CA - Franco-Nevada Corporation: A Softer Q2 Due To Lapping Tough Comps

2023-08-14 15:17:02 ET

Summary

- Franco-Nevada Gold's Q2 results were softer than some might have hoped with lower revenue and GEO sales, suggesting a likely miss on its FY2023 guidance midpoint.

- The main culprit for the softness was Franco-Nevada's energy segment, which saw a major decline in revenue due to weaker energy prices despite the one-time benefit of catch-up payments.

- In this update, we'll look at whether the stock offering enough margin of safety given relatively low growth rates, and how it's positioned after lapping tough Q2 2022 comps.

Just over five months ago, I wrote on Franco-Nevada Corporation ( FNV ), noting that while the company had put up a solid Q4 and was the premier way to get precious metals exposure, it had tough sledding ahead with comps that would be difficult to lap from Q2 2022. This is because the company benefited from outsized strength in its energy segment in Q2 2022, with realized prices of $108.41/barrel for WTI and $7.49/mcf for Henry Hub Natural Gas. This meant that precious metals were going to need to surge to pick up some slack given that attributable production and sales weren't expected to increase materially with Salares Norte pushed out to late 2023 vs. early 2023 previously. And this outlook of tough comps didn't even take into consideration much lower palladium ( PALL ) prices, which would be an additional headwind.

Since this update, FNV has suffered a 4% correction, reported softer revenue and cash flow on a year-over-year basis, and noted that total GEOs could come in at the low end of its guidance range. And while it's outperformed the Gold Miners Index ( GDX ), it's underperformed some of my favorite ideas like Capri Holdings ( CPRI ) which was purchased at $38.00, Pan American Silver ( PAAS ) purchased at US$14.60, and Wesdome Mines ( WDOFF ) purchased at US$4.60. And while the recent correction ahead of an 18-month period with several construction-stage mines pouring their first gold is certainly an attractive setup for owning Franco-Nevada Gold, it's tough to argue that an adequate margin of safety is present just yet. Let's inspect the Q2 results below and how it's positioned after lapping two quarters of tough comps.

{kind=link}

Cobre Panama Operations - First Quantum Minerals Website

Q2 Results

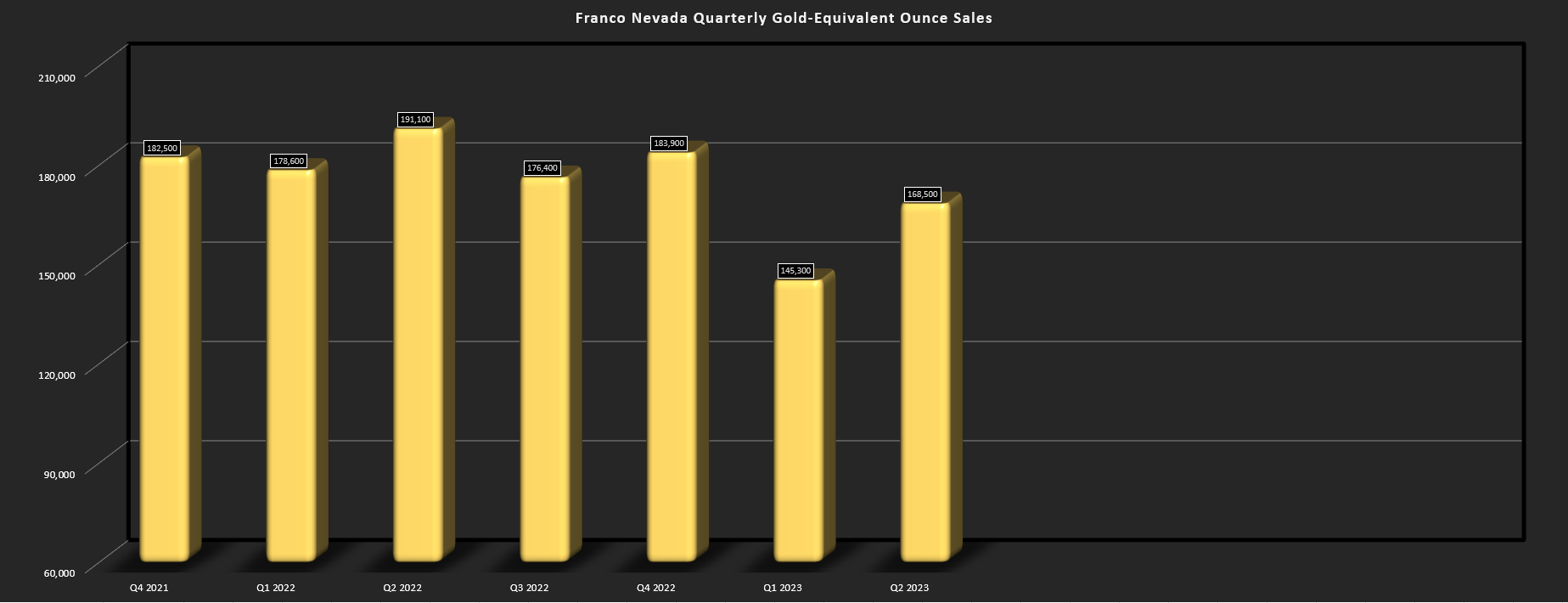

Franco-Nevada reported its Q2 results earlier this month, reporting quarterly sales of ~168,500 gold-equivalent ounces [GEOs], a 12% decline from the year-ago period. On a half-year basis, the numbers were even lower due to the disruptions at Cobre Panama and Antapaccay in Q1, with H1 2023 sales of ~243,300 GEOs, a 7% decline year-over-year. This has resulted in Franco-Nevada tracking well behind its initial FY2023 guidance of 640,000 to 700,000 GEOs, with attributable sales sitting at just ~36.3% of its guidance mid-point, albeit with a strong H2 on deck. Outside of the sharp decline in GEOs from its energy segment due to weaker energy prices, the company saw lower revenue from several assets, including Antamina (impact from Cyclone Yaku), Guadalupe-Palmarejo (lower production and less production on streaming ground), Detour Lake (lower grades not quite offset by record throughput), and lower contribution from its iron ore segment, with lagging sales vs. production at its Vale ( VALE ) royalty and wildfires that impacted production at LIORC (Iron Ore Company of Canada).

{kind=link}

Franco-Nevada - Quarterly GEO Sales (Company Filings, Author's Chart)

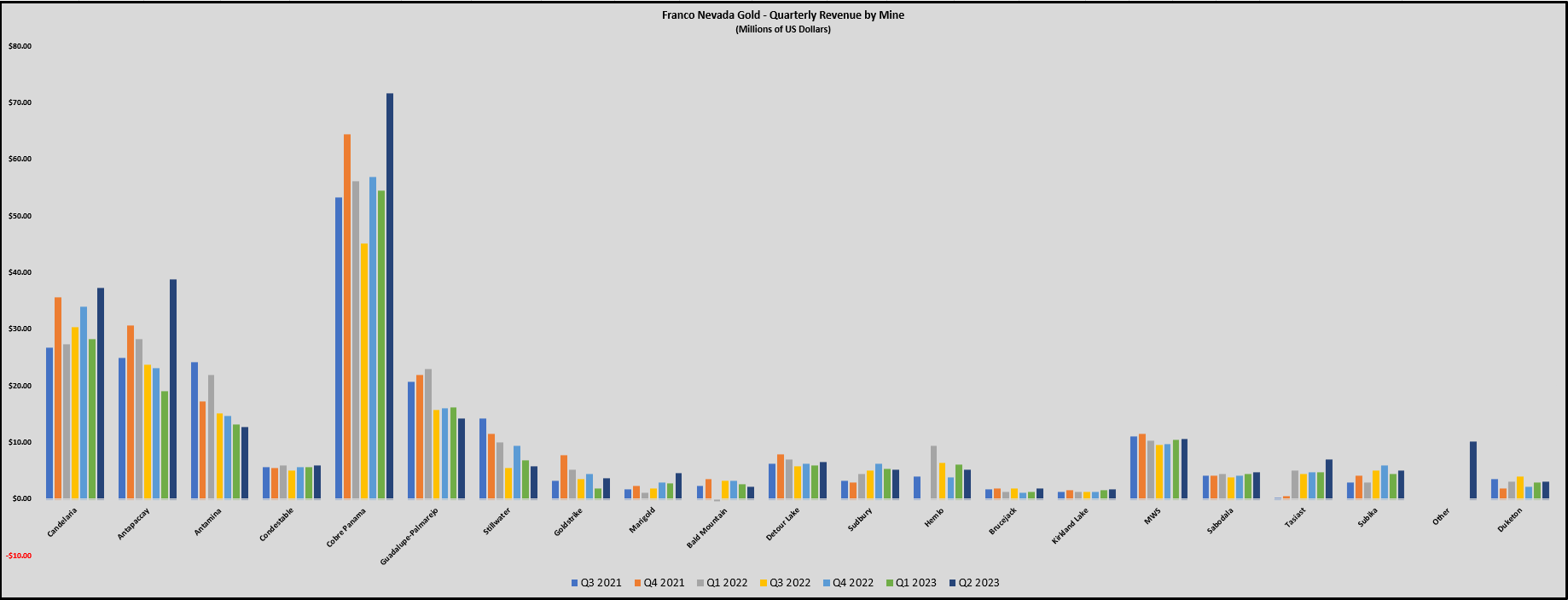

Fortunately, there were some offsets in the precious metals portfolio, and H2 is expected to be much better. For starters, Cobre Panama had a better quarter (~$71.7 million in revenue) with operations returning to normal after the dispute in Q1 between the Panamanian Government and First Quantum Minerals ( OTCPK:FQVLF ). Importantly, investors can breathe a sigh of relief with a Refreshed Concessior Contract signed on June 26 between the two parties. Meanwhile, Antapaccay bounced back in the period to report $38.8 million in revenue, Tasiast benefited from higher production with the 24K Expansion complete with ramp-up underway ($7.0 million in revenue), and Subika and Marigold also contributed more in the period. That said, when all was balanced out across the precious metals portfolio and a further negative impact from lower palladium prices at Stillwater, precious metals GEOs were roughly flat year-over-year at ~132,000, up just 0.3%.

{kind=link}

Franco-Nevada: Quarterly Revenue by Mine (Company Filings, Author's Chart)

{kind=link}

Franco-Nevada - Quarterly Revenue & Energy-Related Revenue (Company Filings, Author's Chart)

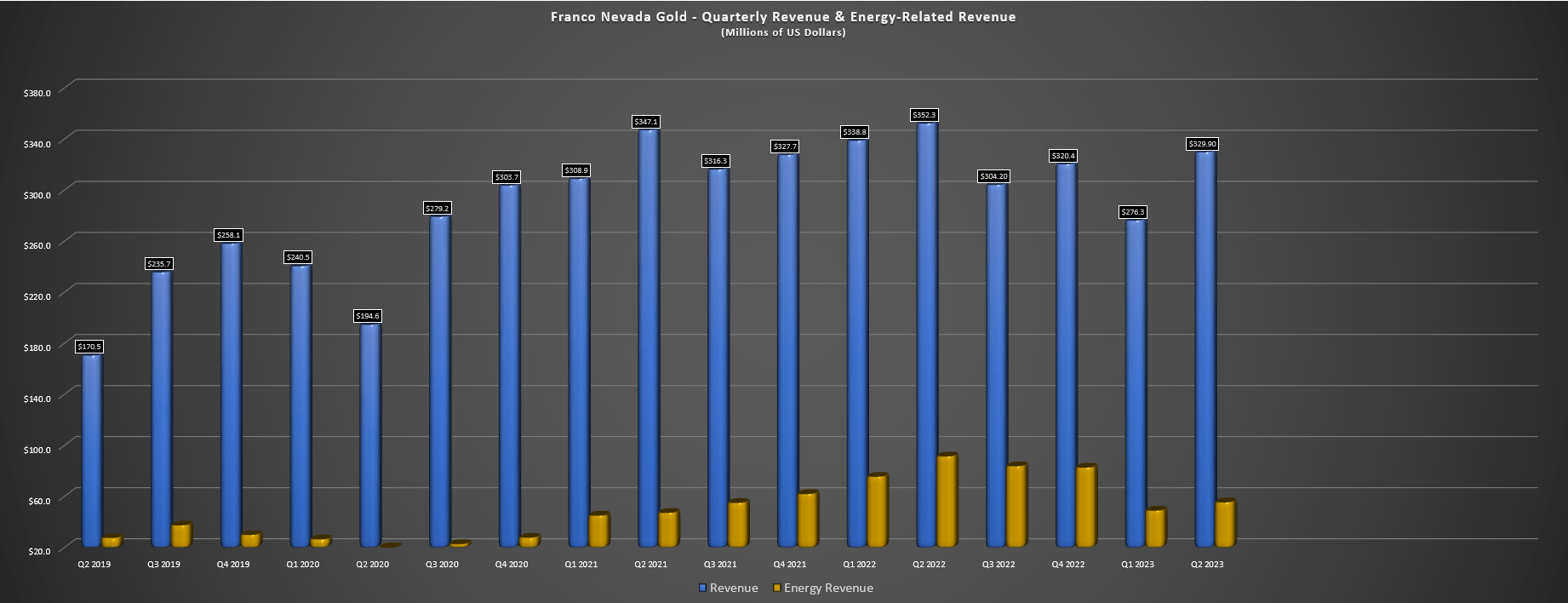

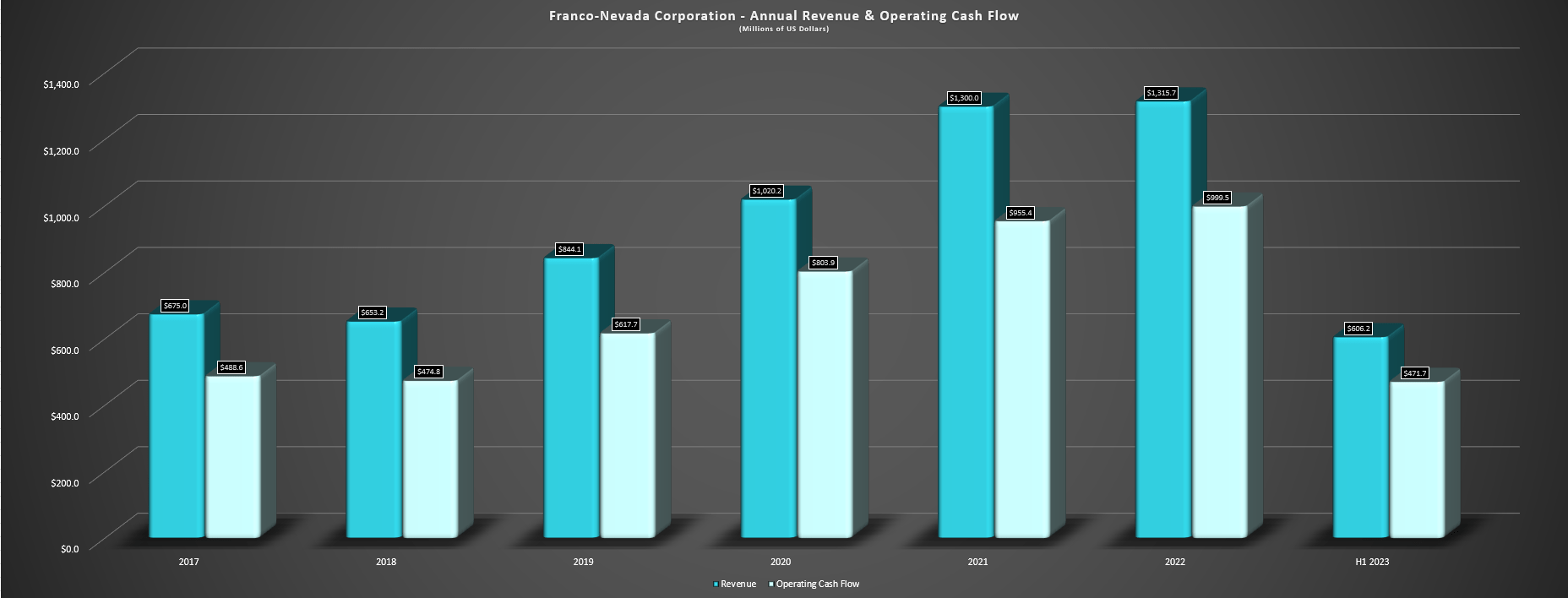

As for the energy segment, this is where we saw the major decline, and this shouldn't be surprising given that energy prices were going to need to remain at elevated levels to lap the tough Q2 2022 comparisons. As we can see below, oil and gas prices did not manage to hold the gains, with revenue from this segment plunging to $55.5 million (Q2 2022: $91.5 million) despite a $7.0 million one-time catch-up benefit in the period from new wells at its Permian assets. The result of this sharp decline in its energy segment was that Franco-Nevada's total revenue slipped to $329.9 million in Q2 (down 6% year-over-year), while H1 2023 revenue fell 12% year-over-year to $606.2 million. Meanwhile, operating cash flow also fell sharply in H1 2023 vs. H1 2022 despite the benefit of higher realized metals prices, with year-to-date operating cash flow coming in at $471.7 million (H1 2022: $487.9 million).

{kind=link}

Franco-Nevada - Annual Revenue & Operating Cash Flow vs. H1 2023 (Company Filings, Author's Chart)

Not surprisingly, Franco-Nevada has commented on guidance, noting that it expects to come in at the lower end of its guidance range this year, which is certainly evident from its H1 2023 results relative to its guidance range. That said, there is some positive news worth pointing out, and while the H1 and Q2 results were disappointing, this was largely due to factors outside of its control (Cobre Panama dispute, lower oil, natural gas, palladium, and iron ore prices), so the guidance miss is hardly anything to lose any sleep over for investors. And the good news is that the full ramp up of the CP-100 Expansion (100 million tonnes per annum) is set to be completed by year-end, pushing annual attributable sales from this one asset alone closer to ~150,000 GEOs.

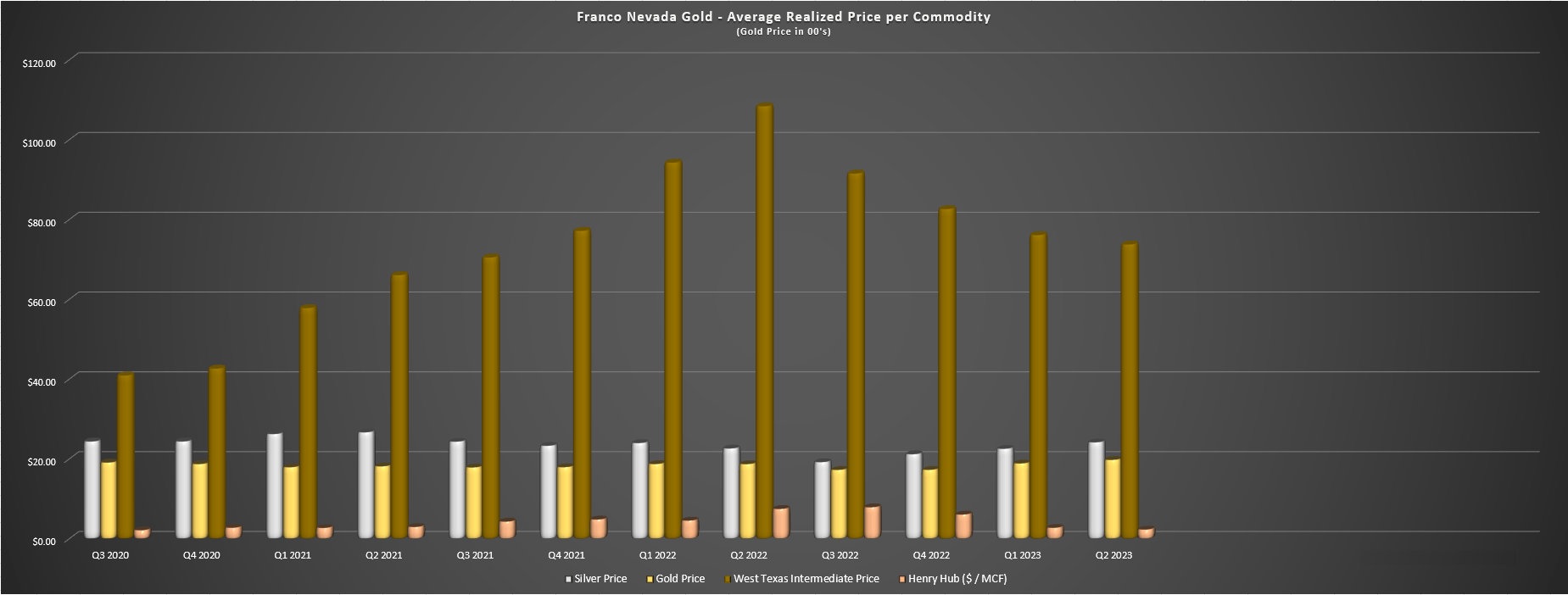

Meanwhile, two new assets poured their first gold recently (Seguela and Magino), and will begin to contribute more meaningfully in H2 of this year as they ramp up to commercial production. Plus, from a positioning standpoint, Franco-Nevada has now lapped some of the difficult comps that it had in place coming into this year, with the Q3 2022 average realized WTI price being $91.56/barrel, an easier figure to lap than the $108.41/barrel in Q2 2022. That said, palladium prices will remain a headwind (Q3 2022: $2,074/oz), as will Henry Hub Natural Gas prices (Q3 2022: $7.91/mcf), partially offsetting the benefit of much easier comps for gold and silver, which both were sitting below $1,800/oz and $20.00/oz, respectively, in Q3 2022.

{kind=link}

Franco-Nevada - Average Realized Price per Commodity (Company Filings, Author's Chart)

Given this setup of higher H2 production but mixed comparisons in Q3 2022, Franco-Nevada may be better positioned than it was in Q2 2023 when it had to lap near insurmountable comps, but the better setup will come in Q4 2023 when its average realized prices on a comparative basis drop to levels that are easier to lap with these being $21.20/oz for silver, $1,729/oz for gold, $82.65/barrel for WTI, and $6.09/mcf for natural gas. And at the same time, Franco-Nevada will benefit from higher production from smaller assets like Seguela and Magino and improved production levels from Cobre Panama with the CP-100 ramp-up nearly complete. And on a positive note, we will likely see the opposite set in H1 2024 for Franco-Nevada, with the company now having relatively easy comps to lap with multiple new assets coming online and weaker energy prices, and especially for its energy segment and Stillwater [PGM asset].

Recent Developments

As for recent developments, we haven't seen any major acquisitions by Franco-Nevada, but they did fund an additional $93.0 million of its $250.0 million total stream deposit at Tocantinzinho ($183.8 million funded to date), and construction at this asset is 27% complete with first pour on schedule for H2-2024. For those unfamiliar, Franco-Nevada has a massive 12.5% gold stream to start (albeit with a step-down) at this asset, translating to an average of ~22,500 GEOs in the first five years of production (2025-2029) at a cost of just 20% of the spot gold price (~$390/oz). Meanwhile, several assets remain on track for their first gold pours in the next 18 months, including Salares Norte (1-2% NSR), Valentine (3.0% NSR), Greenstone (3% NSR), Posse (1% NSR), Red Mountain (1% NSR), and we'll also see higher production from the Sabodala-Massawa Expansion Project.

{kind=link}

Tocantinzinho Construction Progress - G Mining Ventures Presentation

And as for recent deals, Franco-Nevada made the surprising move to acquire a sliding scale royalty (2.70% NSR on gold and 0.54% NSR on copper) on the Chilean side of the massive Pascua-Lama Project, a sleeper asset that doesn't yet have a planned start date. At the price paid of $75.0 million, this could certainly pay off nicely over the long-term, but the company may have to sit on this for a few years given that the operator has a busy development pipeline as it stands with two major projects planned, including Reko Diq and the possibility of a Super Pit at Lumwana. Elsewhere, the company acquired a 1.5% NSR on the Volcan Project in Chile (it currently holds an existing 1.5% NSR of the Ojo de Agua area), increased its Caserones royalty by 0.11% to make it a total of a 0.75% effective NSR, and it doubled its royalty on the Valentine Project in Newfoundland, a vote of confidence in the favor of this construction-stage asset.

Despite these recent developments with over $140 million in royalty acquisitions in the period, Franco-Nevada ended the quarter with one of the sector's strongest balance sheets, sitting on ~$1.3 billion in cash, no debt, and a total of ~$2.3 billion in liquidity. This gives the company the flexibility to bid on large and small assets across the sector if attractive opportunities come across the plate. And with companies like Triple Flag ( TFPM ) and Franco-Nevada willing to bid on smaller assets, this has certainly created a difficult environment for names like Gold Royalty Corp. ( GROY ) and Metalla ( MTA ) which have higher costs of capital and are seeing competition even from the majors which are able to out-bid them to secure future growth on the best assets, making it harder for Gold Royalty and Metalla to compete. That said, the whole royalty/streaming sector has a tailwind from the current environment (high rates, limited appetite for equity), and Franco-Nevada will be in even better shape if it can nail down a couple of major deals in this period.

Valuation

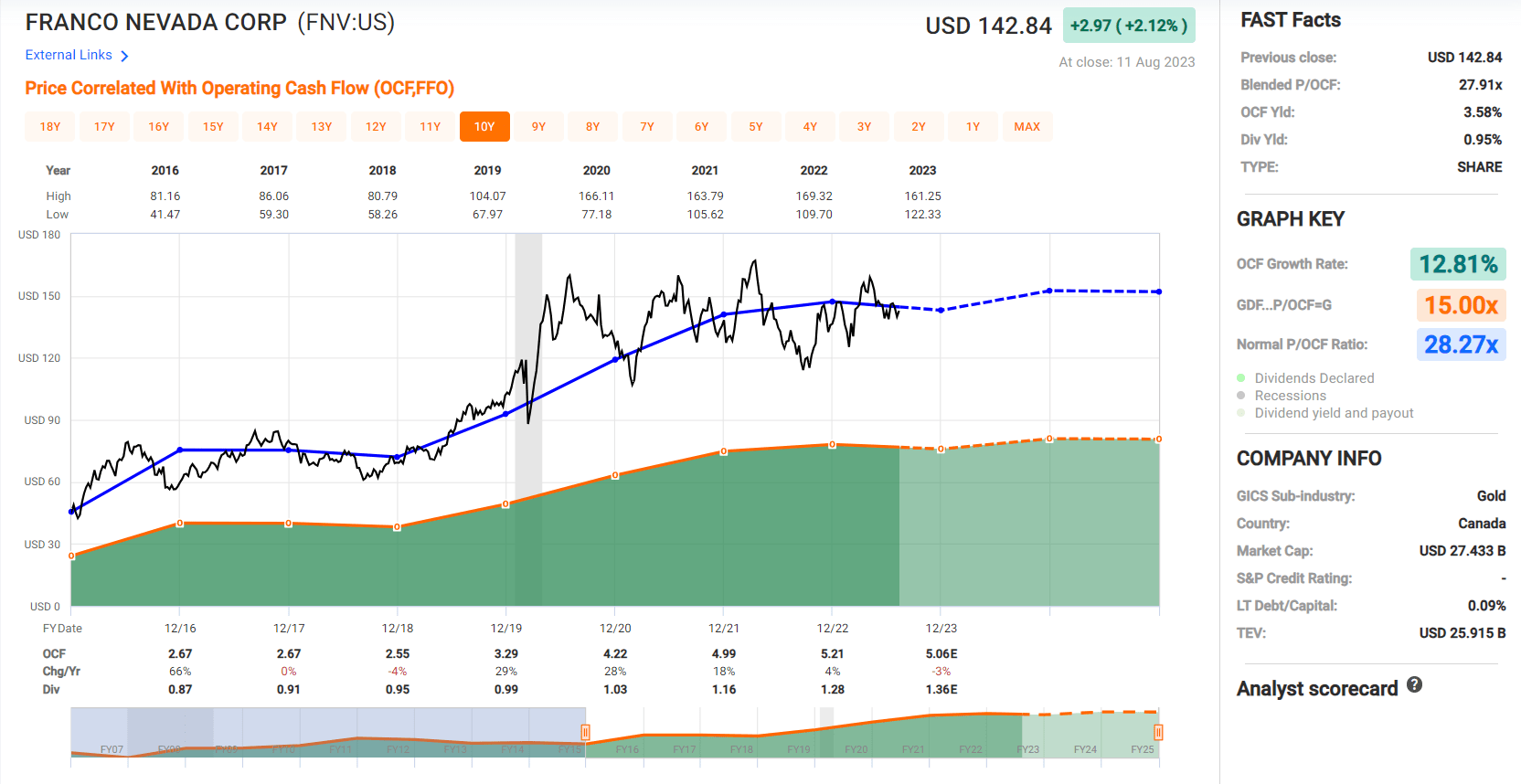

Based on ~192 million shares and a share price of US$142.80, Franco-Nevada trades at a market cap of ~$27.4 billion and an enterprise value of ~$26.1 billion. This continues to earn it a spot among the top-3 largest precious metals companies by market cap, and for good reason, with the company having an incredible portfolio of 116 producing assets (47 precious metals), over a dozen new assets set to move into production over the next few years, and 428 total assets, superior position from a diversification standpoint to Wheaton Precious Metals ( WPM ). That said, while the company has earned itself a premium multiple for its diversification, focus on world-class assets with well-capitalized operators and its low-risk and inflation-protected business model, the stock still doesn't offer nearly the margin of safety I would like to see to justify starting a new position, with it trading at ~25.0x FY2024 cash flow per share estimates ($5.70).

{kind=link}

Franco-Nevada - Historical Cash Flow Multiple (FASTGraphs.com)

If we look at the above chart, this might appear to be a very reasonable valuation, with FNV historically trading at ~28.3x cash flow (10-year average), below its current forward multiple. And I would argue that a fair value for the stock is 30.0x cash flow given that it offers unrivaled diversification and has its tentacles in nearly every world-class asset in the precious metals space. However, even at 30.0x forward cash flow estimates, the stock's fair value comes in at US$171.00, and I require a minimum 25% discount to fair value to justify starting new positions. If we apply this discount to its estimated fair value of US$171.00, the ideal buy zone for the stock comes in at US$128.25 or lower, over 10% below current levels. So, while I see the stock as undoubtedly the best way to get exposure to gold and silver without the headaches, there is no investing without valuation , as Joel Greenblatt says, and I don't see the valuation being compelling enough at current levels.

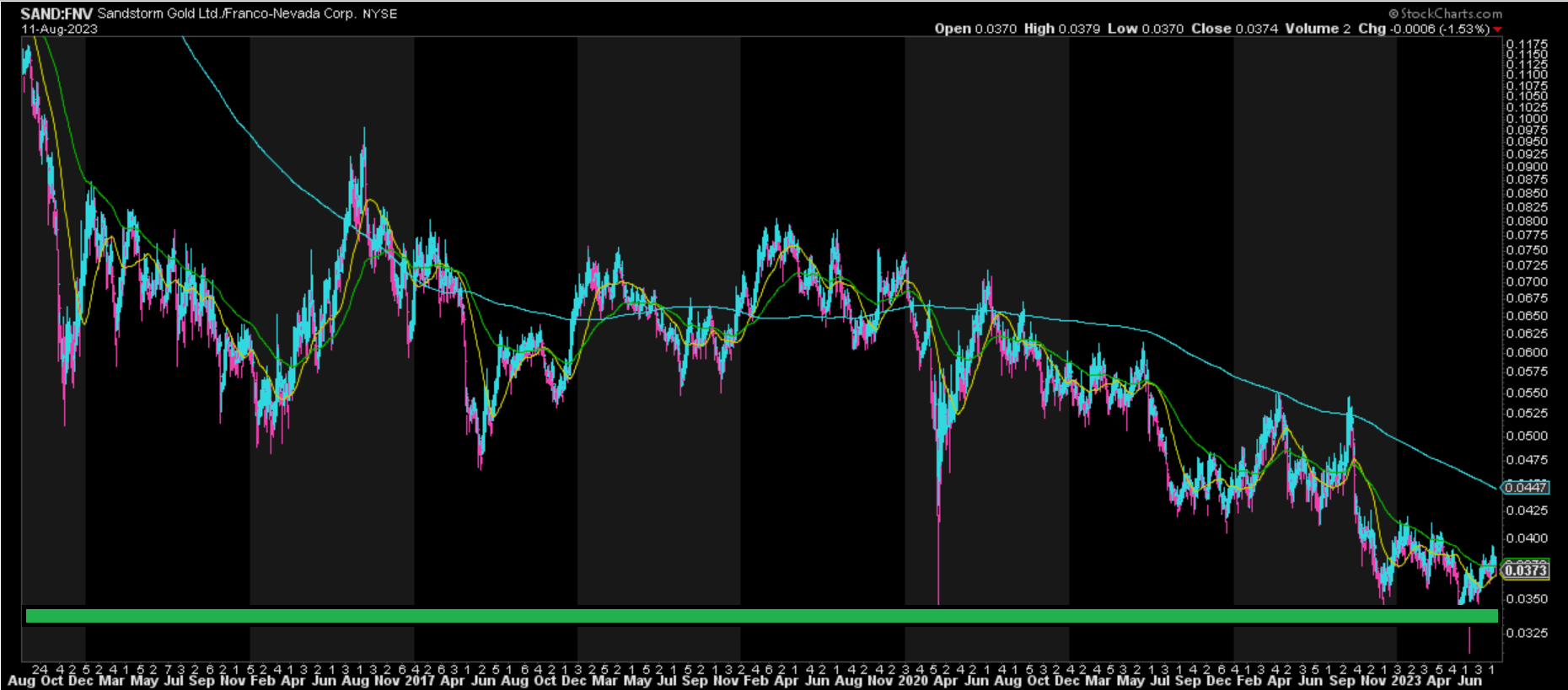

And while there's no question that one has to sacrifice on quality to find more attractive valuations in the mid-tier space, Sandstorm Gold Royalties ( SAND ) has come a long way in improving its portfolio over the past 18 months. The result is that it has brought several higher-quality royalty/streaming assets into its stable (Greenstone, Robertson, Platreef, Caserones), significantly improved its weighted average mine life and its diversification from a, NAV standpoint, yet it hasn't seen this translate to share price performance. In fact, the stock is arguably the most hated name in the royalty/streaming space and this is evident in its valuation, trading at less than 1.0x P/NAV (FNV: ~2.0x P/NAV), and less than 12x FY2024 cash flow per share estimates (FNV: ~25.1x).

{kind=link}

Sandstorm Gold vs. Franco-Nevada Relative Performance - StockCharts.com

So, for investors looking for royalty/streaming exposure with a significant margin of safety, I continue to favor SAND over FNV currently, given the underperformance of SAND relative to its peers (and especially FNV), but with it looking like the stock may be hammering out a bottom relative to peers (shown above).

Summary

Franco-Nevada is the undisputed champion of the sector, with disciplined capital allocation and a nose for occasionally sniffing out monster deposits or average mines before they turn into world-class mines. The market rewarded Franco-Nevada for this gift, evidenced by its 16% CAGR since inception, with its returns trouncing gold bullion, the Nasdaq Composite (COMPQ) and the Gold Miners Index ( GDX ). That said, I prefer to buy stocks when they're hated and trading at extreme discounts to fair value that are unlikely to persist, and even if we assign a premium to FNV relative to its peer group, it's tough to argue that there's a meaningful margin of safety in place at current levels. In summary, while I would strongly consider buying the stock on any pullback below US$128.00, I see the potential for peers like SAND to outperform over the next 12-18 months, hence why I remain on the sidelines for now.

For further details see:

Franco-Nevada Corporation: A Softer Q2 Due To Lapping Tough Comps