UP - Flying 'Wheels Up' - Not A Good Idea

Summary

- A reader of mine is in a fortunate position - he has a membership in Wheels up, which enables private aviation without having to own a plane.

- She asked me to take a look at the company from an investment point of view, because she's considering investing in the business. I'm happy to do so.

- This is my result of looking into the company, and my base thesis on UP - I look forward to your comments and opinions on this one.

Dear readers/followers

For some of us, flying or chartering in/a private plane can be said, together with yachts and the like, can be thought of as the epitome of having "made it", or of luxury. The comfort and convenience of being able to go anywhere, or simply enjoy a trip of a journey by sea or air, according to some, can't really be compared to anything else.

Well, in this article I'm taking a run at one of the companies in this field - The Wheels Up Experience ( UP ), which is one of the premiere businesses catering to exactly these needs.

Flying Wheels Up - from A to Z

The unique selling point of Wheels up, and similar companies, is that you can get initiated to the service fairly easily and cheaply - around $3000 to become a member, which doesn't sound much, and which renews at close to that level. Now, UP doesn't provide you with Gulfstreams or the like - instead, they manage a fleet of Cessnas, Beach Kings and other aircraft, but still respectable private jets.

However, to anyone thinking that this sounds interesting, take a firm hold on your ambitions to fly private, and realize that the company requires you to put down a certain deposit towards you charter hours - and anyone who deposits less than $100,000 has to wait 90 days before chartering, which should tell you what sort of sums are being typically deposited towards flight hours.

You also don't need to be a member to book Wheels up - it can be done on the app - but this greatly limits times and routes, and tie you to prices for a flight that are more or less 3-7x the cost of a regular ticket.

Part of the argument for these sorts of services is the ability to more freely choose flights and connections, to fly in smaller contexts (fewer people).

But to give you an idea of actual costs for flights, which should make this uninteresting to most readers, here are some stats which are about 1-2 years old, so add maybe 5-10% to those prices.

- King Air 350i: $5,295/hour

- Light jet: $6,495/hour

- Midsize jet: $7,795/hour

- Super-midsize jet: $9,295/hour

- Large-cabin jet: $12,995/hour

As you can see, the costs for actually doing this are quite prohibitive, unless you're the type of individual who doesn't mind a $20,000 expense - and there are obviously those among us.

The company's ambition is to be a total aviation solution to interested customers - and to make private flights accessible to a wider group of people than they might have traditionally been available to. Because while the above prices do sound expensive, they really are cheap compared to the actual ownership of owning your own place - which easily runs you into the multiple hundreds of thousands of dollars per year, and that's not even counting the purchase price for the plane.

This sort of service is always a trade-off. People who own private planes in part want this for the privacy and convenience of going anywhere, anytime, how they choose. By using a service like this, you're actually sacrificing some of this freedom in exchange for more affordability.

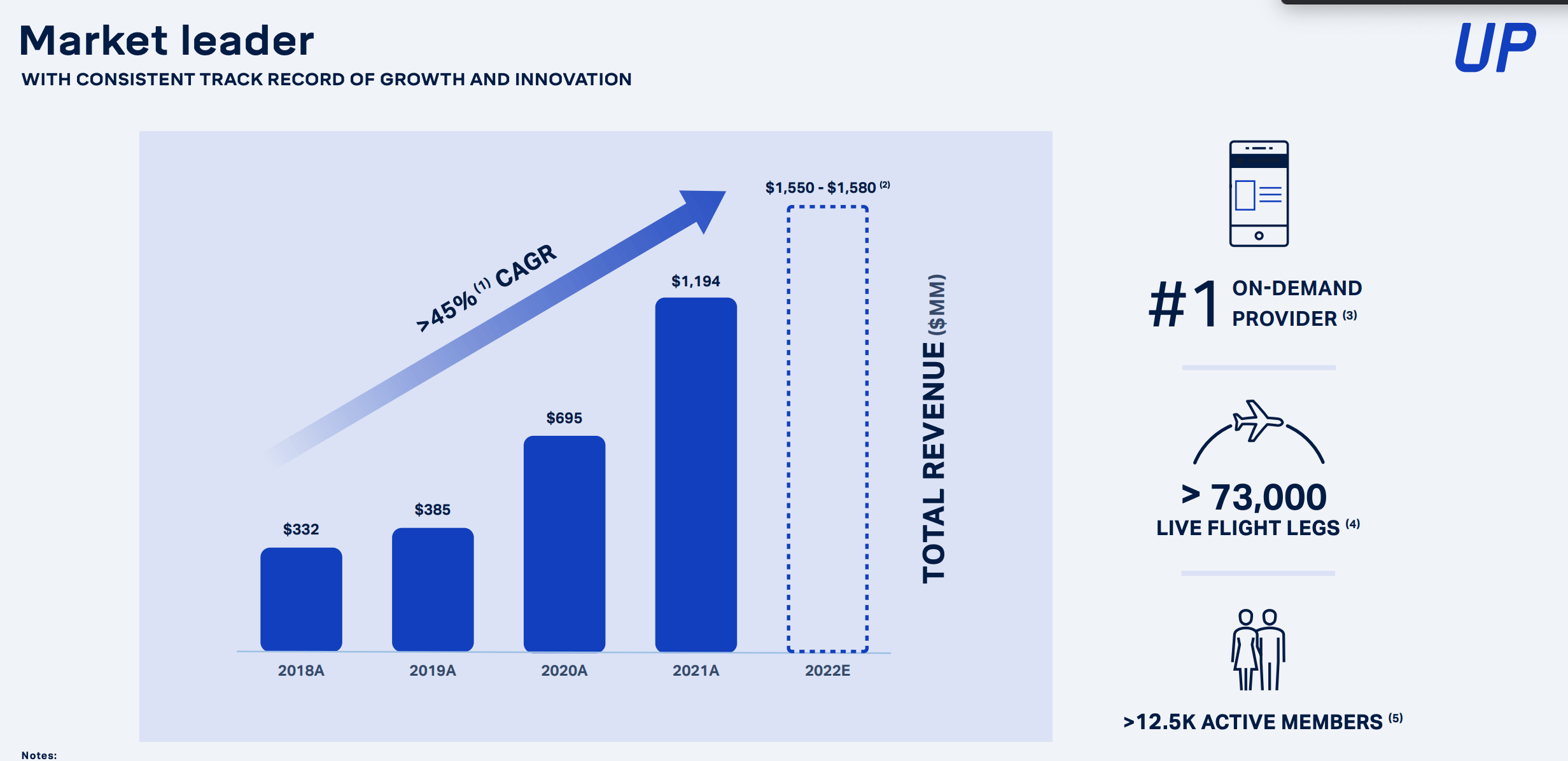

It might not be everyone's cup of tea, but it's clear that some people find it interesting and appealing, given the surge of memberships in 2021, not so much in 2022 as things turned sour.

However, turning sour is relative. The company still has some impressive numbers.

Wheels Up experience has 12,500+ active members, and as a business, generates revenues of upwards $1.5B per year for the 2022E period. This might not sound much, but it's impressive how quickly it got there and where the company comes from.

{kind=link}

Now, Wheels up has some interesting arguments for why the industry is ripe for disruption from actors like UP. They mention examples from other disruptors like Amazon ( AMZN ), Uber ( UBER ), Netflix ( NFLX ), and the like, but I would argue that any such comparison is flawed. That is even without mentioning that they exemplify it using Carvana, which is essentially a failed and bankrupt business. The difference between these businesses, or any of the ones mentioned, and UP, is that UP offers a premiumized service that even with a cheap membership initiation fee, comes at a premium to any sort of normal flying experience.

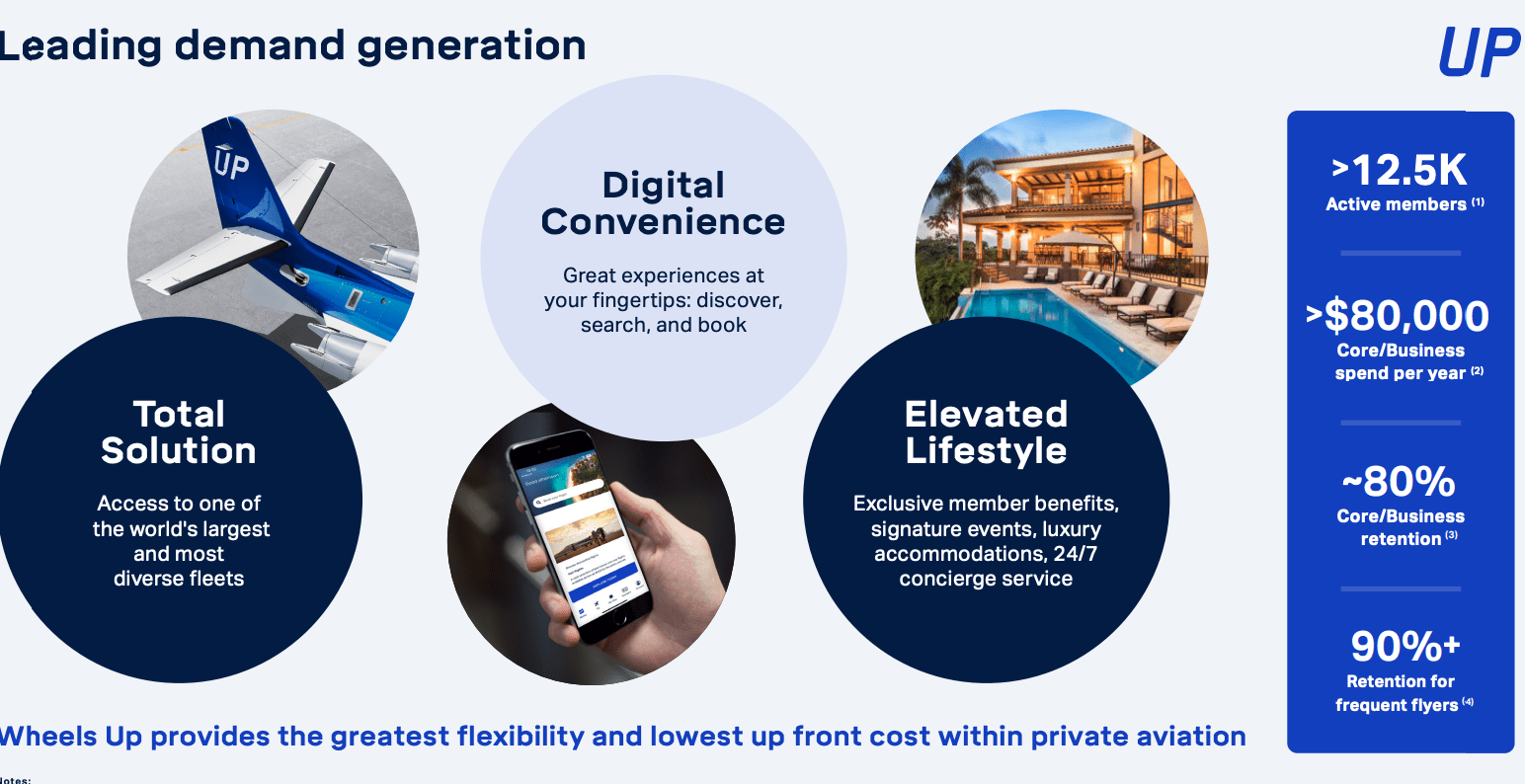

That isn't to say the company's general arguments are invalid as such. The market is incredibly fragmented - top 10 of this industry are at barely 8%, and 1,800+ of them operate less than 10 aircraft. Much in this industry still isn't digitized, but analog, and there's a lack of transparency in pricing and other issues.

The company does post impressive high-level numbers that suggest that most who use the company's service seriously, are very pleased with the convenience the company offers.

{kind=link}

The company is also pioneering several data-driven technology models connecting interested flyers to vetted private aircraft. UP isn't on its own either, it has a strategic partnership with one of the majors, Delta (DAL),

However, there are a few too many "buzzwords" in the company's presentation and filings. As you all may know, I prefer hard data and math. The simple fact is, this company is not yet profitable, and that's a huge issue for me.

Any company that debuted during the ZIRP and tries to transition to what we can call more normal operations is bound to face challenges. Not just in the financing side, but in the demand side. ZIRP and the entire 2016-2021 period brought up a collection of individuals who became used to living a "luxury" lifestyle without actually having the financial means to support such a lifestyle - It was based on credit and the environment we're in. We're seeing this in Europe as well.

It's not an irrational assumption, therefore, that UP is going to see a compression either in members or in the use members make of the company's services as people are being forced to tighten their belts.

And this is being combined with increased financing and interest costs.

Any assumption that the company is seeing scaling or volume advantages is easily disproven by very simple financials. The fact is, Gross margins have been steadily decreasing for several years. In 2018, GMs were 16.8%. Then they moved to 13%, to 12%, to 11%, and in LTM for 2022, we're now at gross margins of 5.6% - that's gross. Operating margins are negative at 22.7%.

Net income is negative $350M, or thereabouts, for the LTM period. This also comes as the company has nearly doubled its shares outstanding in less than 3 years. There's also a fair bit of long-term debt - $270M - on the balance sheet at this point, but this is only a faint positive given what's going on here, and that we're talking about a loss-making company. And double-digit negative operating margins isn't something you "just turn around", especially not in this environment.

The company's business model entails generating revenue off memberships, flights, aircraft management, and other (sub fees, MRO, FBO revenue). The company owns or long-term leases 180 aircraft, out of which 86 are turboprops. The company also offers its services through a number of local subsidiaries, of which there are five.

Obviously, risks to such a business as this are not small. Simple things like fuel costs, repair costs, staffing costs, and the seasonality we're seeing today, it all works against this company being an attractive investment in a way I've rarely seen before. Other contributors are mixed on this stock - but it's been undercovered for some time, and the reasons are understandable. Any positivity on this investment over time, as it stands, has resulted in massive declines in RoR. The company seemed to have been a bit of an investor favorite last year but is now down 67%+ on a 1-year basis. Not exactly good returns.

It has a market cap of $300M or thereabout, it has no credit rating, and despite a relatively impressive amount of insider activity - a positive one, I would say that Wheels up faces a fundamental identity crisis.

The company's entire set of operations and its current business model seems to be predicated on the assumption that there is a large, unapproached group of customers that have disposable income, and are willing to use it to fly private/semi-private instead of flying commercial at what is essentially a 2-3x premium from a normal ticket - at the very least.

While ZIRP may have briefly allowed for the interpretation that this group exists, and is significant, I argue that the group, if it does exist, is extremely small. This company, as I see it, is a failure in its business model. It's too spread out, and it's trying to capture or keep customers that cannot keep the company in business - especially given the way the market looks today.

The fact that the company CFO openly discusses that UP needs to "decide" who its customers are, suggests to me that this is a company still in its infancy. Like other companies during ZIRP, UP has been able to significantly grow its customers and revenue base, as well as its revenues.

However, the mistake people make when looking at a company like this is assuming that increased revenue has a positive correlation to profits. This is not always the case, and it's not the case for this particular business.

Instead, the correlation is the opposite. The more revenue the company has, the faster UP loses money. Cash burn here is intense, and UP, as of December, has less than $600M In cash and equivalents left before it needs to tap financing or equity.

In the end, this sort of company is hard for me to argue for. It's not that I don't like or understand the company's business model - I just don't think it works, and I think the company is starting to realize it, which is why it's starting to change.

{kind=link}

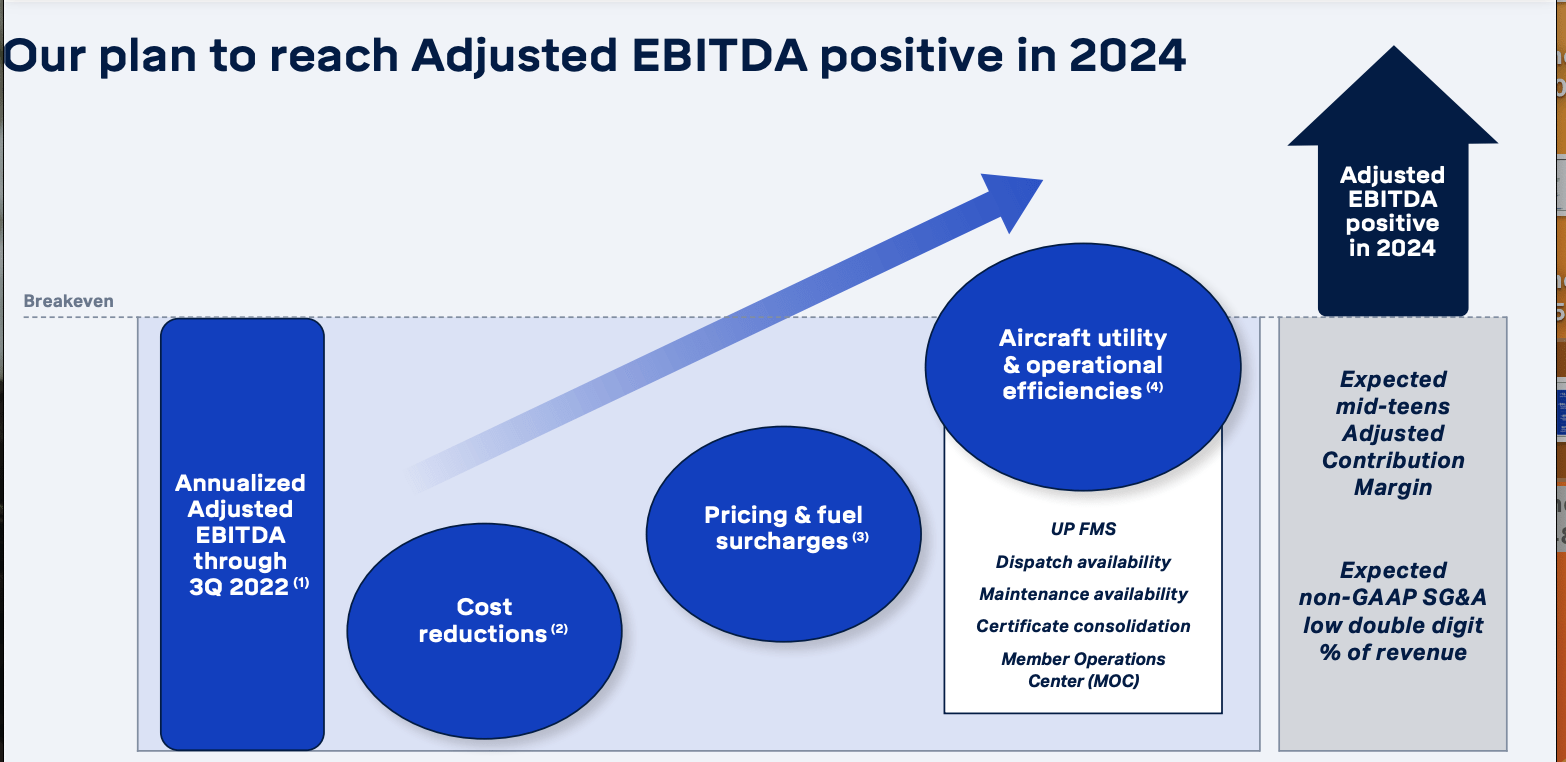

Simple solutions for profitability need to be implemented. Far from growing revenue unprofitably, it needs to consolidate and institute cost control. Start getting up gross margins back above 10%, and give us a pathway to positive OM. The company is arguing that it's moving towards positive adjusted EBITDA in 2024E, which I view as a pipe dream unless those adjustments are something truly outlandish. The company is focusing on reducing costs, surcharges, and operational efficiencies, which translates to lower dispatch availability times, maintenance, consolidation, and changes in the MOC.

The problem with some of those measures is that affluent customers are relying exactly on those freedom-providing variables to drive appeal for what the company offers. And with surcharges and pricing likely going up, that's going to be the bargain-seekers, if they can be called that, away as well.

Let's look at what you should pay for this company.

Valuation for Wheels Up

$0.

I'm only half-kidding, as I have a very low tolerance toward loss-making companies. Estimating what a negative profit business is worth pretty much can come down to the SOTP valuation, the sum of the company's parts, once debt and other considerations are removed.

Wheels up is trading at a fairly amazing revenue multiple of 0.05x. Barring negative, that's one of the lowest I've ever seen. We also have a 0.15x sales multiple, which makes sense, because a sale for this company shouldn't be worth much given that there aren't any positive earnings from a sale. At today's valuation, the company is priced 0.5x to book value, which is low - but has been lower.

Analysts following the company actually do exist - we're seeing 7, and 2 of those are at a "BUY". They value the company at $1.3 low, and a high of $5. With a share price of $1.14 and an average of $3.54, that should mean that 7 out of 7 of these analysts should be at a "BUY". The disparity between these numbers and recommendations should tell you exactly what these analysts actually think, and how serious they are on their stances.

Also, consider the fact that these analysts gave the company a PT of $15 back in 2021. The company was still unprofitable back then. If you'd followed that gem of a recommendation, you'd have been down over 80% at this time.

I'm tempted to give my first "$0" rating in terms of PT, but that would be unprofessional - and every company is worth something. But I'm fairly well-versed in the aviation industry, and leasing/maintenance/operations with planes, given that I spend plenty of time with companies like Exchange Income ( EIFZF ).

Some might have believed the company found an unapproached or untapped, profitable market.

I say, the company "found" a market that should never have been approached in the first place, and anyone with extensive aviation industry experience or in a position in a company like this has likely already considered similar business models and discarded them due to being too risky.

That is not a great position to start out in, but that is where Wheels Up is. And for that reason, I'll impair the company's book value by at least 90%, and my average, impaired SOTP valuation comes to around $0.2/share.

Even at that price though, you should first consider what alternatives might be available to you, and what this company's plans are.

Here is my thesis for Wheels up

Thesis

- Wheels up is a company that targets the private aviation market, and seeks to make the concept of flying "private", or "Wheels Up", available to everyone, or at least a wider audience.

- I question whether this customer segment actually exists, and more importantly, whether the customers can provide positive GAAP to the company, which to me is the first requirement for an investable business.

- For that reason, I'm at a firm "HOLD" here, and I don't think you should invest in the company here.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills none of my criteria for investment. If you own it and want to own it, it's a "HOLD" - but I wouldn't buy this one here under any circumstances for this price.

For further details see:

Flying 'Wheels Up' - Not A Good Idea