FVRR - Fiverr: Risks Are High But Upside Potential Looks Very Attractive

2023-05-23 00:09:09 ET

Summary

- Fiverr experienced a massive selloff last year and is underperforming the market year-to-date.

- I believe that the selloff gives a good buying opportunity, given the company's strong performance under the current harsh environment, which indicates business resilience for me.

- Risks and uncertainties are significant, but my valuation analysis suggests the stock has massive upside potential.

Investment thesis

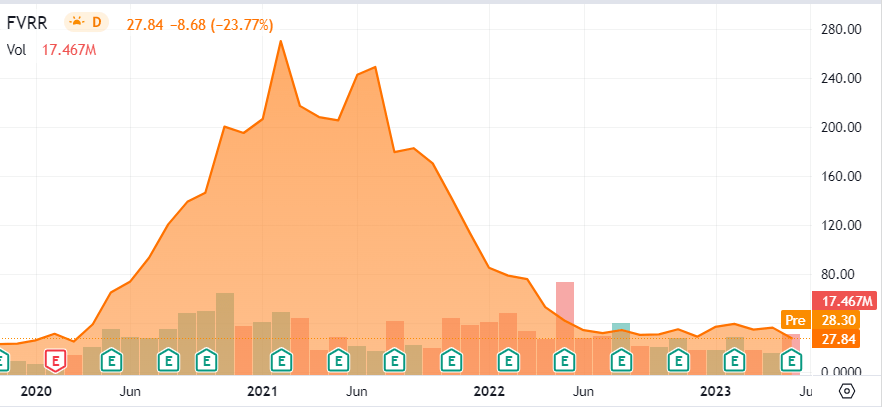

Fiverr International ( FVRR ) is trading more than 90% below its all-time highs, and the stock is underperforming the broad market year-to-date. Despite a massive selloff in recent years, I believe the company is well-positioned to capture growth in the freelance platforms market, which is expected to grow solid double digits over the next several years. Generative AI risks the company's future, but I believe the upside potential outweighs these risks.

{kind=link}

Company information

Fiverr is a global online marketplace connecting freelancers with businesses. The company was founded in 2010 in Israel and has revolutionized how people and businesses collaborate to get work done. FVRR derives revenue from transaction fees and service fees that are based on the total value of transactions ordered through the company's platform. According to the latest annual SEC filing , the company earns about 30% of the gross merchandise volume [GMV].

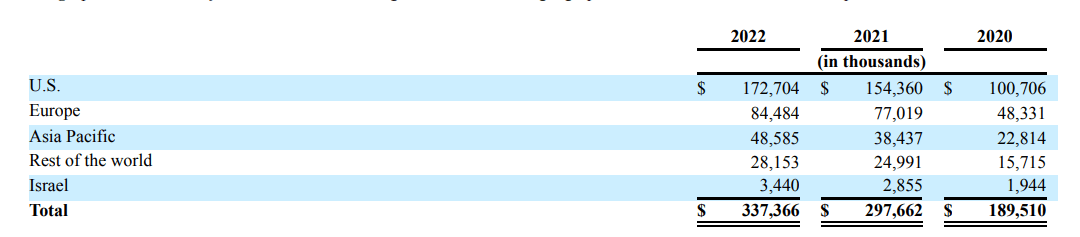

The company's fiscal year ends on December 31 and FVRR operates and reports as a single segment. Though, FVRR disaggregates revenue by geographic areas, where the U.S. represent about half of the company's sales.

{kind=link}

Financials

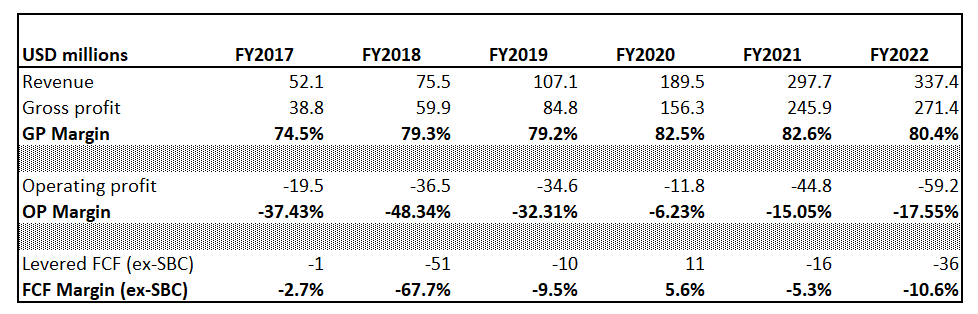

Fiverr went public in June 2019 , so the horizon for long-term financial analysis would be shorter than I usually do. The company delivered an impressive 37% revenue CAGR over the last six fiscal years, with gross and operating margins improving significantly as the company scaled up. The free cash flow [FCF] margin with stock-based compensation [SBC] deducted is still negative, though I cannot call the company a cash burner since Fiverr's net change in cash has been positive last year with insignificant issuance of common stock.

{kind=link}

The company has a healthy balance sheet with a strong liquidity position and almost half a billion cash balance as of the latest reporting date. The leverage ratio might look too high but still, the company is in a net cash position, so I do not see high leverage as a red flag given the context.

Seeking Alpha

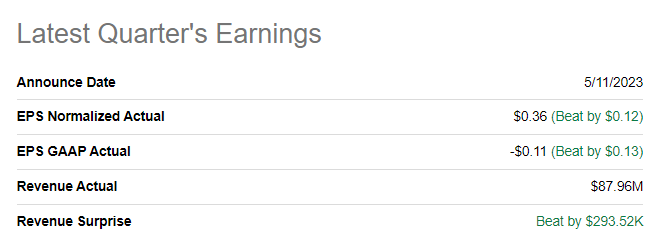

If we narrow it down to the latest earnings, Fiverr delivered higher-than-consensus revenue and EPS for Q1 2023. Revenue increased 1.5% YoY and about 6% sequentially, which I consider vital given the current demanding macro environment when business costs back on spending.

{kind=link}

During the latest quarter, Fiverr still did not-breakeven on an ex-SBC FCF level with SBC about $5 million higher than the levered FCF. I see the closing gap between SBC and levered FCF as a potentially strong catalyst for the stock. The company delivered a 12.8% adjusted EBITDA margin during Q1 2023 and the CFO reiterated the long-term goal to achieve 25% in adjusted EBITDA, though the timing for the goal was not shared during the earnings call .

For the next quarter, the company is expected to deliver about 5% revenue growth YoY and about 1.5% sequentially. For the full FY 2023 management projects revenue is to be within a $350-$365 million range, indicating YoY growth between 4% to 8%. Full FY 2023 adjusted EBITDA is expected at 14.4% at the midpoint. For the long term, consensus estimates project the company's revenue to reach $683 million in FY 2027, indicating about 13.6% revenue CAGR in the next five years. I consider this conservative, given the expected freelance platforms market CAGR projected at slightly above 15% up to 2030.

Overall, I consider Fiverr's financial performance solid, with bright prospects in the market expected to grow double digits. The company is close to the sustainably positive ex-SBC FCF path, which gives more conviction for a bullish thesis.

Valuation

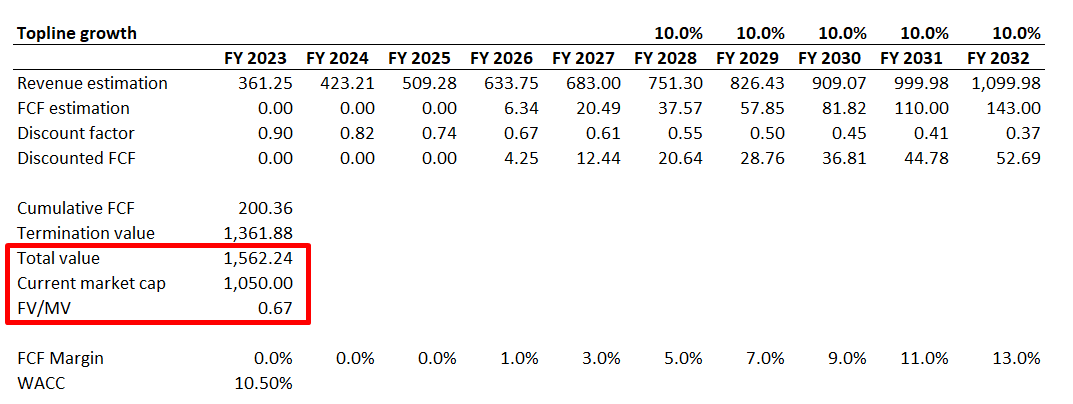

Fiverr is a growth company, and I use discounted cash flow [DCF] approach for valuation. For the discount rate, I take WACC provided by GuruFocus and round it up to 10.5%. For future cash flows, it would be trickier. I have consensus revenue estimates available up to FY2027, and for years beyond I will simulate two scenarios. In terms of FCF margin, the company is not on a sustainable positive path, and to be conservative, I expect the company to deliver a 1% FCF margin which will expand by two percentage points per year. For the first scenario, I expect revenue to grow 10% annually between FY 2028 and F Y2032.

{kind=link}

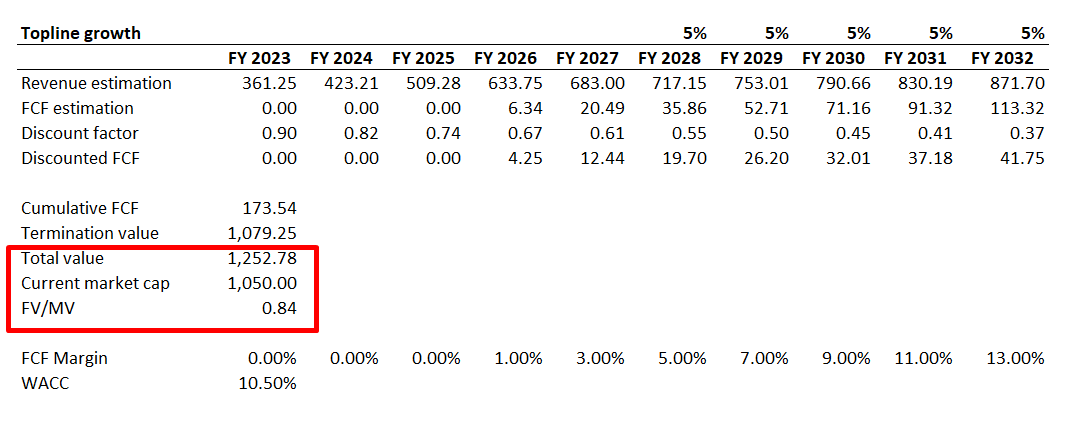

In this case, we can see that fair business value is estimated at almost $1.6 billion, representing an above 50% upside potential which is attractive, in my opinion. Now let me simulate a more pessimistic scenario with revenue growing at 5% per year between FY 2028 and FY 2032, other assumptions untouched.

{kind=link}

As you can see above, even under much more challenging conditions, the stock looks very attractively valued. However, the level of uncertainty regarding underlying assumptions is very high, especially regarding the FCF margin.

To cross-check me, I refer to Morningstar Premium. Their FVRR stock price fair value estimation is at $40.13 per share, which also indicates about 50% upside potential for the stock. The uncertainty level is also very high, according to Morningstar.

Morningstar Premium

Risks to consider

Given the high upside potential under very modest revenue growth assumptions, I think that the risk of overly optimistic expectations is priced in as low.

I consider the biggest threat to FVRR is the rise of generative AI. We are currently at the early stages of this technology development and implementation, but we already see the abilities of generative AI tools. They can generate content and codes that closely resembles human-created work. This can potentially hit the demand for human freelancers, which will hit the GMV on Fiverr's platform. Apart from threats to cut volumes for Fiverr, generative AI will also put downward pressure on the freelancers' services pricing, which will also soften the GMV. I see the potential adverse impact of this risk as massive for Fiverr. On the other hand, the probability is far from a hundred percent given the massive ethical controversy and concerns over the quality of content generated by AI.

The second significant risk I see for the short-term is the potential overall market weakness due to increasingly probable recession together with the looming credit crunch. Under harsh macro conditions, valuations of small-cap growth companies are highly likely to suffer the most. So, if you decide to invest, be ready to hold this stock over multiple years.

Bottom line

To sum up, I believe FVRR is a buy for long-term investors unafraid of potential short-term volatility. The company is demonstrating solid financial performance, improving margins and cash flows. Fiverr is close to breaking even in ex-SBC FCF terms, which is crucial for a young company. The upside potential is massive especially given that I used very conservative assumptions.

For further details see:

Fiverr: Risks Are High But Upside Potential Looks Very Attractive