FVRR - Fiverr: The Crowded Freelance Marketplace

2023-06-13 12:19:59 ET

Summary

- Fiverr International Ltd.'s valuation has been negatively affected by concerns about AI's impact and stagnant growth in active buyers.

- The platform faces competition from other freelance platforms, potentially leading talented freelancers to establish their own online presence.

- Fiverr's revenue growth rates have slowed, raising questions about its valuation and growth potential.

- The increasing take rate may diminish Fiverr's competitive advantage, as freelancers can find alternative platforms with lower fees.

Investment Thesis

Fiverr International Ltd.'s (FVRR) valuation has compressed as investors have come to believe that artificial intelligence, or AI, will be a significant headwind for the company. Essentially, the uncertainty of AI on Fiverr's prospects is weighing on the stock.

In addition, investors' concerns may have some basis. And the reason is that the number of active buyers is not rising. Regardless, no matter how we slice and dice Fiverr's analysis, we get the same conclusion. Yes, Fiverr is a lot cheaper than it was several years back, but its platform is also far from thriving.

It's a case that Fiverr today is cheap. But it's cheap for good reasons.

Why Fiverr? Why Now?

Fiverr is an online marketplace that connects freelancers with clients seeking various digital services. Fiverr offers a range of services, including graphic design, digital marketing, and programming.

Fiverr provides a convenient platform for individuals and businesses to access professional services, making it easy to pay freelancers for their services.

In my previous analysis, as we headed into Q1 earnings , I said ,

[...] the key, I believe, is to be found in Fiverr's active buyers figures.

For now, I remain bullish on Fiverr if Fiverr's Q1 2023 can show that its active buyers have not only stabilized but are in actuality still steadily increasing.

So how did Fiverr's Q1 results actually perform?

{kind=link}

Fiverr saw flat growth y/y. Next, in my prior analysis, I went on to state,

Put simply, if Fiverr were to mostly deliver strong growth rates on the back of increasing its pricing, this would cut into its value proposition, sometimes called a moat. And that's the bear case.

Again, how did Fiverr actually perform on this front?

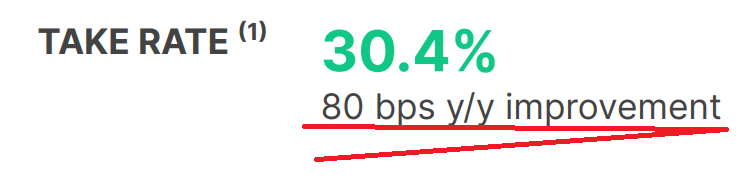

{kind=link}

Fiverr raised its take rate further y/y. In actuality, I believe that by consistently raising its take rate, Fiverr is actually cutting into its own moat. Why?

Because freelancers can just as effectively sell their services on competing platforms, that undercut Fiverr.

Here I'm not only referring to Upwork (UPWK), although that is indeed a large freelance platform. That being said, the argument could be made that Upwork's freelancers are often targeting enterprises rather than small startups.

But there's also Freelance.com and Guru, to mention just a few alternative platforms to Fiverr.

Furthermore, another bearish argument is that the best freelancers, that become big and successful enough, ultimately gather enough of a regular customer base and customer base via social media that they end up opening up their own online presence, outside of Fiverr.

Revenue Growth Rates Mature

{kind=link}

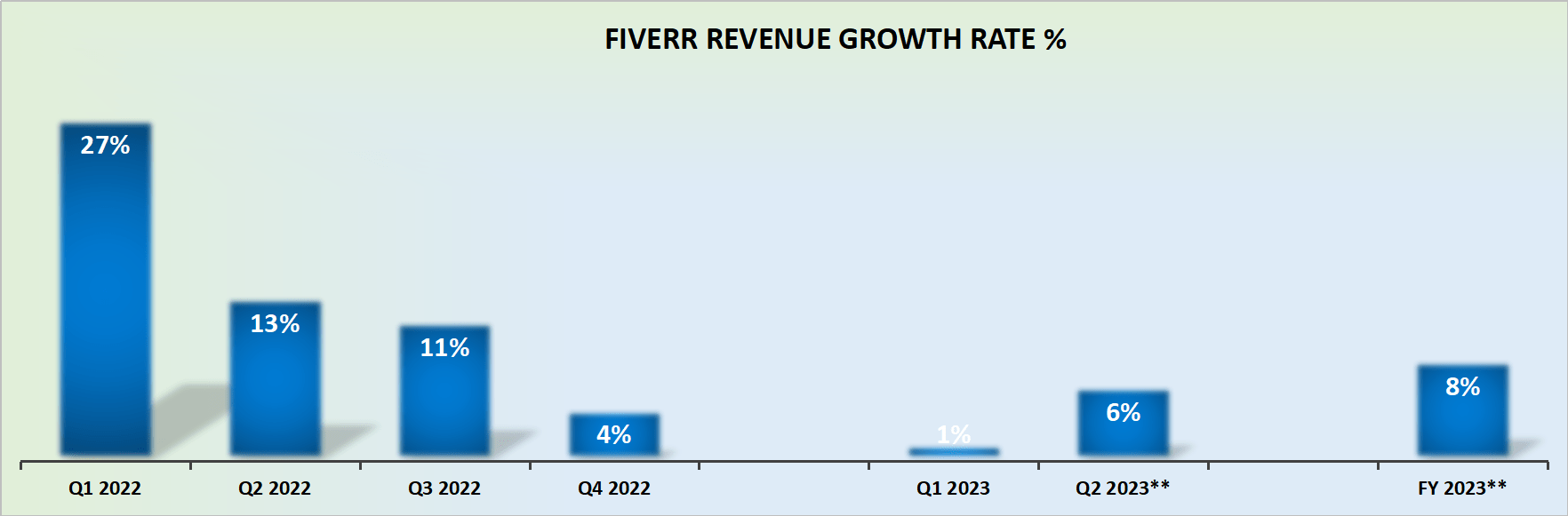

On the one hand, Q1 2023 had a very tough comparable with the prior year. On the other hand, as we look out to Q2 2023 and beyond, the comparables become substantially easier.

And yet, its revenue growth rates point to around 8% CAGR for 2023. Even if we leave Fiverr with some room ''to positively'' impress investors, and Fiverr ends up growing by 10% CAGR this year, we can concretely declare that Fiverr is no longer a rapidly growing business.

Thinking Through Fiverr's Valuation

Fiverr's bull case can be summarized succinctly in the graphic that follows.

At one point, Fiverr was being priced at more than 10x forward sales. Today, it's priced at 3x this year's revenues. Said in other words, a large part of the bull case points to the fact that at one point in the past, Fiverr was more expensive, therefore, today it must be undervalued.

The contra argument, however, contends that in the past, Fiverr's active buyers were swarming towards its platform and Fiverr's revenues were growing at a very fast rate. The same can not be said today.

According to my estimates, Fiverr is priced at very approximately 15x forward free cash flows. That's not so cheap for a business that is barely growing. And the growth that it does deliver, it does so on the back of taking an ever larger cut from its ''partners'' on its take rate.

The Bottom Line

Here, I describe reasons why investors may be hesitant to invest in the company.

Concerns revolve around the potential impact of AI on Fiverr's prospects and the lack of significant growth in active buyers.

Furthermore, I question Fiverr's value proposition and suggest that the platform faces competition from other freelance platforms, potentially leading successful freelancers to establish their own online presence.

Fiverr International Ltd. revenue growth rates have slowed, and its valuation is debated, with the bull case emphasizing the current lower valuation compared to the recent past while the bear case points out the slower growth and increasing take rate cutting into Fiverr's moat.

For further details see:

Fiverr: The Crowded Freelance Marketplace