LOW - Floor & Decor: Its Impressive Growth Story Is On Pause

2023-10-16 07:32:35 ET

Summary

- Floor & Decor has shown strong financial growth, with a CAGR of +27% in revenue and +34% in EBITDA.

- FND is a highly attractive growth business with a compelling omnichannel approach and a PRO solution for larger clients.

- It operates a low-cost business model with an efficient supply chain and aggressive store growth. We see its current trajectory as sustainable.

- The current macroeconomic environment, including softening house prices and declining consumer affordability, may lead to negative comparable growth and share price stagnation.

- The Company's valuation is at the top-end of reasonable, which given the macroeconomic environment, makes the stock a hold in our view.

Investment thesis

Our current investment thesis is:

- FND is a highly attractive growth business. The company is expanding its national presence aggressively, underpinned by an underrated business model that focuses on supply chain management and "doing the small things well". It has a compelling omnichannel approach and a PRO solution for larger clients.

- The current macroeconomic environment appears concerning, however. House prices are softening, consumer affordability is declining, and new home purchases/starts are slowing. These factors will compound, leading to negative comparable growth. We see this contributing to share price stagnation given the elevated trading multiples.

Company description

Floor & Decor Holdings, Inc. ( FND ) is a leading specialty retailer of hard surface flooring and related accessories. With a vast selection of tiles, wood, laminate, and natural stone products, the company operates a network of stores across the United States, catering to both DIY enthusiasts and professional contractors.

Share price

FND's share price has performed well since 2017, exceeding S&P returns with a % change of >150%. This has been driven by strong financial development that is underpinned by commercial strength, suggesting its trajectory is sustainable.

Financial analysis

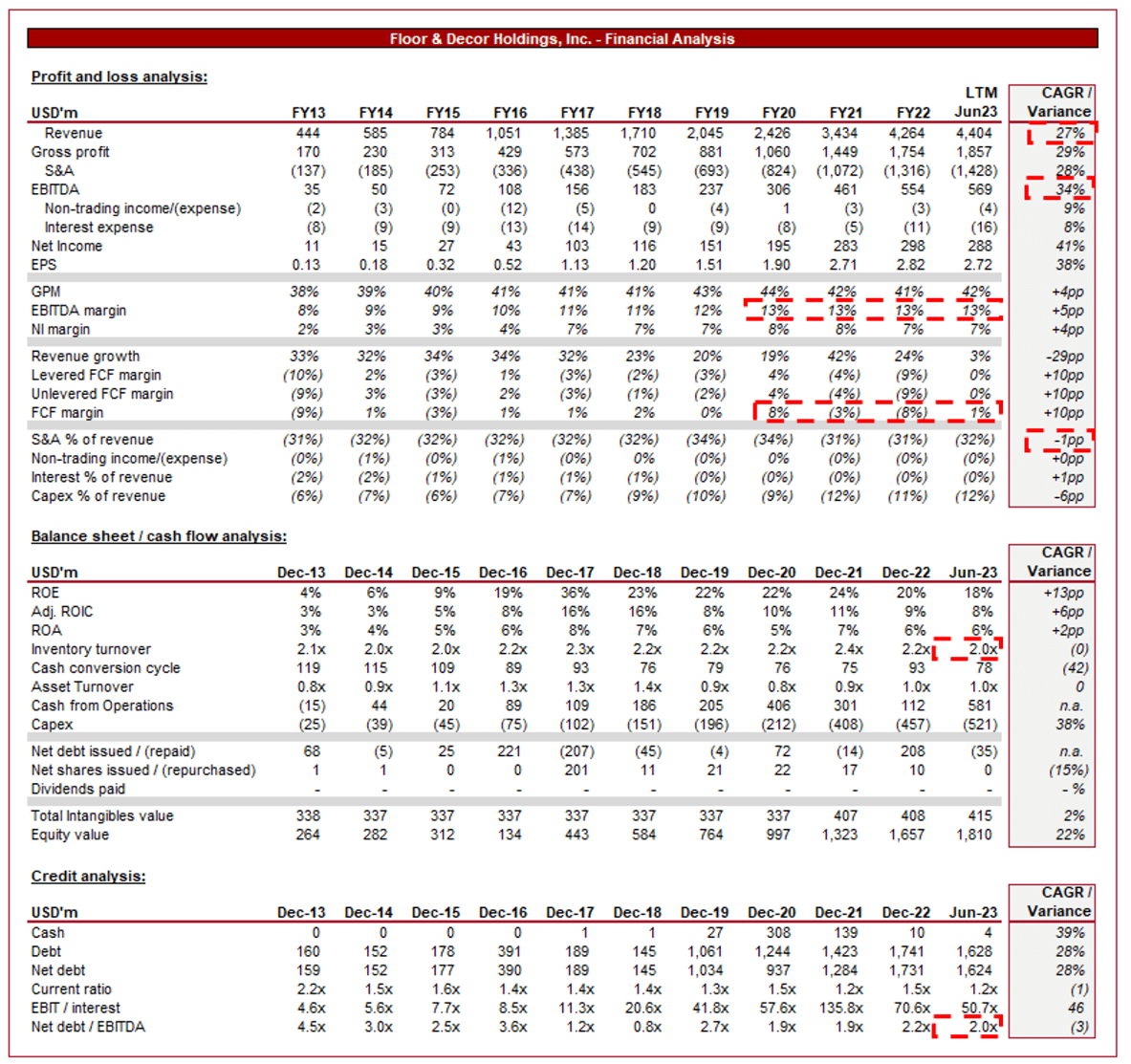

Floor and Decor financials (Capital IQ)

{kind=link}

Presented above are FND's financial results.

Revenue & Commercial Factors

FND's revenue has grown well during the last decade, with a CAGR of +27%. This impressive growth has been broadly consistent, with only a single fiscal year of <20% gains. In conjunction with this, EBITDA has grown by +34%.

Business Model

FND offers an extensive selection of flooring options, including tiles, wood, laminate, and stone. It provides various styles, designs, and price points, catering to a wide range of consumers. This allows the business to target homeowners, contractors, and interior designers.

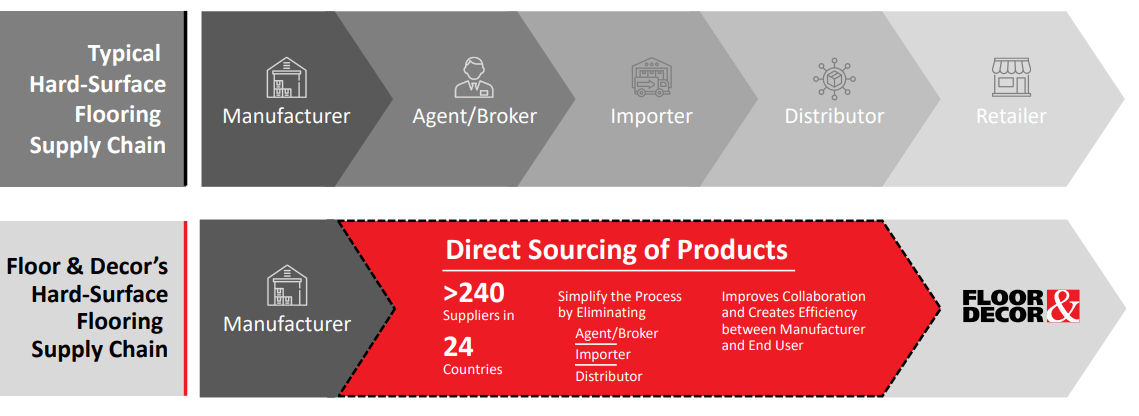

The company operates a low-cost business model, which includes efficient supply chain management, bulk purchasing directly from the source, and a streamlined store layout. This allows FND to offer competitive prices to customers on the bottom end.

{kind=link}

FND stores are designed to be DIY-friendly, with its website enhancing this further. It offers a hands-on shopping experience where customers can explore and interact with the products. Underpinning this are knowledgeable staff members available to provide assistance and advice and a website with information and guidance. The company also has a "PRO" services, with a loyalty program, Commercial credit options, Free Storage, etc. The business is positioned perfectly to support a range of customers beyond just simple factors such as price.

With the development of its PRO services into a fleshed-out offering, we see good growth potential from this segment. This represents a less volatile revenue stream due to long-term relationships and extended production cycles, with scope for up-selling related services such as financing.

{kind=link}

A key component of its current strategy is the objective to locate its stores in high-traffic areas, ensuring easy accessibility for both individual consumers and professional contractors. Proximity to customers enhances convenience and the ability to see before you buy. Management is currently investing heavily in new locations, which is the primary drive of its double-digit growth.

FND has invested in its online presence, providing customers with an easy-to-navigate website and mobile app. Customers can browse products, access installation guides, and even make purchases online. With a clear trend toward digitalization, we consider this to be a key benefit of the business. Management believes this omnichannel approach has been incredibly valuable to its growth story, as it positions its stores as both a location to purchase, a warehouse for stock, a place to pick up purchases, and a place to find inspiration.

Stores (Floor & Decor)

The home improvement industry is forecast to grow well in the coming years, with a CAGR of 6.7% into 2030. This is expected to be driven by broader macro trends, such as demand for housing, sustainability efforts, urbanization, and growing house prices. Despite the wider economic environment, we do not see much challenge to these trends, suggesting growth should be in the MSD range into the long term. FND faces stiff competition from the likes of Lowe's ( LOW ), The Home Depot ( HD ), and LL Flooring ( LL ) . We believe its specialization, supply chain strength, and growing national footprint should support good performance relative to these peers.

Margins

{kind=link}

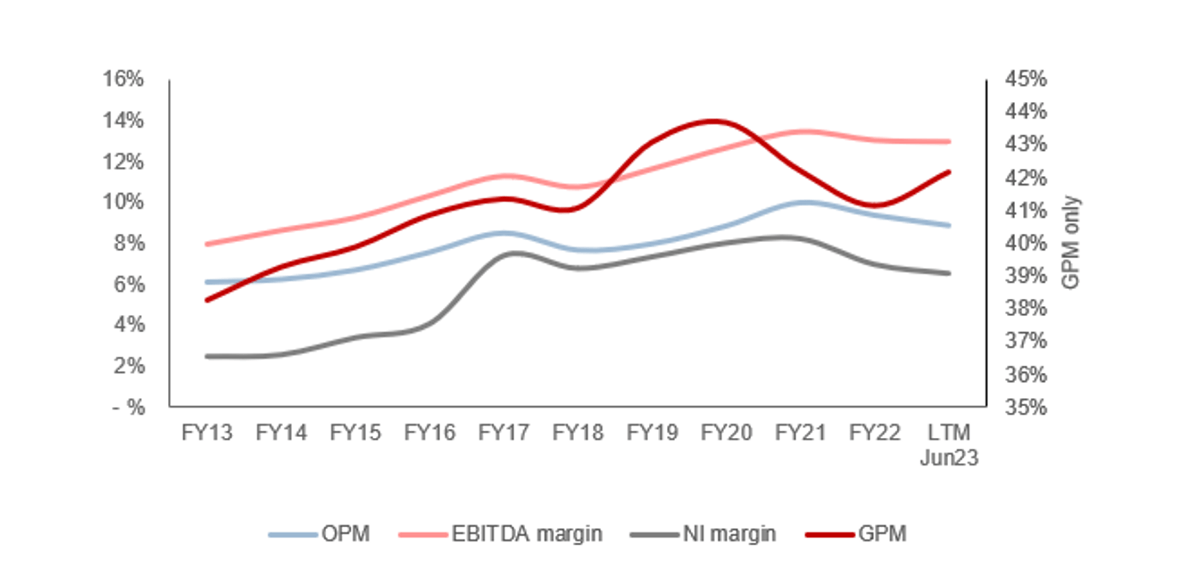

FND's margins have sequentially improved over the last decade, with EBITDA-M increasing from 8% in FY13 to 13% in the LTM. An EBITDA-M of 10-15% is broadly consistent with the levels expected for a retailer, with FND's improvement a reflection of economies of scale from growth and a product mix change toward higher-margin services.

Quarterly results

FND's recent performance has slowed relative to its 3Y performance, with top-line revenue growth of +25.2%, +14.6%, +9.1%, and +4.2% in its last four quarters. In conjunction with this, margin growth has stabilized, with EBITDA-M in all four quarters between 12.9% and 13.1%.

The slowdown in growth is a reflection of the current macroeconomic conditions, with heightened inflation and interest rates contributing to a reduction in consumer spending as a means of protecting finances. Further, many businesses are reducing spending where possible to protect margins and cash, contributing to reduced capital expenditure.

Compounding this for FND is that it is materially linked to the housing market. New home purchases and builds both contribute heavily to the demand for its goods. With interest rates at a decade-high, consumers are being priced out of purchases and have become significantly more hesitant. Home builders in response or slowing production.

The following datasets are key to illustrating this in our view.

- US Fixed Housing Affordability Index - This statistic " measures the degree to which a typical family can afford the monthly mortgage payments on a typical home. Value of 100 means exactly enough income to qualify for a mortgage. " This has fallen below 100 for the first time in over a decade and significantly so, implying a bearish outlook for home purchases in its core demographic. This is unlikely to unwind quickly given inflationary wage increases have already slowed.

- US Housing Starts - Likely in response to an affordability crisis, new home starts have declined to pre-pandemic levels. This metric will always undersell the significance of the issue, as the individuals inherently will need housing and so the rental market will buffer new purchases (if you cannot buy, you rent).

- US Median Sales Price - Despite slowing new supply, the Median Sales Price of properties has declined and noticeably so. The concern here is that individuals who have seen a reduction in their equity, or worse, are now in a position of loss. Individuals are far more likely to invest in their properties when comforted by equity value.

These three factors point to a bearish outlook for the industry. A large portion of the population is completely dissuaded from making purchases, and if they must, will likely trade down to protect finances.

We do not believe this is an issue that will quickly be alleviated. Looking ahead, we suspect expansionary policy can return in mid-to-late 2024 but the period until then looks difficult. Delinquencies are sequentially rising and through discussions in the market, we are hearing that corporate defaults will follow in the coming months.

We believe FND can do little to weather these concerns, relying on minimizing the impact on its top-line through new store locations. We would like to see the business utilize these periods to improve operational capabilities and be aggressive in gaining market share.

Key takeaways from its most recent quarter are:

- Comparable store sales decreased (6.0)%, illustrating the significance of the slowdown currently being experienced.

- Management is pivoting to internal improvement to focus on "what we can control", namely store experience and customer experience.

- Interestingly, Management stated that they will be "effectively managing our profitability". The outlook for margin contraction is uncertain, but we would not be positive about the idea of erosion through discounting.

- Management intended to grow market share by turning marketing focus on its low prices and value options.

- FND achieved its planned opening of 9 new warehouse stores, with the intention to open 32 warehouse stores in FY23. This should keep top-line performance positive while comparable growth is (5)%-(10)%.

Balance sheet & Cash Flows

FND's balance sheet is relatively clean, with a ND/EBITDA ratio of 2x (most of which is capital leases). This gives the business sufficient maneuverability to respond to the current macroeconomic environment.

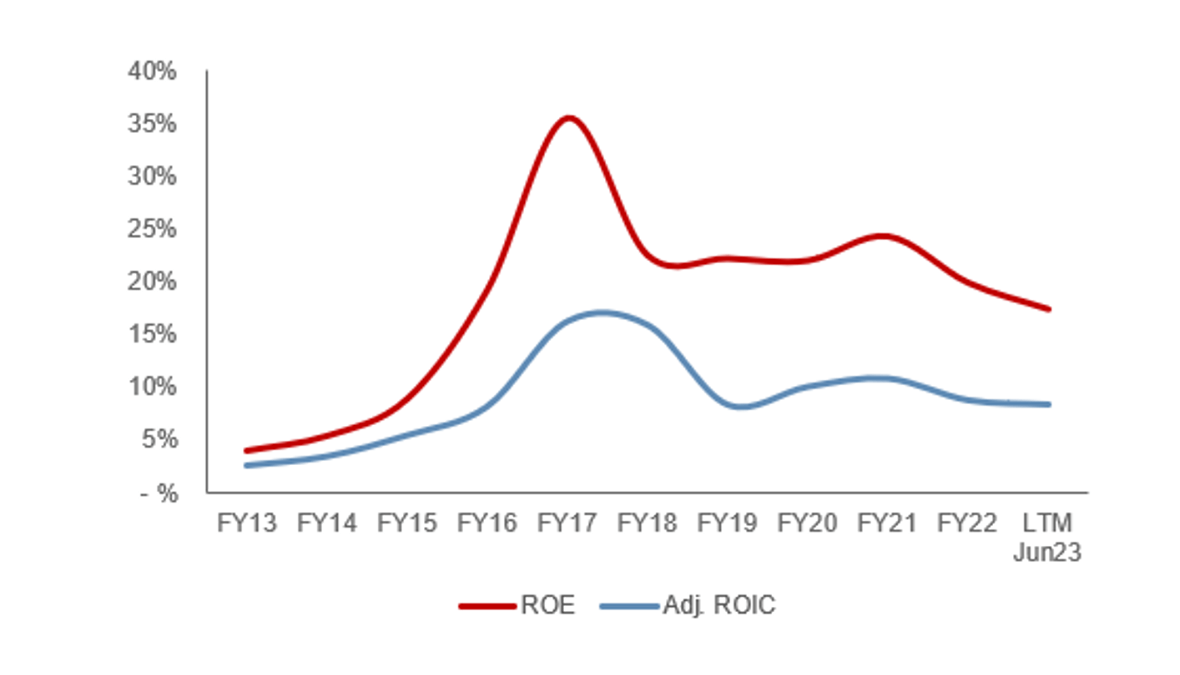

Management is currently heavily investing in growth, with minimal FCFs due to its reinvestment in Capex (which is currently 12% of revenue). As the following illustrates, ROE has broadly flattened in the region of 18-22%, which is a strong return when considering that many stores have not fully ramped up. For this reason, we are supportive of its cash investment in growth.

{kind=link}

Outlook

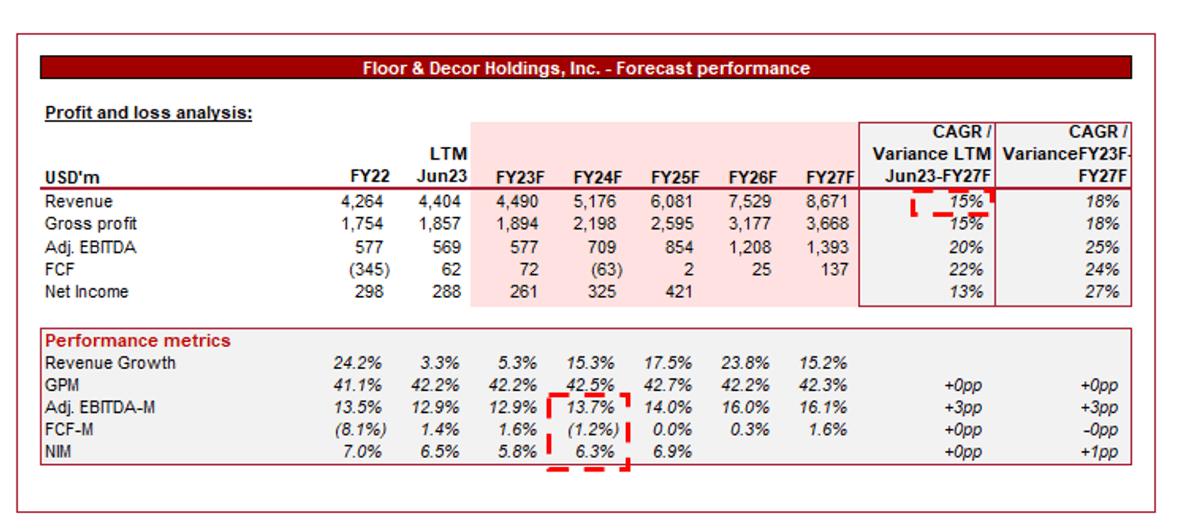

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of its strong growth trajectory, with a CAGR of +15% into FY27F. In conjunction with this, margins are expected to incrementally improve, allow of which come from the operating cost level.

We are supportive of the assumptions underpinning the current outlook over a 5 year period. With aggressive store growth and significant room for further market share growth and penetration, we see the existing strategy as sustainable. Further, with logistical benefits and economies of scale, margin improvement appears reasonable.

This said, we are less convinced by the FY24F assumptions. We do not believe the current macroeconomic environment is wholly being priced in. The slowdown in conjunction with cost inflation will mean store growth cannot be as aggressive in FY24. We suspect comparable growth will be negative again, or flat, in FY24F, limiting the scope to achieve +15% growth.

Industry analysis

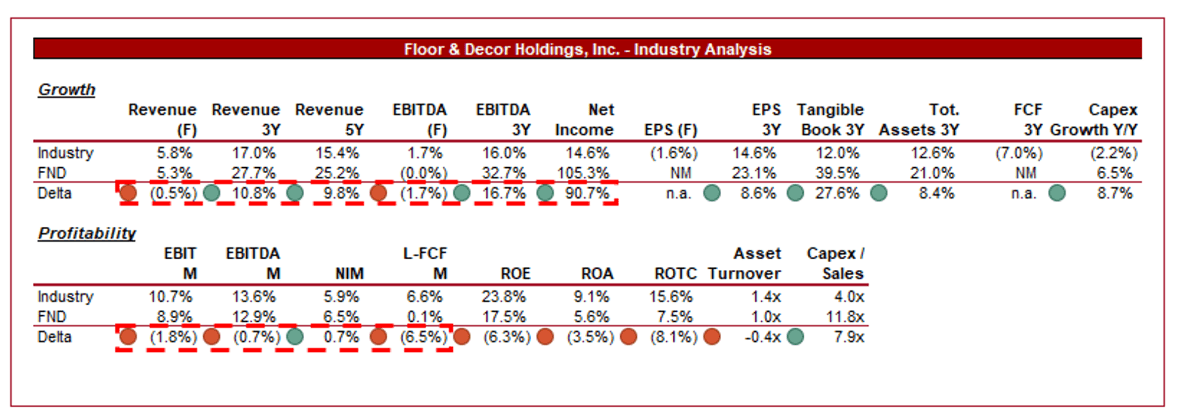

Home Improvement Retail Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of FND's growth and profitability to the average of its industry, as defined by Seeking Alpha (6 companies).

FND performs exceptionally well relative to its peers. The company has significantly outgrown its peers on a revenue and profitability basis, across several time periods, illustrating its impressive trajectory and market share growth. The company has benefited well from its attractive business model and specialism.

FND is currently operating comparable margins to its peers, although lags behind in ROE. Given the company is still in its growth phase and ramping up new locations, we suspect the business will normalize at a level in excess of its peers.

Valuation

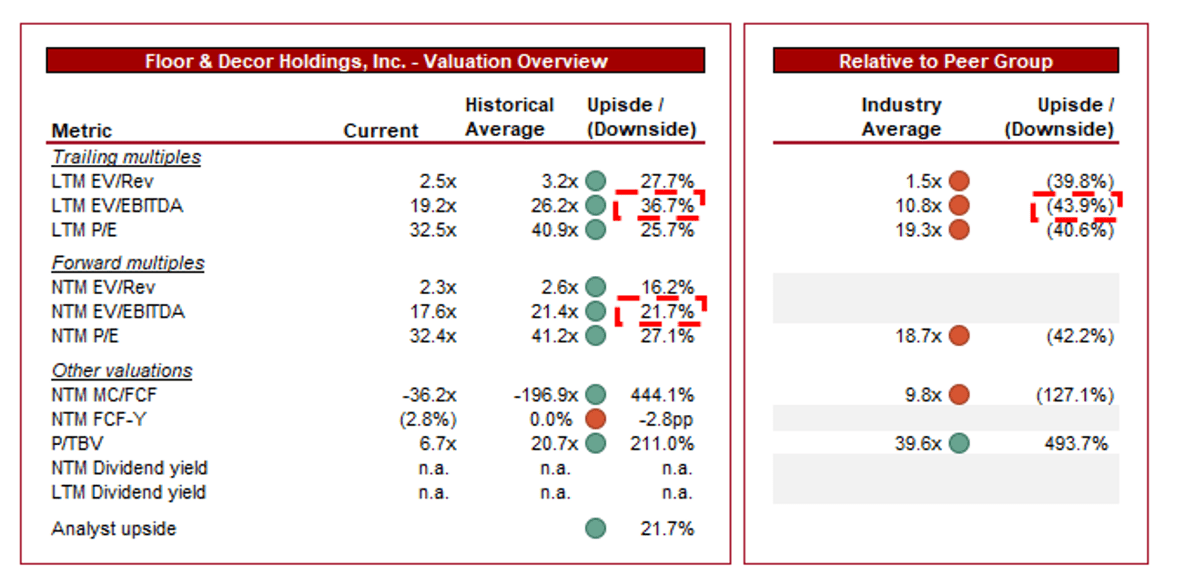

{kind=link}

FND is currently trading at 19x LTM EBITDA and 18x NTM EBITDA. This is a discount to its historical average.

A discount to the company's historical average is warranted in our view. Despite the strong financial and commercial development, investors had priced much of this in and beyond given the >20x multiple.

Further, FND is trading at a ~44% premium to its peers on a LTM EBITDA basis and a ~42% premium on a NTM P/E basis. A premium is warranted in our view, owing to the company's strong trajectory and scope for greater profitability in the long term.

Although FND is trading directionally as we would expect, we are hesitant about the degree. The near-term appears extremely difficult and we do see a downgrade to FY24F estimates. This could contribute to an expansion of its NTM trading multiples, beyond an attractive level we feel.

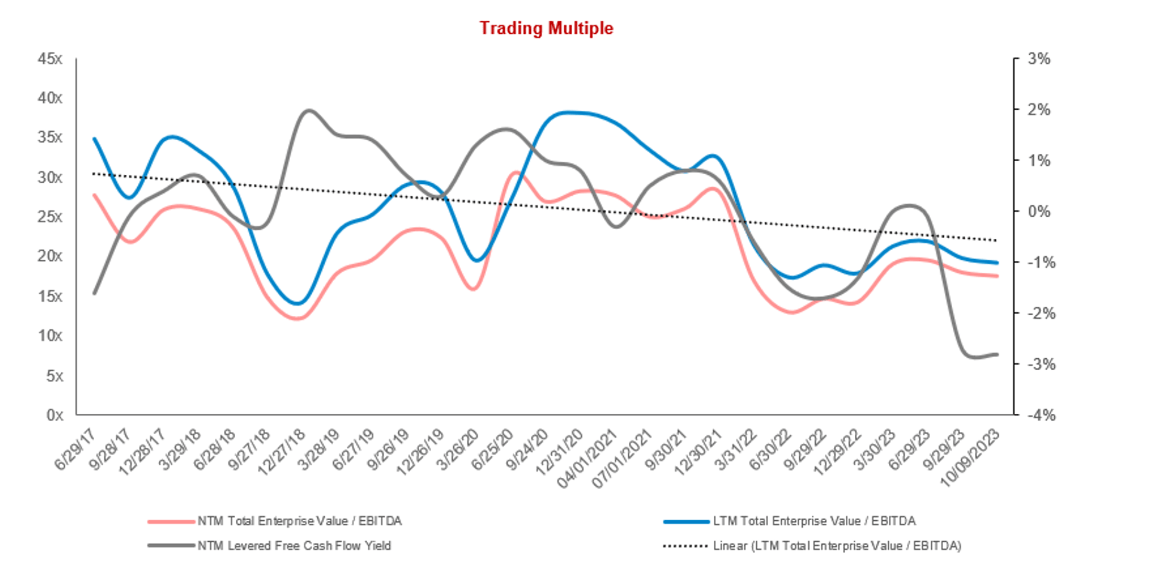

As the following illustrates, FND is only marginally below its trading valuation's trajectory, implying further downside is possible.

Valuation evolution (Capital IQ)

{kind=link}

Final thoughts

FND is a high-quality business that has a strong management team. The company is executing on a well-defined growth strategy, with the long term looking highly lucrative once cash reinvestment begins to slow. We believe an EBITDA-M of ~15% and a ROE of ~18% is achievable at a mature level, which should ensure strong shareholder distributions.

The timing currently is not correct, however. The business is facing material headwinds and has little scope to limit the impact. We expect this to cause share price stagnation until market conditions improve.

For further details see:

Floor & Decor: Its Impressive Growth Story Is On Pause