FVRR - Fiverr International: Solid Company With Decent Risk/Reward

2023-08-02 01:50:39 ET

Summary

- Fiverr International may be undervalued and a good long-term investment opportunity, especially if AI enhances customer experience and global economic sentiment improves.

- The company's outlook is positive, with the potential for AI to create new gig opportunities and an expected increase in spending as inflation falls and purchasing power improves.

- FVRR stock has a large addressable market and potential for growth in the gig platform industry.

Investment Thesis

I wanted to take a look at Fiverr International ( FVRR ) before the upcoming quarterly announcement to see what the outlook for the company in the long run is and whether the current share price is a good entry point for a long-term investor. With somewhat conservative estimates in my opinion, the company is undervalued right now and may be a good investment if the potential for AI to enhance customer experience and the negative sentiment in the global economy shifts to a more positive view.

Outlook

During the last quarterly report , the management was very excited about the emergence of AI and how it is going to impact the company positively in the long run. The management noted that the search for AI-related gigs has soared over 1000% compared to six months ago. I am also in the same boat, which is that AI is not going to replace current sellers of services and will mostly create new gig opportunities in the long run. Creativity is one of the main attributes of humans and it would be very hard to replicate human passion and heart when it comes to providing a particular service that needs to be unique for every customer. Sure, you can ask AI to come up with something on the spot but that will be sourced from millions of data points online, and as Take-Two ( TTWO ) CEO Strauss Zelnick said, "Hits are created by genius. And data sets plus compute plus large language models do not equal genius. Genius is the domain of human beings and I believe will stay that way." I can see the company's total number of buyers on the platform remaining strong and rising over the next decade because of the influx of new technologies that need to be mastered.

2022 was a tough year for many if not everyone. I believe that with the falling inflation, people will start to get back more of their purchasing power, which will lead to spending picking up again. That is on an individual and business basis. The management mentioned that SMBs are spending less than usual right now, however, I believe the cyclicality will turn positive in '24 and beyond, and the company will once again start to see higher revenue growth.

The last couple of years I would say played a large role in the company's revenue growth as many businesses and people realized that we could do a lot of the jobs online with just a laptop and a decent internet connection thanks to the pandemic.

Micha Kauffman, the CEO of Fiverr, has been saying for many years now that most of the freelancing is still done offline, so the total addressable market opportunity is vast for the company if it manages to execute its marketing strategy. Micha has been quoting that around 3% of freelance work has been done online while the remainder is offline for years not, which coincides with this slightly outdated report that shows about 1% of gig workers are working through an online platform. In a more recent article , we can see that online platform gig work has more than doubled during the pandemic, so things are starting to shift and I believe the more we are advancing through technology, the more people will work online as I think that is much more efficient.

Margins

The company is spending a lot of money on sales and marketing every year. In terms of % of revenue, this number has come down slightly from FY21, but it still is almost 52% of total revenues, which makes the company unprofitable on a GAAP basis. The big culprit of this is stock-based compensation. I can see this continuing for a while still mainly because the company does need to be active/aggressive when it comes to promoting the platform to the wider audience, to show that this is an effective way of doing business for your enterprise, which can be more tailored for your needs. I would like to see this coming down eventually because I am not a big fan of adjusted metrics, but I will amuse the company for now because I do believe that it has a lot of potential in the future.

Financials

As of Q1 '23 , the company had around $94m in cash and around $235m in marketable securities, bringing total liquidity to over $320m against no long-term debt. The company does have around $450m in convertible bonds that mature in '25, so that will need to be repaid then or if the share price goes above $213.57 a share, the company will have to issue more shares because the holders of the bond will want to convert. This will dilute the company's total share outstanding, however, by not that much, and if the share price does get to that price in the next 2 years, I am sure investors won't mind slight dilution since the share price is going to 6x from current levels.

I don't think it's going to happen and the company will most likely have to pay back the bond debt, and it seems the debt is 0% interest so the company doesn't have to pay any annual interest expense on those notes, which is good for a company that is not making any money right now.

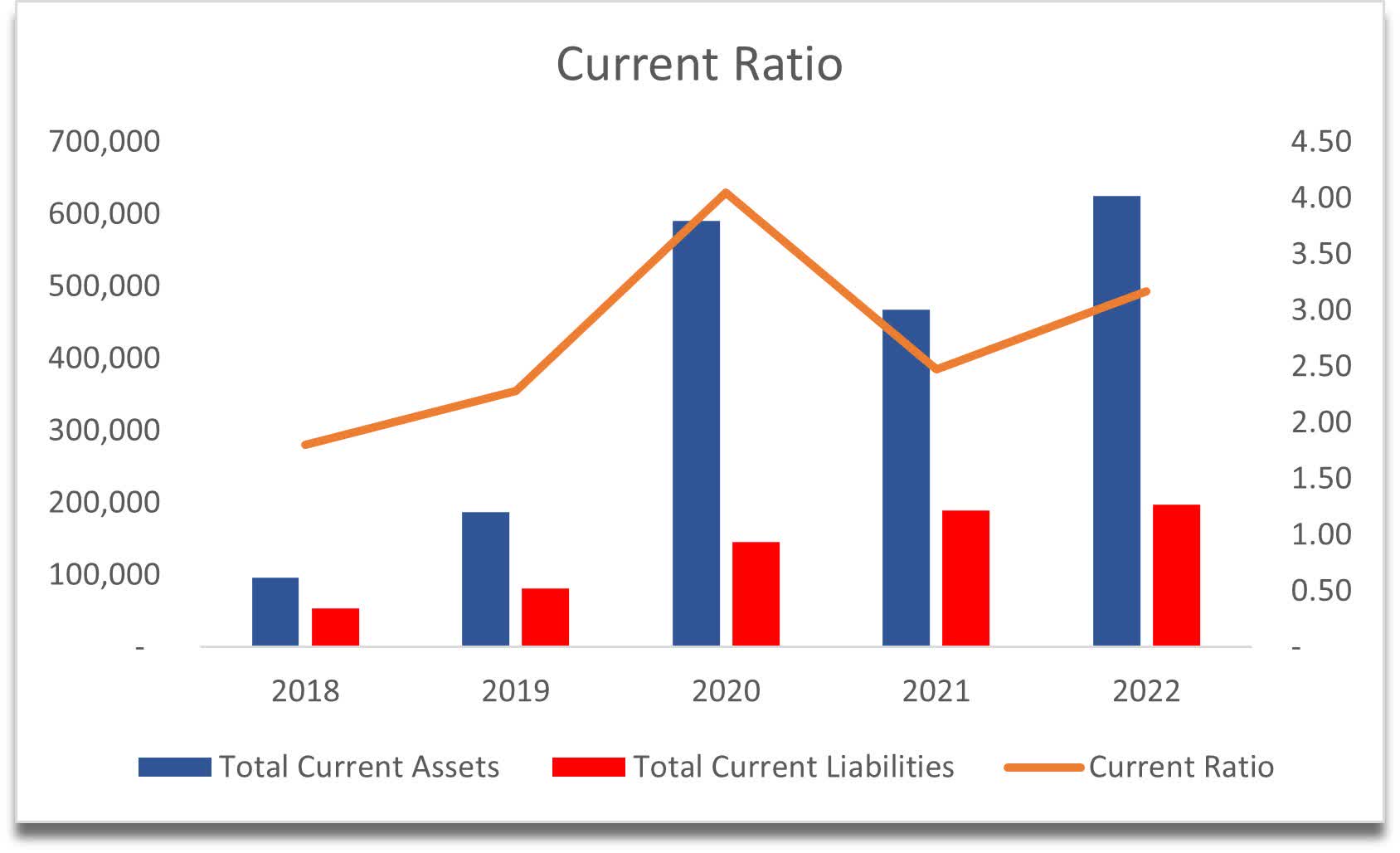

The company's working capital ratio is a little too high in my opinion. I think it is a little too strong because I would like the company to use its assets a little more efficiently, especially the short-term investments that it has, it can be put to use to be more aggressive, to expand its reach further, and to cement its position as the leader in online platform gigs. As of Q1 '23, the ratio stood at around 3, which came down slightly from FY22, but still very far from my range of 1.5-2.0. On the other hand, a high current ratio means that the company will have no issues repaying its short-term obligations.

{kind=link}

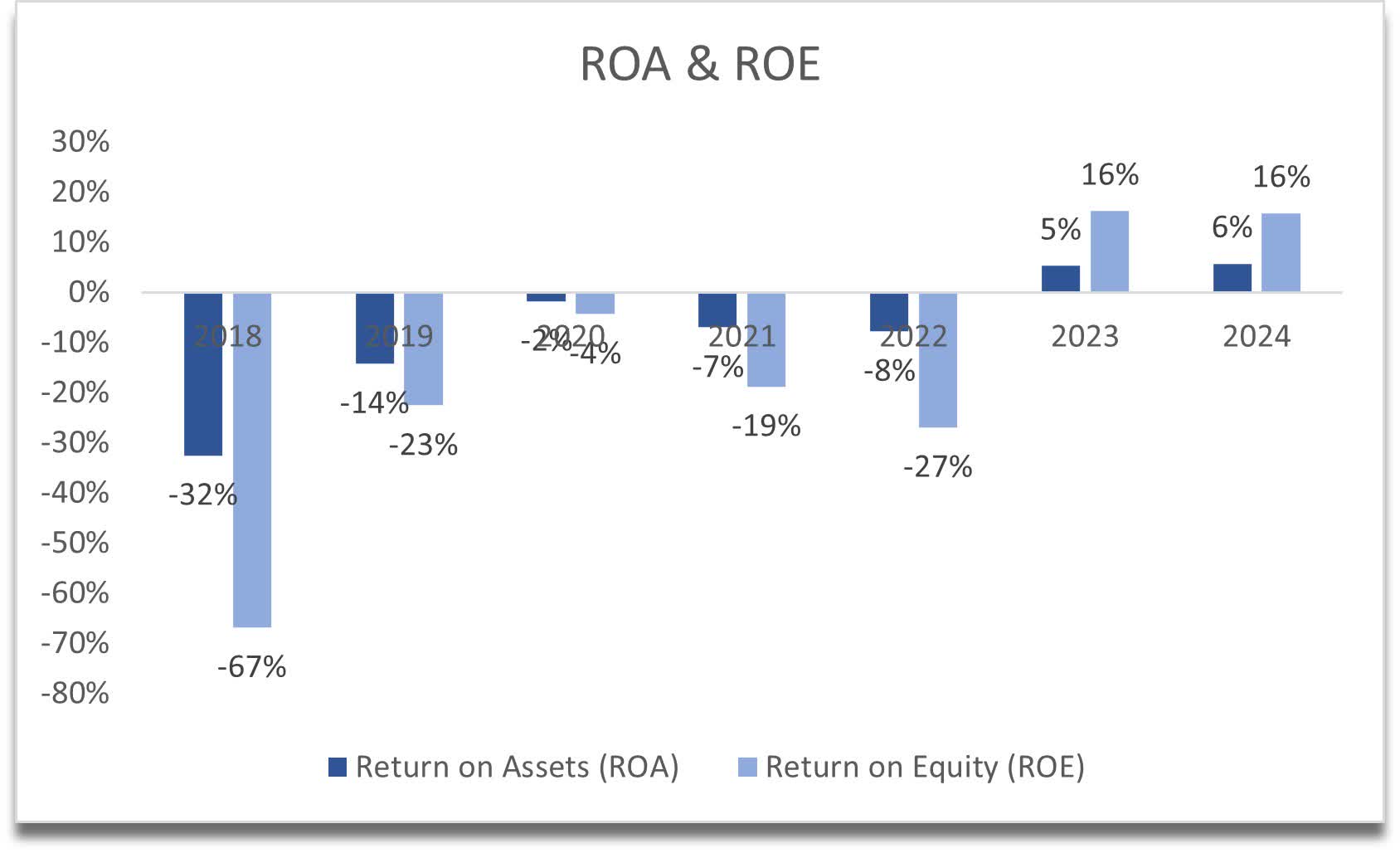

In terms of GAAP efficiency and profitability, the company isn't shining here yet, however, if we take out the stock-based compensation that is included in the operating expenses, the company has reasonable ROA and ROE.

{kind=link}

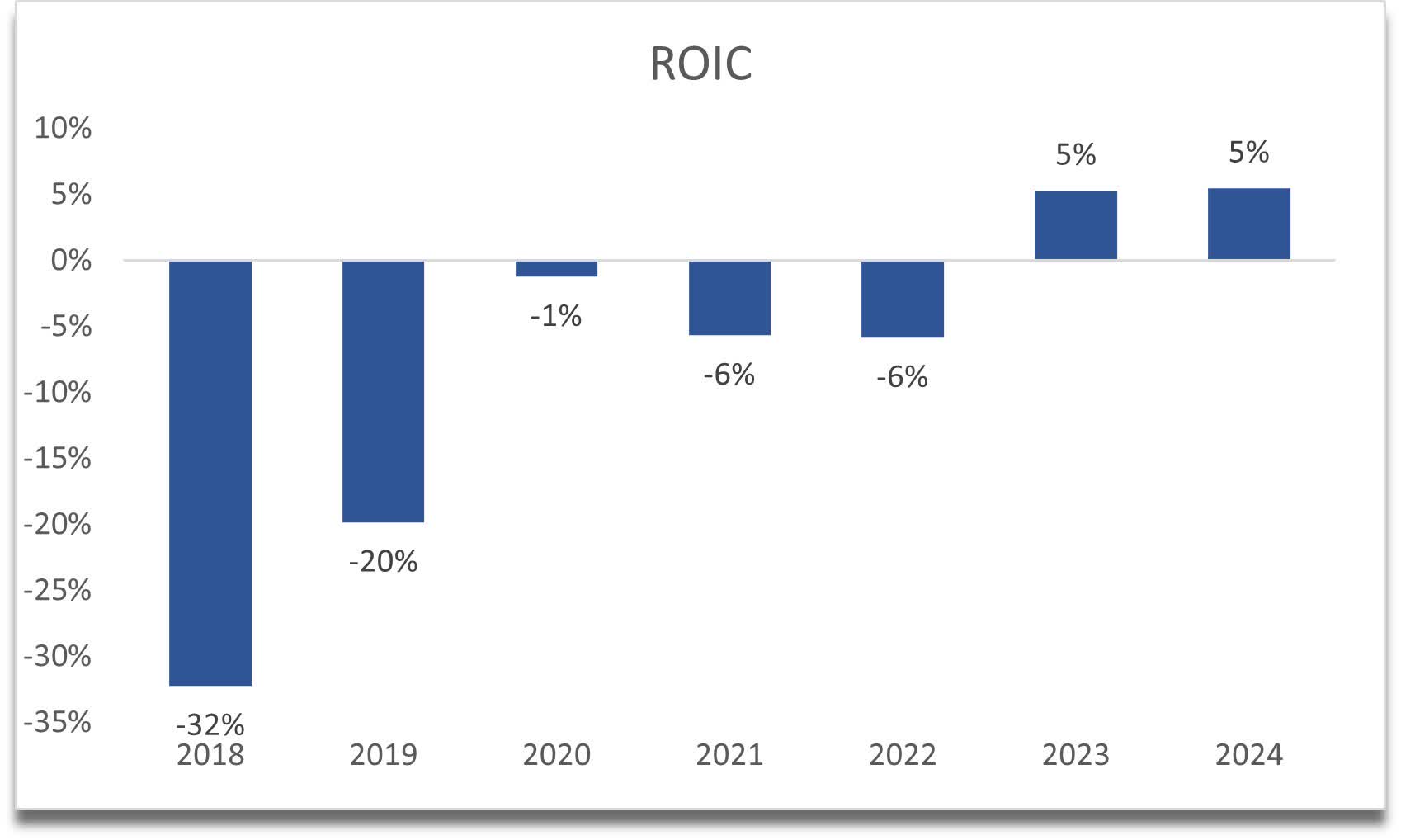

The same story can be said about the return on invested capital. Yes, it may not look very good on a GAAP basis, however, if we go by adjusted numbers, ROIC looks much better. It is still not outstanding, but I believe with time, the company will be able to enjoy a strong competitive advantage and a decent moat if the company maintains its position as the leader in the gig platform industry.

{kind=link}

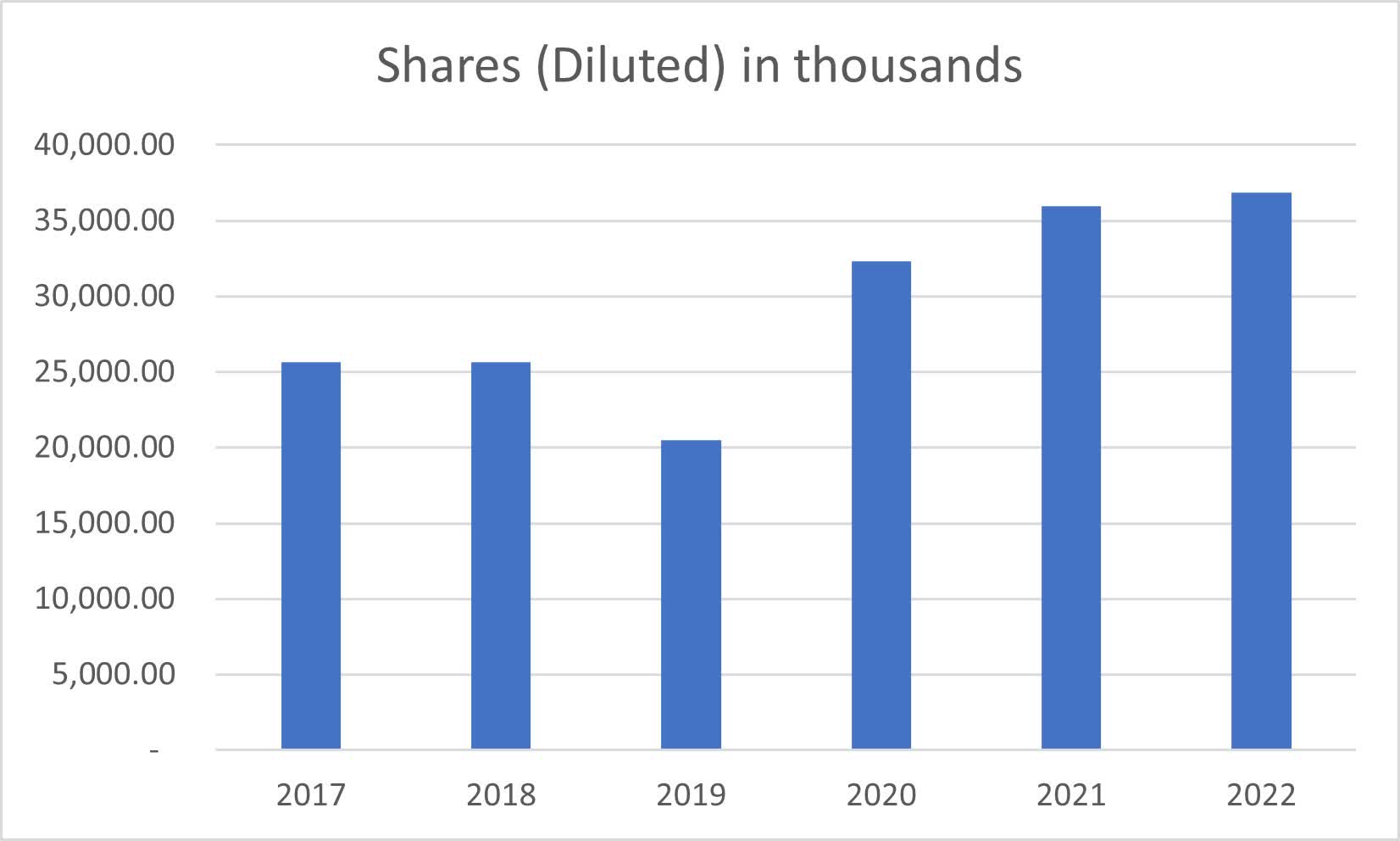

Speaking of stock-based compensation, the company has been diluting its shareholders quite a bit and I could see this persisting in the near future because the company is still aggressively expanding its footprint, which requires a lot of capital and in the short run, another way of raising capital besides getting into massive debt is through issuing more shares. This is one of the bigger red flags I see in the company and if the share price doesn't rise high enough, long-term shareholders will continue to be diluted and lose value.

{kind=link}

Overall, if we were to look at only GAAP figures, we would miss the company's potential once we take out the items like stock-based compensation that affect the company's bottom line massively for now, and I do believe that with an improving outlook in the upcoming years, the company will be able to achieve positive GAAP figures and stop relying on SBC and further diluting shareholders.

Valuation

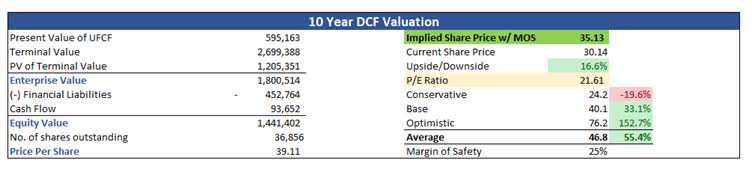

The company achieved an impressive growth rate in revenues over the last 5 years, averaging 47% CAGR. I will approach my valuation with much more conservatism to have a larger margin of safety on my side. For the base case, I went with a 10.40% CAGR over the next decade. For the optimistic case, I went with 14% CAGR, while for the conservative case, I went with 8.4% CAGR over the next 10 years.

The consensus estimates for EPS on Seeking Alpha are showing what I believe to be adjusted EPS figures, so I will adjust my operating margins accordingly and will take out SBC from the equation as it accounts for slightly less than half of sales and marketing expenses. Analysts' estimates show the company's earnings will grow from $1.52 a share in FY23 to $2.8 a share in FY25, while for the same period, my EPS estimates will grow from $1.30 a share to $1.90 a share just to keep things even more conservative.

Seeing that I have beaten down the estimates quite a bit, I will only add a 25% margin of safety to the calculation even if on a GAAP basis the financials don't look the best. With that said, I think the company is a buy at these prices and the intrinsic value calculation says the company is slightly undervalued and presents a decent risk/reward profile currently.

{kind=link}

Risks

The growth of buyers could stagnate or even start to come down if the gig workers on the platform are not providing a valuable service, which means the quality of work would come down and the company's reputation could get hit badly. The first time I heard of Fiverr was when people would perform anything the person asked them to do for 5 dollars, no matter how ridiculous the request was. My first impressions of the company were not great to say the least, however, fast forward a couple of years I needed to use the platform for something, and I realized there are a lot of skilled people for the job I was looking for and it all looked much more professional than what I remembered. In short, the company could still be in a lot of people's minds that it's all for gags and not something a professional would use.

The company could continue to dilute shareholders for much longer than anyone would anticipate and that would not attract many investors, like me, who prefer when companies buy back their shares (at a reasonable price) or stick to the same amount of shares at least going forward because if the share price rises 100% over the next 5 years but shares outstanding doubles, the shareholder essentially gained nothing.

Competitors could offer a better product overall and take market share from Fiverr, which means the company will lose its competitive edge if it doesn't innovate enough and retain the clients and keep growing.

Closing Comments

The company seems to trade at around 21x my FY23 estimates which I remind you are not on a GAAP basis. My view of the company changed quite a bit over the last couple of years and I do believe it will remain one of the largest platforms online in this industry if the management doesn't drop the ball.

I believe right now the share price offers a decent risk/reward outcome and seeing that the company went from $300 a share in '21 to just around $29 currently, the bad is already behind the company and I don't think there is much downside left in my opinion.

I will be looking forward to the company's earnings, which should come out on August 3rd pre-market before pulling the trigger as volatility could be massive.

For further details see:

Fiverr International: Solid Company With Decent Risk/Reward