WFC - First Republic Is Likely The Next Shoe To Drop

2023-04-27 14:19:24 ET

Summary

- The situation at San Francisco-based First Republic appears to be rapidly deteriorating, according to a flurry of reporting over the past few days.

- As of the end of last year, First Republic was America's 14th largest bank.

- Bloomberg recently reported that the FDIC is considering curbing new borrowing by the bank, while CNBC reported that the bank's Hail Mary to the White House apparently had failed.

- First Republic could likely be closed by the FDIC and, as such, may be worth $0.

Since its IPO in 2010, First Republic Bank ( FRC ) was one of the hottest financial stocks in America. Everywhere there was tech money, Bay Area-based First Republic was there as well, with the company even operating a branch inside the headquarters of Facebook (META). First Republic thrived off of offering wealth management to high-net-worth individuals and offered sweetheart deals on interest-only, ARM, and superjumbo mortgages. In a world where property values only went up and interest rates only went down, this was a one-way ticket to profits. The bank used the profits they made to lever up and make even more loans, creating a virtuous circle. It worked wonderfully -until it didn't.

What We Know

FRC stock is now down roughly 95% for the year, the company's credit rating is destroyed , and Bloomberg reported that the bank hired a senior Obama administration staffer to try to negotiate a bailout from the federal government. Poetically, this comes after Fortune reported last month that the bank had lobbied for weaker financial regulation before the crisis - arguing that they weren't too big to fail.

Of course, the bank is now pleading that they're too big to fail, with reporting from CNBC indicating that the bank's pitch to competitors is that they should buy First Republic's assets for more than their market value because they'll pay even more in FDIC assessments if FRC is liquidated. You can't make this stuff up!

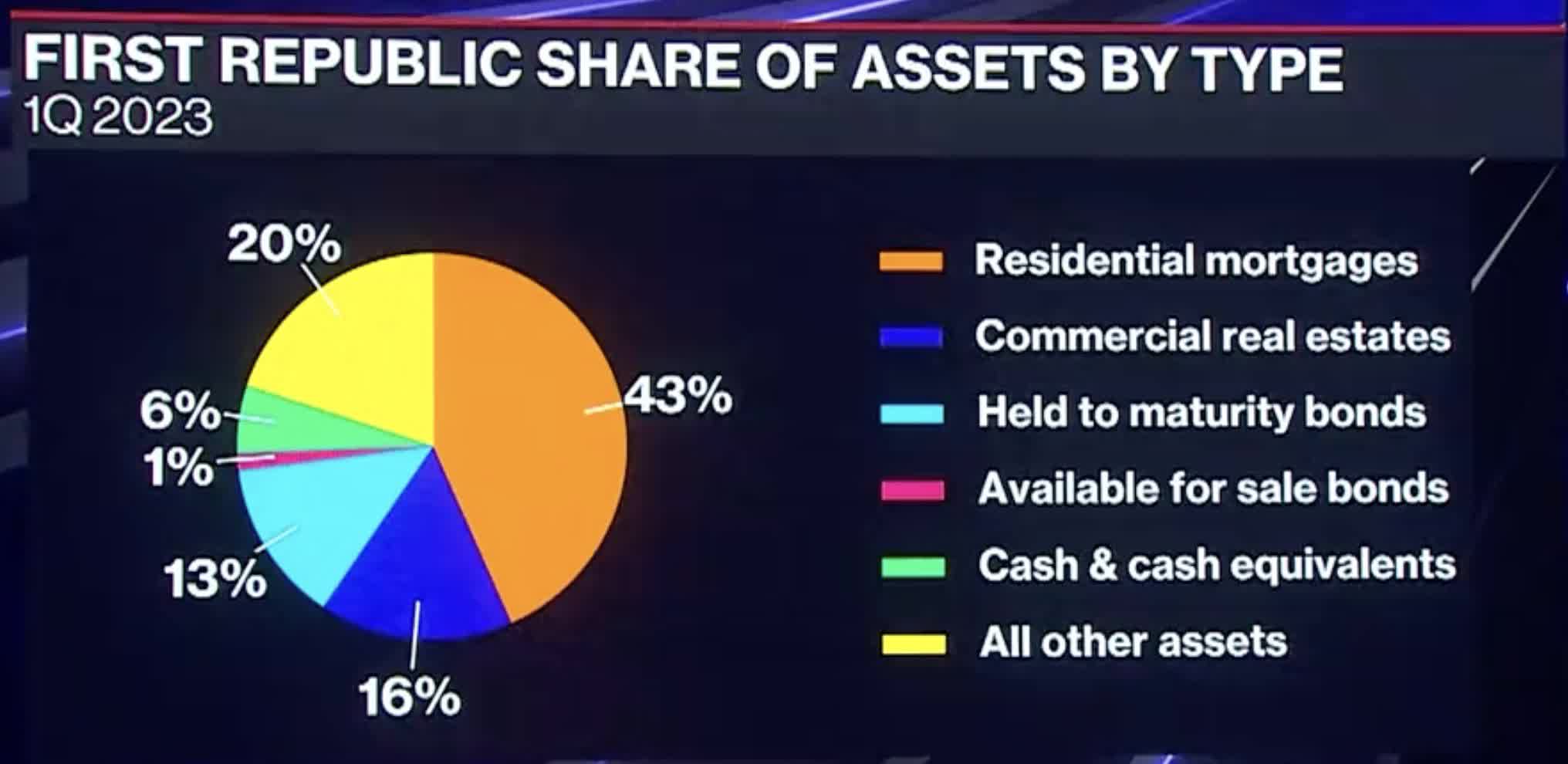

After losing much of its deposits, First Republic appears to be about $25 billion in the hole . Its assets are esoteric and illiquid- most of its assets are jumbo and super jumbo mortgages, while its deposits are largely now gone.

First Republic Assets (Bloomberg)

{kind=link}

Who is going to want to buy $100 billion in below-market mortgages on a bunch of mansions in California and the Hamptons ? According to Bloomberg, at least $20 billion of these are interest-only.

The only real collateral here is that someone rich said they'd pay First Republic back, but many of their clients made the same wrong bets on interest rates that the bank itself did. The price declines in San Francisco since the peak mean that many of these 2021 loans are likely to be underwater now, with barely any interest to cover defaults.

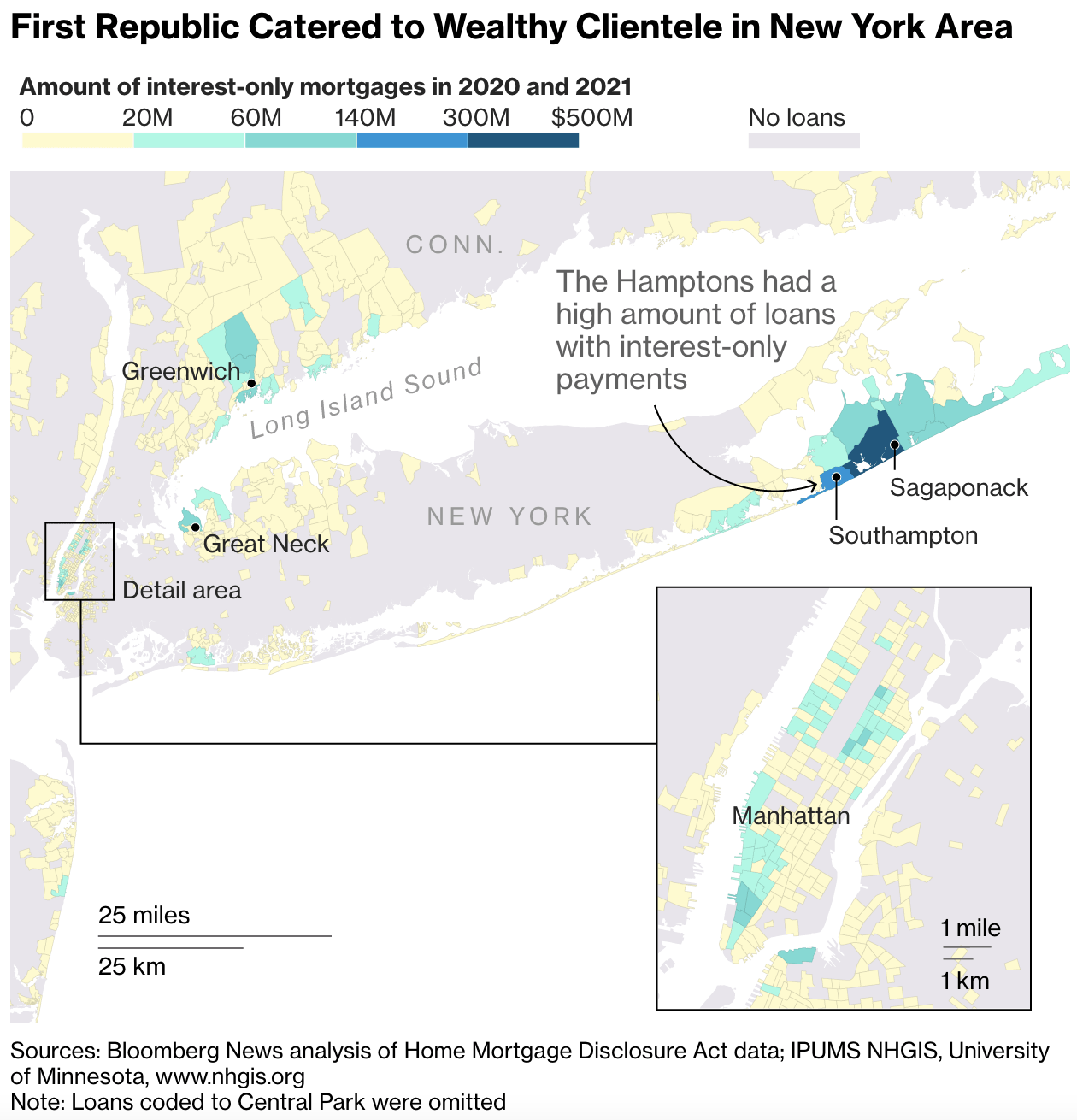

New York

First Republic Loans- New York (Bloomberg)

{kind=link}

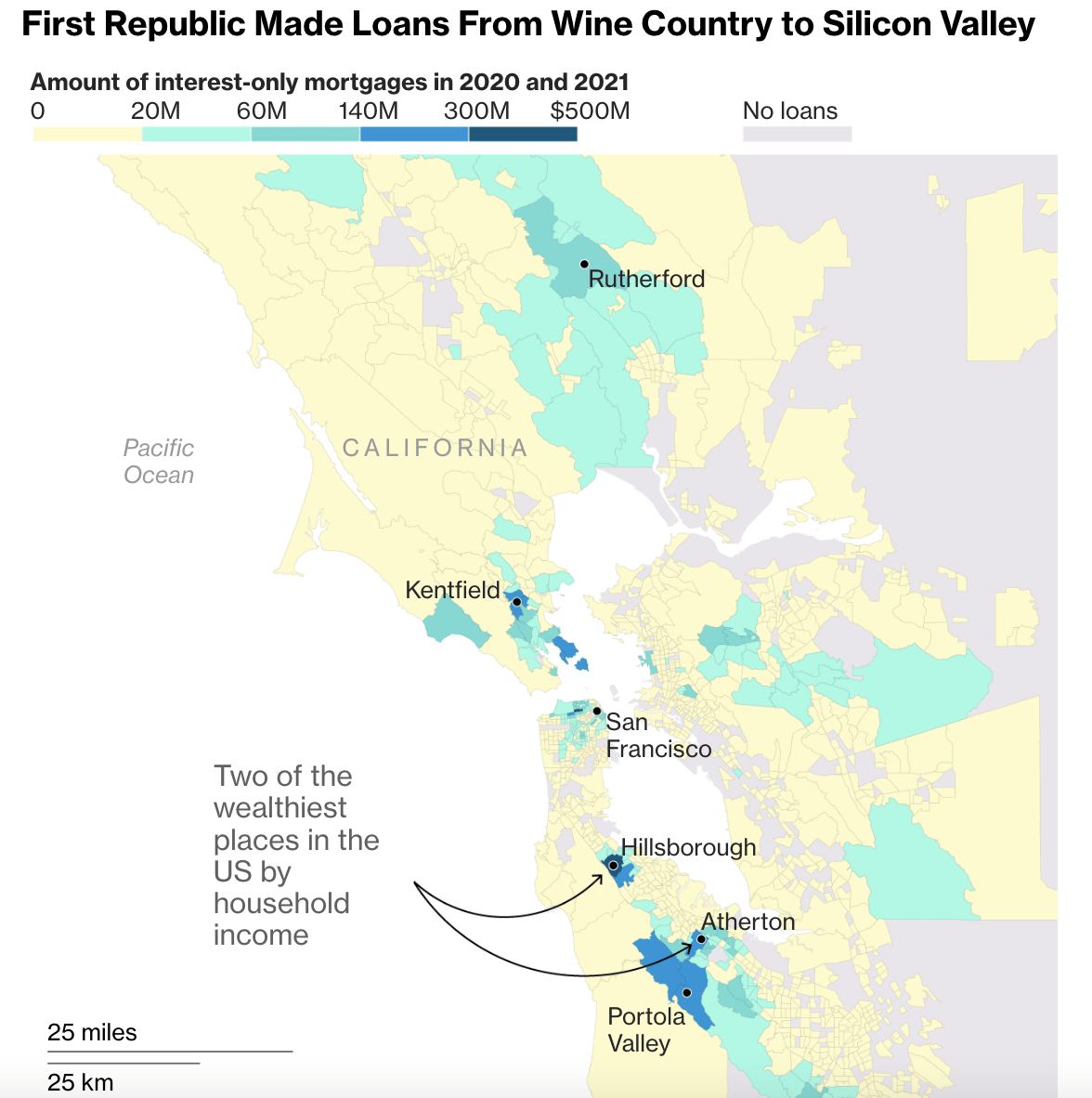

San Francisco Bay Area

First Republic Loans-San Francisco Bay Area (Bloomberg)

{kind=link}

They have commercial mortgages as well, and they have some business loans. Of these, the business loans are probably the most soundly underwritten, while the mortgages clearly weren't. Why? Because they were never meant to be. The mortgages appear to have been underwritten as a loss leader to bring in profitable wealth management business. This loss leader is invisible if times are good, but they sold a very cheap put option to some very rich people on the ultra-luxury housing market.

To these points:

- If JPMorgan (JPM) and Wells Fargo (WFC) thought it was a good idea to bail out First Republic's $25 billion in losses on mortgages, they would have likely done so already.

- Since this bank clientele was a who's who of tech and finance elites, the Biden administration probably isn't going to be thrilled to bail them out. And why would they? The FDIC was designed to deal with situations just like this, and as First Republic had argued for years, they're not too big to go into receivership. To no one's surprise, sources have indicated to CNBC that the government i s not currently thrilled about a bailout for First Republic.

Uninsured deposits are still a problem for First Republic. If you have money at this bank over the $250,000 FDIC limit, there's a >99% chance the government will cover you. But there's no upside to leaving your money there, because if the FDIC guarantee is applied technically as it's written, you lose everything. Likely? No. A risk you should take? Also no.

Also, First Republic's management refused to take any questions from analysts after their earnings call this week. They were likely advised by their lawyers to do this, but if you're a troubled bank, you need to step up and reassure your customers, not do the corporate equivalent of taking the fifth.

What We Don't Know

We don't know whether depositors are continuing to withdraw money from the bank, although it's likely. We do know that the FDIC and Fed are running out of patience and are considering cutting the bank off from new borrowing. The reason for this is that while giving the bank time to get things together is good for financial stability - if that time is squandered, then it serves to inflict even greater losses on taxpayers.

We also don't know whether there could be some sort of Credit Suisse-type deal with First Republic where the company is bought for a few cents on the dollar. However, this is problematic because doing so would set a bad precedent unless the preferred shares were also paid in full.

FRC's preferred shares ( FRC.PI ), ( FRC.PH ) are trading around 15 cents on the dollar, which is more than zero. However, since the preferreds are legally required in the US to be paid before the common shareholders, this indicates that the common stock in FRC could be worth $0.

It's a fair question as to whether a political deal could extract some value for FRC shareholders, but the optics are terrible. Uninsured depositors are very likely to be covered by the FDIC and Fed, whereas common and preferred shareholders are very likely to be wiped out. The company's bonds were trading for around 50 cents on the dollar this week. That's not a great sign for common equity holders. We also don't know if the government will give FRC some more time. If it appears that depositor withdrawals are going to inflict more losses on taxpayers, they'll probably seize the bank sooner rather than later.

What does this mean for the broader market? Inflation is still much too high , as this morning's GDP report showed. Whatever happens with First Republic, the Fed is still set to hike next week. First Republic built its business model around interest rates only going down, and when they went up, the bank imploded.

Bottom Line

My sense is that First Republic Bank will be closed in the next few weeks, possibly as soon as this weekend. There's a >99% chance that uninsured depositors will be paid in full and a >90% chance that the common equity goes to zero, barring some sort of political takeunder by a competitor. This is not currently a threat to the overall financial system, but an example of a large bank using too much leverage in a zero-rate world and flying too close to the sun.

For further details see:

First Republic Is Likely The Next Shoe To Drop