CA - Fortuna Silver: Significant Margin Expansion In Q3

2023-12-08 16:40:03 ET

Summary

- Fortuna Silver has rallied over 50% since reaching a low of US$2.60, outperforming the sector after a strong Q3 report.

- The company's Seguela Mine performed well, offsetting rising costs at other operations.

- In this update, we'll dig into the Q3 results, the stock's updated valuation, and whether it's time to consider taking some profits.

Just over three months ago, I wrote on Fortuna Silver Mines ( FSM ), noting that while the stock might see further downside given the pinched margins for its San Jose Mine (rising Peso), the stock would become much more interesting below US$2.60. Since touching this level, the stock has rallied over 50% to outperform the sector after what's been a brutal two years of share-price performance for investors following its Roxgold acquisition. The outperformance relative to peers can be attributed to a solid Q3 report with its Seguela Mine performing as planned, offsetting rising costs at legacy operations like San Jose, Caylloma, and Lindero. In this update, we'll dig into the Q3 results, the stock's updated valuation, and whether it's time to consider taking some profits.

San Jose Mine Operations - Company Website

{kind=link}

Q3 Production & Sales

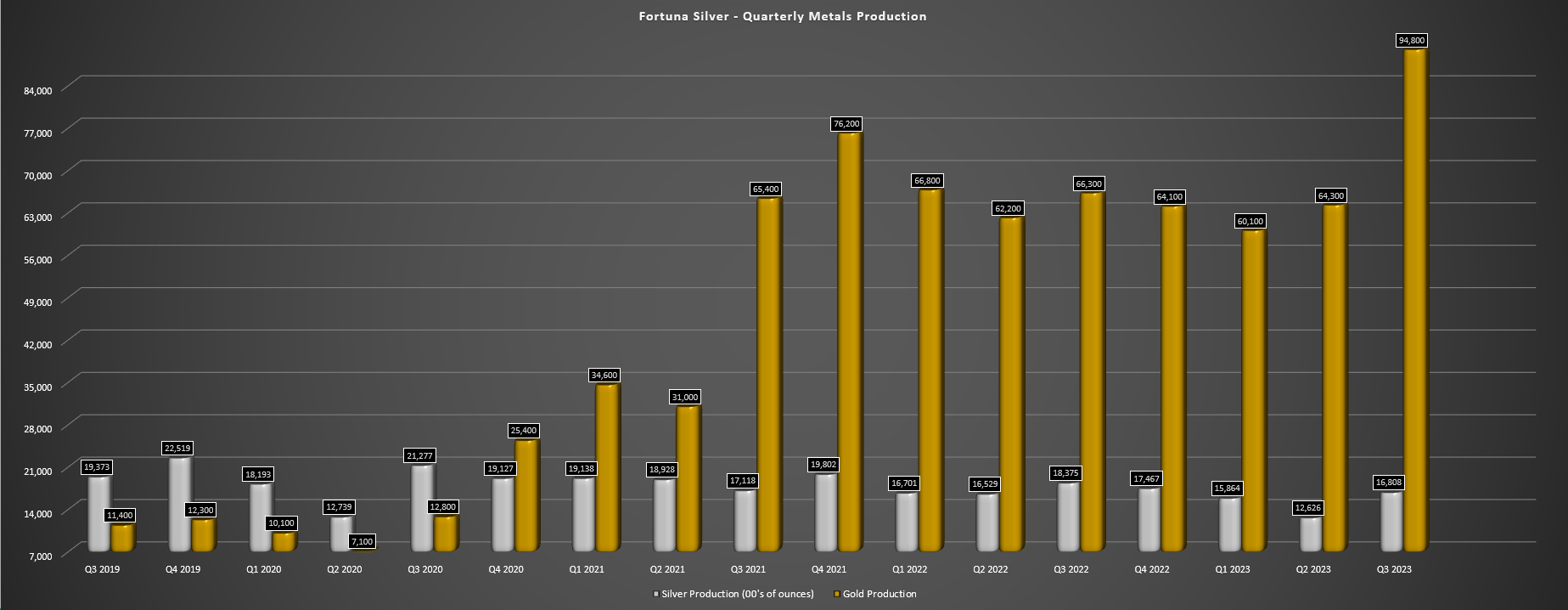

Fortuna Silver ("Fortuna") released its Q3 results last month, reporting quarterly production of ~94,800 ounces of gold and ~1.68 million ounces of silver. This translated to a significant increase in gold production (+43%) partially offset by a nearly 9% decline in silver production, but much higher gold-equivalent ounce [GEO] production overall. The primary driver for this increased production was the start of production from the company's new Seguela Mine in Cote d'Ivoire, offsetting a softer quarter at Lindero (lower grades), and lower gold production at San Jose (lower grades and throughput). However, the company's Yaramoko Mine also performed well and bounced back from weaker grades in the year-ago period (~7.7 vs. ~6.2 grams per tonne of gold), producing ~34,000 ounces to push Fortuna's gold production to just shy of 100,000 ounces.

Fortuna Silver - Quarterly Metals Production - Company Filings, Author's Chart

{kind=link}

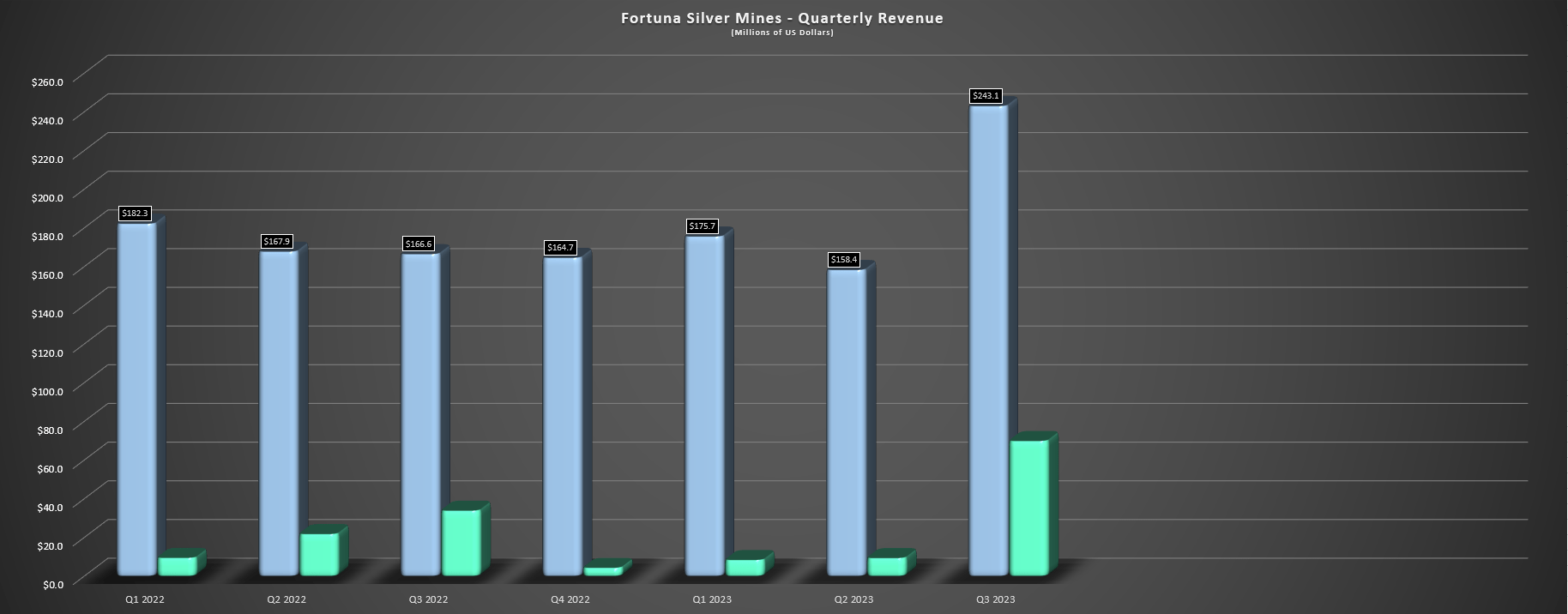

This sharp increase in production was conveniently coupled with a much stronger average realized gold price in Q3-23 of $1,925/oz (Q3-22: $1,718/oz), and silver prices also improve to $23.70, helping the company to report record revenue of $243.1 million, a 46% increase from the year-ago period. The higher sales combined with higher margins from its new Seguela Mine translated to operating cash flow of $106.5 million, free cash flow of $70.0 million, and allowed the company to pay down $40 million of debt on its RCF in the period, ending the quarter with ~$133 million in net debt and ~$118 million in cash, with the ability to further reduce debt over the coming quarters with a newly producing cash-flow machine in Cote d'Ivoire.

Fortuna - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Costs & Margins

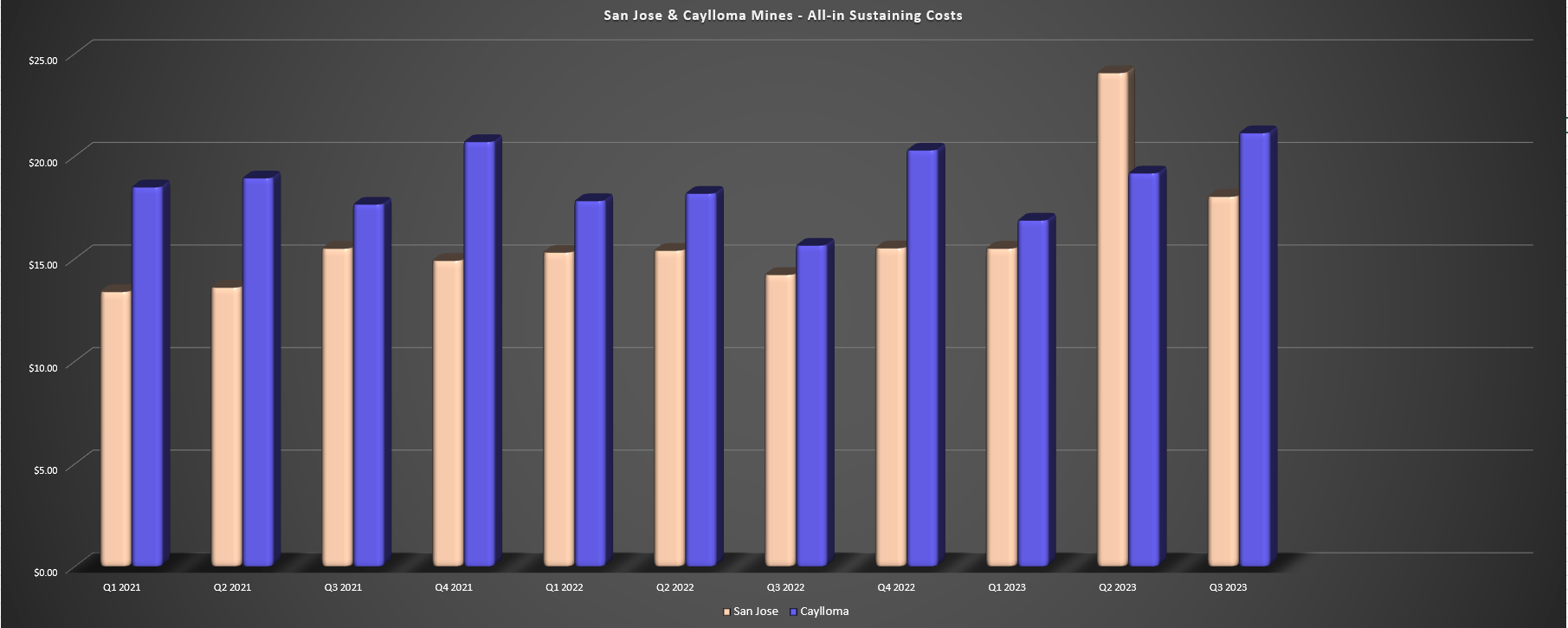

Moving over to costs and margins, we didn't see any improvement in the silver segment, with all-in sustaining costs [AISC] for San Jose and Caylloma of $18.04/oz and $15.66/oz, respectively. This was partially because of the strength in the Mexican Peso, which has continued to negatively impact costs at the company's San Jose Mine in Mexico, and lower sales at Caylloma. The result was that AISC margins at these two assets came in at $5.61/oz and $2.79/oz, respectively (per silver-equivalent ounce), which were well below the industry average. That said, Fortuna reported a significant improvement in its consolidated all-in sustaining costs per gold-equivalent ounce with the benefit of its high-margin Seguela Mine.

San Jose & Caylloma Mines - Company Filings, Author's Chart

{kind=link}

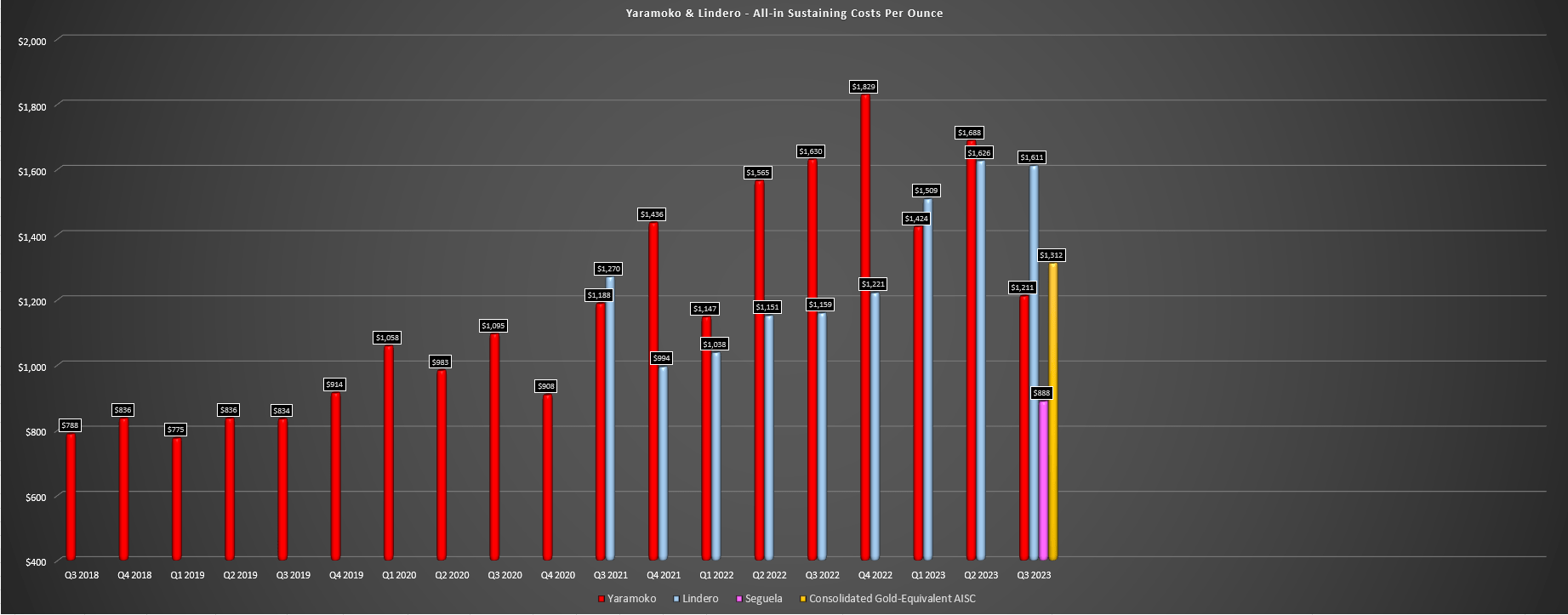

Looking at the company's gold operations below and its consolidated AISC per GEO, we can see that despite Lindero's elevated AISC of $1,611/oz, Fortuna's company-wide AISC came in at $1,312/oz. This represented a significant improvement from $1,431/oz in the year-ago period, helped by a better quarter at Yaramoko ($1,211/oz with the benefit of higher grades), and ultra-low costs of $788/oz at Seguela. And when combined with a higher gold price of $1,925/oz, this translated to AISC margins surging to $613/oz vs. $287/oz in the year-ago period and the ability to generate $70 million in free cash flow, trouncing most of its peers. In addition, management shared that Seguela operated at 174 tonnes per hour in September and 162 tonnes per hour in Q3, suggesting the potential to beat its nameplate capacity, a positive sign.

Fortuna - Yaramoko, Lindero, Seguela & Consolidated AISC - Company Filings, Author's Chart

{kind=link}

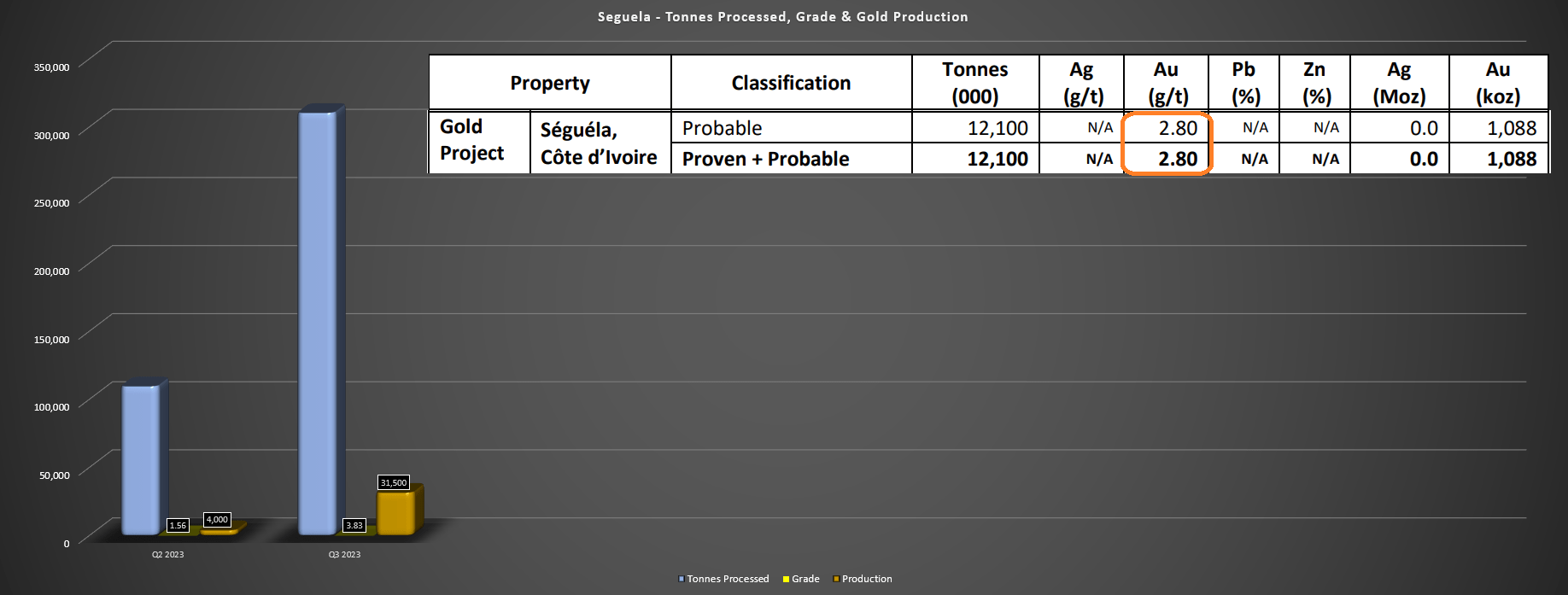

That said, it's important not to extrapolate these results annually because this was an unusual quarter for Seguela that helped to drive its AISC well below expectations. For starters, the company was processing an average grade that was 37% above the reserve grade (3.83 grams per tonne of gold vs. 2.80 grams per tonne of gold). Second, all-in sustaining costs benefited from ~35,500 ounces being sold vs. ~31,500 ounces produced, with actual AISC on ounces produced being closer to $888/oz. Third, the company benefited from mining the deposit closest to the plant (Antenna is directly northeast of the plant) and a lower strip ratio, with the life-of-mine strip ratio closer to 13.9/1.0 vs. below 2.4 to 1.0 in the period. In fact, the next deposit to be mined may be higher grade, but it's ~6 kilometers from the plant and carries an ~18/1.0 strip ratio, suggesting that AISC should drift above $1,000/oz.

Seguela Mine Operating Metrics & Reserve Grade - Company Filings, Author's Chart & 2021 TR

{kind=link}

This is not intended to take away from the phenomenal performance at Seguela and the team has done a great job of getting this asset built on time, on budget, and ramping it up successfully. However, with no income taxes paid from offsets in the construction period, which benefited Fortuna's effective tax rate (Q3-23: 17.6%), higher strip ounces, more normalized grades at Seguela and Yaramoko, I don't expect AISC to sit near these levels on an annualized basis in 2024/2025 and I would not expect the company to generate similar levels of free cash flow on an annualized basis (~$280+ million) without significantly higher metals prices. Hence, while this was a great quarter, and certainly helped with debt repayment, this doesn't change the overall profile, which is Fortuna being an average cost producer company-wide in less favorable jurisdictions and with a very short mine life at its primary silver asset.

Recent Developments

As for recent developments, investors can breathe a sigh of relief for the EIA at San Jose, with previous worries about the Secretaria de Medio Ambiente y Recursos Naturales' [SEMARNAT] reassessment of the 12-year extension in the rear-view mirror. This is because the Mexican Federal Administrative Court ruled in favor of Fortuna and reinstated the 12-year EIA in late October. That said, and as I have noted in past updates, I would be more worried about the ability to replace reserves here with consistently rising production costs ($97.30/tonne year-to-date vs. $77.60/tonne last year). On a negative note, Burkina Faso's mining code has been revised, with a 1.5% increase in the royalty between $1,700/oz to $2,000/oz (6.5%) and a 7% royalty above $2,000/oz. Fortunately, the company has only one operation in Burkina Faso (Yaramoko) and it's also one of its shorter life assets, so while this could affect profitability slightly, this would be a far worse development if it was on Seguela or Lindero.

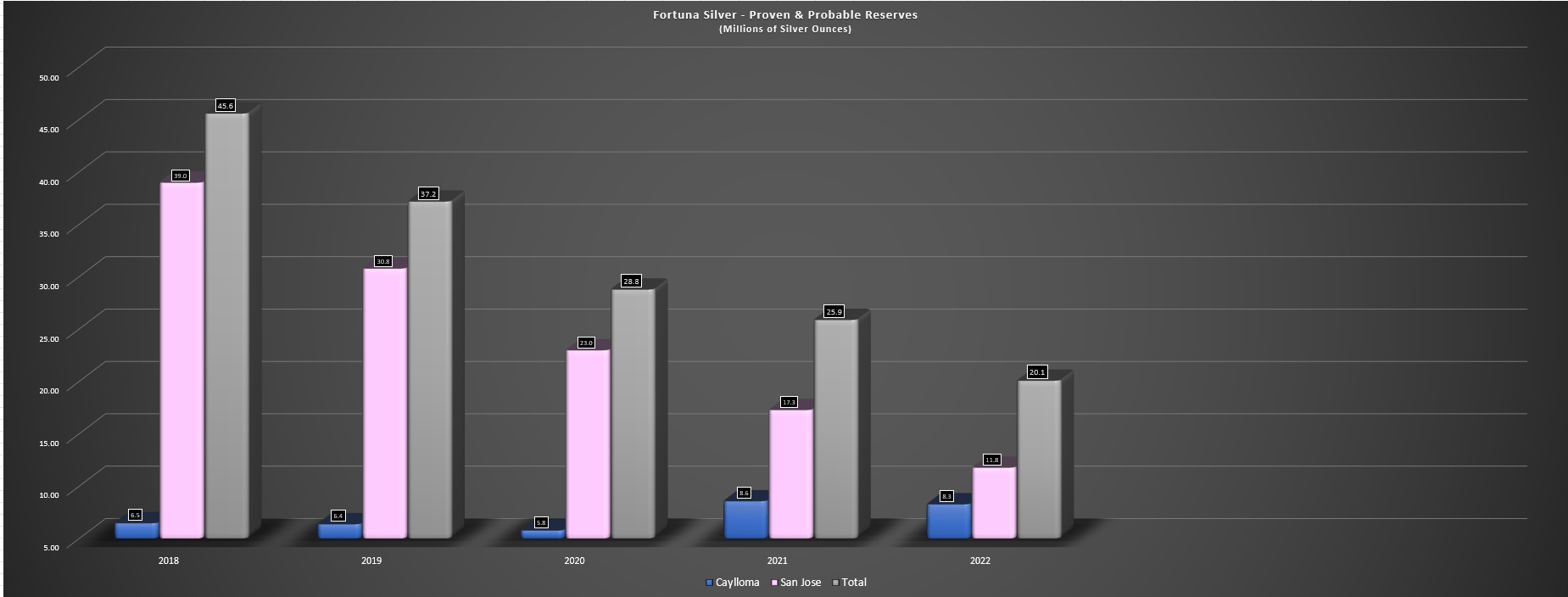

Fortuna Silver - Annual Silver Reserves (San Jose/Caylloma/Total) - Company Filings, Author's Chart

{kind=link}

Last but not least, Fortuna noted it made a new discovery of the Yessi vein, which is a blind structure just 200 meters laterally from its existing infrastructure at San Jose. Early results are encouraging, with a highlight intercept of 9.9 meters at ~1,300 grams per tonne silver-equivalent and 5 meters at ~620 grams per tonne silver-equivalent. That said, the key will be expanding on this new discovery and it's far too early to tell if this will move the needle in terms of adding to the mine plan. For now, I think it's safer to assume that San Jose winds down in 2026, given that it has just ~2.1 million tonnes of material (June 2022), has been losing over 400,000 tonnes per annum to depletion, and the outlook for adding reserves is poor with an unfavorable combination of a strong Peso and sticky inflationary pressures.

Valuation

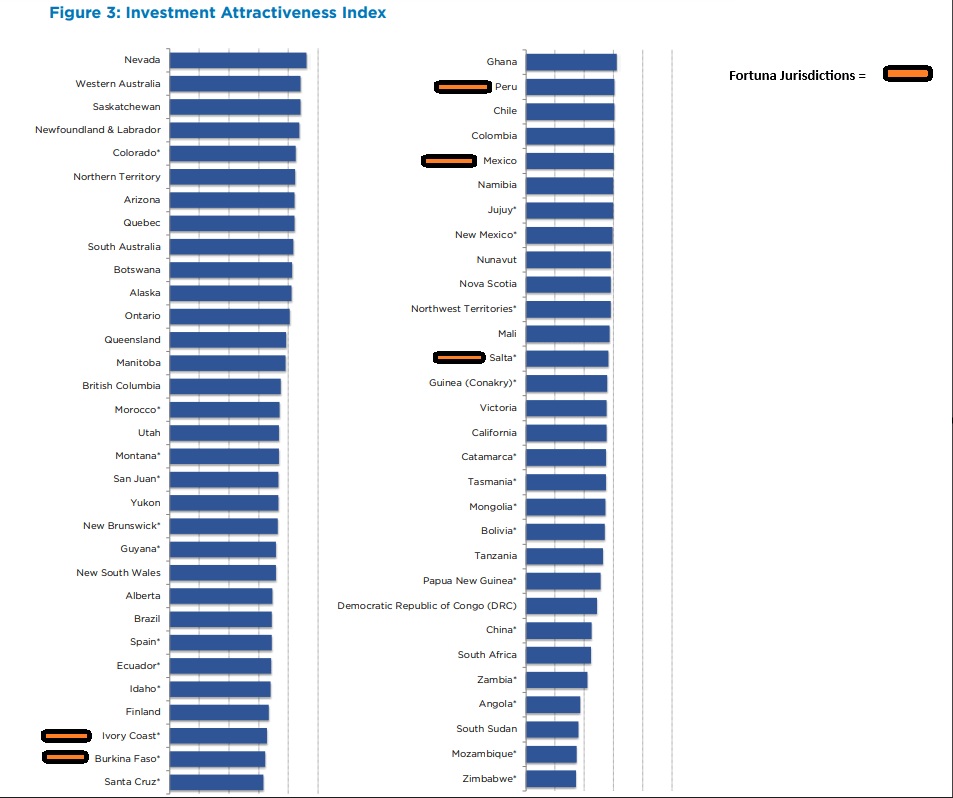

Based on ~310 million fully diluted shares and a share price of US$3.80, Fortuna trades at a market cap of ~$1.18 billion and an enterprise value of ~$1.31 billion. This leaves Fortuna trading at a premium to its estimated net asset value of ~$1.02 billion (5% discount rate for San Jose, Caylloma, Lindero / 7% discount rate for West African assets). To put this in perspective, peers with assets in Tier-1 jurisdictions like SSR Mining ( SSRM ) trade at ~0.65x and names like B2Gold ( BTG ) that also have assets in Tier-1 jurisdictions (but with the bulk of production from Mali) at just ~0.80x P/NAV, but Fortuna has a much smaller scale. In fact, Fortuna's P/NAV multiple of ~1.13x is in line with Agnico Eagle ( AEM ), which has over 90% of NAV in Tier-1 ranked jurisdictions (Canada, Finland, Australia), is the world's third largest gold producer, and one that has the best track record of per share growth over the past two decades couple with industry-leading margins. In summary, the recent rally in FSM has severely affected its relative value compared to peers.

Fortuna Mining Jurisdictions - Fraser Institute Investment Attractiveness Index

{kind=link}

So, what's a fair value for the stock?

Using what I believe to be a more conservative multiple of 5.5x forward cash flow given its significant exposure to West Africa and 1.0x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see an updated fair value for Fortuna of US$5.00. However, I am looking for a minimum 40% discount to fair value to justify owning small-cap producers based out of Tier-2/Tier-3 ranked jurisdictions (Mexico, West Africa, Argentina, Peru) and with no Tier-1 exposure. If we apply this discount to ensure an adequate margin of safety, the ideal buy zone for the stock comes in at US$3.00 or lower. Hence, I don't see nearly enough margin of safety at current levels despite the improving free cash flow profile.

Summary

Fortuna Silver has outperformed the sector over the past two months after another a huge quarter out of Seguela, but it's important to note that this will be an abnormal year for the asset with the benefit of above-average grades, lower strip, and mining right next to the plant (besides the benefit no income taxes paid in the most recent quarter vs. 35-40% at full income tax rates). Meanwhile, the outlook for growing reserves at its silver business is not great even if the 12-year EIA at San Jose has been reinstated, and it would be hard to justify a 1.0x P/NAV multiple without the silver premium at San Jose. In summary, I see far more attractive bets elsewhere in the sector, and I would view any rallies above US$4.19 before February as an opportunity to book some profits. One name still trading at a deep discount to fair value is Argonaut Gold ( ARNGF ), trading at ~0.30x P/NAV with Tier-1 jurisdictions operations and less than 1.5x FY2024 P/CF estimates.

For further details see:

Fortuna Silver: Significant Margin Expansion In Q3