CA - Fortuna Silver Mines: A Massive First Quarter From Seguela

2023-10-06 14:09:49 ET

Summary

- The Gold Juniors Index has continued its plunge from its Q3 2020 peak, and Fortuna Silver Mines Inc. hasn't fared any better, underperforming by over 1500 basis points.

- Fortunately, the company's Q3 results were better than expected, and its new Seguela Mine came out swinging with impressive positive grade reconciliation.

- In this update, we'll look at whether this changes the thesis on Fortuna Silver Mines Inc., dig into the stock's valuation, and see whether the stock has finally entered a low-risk buy zone.

It's been a rough stretch for the Gold Juniors Index (GDXJ), with the sector finding itself down ~31% from its May highs despite a relatively mild decline in the gold price. This performance is even more frustrating when looking at the 3-year return, with the GDXJ down nearly 55% since Q3 2020 in a period when the gold price is relatively flat, which has some investors scratching their heads. Unfortunately, it's not this simple, and while the gold price has held its ground above $1,800/oz outside of brief excursions below this level, margins have clobbered, affected by rising labor, fuel, and consumables costs. The result? A 35% plus decline in margins sector-wide from peak levels in Q3 2020, and up to 75% declines in margins for higher-cost producers.

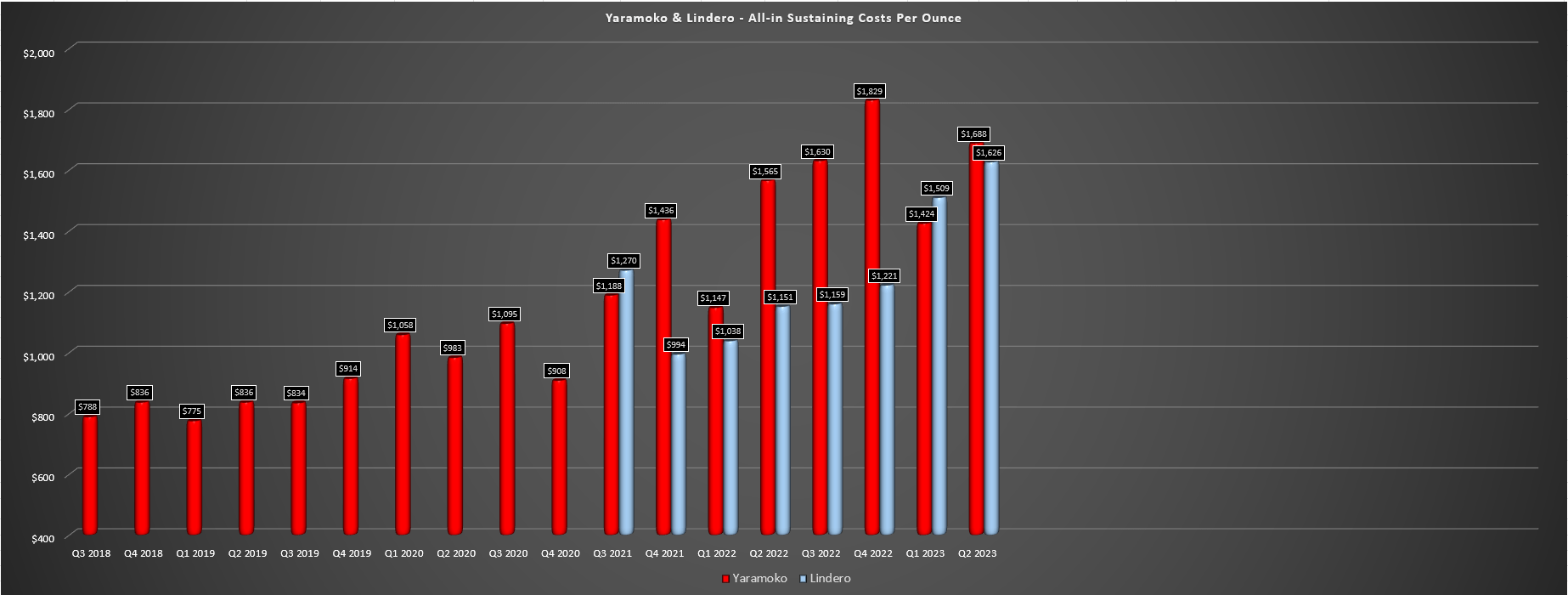

At the time of the Fortuna Silver Mines Inc. (FSM) acquisition of Roxgold in 2021, there was reason to be quite optimistic about the company's future, given that it was adding a sub $850/oz all-in sustaining cost [AISC] mine that would help its consolidated costs, pulling its company-wide AISC back below $1,150/oz. However, two years of inflationary pressures have thrown a wrench in these plans, and Seguela is now looking like a $1,000/oz AISC mine, given that the 2021 AISC projections did not include corporate G&A and we've seen significant inflation over the past two years. And with Seguela being a ~$1,000/oz AISC mine and the rest of its operations having costs above $1,500/oz on average on a gold-equivalent basis, the outlook for margins is much weaker.

Fortuna Gold Mines - Quarterly AISC - Company Filings, Author's Chart

{kind=link}

That said, for things that Fortuna can control, it's worth commending the company for bringing this asset into production on schedule and budget, and the first quarter out of Seguela was certainly impressive, well exceeding my expectations of 26,000 to 28,000 ounces. And while these grades were well above the average reserve grades over the mine life and won't last, it was nice to see some positive grade reconciliation even if a relatively small sample of total tonnes relative to the mine life, and with the better than expected grades partially offset by fewer tonnes.

In this update, we'll look at the Q3 production results and whether the stock is finally offering a margin of safety after significant outperformance in the past few years.

Seguela Mine Operations - Company Website

{kind=link}

All figu res are in United States Dollars unless otherwise noted.

Q3 Production & H2 Outlook

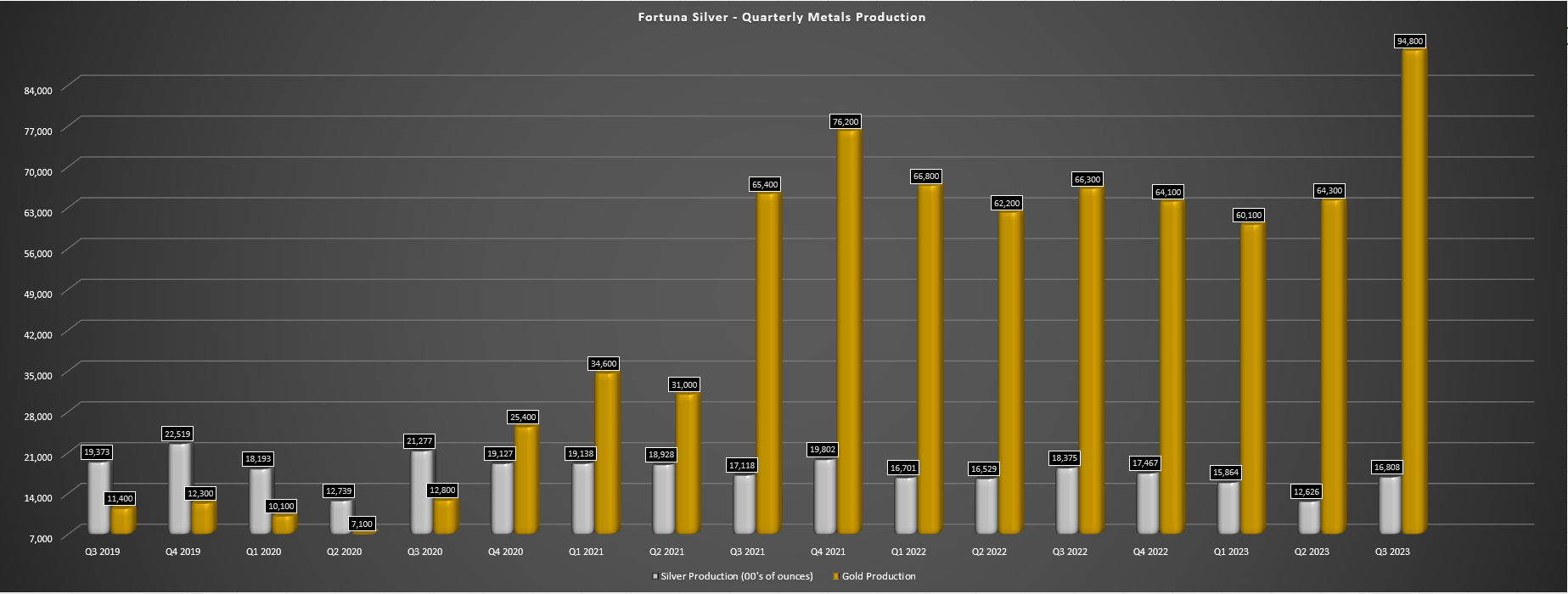

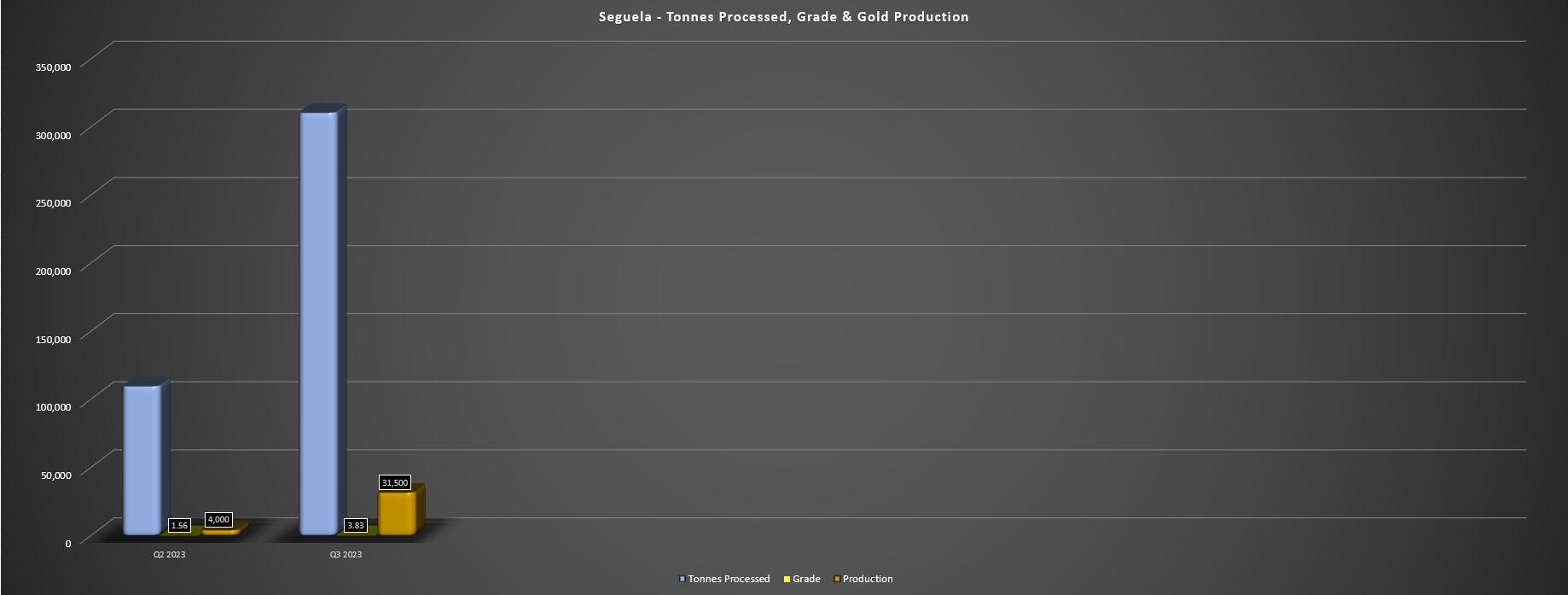

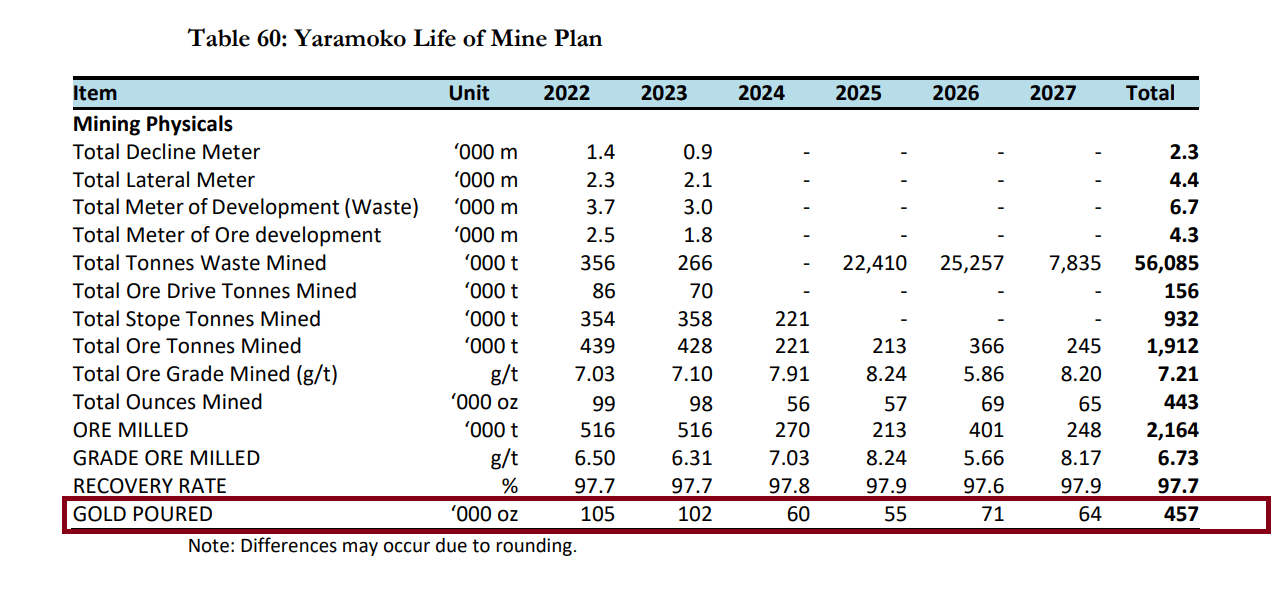

Fortuna Silver Mines ("Fortuna") released its Q3 results this week, reporting quarterly production of ~94,800 ounces of gold and ~1.68 million ounces of silver, translating to a 43% and 8% decline from the year-ago period. The sharp increase in gold production was helped by another solid quarter out of Yaramoko, which benefited from above-average head grades in the period, but the major contributor was Seguela, which came out of the gate strong with ~31,500 ounces of gold produced in its first full quarter.

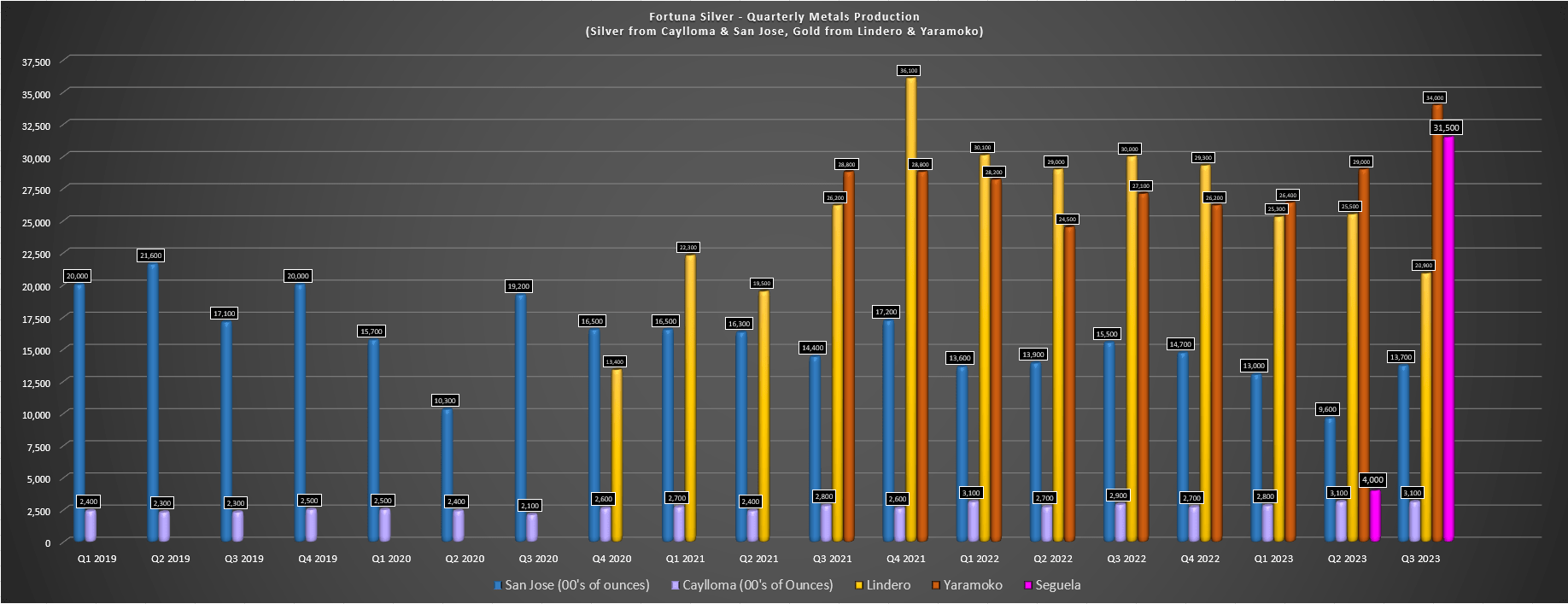

Unfortunately, the solid results out of these two mines were offset by another soft quarter at San Jose with less than ~1.4 million ounces of gold produced, and a further decline in production at its Lindero Mine in Argentina, with lower grades resulting in a 30% decline in production to just ~20,900 ounces. The result was that despite the addition of a new mine, gold production was only up 15% to ~116,000 gold-equivalent ounces from Q4 2021, despite a ~60% increase in the share count related to the Roxgold acquisition.

Gold-equivalent ounce production comparisons use a constant 80 to 1 gold/silver ratio.

Fortuna Silver - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, we can see that Seguela moved up to the #2 spot in terms of quarterly output, just behind Yaramoko, which had an abnormally strong quarter with its grades coming in ~15% above expected life-of-mine grades at 7.73 grams per tonne of gold. Meanwhile, Lindero and San Jose have seen a continued decline in quarterly production, with Lindero's production peaking in Q4 2021 at ~36,000 ounces and set to settle at a lower level of ~25,000 ounces per quarter in the future. Finally, Caylloma brought up the year with ~300,000 ounces of silver, but this is a relatively insignificant asset, especially with lower zinc prices than last year weighing on costs because of reduced by-product credits.

So, what led to the impressive performance at Seguela?

Fortuna Silver Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

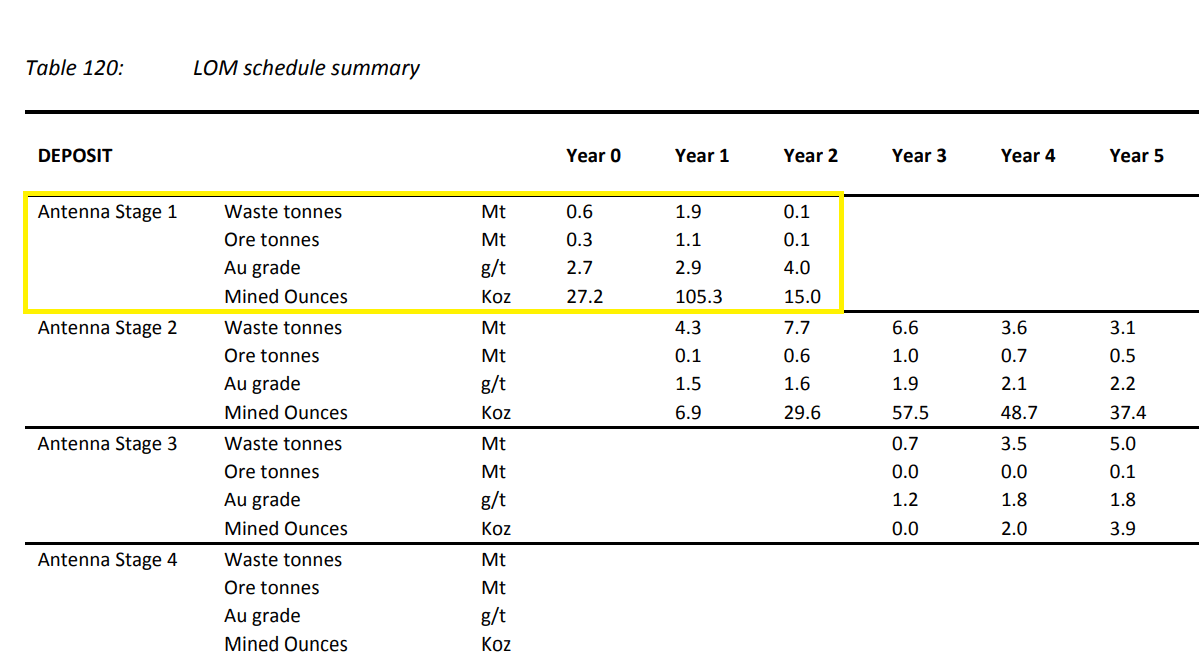

While Seguela is certainly a phenomenal asset with above-average open-pit grades, the Q3 performance was much better than I expected, with ~502,000 tonnes mined at 3.48 grams per tonne of gold at a low strip ratio of 2.3 to 1.0. These better than expected grades combined with throughput rates above nameplate capacity (plant throughput was 174 tonnes per hour in September, 13% above nameplate capacity) helped the asset to deliver well above my estimates of 27,000 ounces of gold in Q3, and Fortuna noted that grades have reconciled well since mining began, with the 6 percent dip in expected tonnes more than offset by a 29% increase in grades. As shown below, higher grades were certainly to be expected from Antenna Stage 1, with an expectation of ~1.5 million tonnes at 3.0 grams per tonne of gold from this first phase of the project.

That said, this is a significant outperformance. While it's encouraging, I wouldn't be banking on this level of positive grade reconciliation in the future which bumped up the Q3 output.

Antenna Stage 1 - Grades & Tonnes - 2021 TR

{kind=link}

That said, investors can be excited because the plant is running at well above nameplate capacity, suggesting this asset can run at closer to 1.55 to 1.60 million tonnes per annum, in line with levels it expected to ramp up to in Year 3 according to its initial mine plan. Assuming the asset can operate at ~1.50 million tonnes next year with an average grade of ~3.40 grams per tonne of gold for its first two years, the asset should produce upwards of 155,000 ounces per annum, setting it up to report new quarterly records closer to 40,000 ounces over the next several quarters. Hence, there is some upside to the production we just witnessed at Seguela, and as noted in past updates, there is room to optimize this mine plan by pulling forward high-grade ounces from Sunbird.

Seguela - Operating Metrics & Gold Production - Company Filings, Author's Chart

{kind=link}

Although this is certainly exciting, this is just one asset, and the reality is that while the best years are ahead of Seguela, with an average annual gold production profile of ~150,000 ounces from 2024 to 2027 at sub $1,050/oz AISC, the best years are behind the company at three of its other assets, which include Lindero (past its peak years of grade), Yaramoko (steadily declining throughput offsetting similar grades), and San Jose, which continues to see declining grades and is struggling to replace its reserves.

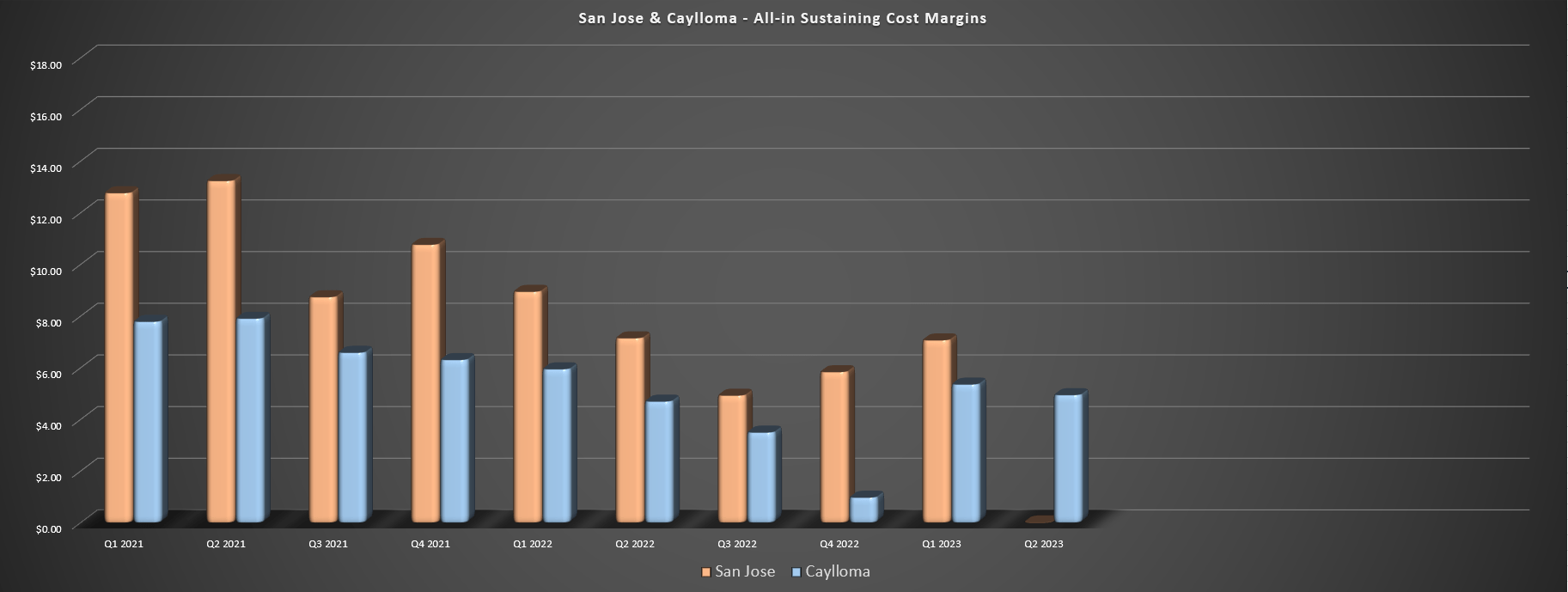

So, while it's certainly positive to have this impressive asset online and firing on all cylinders, Seguela is no Fekola, which transformed B2Gold (BTG) overnight into a cash flow machine, so it's only going to help so much from a cash flow standpoint when balancing this against declining production at its other assets. And, as I've stated previously, I am not optimistic about reserve growth at San Jose/Yaramoko, with sticky inflationary pressures potentially contributing to rising cut-off grades and a higher hurdle to adding new reserves at these mines.

San Jose & Caylloma - AISC Margins - Company Filings, Author's Chart

{kind=link}

Finally, it's worth noting that while Seguela will have a strong H2 with elevated grades and a full quarter of higher processing rates (~360,000 tonnes) in Q4, the company isn't getting any help from the gold price, and certainly not from the silver price. In fact, silver is back to plumbing its year-to-date lows and its margins were already razor-thin at its silver assets in Q2 despite a higher silver price. So, while there's no question that Fortuna's gold business will have a better H2 with the benefit of a third mine in Seguela, the silver segment will have another rough half year, especially if silver can't find its footing soon given that the company is up against similar silver prices, higher consumables inflation, and a stronger Mexican Peso (despite the recent rebound) on a year-over-year basis at its flagship silver mine, San Jose.

Valuation

Based on ~310 million shares and a share price of $2.84, Fortuna trades at a market cap of ~$880 million and an enterprise value of ~$1.07 billion. This is a very reasonable valuation for a multi-mine producer that is diversified across the Americas and in West Africa.

However, it's important to note that two of the company's mines have sub 4-year mine lives and a poor track record of reserve replacement, and one of the company's mines is relatively insignificant (Caylloma). Hence, although the company is a five-mine producer, its future looks to be that of a three-mine producer, as San Jose and Yaramoko are likely to head offline by 2027. This means that while the company will see a significant increase in revenue and cash flow in 2024 and 2025, these numbers are not run rates that can be relied upon post-2025 when Seguela sees a slight dip in production, San Jose potentially heads offline, and Yaramoko also has a much less significant production profile, even if it can add some reserves at 55 Zone extensions.

{kind=link}

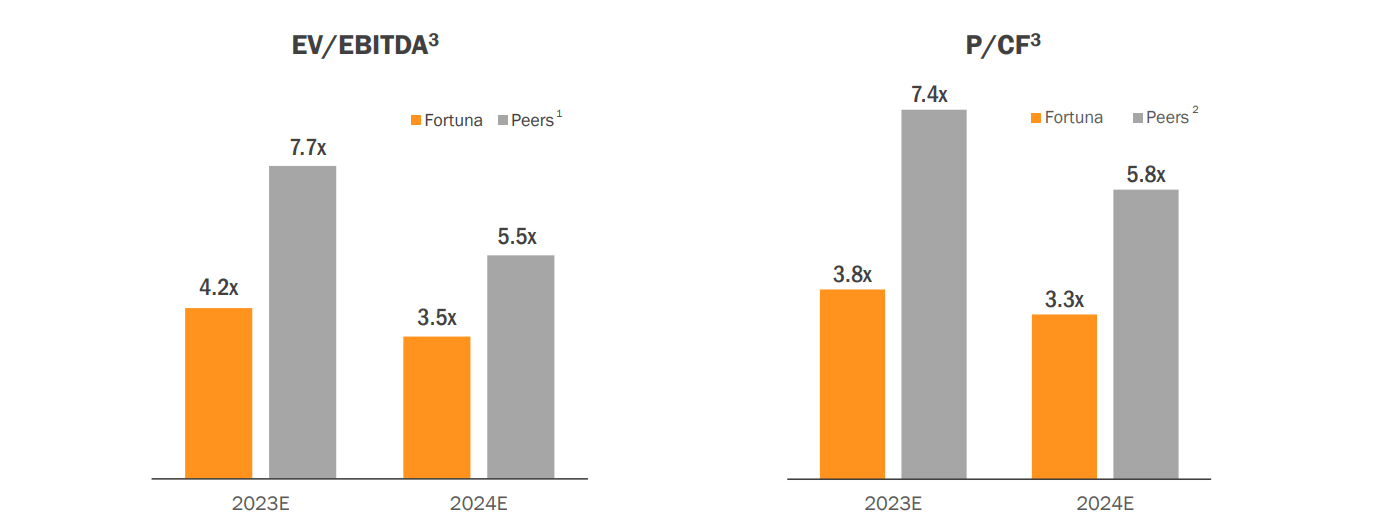

Given this setup, I don't think it's fair to value the stock on a price to cash flow basis, and I think a significant weighting should be placed on P/NAV vs. P/CF given that the forward 10-year run rate will look much different from the elevated years of 2024/2025. Plus, while Fortuna is quick to point out that it remains discounted relative to peers on a P/CF and EV/EBITDA basis in its most recent presentation, these charts can deceive if one doesn't read the fine print. And while the company does trade at a discount to its peer group, I would argue that it has conveniently chosen its peer group to include three groups that benefit from higher multiples on balance, including:

1. Some of the lowest-cost producers sector-wide like Lundin Gold (LUGDF), Alamos Gold (AGI), Dundee PM (DPMLF), and Centerra Gold (CGAU).

2. Several Tier-1 jurisdiction producers like SSR Mining (SSRM), Wesdome Gold (WDOFF) and OceanaGold (OCANF).

3. The highest-margin and only large Tier-1 jurisdiction silver producer: Hecla Mining (HL).

And with only one West African producer in the peer group and Fortuna hardly being a silver producer - with the bulk of its revenue from gold (and less silver revenue than its silver producer peers on balance) - it's no surprise that this discount is in place, as the peer group is not realistic compared to Fortuna's portfolio.

FSM EV/EBITDA & P/CF Multiple vs. "Peers" - Company Presentation

{kind=link}

The second point worth making is that while there might have been an argument for using a 5% discount rate for Fortuna previously to calculate its net asset value, it's hard to justify using this same discount rate today when rates are much higher and over 50% of its net asset value is tied to a Tier-3 ranked jurisdiction: West Africa. And even if we use a 5% discount rate for its non-West African assets and a 7% discount rate for Seguela, Yaramoko and Diamba Sud, Fortuna's estimated NPV comes in at ~$1.55 billion, with an estimated net asset value of ~$1.11 billion after subtracting out estimated corporate G&A and net debt. If we divide this figure by 310 million fully diluted shares, Fortuna's fair value comes in at US$3.60, translating to a 26% upside from current levels.

To be fair, I think we should assign some weighting to P/CF, and use what I believe to be more conservative multiples of 5.5x forward cash flow and 1.0x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see a fair value for Fortuna of US$4.05. However, I am looking for a minimum 40% discount to fair value to justify owning small-cap producers based primarily in Tier-2/Tier-3 ranked jurisdictions (Mexico, West Africa, Argentina, Peru). And after applying this discount, the ideal buy zone for the stock comes in at US$2.43 or lower, slightly lower than my previous low-risk buy zone of US$2.60 which the stock has rallied 7% from recently. So, while FSM has undoubtedly become more reasonably valued, I continue to see more attractive bets elsewhere in the sector, and one could argue that a 7% discount rate still isn't cheap enough for West African gold mines in the current rate environment.

Summary

Fortuna Silver Mines Inc. had a decent production quarter, and the stock continues to trade at a very reasonable valuation, especially if it were a diversified silver producer in the Americas. However, with its silver exposure being a melting ice cube and its gold exposure predominantly coming from a jurisdiction where low single-digit cash flow multiples are not unusual, it's hard to argue for any extreme undervaluation relative to its more relevant peers like Perseus Mining (PMNXF) and Endeavour Mining (EDVMF).

In fact, Fortuna arguably looks expensive relatively, trading at ~3.2x forward EV/EBITDA vs. Perseus at ~2.5x and Endeavour at ~3.6x despite these being larger and higher-margin producers. That said, if Fortuna Silver Mines Inc. shares were to decline below US$2.44, it would drop into a low-risk buy zone. So, if I were looking to add long exposure and was comfortable owning what's become primarily a small-cap West African gold producer, FSM looks like an attractive reward/risk bet below US$2.44.

For further details see:

Fortuna Silver Mines: A Massive First Quarter From Seguela