FVRR - Fiverr Stock: It's Time To Double Down

2023-08-03 11:07:50 ET

Summary

- Fiverr’s second-quarter financial performance sheds light on the success of its recent initiatives to drive profits higher while creating a platform to enjoy steady revenue growth in the foreseeable future.

- The notable improvement in gross margin is a testament to how the company is scaling profitably.

- Digging deeper into the earnings report, we find that Fiverr continued to invest in new products and features to lure high-quality customers and freelancers.

- The company is not aggressively cutting down its marketing budget, which is another promising sign.

- Monthly website visits for Fiverr have declined in the last three months, but more granular data indicates the presence of competitive advantages.

Fiverr International Ltd. ( FVRR ) has been on my radar for quite some time, and I have successfully traded in and out of FVRR stock a couple of times since its IPO in 2019. I am long FVRR today - I am sitting on losses - and after digesting the company's second-quarter earnings, revisiting the outlook for the gig economy, and Fiverr's market position, I believe it's an opportune time to double down on Fiverr stock.

Transitioning From Growth To Profits

Fiverr, along with Upwork Inc. ( UPWK ), dominates the freelance platform market. Given that freelancing has been on the rise for many years and exploded during the pandemic, it is not a surprise that Fiverr grew exponentially in the last few years. From just $52 million in 2017, Fiverr's revenue surged to more than $337 million last year, highlighting the company's stellar growth. Similar to many growth companies, Fiverr, during the pandemic days, focused on expanding its scale aggressively, which helped the company grow in leaps and bounds. With many professionals going back to office and pandemic-related restrictions easing, Fiverr's growth decelerated in recent quarters. The company has made this an opportunity to focus on profitability, which, in my opinion, is a welcome sign for long-term-oriented investors.

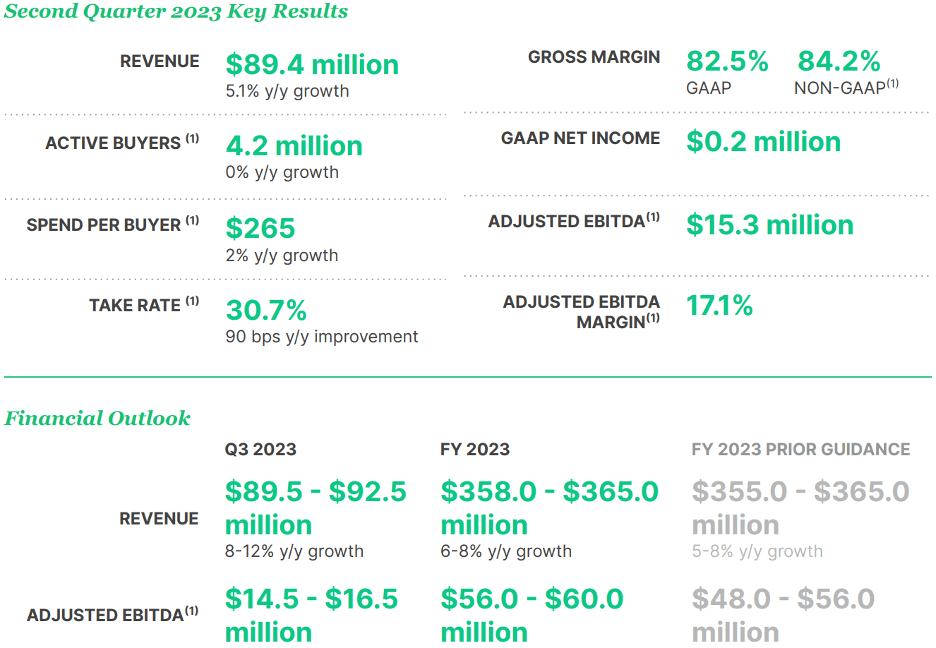

Fiverr's second-quarter financial performance sheds light on the success of its recent initiatives to drive profits higher while creating a platform to enjoy steady revenue growth in the foreseeable future amid macroeconomic challenges. For the second quarter, the company reported revenue of $89.4 million, a year-over-year increase of 5.1%. The gross profit increased by 9.3% - eclipsing the growth of revenue - to $73.8 million, aided by a 310-basis point increase in the gross margin to 82.5%. The notable improvement in gross margin is a testament to how the company is scaling profitably. GAAP operating expenses declined sharply from $110 million in Q2 2022 to $77.8 million in Q2 2023, paving the way for an expansion in the operating margin. This, combined with the improved gross margin and steady revenue growth, suggests Fiverr is making progress toward profitability. In fact, the company reported a profit of $227,000 for the second quarter compared to a loss of $41 million in the corresponding quarter last year. Based on the momentum of recent strategic decisions, Fiverr boosted its guidance for adjusted EBITDA for the next quarter, sending a clear signal that the company is executing well on its profitability initiatives.

Exhibit 1: Fiverr's Q2 performance highlights and outlook for 2023

{kind=link}

Digging deeper into the earnings report, we find that Fiverr continued to invest in new products and features to lure high-quality customers and freelancers. One of the pitfalls of investing in a growth company with a focus on profits is that the management might end up focusing too much on the short-run profitability of a company, thereby missing out on opportunities to grow. Fiverr, commendably, is avoiding this by investing to grow. In the second quarter, R&D expenses came to $16.6 million on a non-GAAP basis, or 18.6% of revenue compared to 21% of revenue in Q2 2022. Maintaining R&D investments at this pace allows the company to expand profitably. Supported by these investments, Fiverr recently launched several new products to attract business clients - a customer cohort that will drive the growth of the platform in the coming years through higher spending. Some of these new products include:

- Fiverr Enterprise - a SaaS platform designed to help companies manage their relationships with freelance and contract workers efficiently. The platform includes services such as sourcing freelancers, onboarding them, and ensuring regulatory compliance.

- Fiverr Certified - a partnership program launched to build deep relationships with SMB service providers on the platform. Fiverr will run the marketplaces of Certified businesses, thereby saving time for these service providers to focus more on their work and less on marketing.

- Fiverr Neo - a freelancer matching tool that matches freelancers on the Fiverr platform with buyers who are looking for a specific service. This tool is expected to improve the experience of buyers who are looking for talent.

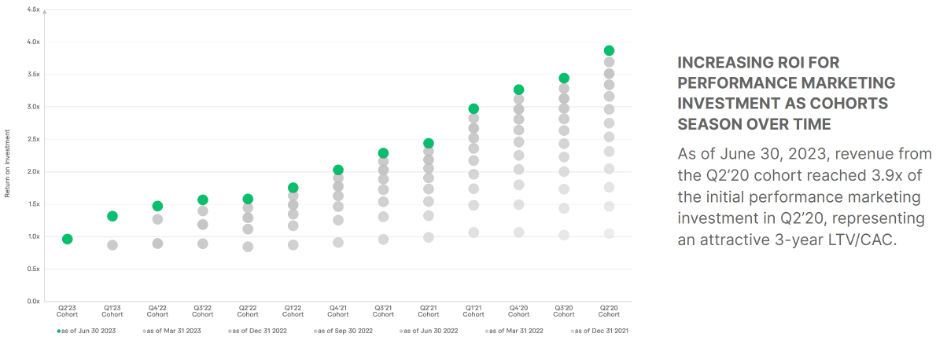

The company is not aggressively cutting down its marketing budget as well, which is another promising sign. It is easy to manipulate the short-term earnings of a company by spending less on marketing, but investors should be cautious about this approach as it could potentially open the door for competitors to eat into market share. Rather than slashing marketing costs aggressively, Fiverr has focused on improving its marketing ROI. The company's performance marketing investments - direct variable costs related to buyer acquisition - are delivering better results with time, which is an encouraging sign.

Exhibit 2: ROI of performance marketing investments by customer cohort

{kind=link}

Overall, I am impressed with the progress Fiverr has made in the second quarter to inch toward profitability, and I believe a platform has been set for the company to grow earnings in double-digits over the next 5 years aided by steady revenue growth.

The Macroeconomic Outlook

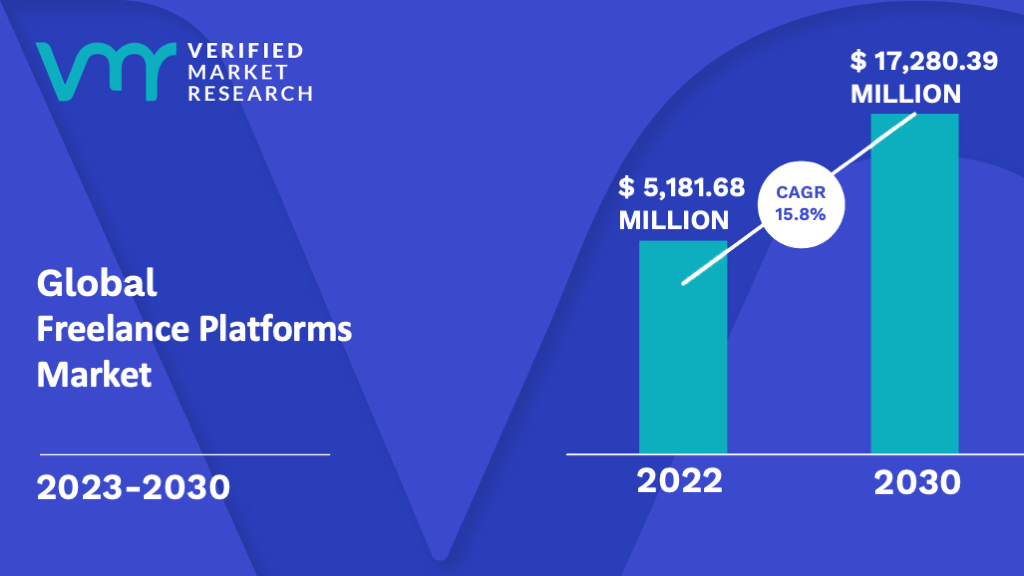

A young, small company such as Fiverr will be influenced by macroeconomic conditions. This is why it is important to assess the industry outlook for Fiverr on a regular basis to identify potential inflection points. The gig economy got a boost with mobility restrictions in 2020 but the reopening of the economy has dealt a blow to the number of skilled professionals who are joining the gig economy. This, however, does not mark the end of the growth of the gig economy. Although there are certain limitations to the growth of the gig economy, such as the lack of job security, variability in income, and lack of access to employer-provided benefits including healthcare, many skilled professionals are joining the gig economy to improve their income, to follow their entrepreneurial dreams, and to enjoy the high degree of flexibility associated with freelancing. Most professionals start out on a part-time basis and transition to full-time gig work after reaching a certain level of income. Freelance platforms such as Fiverr play a key role in the growth of the gig economy. According to Verified Market Research, the global freelance platforms market will grow at a CAGR of 15.8% through 2030, lifting the industry to a multi-billion-dollar valuation.

Exhibit 3: Global freelance platforms market

{kind=link}

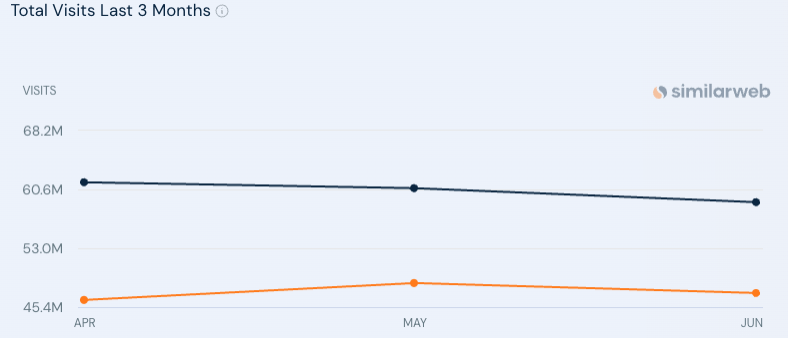

In the short term, I believe freelancing platforms will come under some pressure with the ongoing fallout from pandemic highs. Pandemic-related mobility restrictions and layoffs pulled forward years of growth, and it is reasonable to expect the market to normalize. Confirming some of the challenges faced by freelancing platforms, monthly website visits for Fiverr have declined in the last three months. What is encouraging, however, is that Fiverr has attracted substantially more visitors than Upwork, its arch-rival.

Exhibit 4: Website visits for Fiverr (black line) and Upwork (orange line)

{kind=link}

Upwork is a much larger company than Fiverr, bringing in almost double the annual revenues of Fiverr. Fiverr's ability to attract more users to its platform, in my opinion, stems from the recent investments of the company to attract more enterprise customers. Also, Fiverr's value proposition is different from Upwork as Fiverr has built a freelancer-friendly platform where freelancers do not have to bid for projects to land gigs. Upwork, on the other hand, is customer-friendly where freelancers have to bid for projects. Fiverr's strategy helps the company attract high-quality freelancers, which results in attracting businesses in return.

Takeaway

Fiverr reported impressive earnings for the second quarter with the company showcasing the progress of recently implemented strategies to drive profitability higher. As Fiverr transitions into a profitable freelancing marketplace, I believe the company will create immense shareholder wealth in the long term. There are early signs of competitive advantages as well, which bode well for long-term investors. I believe now is a good time to double down on Fiverr before the trade gets crowded once macroeconomic conditions improve.

For further details see:

Fiverr Stock: It's Time To Double Down