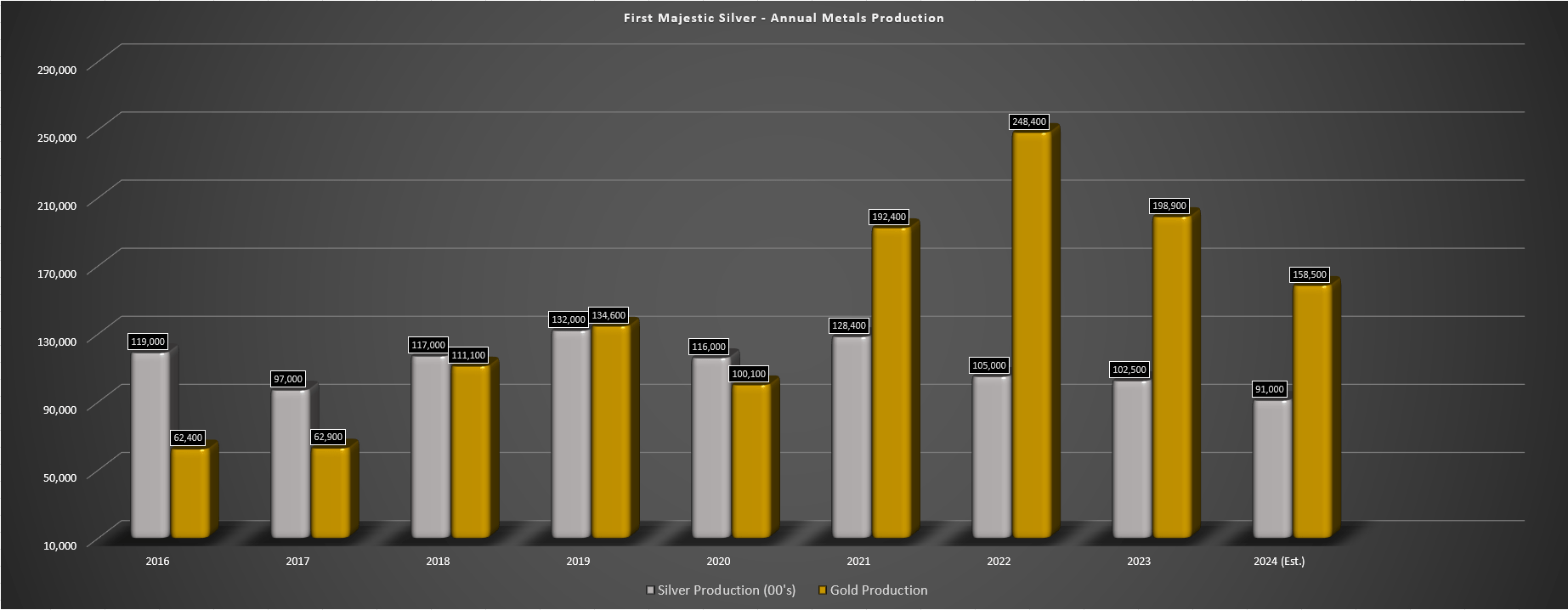

As for the consolidated 2024 outlook, there's not much to write home about, with First Majestic guiding for significantly lower production than at the onset of 2023 (~35.2 million SEOs), with FY2024 guidance sitting at 21.1 to 23.5 million SEOs and just ~9.1 million ounces of silver vs. ~10.5 million ounces produced last year. Worse, gold production estimates have been roughly halved to ~158,000 ounces vs. the high end of FY2023 guidance at 310,000 ounces of gold, impacted by the suspending of operations at Jerritt Canyon and lower gold grades at San Dimas. And while the 40 million silver-equivalent ounce goal looked to be within reach by 2025 with an optimized Jerritt Canyon, the company looks like it will be lucky to do 23 million SEOs.

2024 Guidance - Company Website

{kind=link}

From a cost standpoint, the results are even uglier, with all-in sustaining costs [AISC] set to come in near $20.00/oz, pointing to less than $100 million in operating cash flow this year even in an upside price scenario for gold and silver ($26.50/oz and $2,000/oz gold). If we compare this figure to planned capex of $125 million, this suggests continued free cash outflows, putting the risk of further share dilution on the table if gold and silver prices stay near current levels. And with the company already active on its ATM last year (~13.9 million at US$6.50 in first nine months of 2023), I would not be surprised to see upwards of 10 million shares sold this year, contributing to an additional ~3% share dilution. Finally, while the free cash outlook is poor, this will further dent already declining per share metrics (production per share) given that production was up barely 10% vs. Q4 2020 but the share count is up 30% from ~221 million shares to ~288 million shares, and that assumes no further dilution (which looks likely).

First Majestic Silver Annual Metals Production & 2024 Guidance Midpoint - Company Filings, Author's Chart & Company Guidance

{kind=link}

So, is there any good news?

While not much of a needle-mover, First Majestic has opened a minting facility and stated in its most recent conference call that this could contribute upwards of $25 million in revenue this year and potentially higher (representing ~5% of total revenue) with these sales coming in at higher average realized sales prices ( currently $26.50/oz for its 100 oz bars ). This certainly doesn't hurt when it comes to offsetting inflationary pressures with a portion of its sales at ~20% higher prices, and demand continues to be quite strong with most of its products sold out (with management also noting that revenue last year was constrained by supply but this will no longer be an issue). Overall, it will be interesting to see if First Majestic can get this minting facility up to $50 to $60 million in revenue later this decade, which would provide a low single-digit lift to its average selling price if accomplished.

First Majestic Silver Bullion - Company Website

{kind=link}

The other news worth reporting is that the company has not given up yet on Jerritt Canyon and plans to spend just shy of $30 million next year (including exploration) to work towards optimizing the asset for a potential restart. Management stated in the recent conference call that it's working to improve plant reliability given the harsh winters in Nevada and its mining plan, and while I have valued Jerritt Canyon at $200 million for now given the significant sunk costs, the combination of higher gold prices and a successful restart could significantly lift company-wide profitability (assuming the company can get costs below $1,700/oz AISC consistently). That said, I think it's best to be cautious on the future of Jerritt Canyon for now with this being a high-cost asset that would struggle to generate consistent free cash flow even at $2,000/oz without an improved mine plan.

"Jerritt Canyon has a lot of opportunities for improvement, and even though we've done the temporary suspension we've had teams working on many issues to get Jerritt Canyon positioned to restart. For example, we're looking at the plant because plant reliability towards the end of 2022 was quite difficult because of the record winter snowfall, so we looked at winterization issues on that plant, we have to do some work on the oxygen plant there, there's a whole number of issues we've gone through, and we've done that in great detail.

So we know what we need to know in the plant, we also know what we need to do in terms of gaining more confidence in the reserves and resources that we might have there, and that's why the exploration program is robust this year. And we also know that from that, we need an optimized mining plan before we make any kind of decision to restart. There's a lot of moving parts, we don't have a firm restart date, it'll depend on the results of many of these studies, including de-watering which is a major issue. So, we'll just have to see how these studies come through, and I'm sure in the future we can give better guidance."

- First Majestic Silver, January 2024 Guidance Conference Call

Valuation

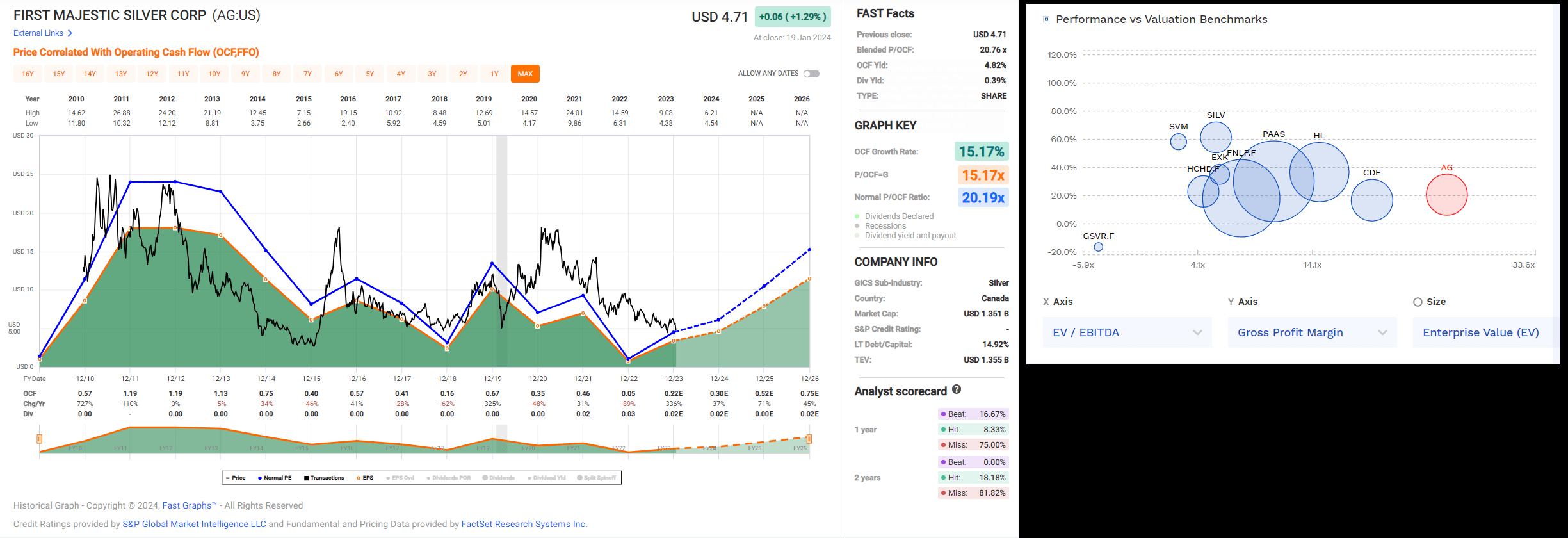

Based on ~297 million fully diluted shares (excluding warrants) and a share price of US$4.70, First Majestic trades at a market cap of ~$1.4 billion and an enterprise value of ~$1.48 billion. This continues to make First Majestic one of the higher capitalization names in the silver space. However, while the stock is down over 70% from its highs, the valuation continues to leave a lot to be desired. This is because First Majestic still trades at ~15x FY2024 cash flow per share estimates in a more bullish metals price scenario and over 2.0x P/NAV based on an estimated net asset value of ~$670 million (*), nearly 3x the multiple of B2Gold ( BTG ) with B2Gold sitting at ~4.8x FY2024 cash flow estimates and barely 0.80x P/NAV. And while B2Gold may not be a great comparison as a gold producer with the bulk of its NAV in Mali, First Majestic also trades at a premium to Tier-1 jurisdiction silver producers with lower costs like Hecla Mining ( HL ), which currently sits at ~12x FY2024 cash flow estimates and ~1.40x P/NAV.

(*) First Majestic's estimated net asset value of $670 million includes $200 million at Jerritt Canyon (which could end up being a liability with reclamation costs if it can't be restarted, and $200 million for its non-producing assets as well as exploration upside on producing assets). It also does not include any potential impact from existing tax disputes in Mexico. (*)

First Majestic Historical Cash Flow Multiple & Valuation/Margins vs. Peers - FASTGraphs, FinBox

{kind=link}

Given the stock's relatively expensive currency despite inferior margins, I'm surprised First Majestic hasn't been active on the M&A with its P/NAV and cash flow multiples still above its peer group, especially when many junior producers in more attractive jurisdictions trading at significant discounts to net asset value, and arguably the largest discounts in years. Recently, the company stated that a deal has to include silver, which certainly makes the list of potential projects quite small if it wants to avoid Mexico ( producer options ex-Mexico that it could swallow being Aya Gold & Silver, Americas Gold & Silver, though I'm not sure acquiring another high-cost operation is the right move in Galena's case ), I am surprised it's limiting itself to silver given that there are exceptional assets in the gold space on sale. And if cash flow and growth in NAV is what it needs to put a floor under its valuation and offset its shorter mine lives/higher cost assets, the commodity (gold or silver) shouldn't be a priority.

"As far as I'm concerned, it has to be silver. And it needs to be in production. So we're, we cannot fill our portfolio with a bunch of exploration projects and that does make the space you know a lot smaller than others may think".

- First Majestic Silver, January 2024 Guidance Conference Call

To summarize, with shorter reserve lives, industry-lagging margins, high concentration to a Mexico, and no margin of safety at current levels from a valuation standpoint, I continue to see the stock as un-investable. That said, if the stock were to branch out into another with a higher-margin asset to increase its weighted-average mine life and NAV, I would be more open to owning the stock.

Summary

First Majestic Silver had a tough Q4 with lower output from La Encantada and FY2024 isn't expected to be much better with lower production at higher costs and a further decline in per share metrics. Unfortunately, these per share metrics could worsen if the company continues to lean on its ATM in this period of negative free cash flow, and while I remain cautiously optimistic on Jerritt Canyon in a higher gold price environment with a better mine plan with additional optimization work, I think it's hard to assign much value to this asset today which leaves AG overvalued relative to peers on a P/NAV basis.

Hence, with no margin of safety at current levels, risk of further share dilution and significant concentration to Mexico which is a non Tier-1 ranked jurisdiction, I continue to see far more attractive bets elsewhere in the sector. Among medium-risk names, B2Gold is a preferred option, trading at less than ~5.4x FY2025 free cash flow estimates with a 5.2% dividend yield. Among lower-risk names, Agnico Eagle ( AEM ) looks quite attractive ahead of its Q4/FY2024 results with the company often over-delivering on promises and now back to trading at one of its lower cash flow multiples in years (~8.2x vs. 10-year average of 13.5x).

For further details see:

First Majestic Silver: A Weak Q4 With A High-Cost Year On Deck