CA - Fortuna Silver: Seguela Doesn't Fix Rising Costs At Existing Assets

2023-05-08 05:40:16 ET

Summary

- Fortuna Silver continues to be one of the worst-performing precious metals stocks, up just 4% year-to-date, translating to a fraction of the return for the Gold Juniors Index.

- This share price performance is even more disappointing given the stock's underperformance since 2021, with FSM entering the year down ~60% from its 2021 highs.

- And while the company's Q1 results were satisfactory & its new Seguela Project will head into production by June, uncertainty related to San Jose continues to weigh on the stock.

- So, with rising costs (ex-Seguela), short mine lives at two assets and continued uncertainty related to San Jose plus the stock trading in line at a slight premium to estimated net asset value, I see zero margin of safety here.

Just four months ago, I wrote on Fortuna Silver ( FSM ), noting that there was limited margin of safety at a share price of US$3.90 and that there was no reason to pay up for the stock. Since then, the stock has made zero upside progress despite a ~10% gain in the gold price and new 52-week highs for silver, with the stock massively underperforming its peer group. I attribute this outperformance to the stock heading into the 2023 trading at ~1.0x P/NAV, a rich valuation for arguably a West African gold producer with a small side of silver and Argentinian gold production. Plus, the outlook isn't getting any better in Mexico, with continued permitting uncertainty for San Jose, a recent illegal blockade, and negative mining reforms. Let's take a look below:

{kind=link}

Q1 Production

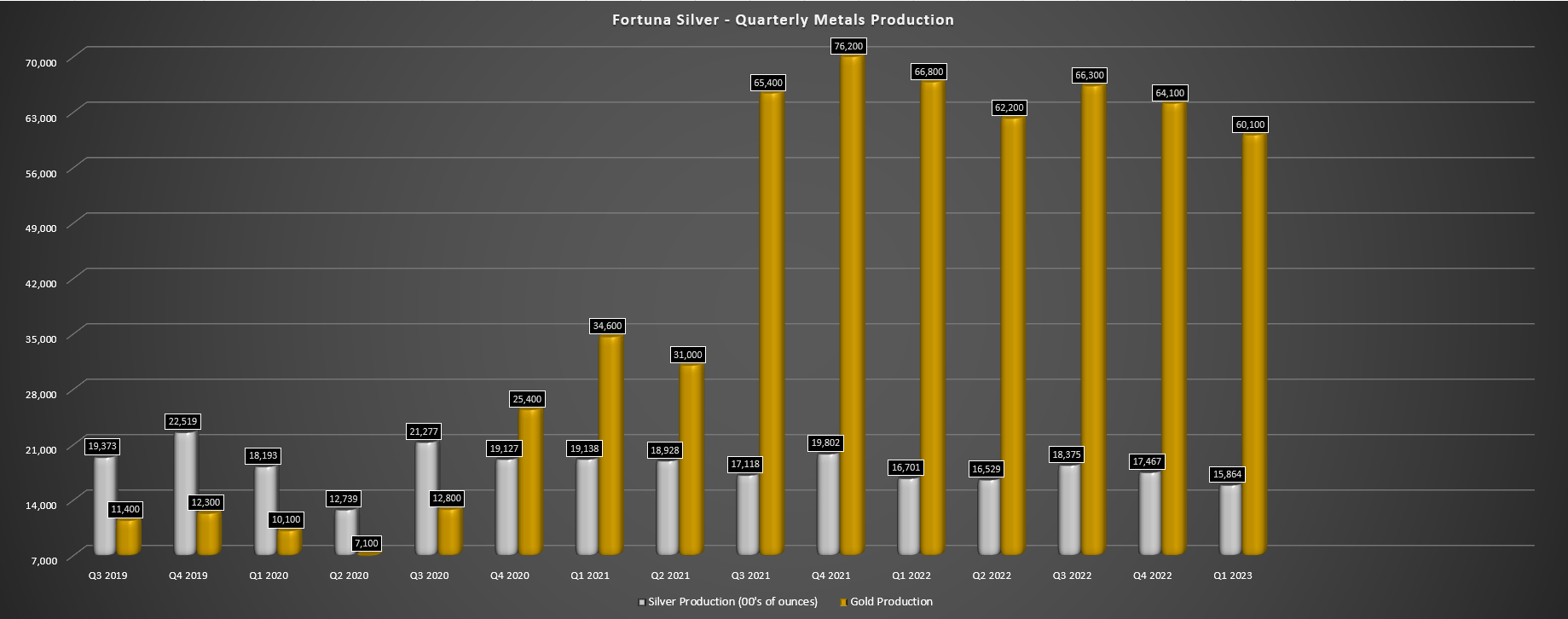

Fortuna Silver released its preliminary Q1 results last month, reporting quarterly production of ~1.59 million ounces of silver and ~60,100 ounces of gold, with the company continuing to be primarily a gold producer with a 73%/27% gold/silver profile using a 75 to 1 gold/silver ratio. And while these production figures were slightly better than I had expected, silver production declined 5% year-over-year while gold production fell 10%, impacted by lower grades at all of its assets. This was most prevalent in its gold segment, with Yaramoko's grades down 21% year-over-year and Lindero's grades down 19% to 5.94 grams per tonne of gold and 0.71 grams per tonne of gold, respectively.

Fortuna Silver - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

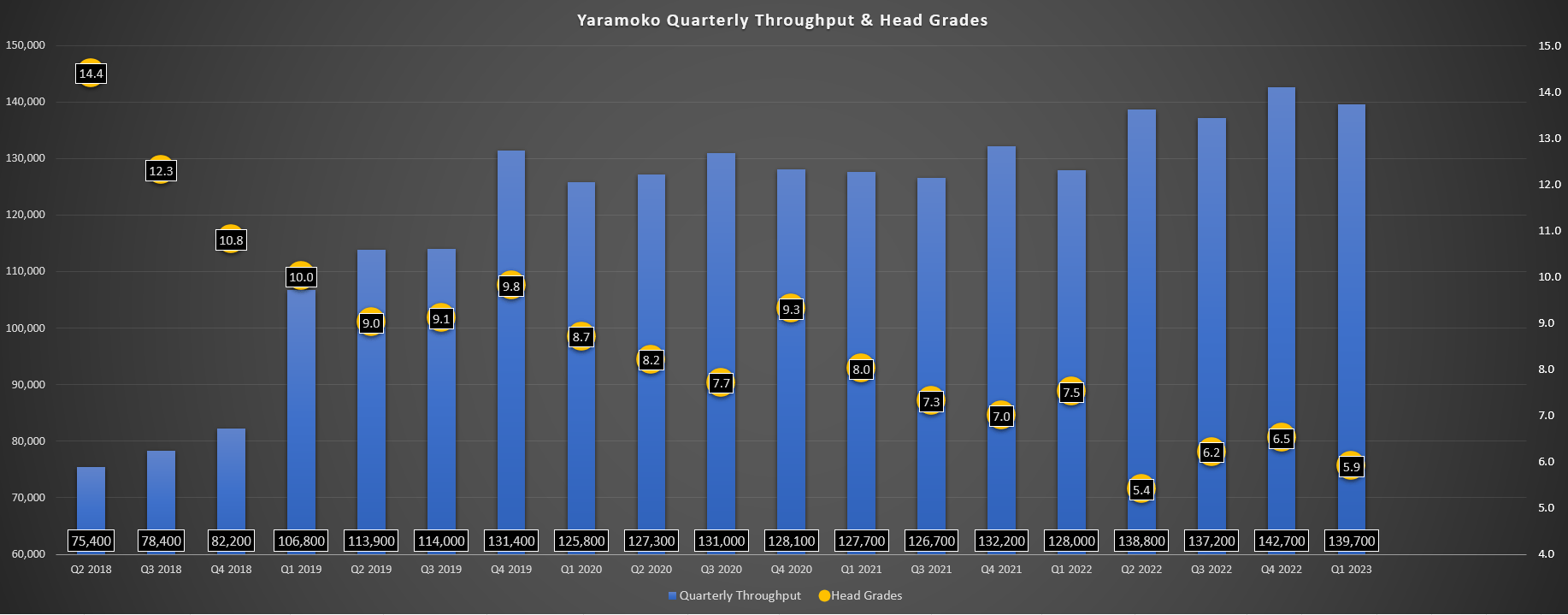

Digging into the production results, Yaramoko continues to disappoint from a production and cost standpoint, with steadily declining grades and higher throughput having a material impact on costs. And while production was up marginally on a sequential basis to ~26,400 ounces of gold in Q1, production fell over 6% year-over-year. As shown in the below chart, the increased throughput of ~139,700 tonnes (Q1 2022: ~128,000 ounces) could not make up for the significantly lower grades, and judging by the current mine plan, we should see a steady decline in throughput in the future at only slightly better grades (6.50+ grams per tonne of gold), making this a sub 65,000-ounce per annum asset at ~$1,500/oz costs when factoring in inflationary pressures.

Yaramoko - Quarterly Throughput & Grades (Company Filings, Author's Chart)

{kind=link}

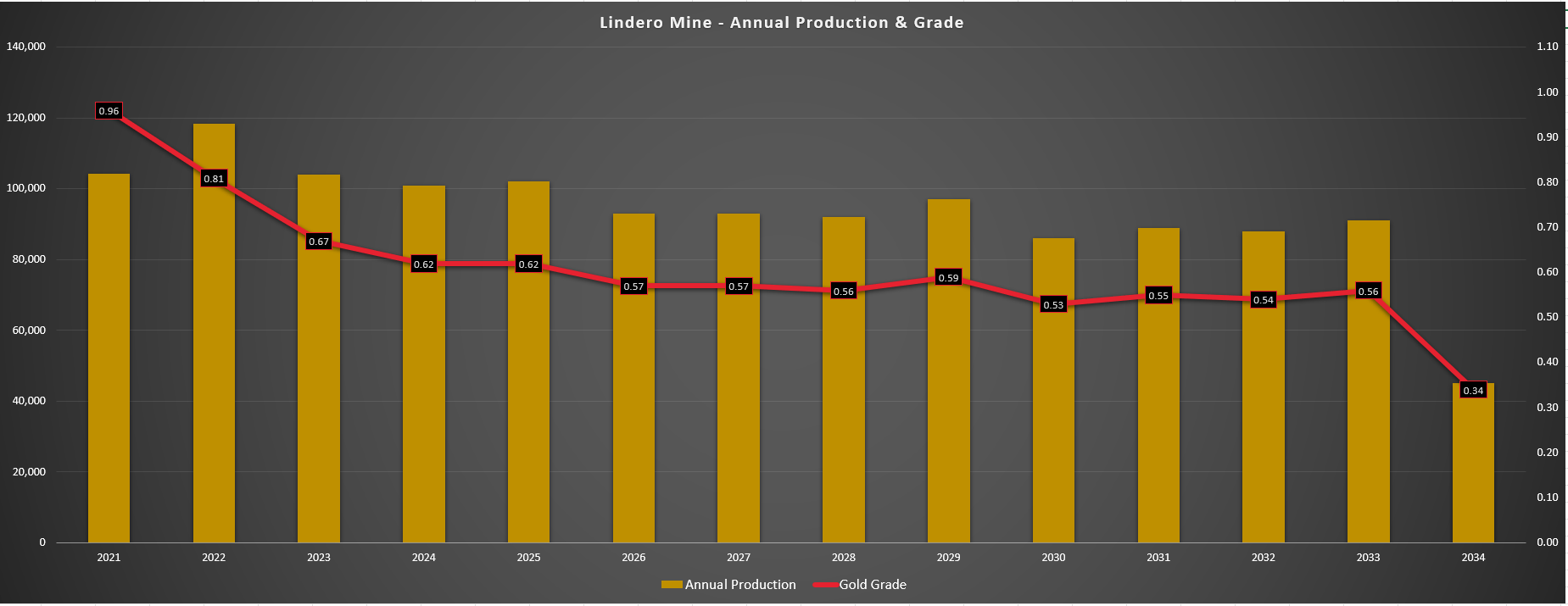

Moving over to Lindero, the best grades are in the rear-view mirror as I warned last year, with the mine plan expected to see a material drop-off in grades post-Year 2, with average grades declining from an average of ~0.90 grams per tonne of gold to sub 0.70 grams per tonne of gold. As the mine plan shows, and like Yaramoko, the grade profile is not expected to improve much, with average gold grades over the mine life of sub 0.60 grams per tonne of gold when excluding the first three years of elevated grades. In a pre-inflationary environment, this was not an issue, with costs expected to remain below $1,000/oz. However, the impact of inflationary pressures and a much lower production profile have severely impacted unit costs, and the new normal looks to be ~$1,400/oz plus AISC, 7% above the industry average.

Lindero Proposed Production & Grades (Company Filings, Author's Chart)

{kind=link}

As for Q1 production, Lindero's grades slid from 0.88 grams per tonne of gold to 0.71 grams per tonne of gold, which should result in a material increase in all-in sustaining costs year-over-year when combined with increased sustaining capital this year (P2 leach pad expansion), and heavy equipment replacement. During the quarter, Lindero's production slid to ~25,300 ounces of gold vs. ~30,100 ounces of gold year-over-year, and I would not be surprised to see all-in sustaining costs [AISC] come in above $1,470/oz in FY2023, translating to a ~32% increase in unit costs on a two-year basis.

Finally, at the company's San Jose Mine in Mexico, head grades slid to 181 grams per tonne of silver and 0.85 grams per tonne of gold, respectively, down from 185 grams per tonne of silver and 0.89 grams per tonne of gold in the year-ago period. And while throughput was up slightly, this wasn't able to offset the lower grades. The result was that production fell to a multi-year low of ~1.30 million ounces of silver and ~8,200 ounces of gold, translating to a 5% decline in year-over-year silver output. And with the asset already tracking slightly behind its guidance midpoint of 5.55 million ounces of silver, the recent illegal blockade doesn't inspire much confidence when it comes to meeting this guidance mid-point.

{kind=link}

Recent Developments

Moving over to recent developments, the two positives are the rising gold and silver price, and the fact that Seguela is getting closer to its first gold pour, which is expected by June of this year. The combination of rising metals prices and a high-margin asset being brought online is certainly positive for a company that struggled to generate even $70 million in free cash flow last year (down 20% year-over-year basis). Unfortunately, this has been overshadowed by continued uncertainty at San Jose, with operations currently halted following an illegal blockade in early May by ~15% of the mine and plant workforce, meaning Fortuna's primary silver asset isn't currently benefiting from these high silver prices (at least temporarily).

For those unfamiliar, the Secretaria de Medio Ambiente y Recursos Naturales [SEMARNAT] noted in January that it's re-assessing the 12-year extension of the Environmental Impact Authorization [EIA] which was originally granted in December 2021 related to a typographical error that the correct term was two years, not the 12 years that Fortuna was expecting. Fortunately, San Jose was able to operate operating under the 12-year EIA (permanent injunction from Court to allow Minera Cuzatlan), but the recent illegal blockade has impacted the mine's ability to operate, with no update of a resolution since the May 2nd news release that San Jose's operations were halted.

Fortuna noted that the reason for the illegal blockade was that a small group of workers didn't agree with the estimated amount being distributed to the workforce per the workers' profit sharing entitlement. And while this figure is in line with Mexican legislation, we've seen a history of illegal blockades in the country, with multiple blockades at the Los Filos Mine, and a blockade at Torex's El-Limon Guajes Mine, both in Guerrero. Fortuna noted that the blockaders demanded a higher level of profit-sharing beyond what is stipulated by law, and while Fortuna may not agree here, a raise may be what's needed to ensure no future blockades, impacting a mine that's already suffering from lower grades, declining reserves, and shrinking profitability.

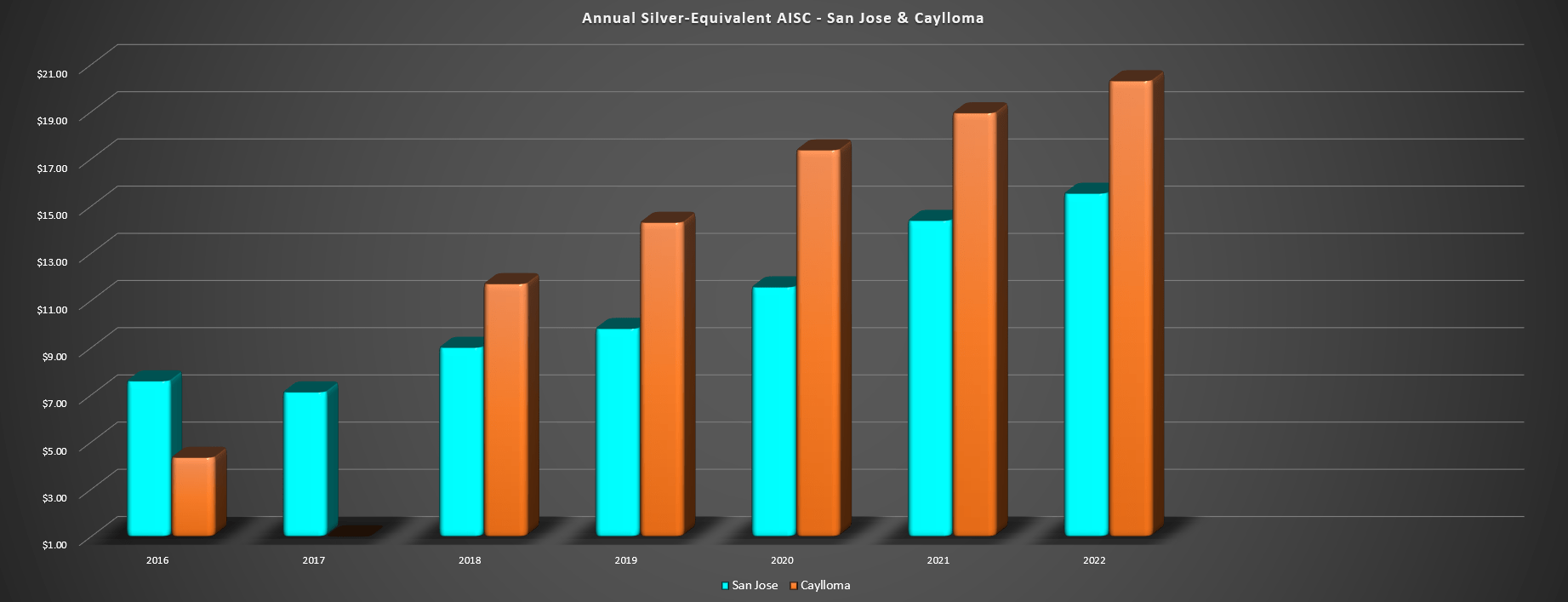

Annual Silver-Equivalent AISC - San Jose & Caylloma (Company Filings, Author's Chart)

{kind=link}

And while the higher silver price will help both San Jose and Caylloma's profitability, we've seen a clear trend in higher costs over the past several years with the impact of lower grades and inflationary pressures. In fact, San Jose is operating at close to $20.00/oz all-in costs while Caylloma's all-in costs are well above $20.00/oz, translating to razor-thin margins in periods of weakness for the silver price. And if we see higher profit-sharing payments as in order to ensure no future illegal blockades at San Jose, this will further affect profitability. In summary, while the rise in silver prices is positive, it's barely making up for the significant rise in operating costs at both assets since 2020.

Plus, as I've discussed in past updates , this unfavorable trend is holding true for its gold assets as well, with Lindero and Yaramoko's costs well above industry average all-in sustaining costs of ~$1,310/oz.

Valuation

Based on ~294 million fully diluted shares and a share price of US$3.95, Fortuna trades at a market cap of $1.16 billion and an enterprise value of $1.30 billion. If we compare this to an estimated net asset value of ~$1.16 billion (which includes exploration upside assigned to Seguela, Boussoura, and Lindero), Fortuna trades at 1.0x P/NAV. At first glance, some might assume this to be a very reasonable multiple, given that most silver producers trade at a premium to net asset value. However, as I've discussed in previous updates, Fortuna's silver production continues to decline as a percentage of total sales and by 2024, it will be a predominantly West African gold producer with a side of silver production from Peru/Mexico, and gold production from Argentina.

Fortuna - Declining Silver Production As Percentage of Total Production (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Given the less favorable jurisdictional profile with Mexico arguably becoming even less attractive than West Africa given the issues at San Jose (permitting, recent illegal blockade), I don't see any reason that Fortuna would trade at a premium to net asset value, especially when higher-margin West African gold producers like Perseus ( PMNXF ) and Endeavour Mining ( EDVMF ) have greater scale and don't even trade at a premium to net asset value. So, based on what I believe to be a more conservative multiple of 0.95x P/NAV and after subtracting out $250 million in corporate G&A, I see a fair value for Fortuna of ~$1.08 billion or US$3.70 per share.

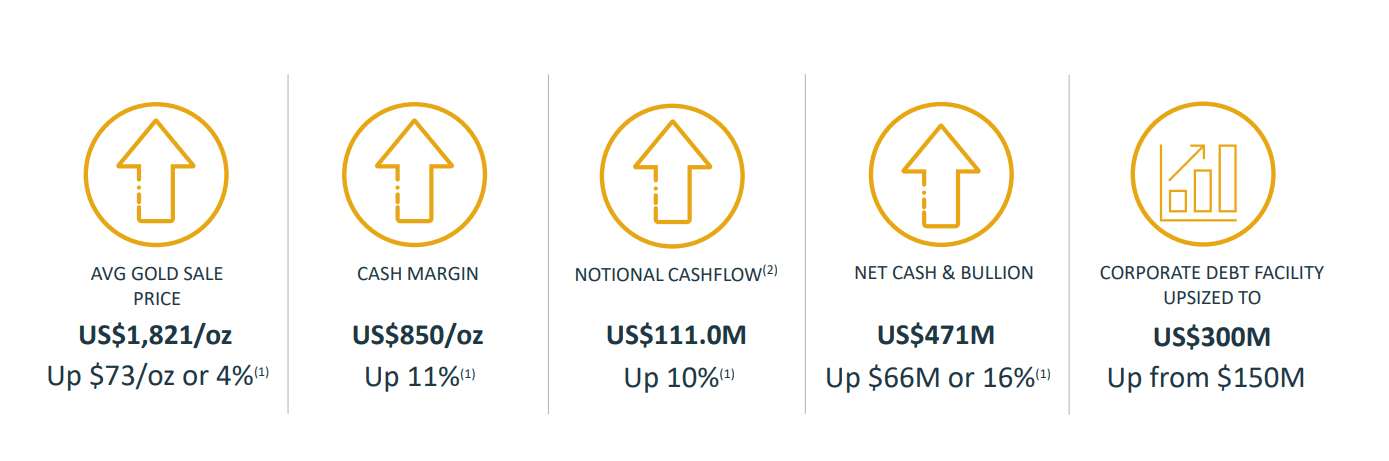

Perseus Mining - Recent Financial Highlights (Perseus Presentation)

{kind=link}

To better illustrate my view of Fortuna's unattractive relative valuation, Perseus Mining trades at an enterprise value of ~$1.50 billion with ~500,000 ounces of annual gold production at sub $1,000/oz AISC and a path to 550,000+ ounces at sub $950/oz AISC with Block 14. Meanwhile, even with Seguela at full production, I would expect Fortuna's AISC to remain above $1,250/oz from a consolidated standpoint, with Yaramoko, Lindero, San Jose and Caylloma more than offsetting the sub $900/oz AISC at Seguela. So, with Fortuna being a smaller and higher-cost miner with a weaker balance sheet (~$140 million in net debt vs. Perseus' ~$470 million in net cash while paying dividends), I don't see any reason both companies should have similar valuations.

In summary, I see no margin of safety at current levels for FSM, and I struggle to see how Fortuna will outperform its peer group when we have continued uncertainty at San Jose, a less favorable outlook for mining in Burkina Faso because of security issues (Boussoura, Yaramoko), and a continued hyper-inflationary environment in Argentina. To summarize, I do not see Fortuna Silver as investable, and with the stock over 90% off its Q3 2022 levels, I don't see the stock as attractive from a swing-trading standpoint either. So, if the stock were to see further strength as investors await the first gold pour from Seguela, I would view any rallies above US$4.20 before July as profit-taking opportunities.

Summary

Fortuna Silver may look cheap as a ~350,000 plus ounce per annum producer with a ~$1.3 billion enterprise value, given that some producers of this size trade at market caps north of $2.0 billion. However, I would argue that Fortuna is an apple or oranges comparison with most of its peers, with short mine lives at Yaramoko and San Jose, an unattractive cost profile for its current assets, and continued challenges at San Jose between trying to solve permitting dispute with SEMARNAT and now working to solve an illegal blockade related to a small portion of union employees. And while Seguela will be a cash cow in Cote d'Ivoire, I see this as one of the few redeeming qualities and one mine can only justify so much in fair value.

If Seguela were in a Tier-1 jurisdiction, one could make the argument that this would solve the issues and help the stock command a premium multiple. However, as we've seen with Perseus Mining and Endeavour Mining, that have even more impressive assets in Yaoure and Sabodala-Massawa which both have AISC below $800/oz and larger production profiles, these assets aren't enough to justify a premium valuation, and West African producers typically trade at sub 0.90x P/NAV regardless of the quality of their assets. To summarize, I continue to see FSM as fully valued. So, while a rising tide will lift all boats, I don't see any margin of safety at current levels.

For further details see:

Fortuna Silver: Seguela Doesn't Fix Rising Costs At Existing Assets