KNSL - For Kinsale Small Remains Beautiful

2023-12-26 17:15:25 ET

Summary

- Kinsale Insurance focuses on providing tailored insurance for the excess and surplus lines sector in the US.

- The company emphasizes smaller to medium-sized risks and aims to improve cost efficiency through technological advancements.

- Despite a mature market cycle and pricing pressures, Kinsale remains optimistic about future growth prospects and aims for a long-term growth target of 10-20%.

- Consider accumulating KNSL when valuations become more reasonable.

Kinsale Capital Group, Inc. ( KNSL ), established in 2009, is focused on providing insurance specifically tailored for the excess and surplus lines sector within the United States. After a strong run in its share price, expectations for Kinsale Insurance remain high due to strong performance in revenue and profits, outpacing similar specialty insurers. Today KNSL faces some challenges in the market and headwinds from the property and casualty cycle. Growth in their unique E&S submissions might slow despite rate adjustments. In a recent investor day presentation, KNSL highlighted its strategy of being solely focused on E&S despite being in a mature phase of the specialty cycle. KNSL's avoidance of delegated underwriting, along with its highly rated fixed income portfolio, set it apart from its US and Bermuda counterparts. Nonetheless, given its current valuation compared to peers, KNSL is a hold today. There is room for KNSL's multiples to rerate lower in 2024 driving a potential decrease in its share price.

Why Small Remains Beautiful

In 2024, Kinsale plans to continue exclusively focusing on underwriting Environmental and Social (E&S) policies for the foreseeable future. Their emphasis lies on smaller to medium-sized risks, where competition is lower, and risks are smaller, particularly targeting business with annual premiums under $15,000, which constitutes 75% of their business. They prefer in-house underwriting over delegated authority as it's more cost-effective and avoids potential conflicts of interest. Kinsale prioritizes a streamlined claims process and overall cost efficiency. They take pride in their competitive acquisition ratio (15%, compared to the industry's 17-20%) and aim to further improve their already strong expense ratio of around 10% through technological advancements. Adjustments in their strategy involve introducing new casualty and property products, specializing their organizational structure due to business growth, and restructuring their technology systems.

{kind=link}

KNSL is hiring and organizing internal underwriters for new business lines and prefers aligning them with the company's unique culture rather than relying on external talent. Additionally, they anticipate cost savings as they retire older systems without incurring additional expenses for technological updates.

COO Remains Optimistic Despite Softer Pricing

The market cycle for E&S is mature and pricing remains under pressure. On this topic, COO Brian Haney shared an optimistic outlook on various market aspects during an investor day hosted by KNSL. Pricing, though lower than recent highs, remains favorable overall. There's a notable increase in business flowing into the excess and surplus (E&S) lines, indicating a shift from admitted markets. Property insurance market stability has improved, with healthy pricing and terms. Casualty insurance maintains a steady to improving pricing environment, while professional lines see softer pricing but strong margins due to prior years' gains. Haney highlighted key factors: Reinsurers' cautious stance on pre-COVID accident years might drive further price shifts in casualty insurance. Elevated natural catastrophes in 2023, primarily from severe storms, impacted the market. Inflation, though lower than its peak in 2022, could help mitigate observed loss trends. Economic softness in construction and real estate markets affected premium growth, and higher bond yields are boosting insurer profitability and market discipline. Stuart Winston sees the hard casualty market in a later stage, while John Bowen views the property market as the best in two decades and still evolving.

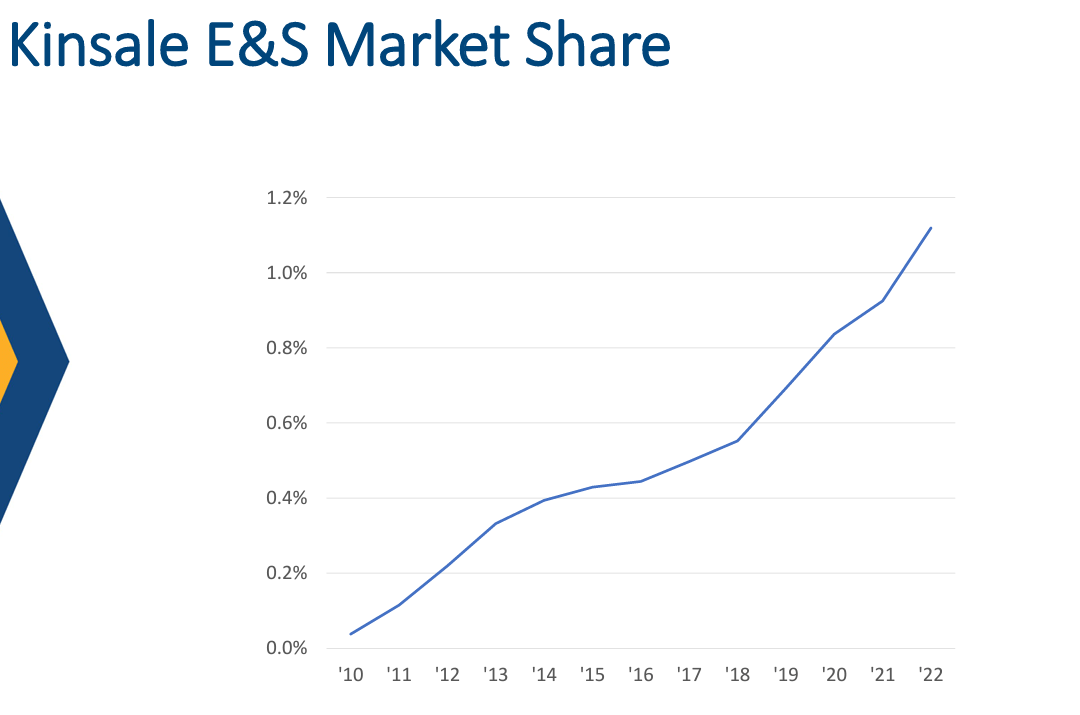

Kinsale's management also remains positive about its future growth prospects despite significant recent market share gains. They estimate their potential market share within the E&S market to be much larger than their current 1%, suggesting substantial room for expansion. Using a comparative framework, they highlight that the market share of other top E&S companies is several times higher than Kinsale's current share. CEO Michael Kehoe reiterated a long-term growth target of 10-20%, similar to previous statements. Analysts believe that Kinsale's ability to surpass the overall E&S market's growth, projected to be in the mid to high single digits, is feasible due to its significant cost advantage, allowing for competitive growth without compromising pricing.

{kind=link}

Multiples Remain Stubbornly High Despite Softening Market Conditions

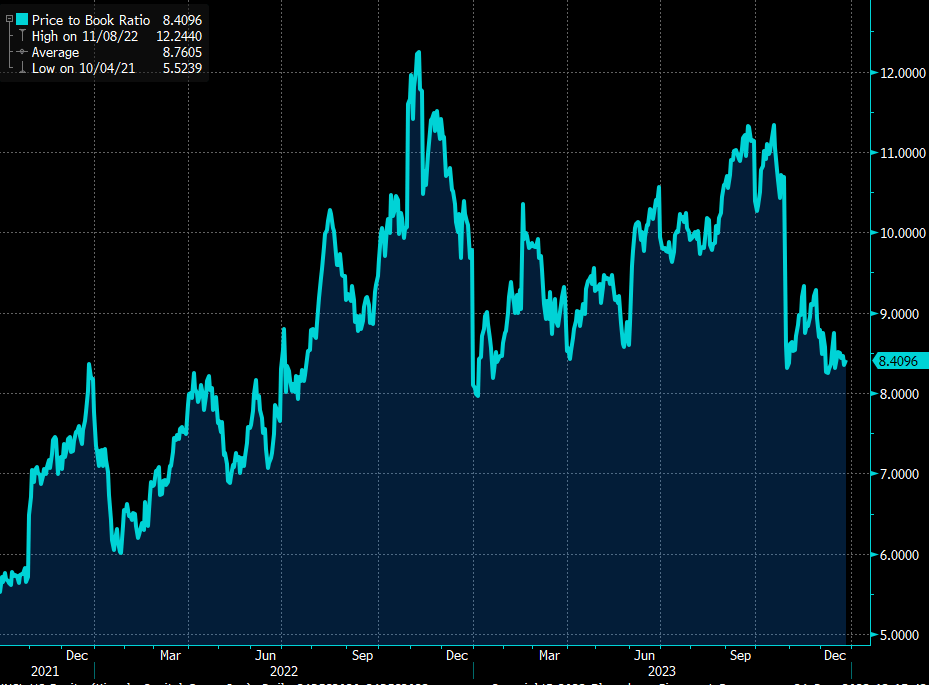

KNSL's wonderful execution on its strategy has attracted significant investor interest. This in turn has made KNSL a rather expensive proposition for new investors. As the chart below shows, KNSL's price to book value has increased from ~5.5x in early 2022 to a lofty ~8.4x at the time of writing. Put differently, all else being equal, KNSL's multiple expansion has made the stock over 50% more expensive over the past two years.

{kind=link}

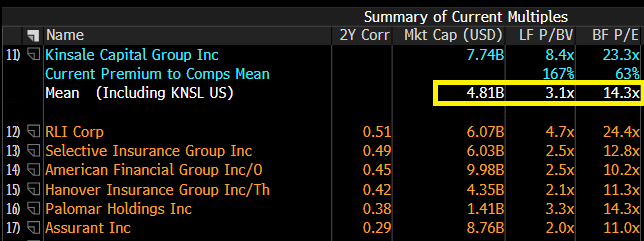

I recognize that KNSL is unique in that it is 100% focused on E&S insurance, however, when compared to peers which operate in KNSL's segment and with a similar market cap, KNSL's valuation looks quite rich.

{kind=link}

As shown by the table above, KNSL trades at an enormous 167% premium to its peer group on a Price/Book multiple and a 63% premium on a Price/Earnings multiple.

Conclusion

If you've been fortunate enough to have built a position in KNSL over the years, I'd advise holding onto it. I'm a fan of KNSL's business model—its focus on small and medium businesses has turned it into a profit-generating machine. With its continued focus on the E&S segment, I anticipate KNSL's profitability to maintain stability around its historical averages. However, the market cycle is indicating a softening trend as evidenced by pricing pressures. This could impact KNSL's profits over the next 12-24 months. KNSL's valuation multiples have also surged over the past two years. For this reason, I'd suggest waiting for more reasonable valuations in the future before considering accumulating a position in KNSL.

For further details see:

For Kinsale, Small Remains Beautiful