FVRR - Fiverr: Cash Is King

2023-04-21 16:01:58 ET

Summary

- Upon mixed Q4 results and weak outlook into Q1 and FY 2023 that suggest continuing macro-driven slowdown, FVRR has been under selling pressure.

- Prolonged downturn is a risk, but FVRR is well-positioned for a strong rebound. Ongoing upmarket move will also minimize cyclicality.

- Cash is king. FVRR's proven ability in consistent operating CF generation is an evidence of solid business model and disciplined execution.

Fiverr ( FVRR ) is one of the tech stocks I have been following for some time. My most recent coverage was in June 2020 , when the stock was trading at $60+ per share and on an upward momentum due to the remote work trend as a result of COVID-19. Then, I initiated an overweight rating on the stock based on the business’ overall strength across growth and profitability.

Obviously, the stock performed exceedingly well and reached an all-time high of $320+ per share back in February 2021, before facing massive selling pressure as a result of post-pandemic macro headwinds that depressed its growth for most of 2022 and into 2023.

As the share price has been forced to retreat to $35+ per share today, I continue to maintain my buy rating for the stock for a few reasons:

- Fiverr has a scalable e-commerce marketplace business model with a consistent track record of operating cash flow / OCF generation over the last 3 years.

- Price pressure is temporary. Aside from a tough compare, what has depressed Fiverr’s growth is the muted spending growth of its core buyer segment, the SMBs, which has been affected the most by the toughening macro situation. As the macro outlook is expectedly set to improve beyond 2023, so is Fiverr’s growth.

- Fiverr’s ongoing progress upmarket should reduce over-dependence on the SMBs segment, and diversify the business to better absorb the impact of future economic shocks.

Ultimately, as I integrate my version of growth story into the target price model, I found that the stock is undervalued today. My bullish call highlights the opportunity to accumulate position before the imminent rebound.

Q4 and Financial Review

Upon mixed Q4 results, Fiverr started trading ~11% lower from its then-current level of $44 per share over the following week and then continued its downtrend to reach $35+ today. Aside from missing the revenue estimate, I think that the weak outlook into Q1 and the rest of FY 2023 also played a part in driving selling pressure. Here is the recap of Fiverr’s Q4 :

- Q4 2022 revenue of $83.1 million represents merely a +4.2% YoY, which missed the estimate by $0.36 million. In addition to the tough compare from last year, the slowdown in the SMB segment due to the macro headwind is clearly apparent. Revenue for FY 2022 was $337.3 million, an increase of 13.3% YoY.

- Q4 active buyers grew to 4.3 million, an increase of 1% YoY. On the other hand, spend per buyer increased by 8% YoY to $262. Here, we see some indication of Fiverr’s progress towards upmarket. Consequently, customers with annual spending of $10k also grew by 29% YoY, surpassing the growth of other customer segments.

- Fiverr also continued to maintain a steady increase in its take rate every year. FY 2022’s take rate is +30%, higher than the 27% - 29% level in previous years.

- For Q1 2023, Fiverr expects revenue of $86.5 million - $88.5 million (0% - 2% YoY growth) and adjusted EBITDA between $9.0 million - $10.5 million.

- For FY 2023 Fiverr expects revenue of $350.0 - $365.0 million (4% - 8% YoY growth) and adjusted EBITDA of $45.0 million - $55.0 million.

It appears that Fiverr’s growth is to slow down into FY 2023 due to the tough macro situation affecting the spending activities of its core customers, the SMBs. I think that it is a temporary headwind that should soften anytime after FY 2023. In fact, investors who base their selling decision based on that factor alone are missing the big picture.

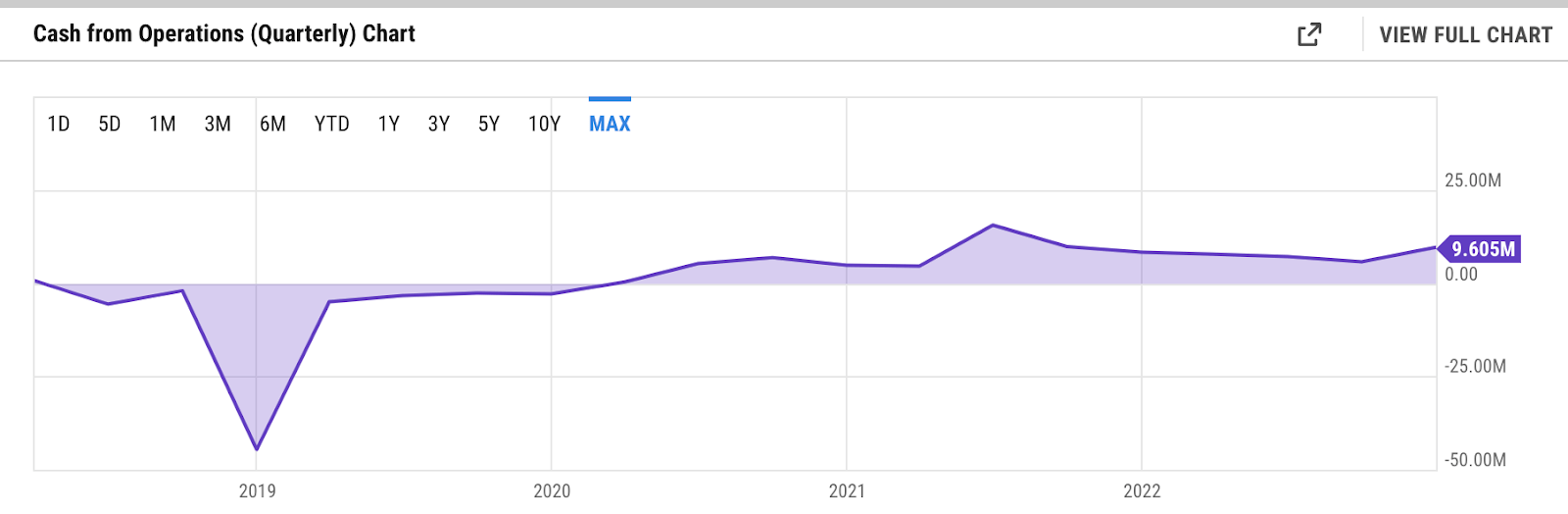

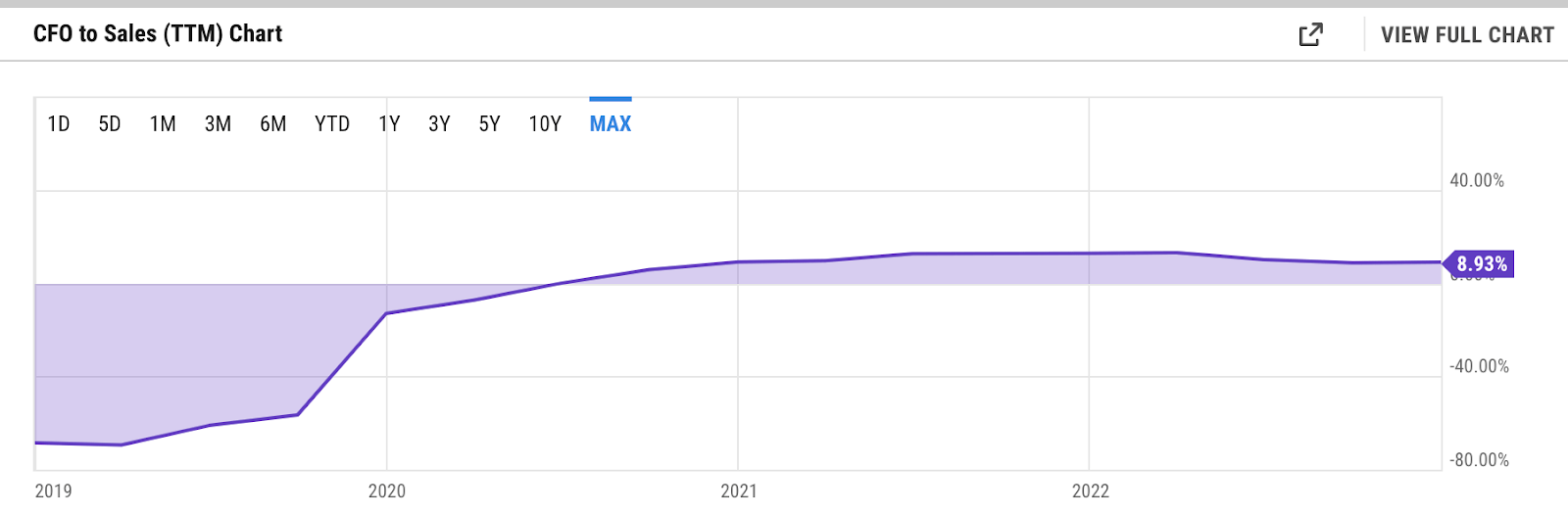

In any given situation, and most importantly during the downturn, cash is king. As it stands, Fiverr has a highly scalable e-commerce marketplace business model with proven capability to generate OCFs. Since 2020, OCF has been positive and on an upward trend every quarter - I think that the level of consistency is really strong here, indicating a solid business model.

{kind=link}

While the credit also goes to the management, who reiterates the commitment to build Fiverr as a business aiming for profitable growth, I have seen many e-commerce marketplace businesses struggle to generate OCFs due to inherent weakness in business and operating models.

{kind=link}

In most cases, those businesses also fall into a trap of chasing high growth with little regard to the bottom line. That is not the case with Fiverr, which has been very disciplined. As the remote working trend accelerated between 2020 - 2021, Fiverr took that opportunity to not only grow its top line but also OCF generation. Revenue growth was ~77% and ~57% annually in 2020 and 2021, but OCF margin was also steady in that period, and even expanded from +9% level to +12%. As growth subsided in 2022, Fiverr continued to be prudent with its marketing spending and managed to keep OCF margin at ~9%, though OCF actually increased on an absolute basis to +$9.6 million.

Business Model and Growth Strategy Review

Fiverr is an e-commerce platform with a marketplace business model that connects businesses of all sizes, including sole proprietors (the buyers) with freelancers (the sellers). As a two-sided marketplace, it charges a commission and service fee on any successful transaction within the platform.

FVRR Q4 presentation - business model

Buyers can search for sellers based on service categories relevant to their needs. Fiverr currently has over 600 categories. When a buyer finds a seller they are interested in working with, they can converse through the platform's messaging system. The buyer and seller can discuss the project details, including scope, timeline, and budget. Once they agree on the terms, the buyer can place an order through the platform, and the seller would then start working on the project. For any successful transaction, Fiverr would then take a commission, which varies based on the transaction value.

As in any two-sided marketplace model , optimizing sales and marketing activities to drive higher frictionless conversions, retention, and repeat purchases is the norm. The end product of all that is eventually sustainable revenue growth. It seems like a straightforward process but is marred with various moving parts. From a buyer’s point of view, for example, it takes several steps and sub-steps before a transaction can happen:

- Awareness: Buyers become aware of the platform through advertising, search engines / SEO, or social media.

- Consideration: Buyers consider the platform by browsing services, reading reviews, and comparing prices.

- Conversion: Buyers convert into active users by registering, creating profiles, and making purchases.

I think in general, Fiverr has applied an already effective yet disciplined approach in executing those activities and managing retention and repeat buying. The rule of thumb in this model is making sure that the LTV (Lifetime Value) of a user is higher than its CaC (Customer Acquisition Cost). In a less-desired scenario, a platform may be tempted to drive growth by making unsustainable conversions, effectively maintaining a very low LTV to CaC ratio and negatively affecting the bottom line and cash flows. While I have seen many tech companies resorting to such practices, it does not seem to be the case with Fiverr.

To grow the business, Fiverr can either increase the number of categories or increase the spend-per-buyer while maintaining the balance between the number of freelancers (supply) and the buyers (demand).

Aside from applying organic growth strategies by improving the ease of use and comparability of the platform, the company has also made ~$96 million worth of acquisition deals to target those parameters since 2021:

- Working Not Working : a platform that connects high-end creative freelancers with businesses. The acquisition helped Fiverr expand its categories in the creative industry and also improve spend per buyer.

- CreativeLive : an online learning platform that offers classes and workshops in various creative fields, such as photography, design, music, and entrepreneurship. The platform features live and pre-recorded classes taught by industry experts. The acquisition helped Fiverr expand its creative categories, target the growing vocational education market, and access CreativeLive's existing user base that can potentially convert into freelancers at Fiverr’s platform.

- Stoke Talent : a platform that offers a freelance management system designed to help businesses manage their freelance workforce. The acquisition helped Fiverr to boost the capability of Fiverr Business platform, in addition to access Stoke Talent’s customer base to target higher spend per buyer.

Valuation / Pricing

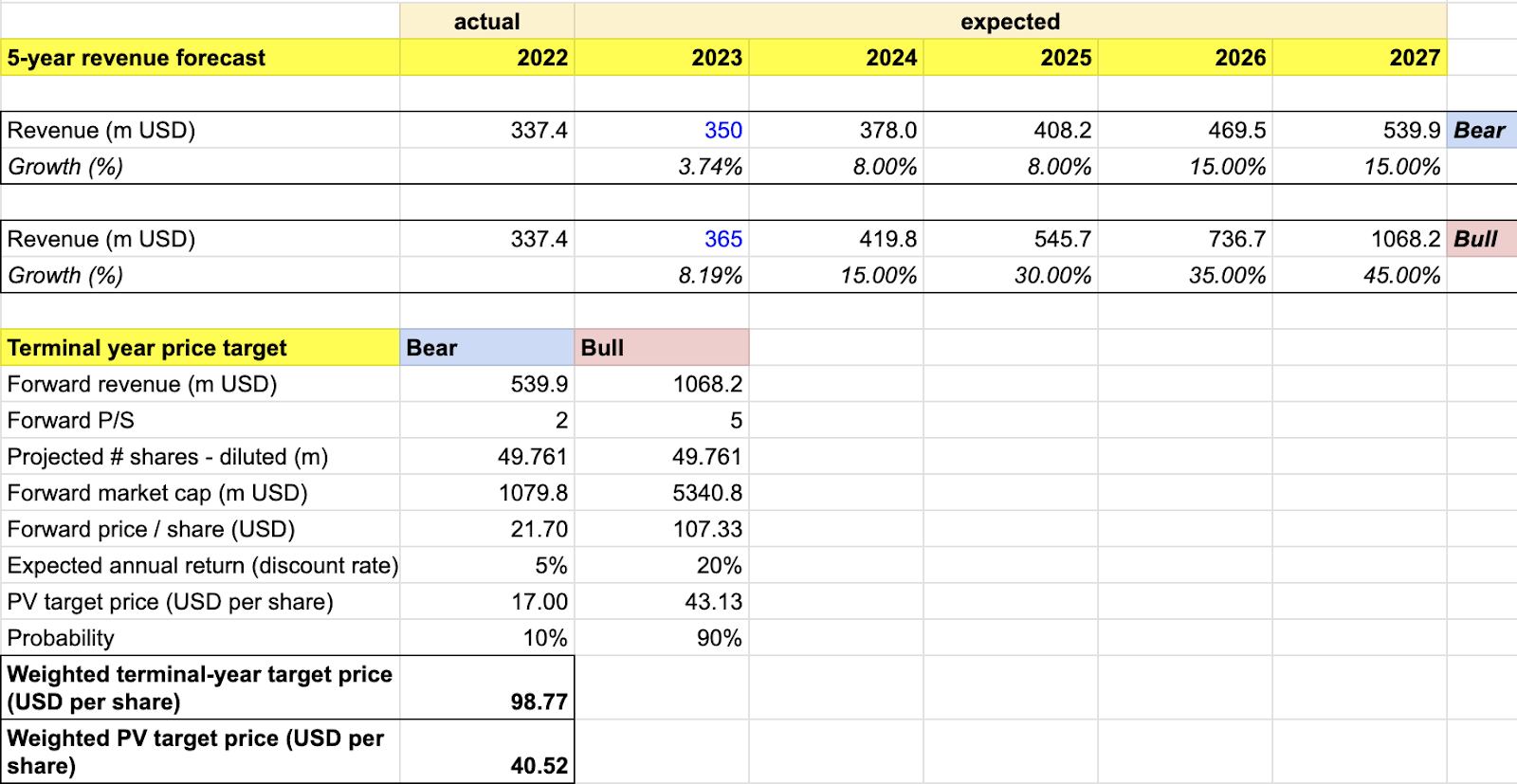

In estimating the stock’s fair price today, I consider two extreme probability-based scenarios in the 5-year target price model for my overweight call:

- Bear scenario (10% probability): I assume the macro slowdown to continue until FY 2024, followed by a series of weak rebounds all the way to FY 2027. Output-wise, I expect slowing growth reacceleration that leaves Fiverr with 8% - 15% annual growth and ~2x P/S multiple. I applied a lower valuation multiple than the already-depressed ~3x P/S today.

- Bull scenario (90% probability): I assume the macro slowdown to subside starting in FY 2024, allowing Fiverr to reclaim a double-digit revenue growth of 15% in FY 2024. Growth would then reaccelerate every year to reach ~45% annual growth in FY 2027, comparable to the pre-COVID level. I also assume P/S to expand from the current level to ~5x, which is very conservative, considering the stock still traded at least at ~7x P/S pre-tailwind-driven period in 2020 - 2021.

author's analysis - price target FVRR

{kind=link}

I consolidate the two scenarios by estimating the probability-weighted target price for FY 2027 and then discount that price back using two different discount rates. In my bearish scenario, I applied a merely 5% discount rate to the FY 2027 fair value of +$21 per share, which is already lower than today's price level, indicating an overvaluation. In contrast, my bullish scenario points to a 20% annual return (discount rate) over the next five years to an FY 2027 price of $107+ from a possible entry point of $43 per share today.

I arrived at a weighted target price of ~$99 per share for FY 2027, which is comparable to $40 per share today. This $40 would be the maximum entry point to initiate a long position to realize the probability-weighted annual return in the model.

It simply means that at ~$35 today, Fiverr is still undervalued by 12.5%, giving room for investors to realize excess returns if Fiverr is to achieve or outperform my conservatively bullish projection.

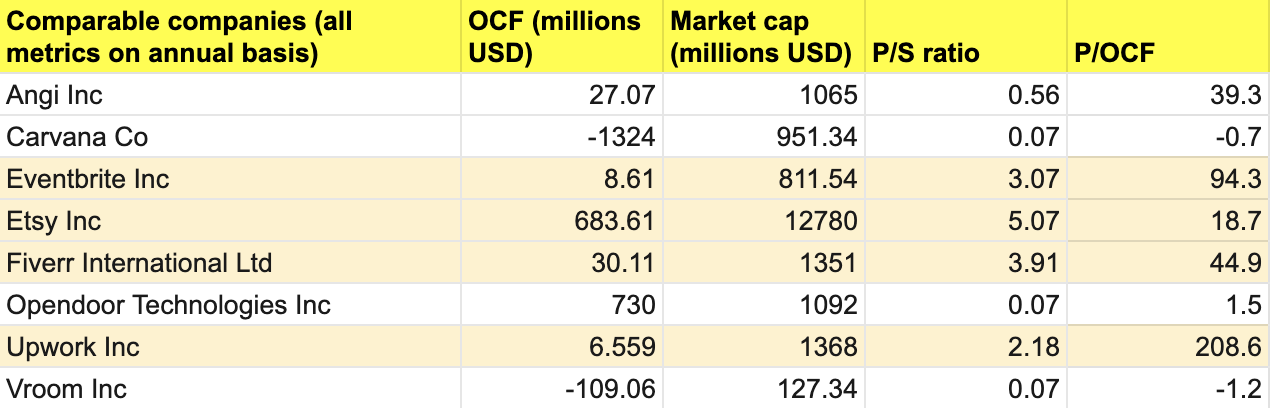

Valuation multiple wise, the ~3x P/S today is also attractive. On the other hand, while Fiverr's current P/OCF of ~45x appears a bit high, it is important to note that the company does not guide to OCF despite its profitable growth objective. As such, while Fiverr has been consistent in OCF generation, it is still a growth stock with an expectation of steady revenue uptrend more reliably measured with P/S.

author's own analysis - FVRR comparable

{kind=link}

Comparing Fiverr to other growth stocks with a similar e-commerce business model such as Upwork, Etsy ( ETSY ), or Eventbrite ( EB ) in terms of P/S also leads to a lower variability than it does in terms of P/OCF. Nonetheless, Fiverr's P/OCF is also much lower than Upwork's, its direct competitor.

Risk

I consider Fiverr’s high dependency on SMB segments, prolonged macro slowdown, and intense competition in the upmarket segment as key risk factors of the business. In a way, all these three risk factors are correlated with each other.

The biggest near-term risk for Fiverr today, though, remains the macro slowdown. Given the uncertainty of how long the current economic downturn will last, revenue growth should slow down into the near future, pressuring the share price with no line of sight to a rebound even towards the end of FY 2023.

The fact that SMBs make up the majority of Fiverr’s customers is another risk factor that further amplifies the macro risk. This heavy SMB concentration is a risk factor that Fiverr has not yet neutralized, yet is working towards minimizing it. As we have seen in the current situation, an economic downturn that greatly affects SMBs' spending would significantly affect Fiverr’s growth.

Fiverr has attempted to diversify its revenue base by targeting more upmarket customers with the launch of Fiverr Business in 2020. Nonetheless, it is a competitive segment that is relatively new to Fiverr. The encouraging uptrend in spend-per-buyer in Q4 still does not yet tell us the details of how well Fiverr is positioned in this new segment.

The business today faces competition from Upwork (UPWK), Toptal, Topcoder, all of which are differentiated by their strong positioning in the upmarket segment across particular categories. Topcoder, for instance, specializes in connecting businesses with freelance workers in high-value categories such as software development and data science. In contrast, Fiverr has historically been more of a mass-market freelance marketplace platform targeting SMBs.

As much as Fiverr’s core e-commerce marketplace business model is a solid cash-flow generator, it is highly optimized more towards SMBs than upmarket buyers. I think that Fiverr is in fact a market leader in the SMB segment. With over 600 categories with price points ranging from $5 all the way to thousands of dollars, the core platform generally relies on frictionless purchases of freelancing services to drive scalable growth. While the process fits the decision-making processes of most SMBs seeking freelance workers, it has little relevance towards onboarding upmarket customers, which requires a more dedicated go-to-market approach and a different set of features.

Conclusion

I continue to favor the stock today, despite it being under pressure. It is one of the few companies with an e-commerce marketplace business model that has demonstrated the ability to generate positive OCF.

I also credit the management for being very disciplined and long-term-minded in the execution. The emphasis on cash generation and profitability is the right thing to do given the depressed growth environment. Fiverr has been doing its best to control what it can control by diversifying its revenue stream by moving more upmarket, as well as by improving the platform experience to increase conversion.

The possibility of a prolonged economic downturn remains the most immediate key risk. It not only significantly depresses the business’ growth today, but also distracts Fiverr’s overall execution to improve its strategic positioning. To that extent, Fiverr's proven ability to generate and accumulate operating cash flows out of its solid and scalable business model is the key to weather that storm.

For further details see:

Fiverr: Cash Is King