FVRR - Fiverr: Recent Weakness Provides Better Buying Opportunities

2023-10-07 04:02:05 ET

Summary

- Fiverr International is a growth company with solid long-term potential, despite the recent stock price decline.

- Recent earnings showed modest revenue growth and improved margins, indicating a positive financial outlook.

- Fiverr's introduction of new products and commitment to innovation position it well in the growing freelance platforms market.

Investment thesis

My first bullish thesis about Fiverr International ( FVRR ) did not age well, since the stock price declined by 16% after May 23. Today, I would like to reiterate my bullish opinion because the company still demonstrates improving profitability and expanding its offerings portfolio to absorb the secular growth of the freelance market. Therefore, the reasons why I am bullish are the same as they were in my initial thesis. However, Fiverr is still a growth company in the early stages of its development and is still seeking consistent profitability. Therefore, I do not expect the stock to be a quick winner. Rather, it is a long-term bet with the potential to become a moonshot. The recent dynamic of the company's financial performance and the introduction of new game-changing products improved my confidence in the company's bright long-term prospects. Moreover, the valuation is very attractive, according to my analysis. All in all, I reiterate a "Buy" rating for FVRR.

Recent developments

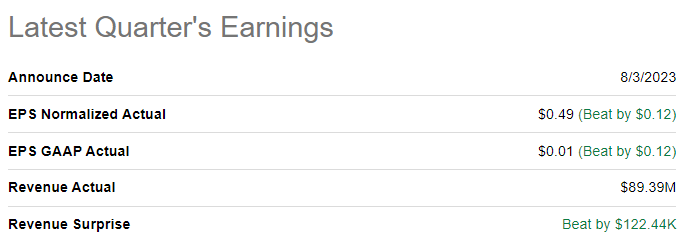

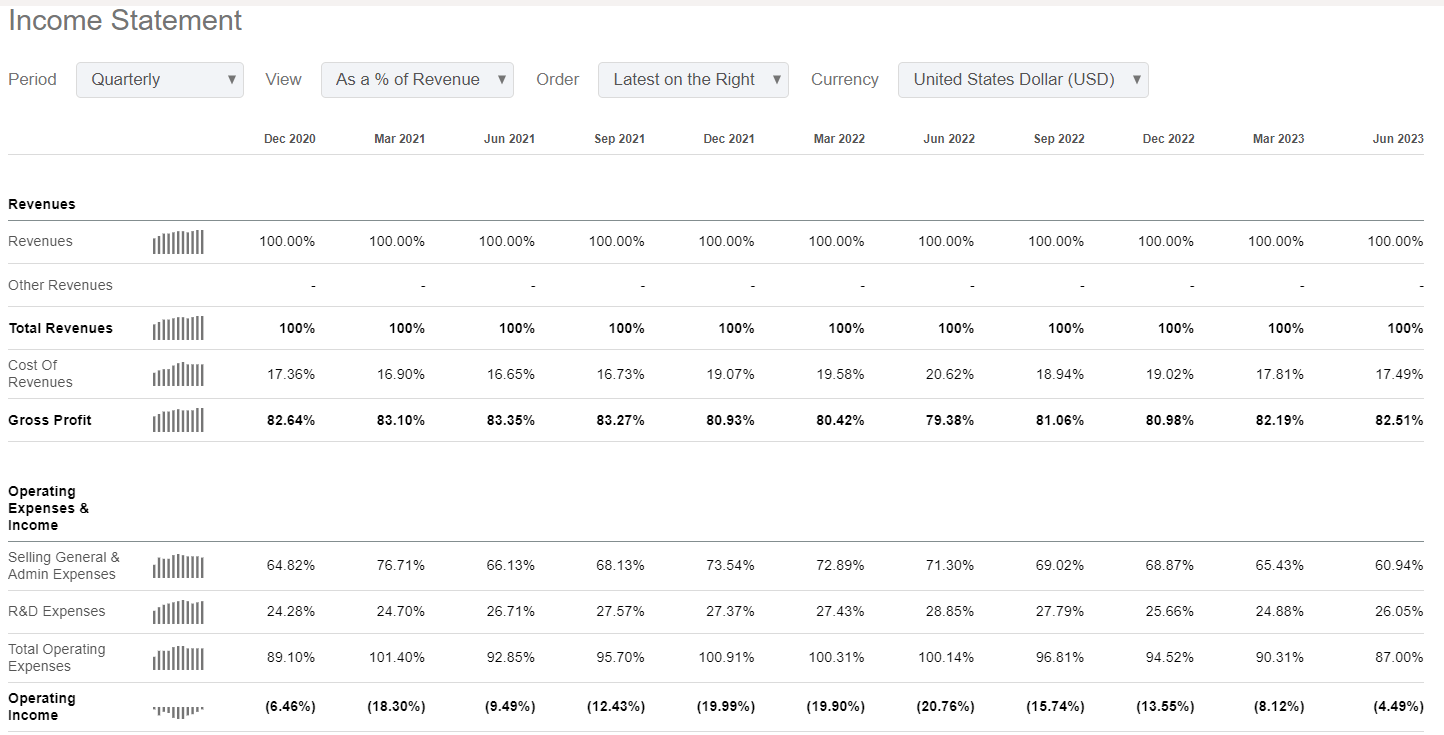

The latest quarterly earnings were released on August 3, when the company topped consensus estimates. Revenue demonstrated a modest YoY growth of 5%, though representing a notable acceleration from the 1.5% YoY growth in Q1. The adjusted EPS expanded substantially from $0.12 to $0.49. The gross margin expanded from 79.4% to 82.5%, and the operating margin is consistently moving closer to breaking even.

{kind=link}

The management's cost-saving measures seem to be efficient, as the adjusted EBITDA of $15.3 million exceeded the management's guidance range. The levered free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] was still negative in the latest quarter, but I like the positive dynamic as the operating margin continues demonstrating solid improvement both YoY and sequentially.

{kind=link}

The company's solid balance sheet and consistently improving operating margin means I have a positive outlook for the company's financial position. I am optimistic about the balance sheet because the company is in a strong net cash position. The leverage ratio might look too aggressive at above a hundred percent, but it is crucial to understand that a significant part of the debt is long-term. Having a solid above $400 million cash balance also gives me confidence that high leverage is not a big risk. Last but not least, the current liquidity metrics are in excellent shape, so I see no near-term liquidity risks for FVRR.

Seeking Alpha

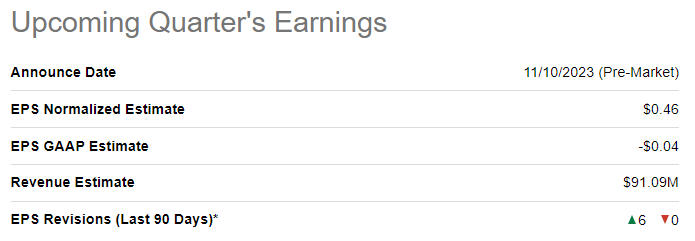

The upcoming quarter's earnings are scheduled for release on November 10. Consensus estimates forecast quarterly revenue at $91 million, indicating acceleration to a 10% YoY growth. The adjusted EPS is expected to more than double YoY. There were six upward EPS revisions in the last 90 days, which is a bullish sign, especially in the current uncertain environment.

{kind=link}

Overall, I am optimistic about the company's prospects. From the near-term perspective, a big positive sign is that during the latest earnings call , the management increased its full-year guidance both on revenue and the EBITDA. I have a high level of confidence that Fiverr will be able to meet its full-year guidance because the company has a stellar earnings history . Since the company went public, it never missed profitability estimates and had only three slight misses on revenue.

From the long-term perspective, I like the management's commitment to drive innovation and expand to new niches. The company introduced several new products recently under the Fiverr Business Solutions suite. New offerings look promising because they are aimed at helping Fiverr to cover larger businesses' needs. New products also leverage AI algorithms to provide a better matching experience, which will likely enhance engagement and retention on the platform. Targeting larger companies looks sound also because it increases the probability of unlocking higher lifetime value buyers. While it is difficult to reliably assess the near-term financial impact of new products, I believe that they will be a great asset for the company to achieve its financial goals. The management aims to accelerate Fiverr's path to the long-term non-GAAP EBITDA margin target of 25%, and I think that new offerings will highly likely boost the probability that this target will be achieved.

Being one of the pioneers as a marketplace for freelancers means the company already has vast experience in this field, which provides a solid competitive advantage compared to potential new entrants. Having solid experience in the industry with consistently improving profitability metrics and heavy investments in product innovation and development makes Fiverr well-positioned to absorb secular tailwinds. The freelance platforms market is expected to compound at above 15% by 2028, which is a solid, favorable shift for Fiverr.

Valuation update

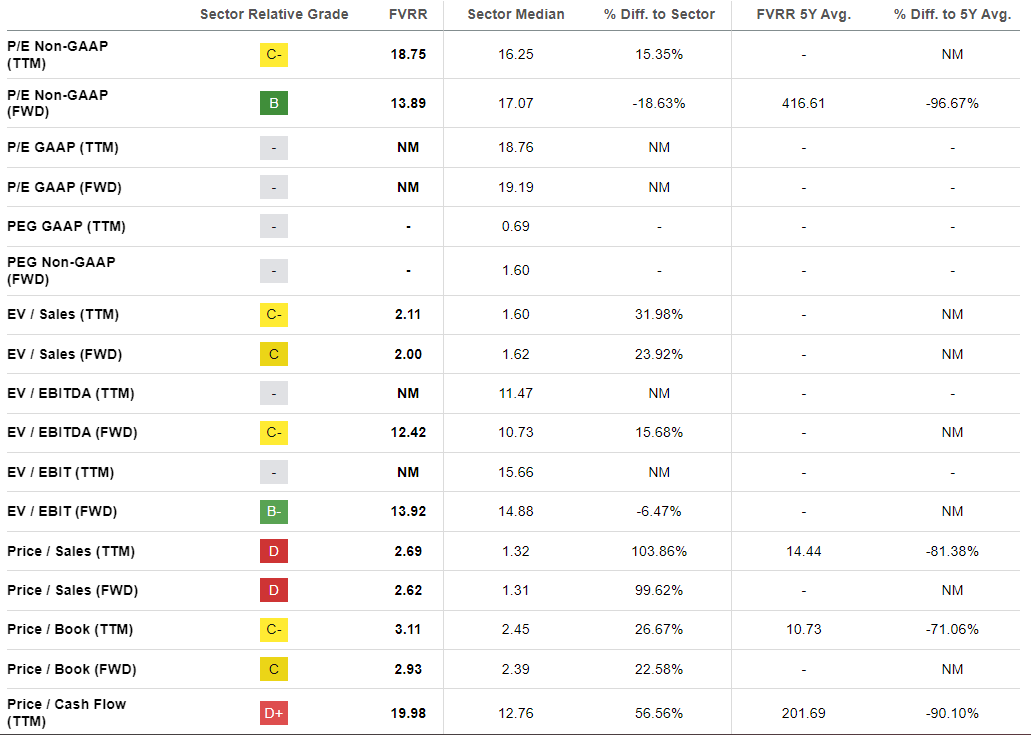

The stock price declined about 16% year-to-date, significantly underperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent "C" valuation grade, suggesting the stock is approximately fairly valued. On the other hand, an important for all growth stocks price-to-sales ratio is about two times higher than the sector median. At the same time, compared to historical averages, we can see that multiples are moderating and moving to more normal levels.

{kind=link}

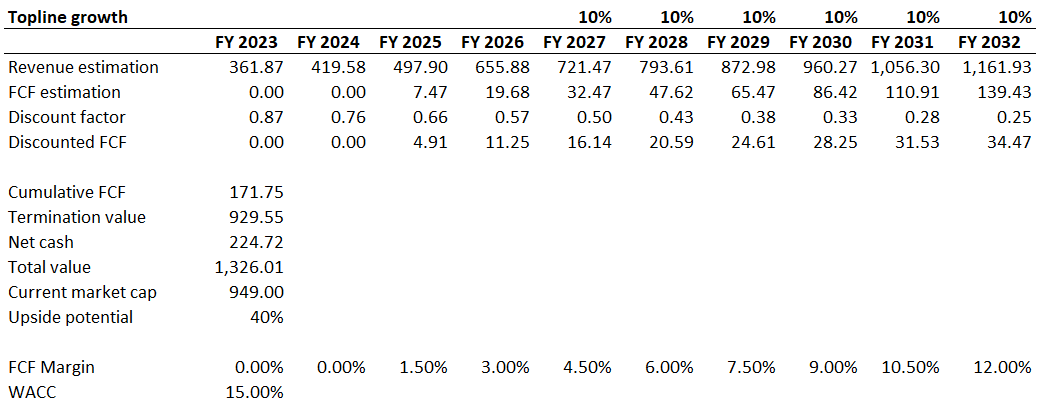

The multiples analysis outcomes are mixed, so I must simulate the discounted cash flow [DCF] model to understand the valuation fairness. The company still needs to be more profitable, and the level of uncertainty regarding the breaking-even timing is high. Therefore, I use an elevated 15% WACC for discounting. I mix revenue consensus estimates together with my professional judgment, resulting in a 13.8% CAGR for the next decade, which I consider fair. I expect the FCF margin to be zero in FY 2023-2024, with a 150 basis points yearly expansion for the years beyond.

{kind=link}

If compared to my first thesis, I have changed the underlying assumptions in line with the evolving environment. To be conservative in the current uncertain environment of interest rates, I have substantially expanded my discount rate to 15%. To balance this massively conservative revision, I have added the net cash position to the business's fair value. I have also implemented a slightly more conservative FCF dynamic. Revenue estimates were slightly upgraded in line with management's guidance and consensus estimates revisions.

According to my DCF simulation, the business's fair value is $1.3 billion, which indicates a 40% upside potential compared to the current market cap. That said, my target price for the stock is $33.

Risks to consider

Fiverr still does not generate a positive FCF ex-SBC margin, and there is a high level of uncertainty regarding the timing of this metric breaking even. As a growth company, Fiverr is also under substantial pressure to consistently meet its ambitious revenue growth plan. If the company fails to drive revenue at the expected trajectory or the business model proves itself unable to generate positive FCF consistently, it will highly likely lead to massive investor disappointment. As a small-cap growth stock seeking profitability, the price of FVRR is highly volatile. The stock now trades 92% below its record levels of February 2021. That said, investors need to be ready to tolerate high volatility and be ready to accept substantial risks of investing in the stock.

Fiverr stores vast volumes of private data of both freelancers and employers. That said, the company faces substantial cybersecurity risks. Any leakage of sensitive information might lead to significant damage to Fiverr's reputation and might also result in costly litigations.

Bottom line

To conclude, FVRR is a "Buy". The recent pullback in the stock price gives long-term investors solid buying opportunities. FVRR is apparently not a stock to deliver quick wins for investors, but the dynamic of its financial performance is stellar. Prospects also look promising given the management's strong commitment to driving innovations but having strong cost control at the same time. The freelance industry is expected to compound at double digits over the long term, and Fiverr is one of the pioneers with massive experience in the niche. Recent new product launches suggest that Fiverr is aiming to expand its target audience among businesses and will highly likely unlock higher lifetime buyers among new larger clients.

For further details see:

Fiverr: Recent Weakness Provides Better Buying Opportunities