FVRR - Fiverr: Room For Growth Is Limited Especially In The AI Era (Rating Downgrade)

2023-12-18 10:34:14 ET

Summary

- Fiverr's stock has not performed well this year and is unlikely to see much upside in 2024.

- The company faces challenges from businesses streamlining for efficiency and the potential automation of its core functions.

- Despite its cheap valuation, concerns about AI and limited growth potential make Fiverr a risky long-term investment.

The market is elated again over the prospect of lower interest rates in 2024, but that doesn't mean that investors should be any less choosy when it comes to stock-picking. I continue to hold firm to the belief that we can achieve outsized gains against market indices next year if we pick the right small and mid-cap stocks to invest in.

And part of choosing the right stocks is also identifying the wrong stocks to bet on. In the case of Fiverr International Ltd. ( FVRR ), the online gig/freelance marketplace that is primarily used by small and mid-sized businesses, this company has been one of the few holdouts to this year's rally, down slightly while the S&P 500 is clinging to ~20% gains. Despite missing out on this year's advances, I don't think there's much room for Fiverr to gain much upside in 2024.

I last wrote a bullish article on Fiverr a year ago, when the stock was trading closer to $32 per share. Since then, the company has entered a choppy buying environment that has, at least for the first two quarters of this year, pushed y/y revenue growth into single-digit territory. The company has made sizable improvements in profitability as it rationalized its own costs - but not to a degree sufficient enough to justify an already-low valuation.

The core problem that Fiverr faces, in my opinion, is businesses' streamlining for efficiency. Efficiency has been the hallmark theme for most companies this year (some, like Meta Platforms, Inc.'s ( META ) Mark Zuckerberg, publicly declared the word "efficiency" as the company's top goal for the year). And when it comes to reviewing spend and optimizing work streams, freelance workers are often among the first to go. The same is true of both large and small businesses that are looking to preserve their wallets (the latter being the more common customer for Fiverr).

The second major issue that Fiverr contends with, and the main reason for its stock price decline this year, is AI. Of course, the company argues (and many others do) that AI and human labor need to work hand in hand, and that artificial intelligence will never be able to replace labor entirely. But many of the core functions that Fiverr offers - graphic design services, website setup, copy editing - are all rather mechanical tasks that have a clear path to automation. And amid this year's push for efficiency, automating manual labor - and doing it cheaply - is also chief in executives' minds.

Now, I don't think either of these things makes me fully bearish on Fiverr just yet, and the main reason for that is the price. Fiverr is cheap - especially after this year's decline, and in light of the company's improving adjusted EBITDA margins. At current share prices near $28, Fiverr trades at a market cap of just $1.08 billion. After we net off the $593.3 million of cash and $454.7 million of debt on Fiverr's most recent balance sheet, its resulting enterprise value is even lower at $942 million.

Meanwhile, for FY24, Wall Street analysts are expecting Fiverr to generate $410.2 million in revenue, representing 13% y/y growth (data from Yahoo Finance ). If we assume Fiverr holds its current-year adjusted EBITDA margin of ~16% on next year's revenue, adjusted EBITDA in FY24 would be ~$66 million. This puts Fiverr's valuation multiples at:

- 2.3x EV/FY24 revenue.

- 14.3x EV/FY24 adjusted EBITDA.

Its EBITDA multiple is fair, but its revenue multiple is quite cheap. It's cheap, however, for longer-term concerns around AI and its limited growth potential. I don't see much of a future in which we're still using a site like Fiverr to serve short-term freelance needs.

All in all, I'm downgrading my viewpoint on Fiverr to neutral. I'd prefer to move to the sidelines here or take advantage of volatility in this stock for some shorter-term trades, but I'm no longer comfortable holding this stock for the long term.

Q3 download

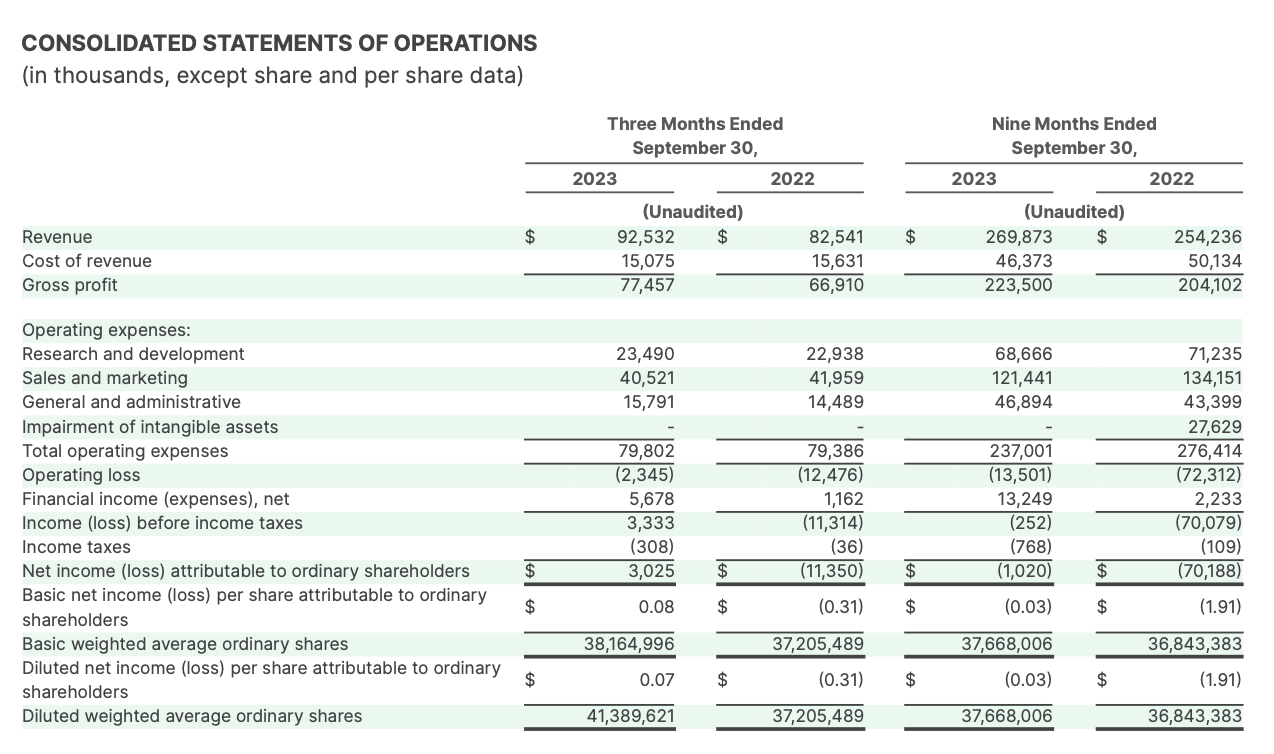

Let's now cover Fiverr's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

Fiverr Q3 results (Fiverr Q3 shareholder letter)

{kind=link}

Fiverr's revenue grew 12% y/y to $92.5 million, ahead of Wall Street's expectations of $91.1 million (+10% y/y) by a two-point margin. The positive spin on this is that Fiverr's revenue has accelerated from single-digit growth in the first two quarters of FY23.

Note as well that part of the return to Fiverr's double-digit growth rates is due to easier comps, as the company's growth started to slow in the back half of 2022. And even 12% y/y growth in the current quarter is a far cry from ~30% y/y growth during the heyday of the pandemic.

Growth has benefited in large part from an increase in the company's take rates, up to 31.3% of total spend - from 30.0% in the year-ago Q3. The company notes that the increase in take rates is due to better attach rates on value-added services, such as Seller Plus, a monthly subscription program for sellers (freelancers) on the Fiverr marketplace that gives an expanded set of features such as more analytics tools and more promotional customer-facing options, such as coupons.

At the same time, however, we have to be wary of the fact that spend per buyer is slowing to just 4% y/y growth to $271 - indicating that the vast majority of Fiverr buyers are still individuals or smaller businesses - and once armed with more advanced and easy-to-use AI tools, a large swath of this market could vanish.

To Fiverr's credit, integration with AI and co-existing with AI tools is one of the company's top priorities for 2024. Speaking to these priorities on the Q&A portion of the Q3 earnings call , CEO Micha Kaufman noted as follows:

Yeah. So, on priorities for 2024, I would say that a lot of what we've been doing throughout the years has been paying off well. And there are a few specific things when it comes to next year. So, continuing on my previous comment, given the macro environment, going upmarket is a strategic move and target for us. And at least until macro changes, this is the center of focus.

The other one that I can call out is AI integration, both internally as a team and how it makes us move faster and more efficient, but also in our products to make the lives of our customers better and get what they're trying to do faster.

On the same note, pretty much, catalog expansion is extremely important as we're seeing so many different -- so many new areas of professionalism appear as the landscape changes. And so, continuing to expand the catalog and ensure that we add the necessary categories and skills to the catalog is important.

International expansion is another one. I think 2023 has been very successful in that front and we've been -- I think the playbook or the playbooks that we've been developing have been paying off and we're seeing regions where we're doubling down and growing much faster than the average growth of the marketplace. Team excellence is an ongoing investment."

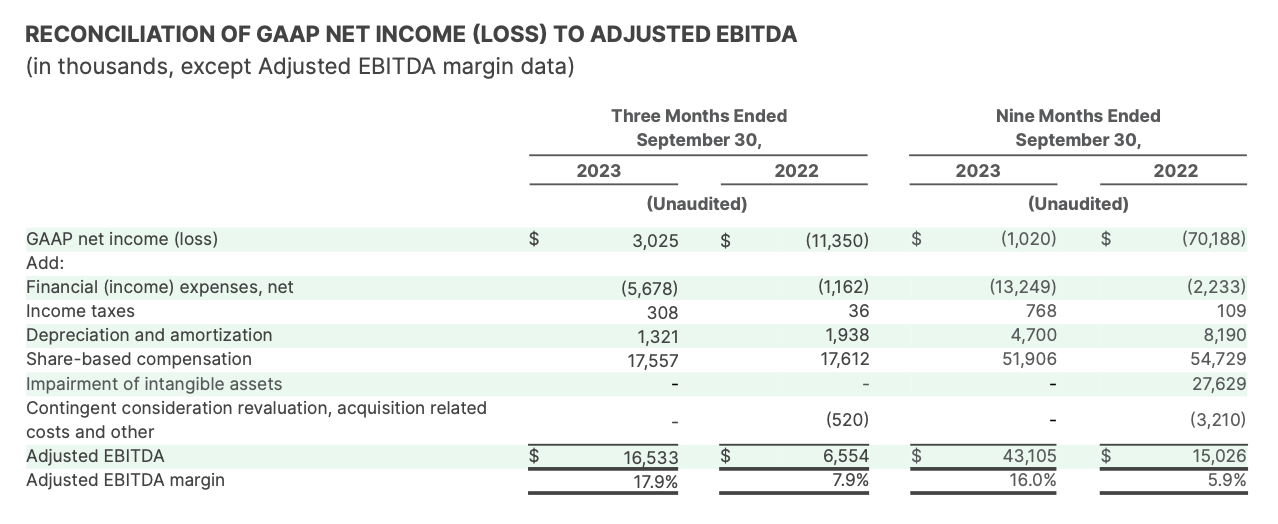

On profitability: owing to advanced take rates that didn't require much in incremental opex investment, Fiverr's adjusted EBITDA more than doubled y/y to $16.5 million, representing a 17.9% adjusted EBITDA margin: a 10-point increase from the year-ago Q3.

Fiverr adjusted EBITDA (Fiverr Q3 shareholder letter)

{kind=link}

Still, though, I expect the company's adjusted EBITDA expansion to slow into next year, and a mid-teens adjusted EBITDA multiple isn't exciting enough to make me bullish on this name.

Key takeaways

Needless to say, there are a number of puts and takes on Fiverr: but when I look at the long-term and the overall viability of a freelance marketplace in a world that is rapidly adapting to automation and AI, I don't like the stock as a long-term play. In the short term, I think 2023 has already been hard enough on Fiverr and there won't be much downside in 2024, but neither do I see the stock rapidly rebounding. I'd prefer to move to the sidelines and invest elsewhere.

For further details see:

Fiverr: Room For Growth Is Limited, Especially In The AI Era (Rating Downgrade)