AMRS - From Spending Cash To Fermenting Money: Amyris Is Fit To Profit From High ROI Plants And Innovative Marketing

Summary

- "Fit To Win," high ROI Capex and innovative marketing are reducing cash burn equaling 19% of H2 2022 and 26% of 2023 product sales, delivering positive cash flow in 2023.

- Barra Bonita changes everything. Mfg. efficiencies and 30-60% lower COGS swings Amyris Ingredients margins from negative to positive 20-50%, producing faster and more profitable Ingredient growth than we expected.

- Don't forget new Reno and Sao Paulo Consumer Products finishing plants reducing pick/pack/ship costs, improving COGS an estimated 23% and boosting Consumer margins by 10% points.

- Amyris innovates in lab science, fermentation, downstream processes, product formulation - and now is reinventing with AI-driven marketing methods reducing customer acquisition costs by 90%.

- Favorable financings, higher margins and more efficient company-owned facilities are delivering Amyris on a path to positive cash flow and self-financed, highly profitable growth for years to come.

Investors Have Seen a Surge in "Cash Burn" But We Believe Spending Will Decline Dramatically In the Next 4 Quarters From "Fit To Win," Efficient New Plants, Innovative Marketing, Rising Margins and Rapid Revenue Growth At Scale

The last 5 quarters have been disappointing for Amyris (AMRS) investors as the stock has declined 87.7% from its 2021 high to $2.78 ostensibly on the basis of a surge in spending or "cash burn" and the fear of serial dilution of equity holders. However, Amyris is not alone as there has been a sharp drop in the entire synthetic biology sector with Ginkgo (DNA) down 84% from its high, Zymergen (ZY) down 80% before its takeover and Berkeley Lights (BLI) down 98% from its high.

This article focuses on the reasons for Amyris' surge in negative cash flow as well as what we believe will be important fundamental contributors to a fairly quick transition to positive cash flow and profitability.

Covid shutdowns in China, shipping bottlenecks, supply chain shortages and extra air freight costs encouraged Amyris to build its own Consumer finishing plants in Reno and Sao Paulo as well as its own downstream processing plants for making finished ingredients. Fortunately, construction of a state of the art fermentation facility at Barra Bonita, Brazil was already well underway.

At the same time, given its early success with new Consumer Brands, Amyris made strategic decisions to accelerate launches of 8 additional Consumer brands and acquire social media-based marketing, influencer and AI/digital try-on technology companies.

We believe that Amyris has passed the peak inflection point beyond which spending and cash burn will decline due a winding down of foundational capital investments and what Amyris calls its "Fit To Win" 5-action program.

We believe the most important Fit To Win actions are simply beginning to realize the payoffs on the capital investments in the form of much lower production costs in both Ingredients and Consumer Products which should be manifested as significantly higher gross profit margins. In addition, we believe digitally reinvented marketing/advertising methodologies should result in significantly lower marketing spend while continuing to deliver strong double digit Consumer top line growth.

Source: Company data and Tanaka Capital Management estimates. All graphs and tables by Benjamin Bratt

{kind=link}

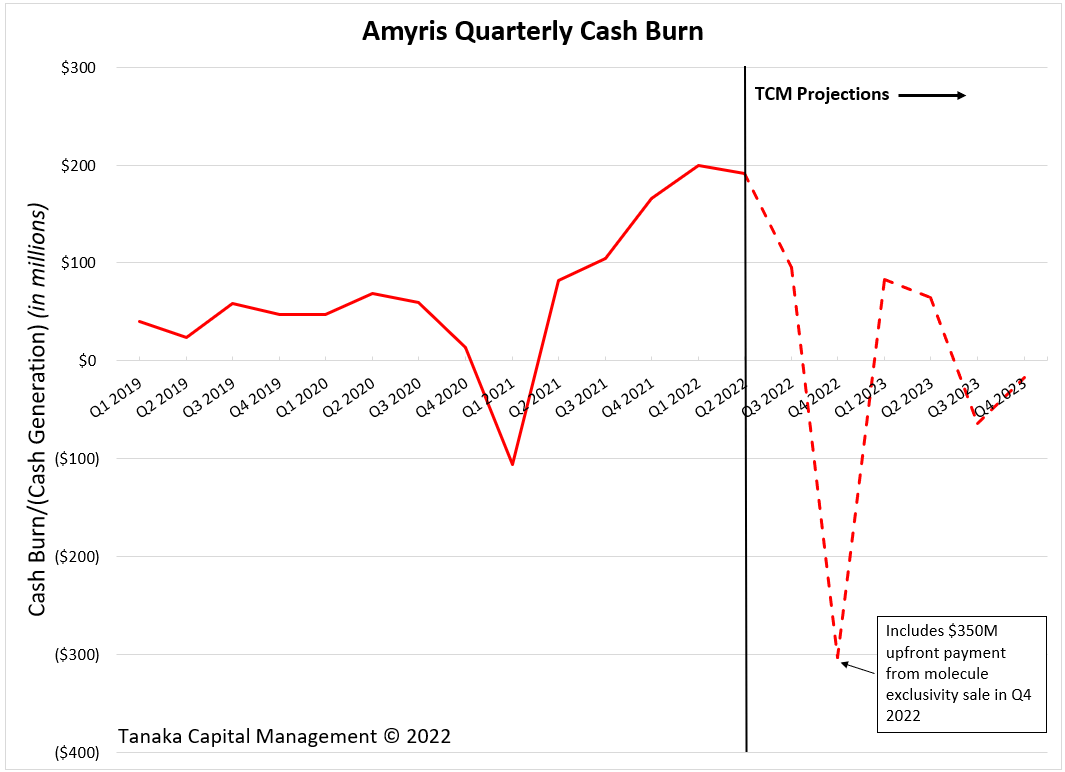

60% of the Last 5 Quarters of "Cash Burn" Reflects a Tripling of SG&A Plus 15% for Capital Spending and 5% for Cash M&A. Low Gross Profits Didn't Help.

The red line in the graph above presents Amyris' big bulge in negative cash flow or "burn rate" which surprised investors over the last 4-5 quarters and weighed heavily on the stock.

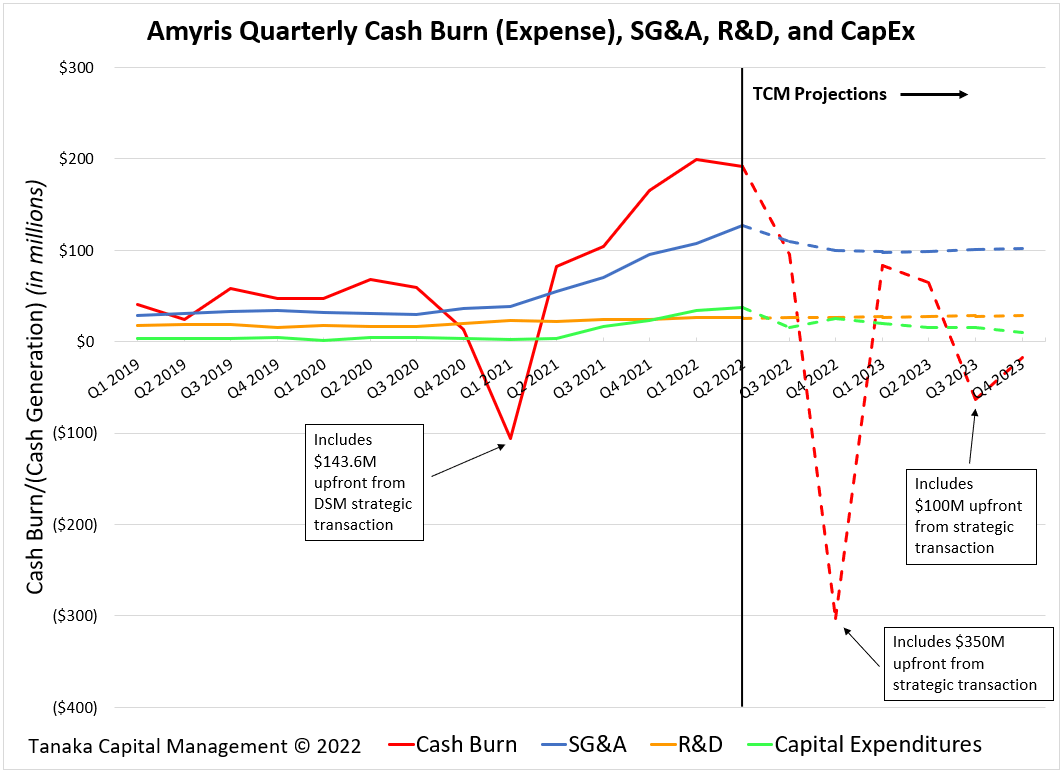

To understand why so much money went out the door, it is instructive to look at the major contributors, SG&A , capital expenditures and low gross profits . Amyris launched new Consumer brands boosting SG&A and boosted Capital Spending (Cap Ex) on new plants to meet rapidly growing demand, gain efficiencies and address unexpectedly high costs from supply chain disruptions, CMOs and air freight.

Source: Company data and Tanaka Capital Management estimates

{kind=link}

Of the $743 million of total cash burn from Q2 2021 through Q2 2022 (area under hump of the red line), SG&A totaled 60%, cap ex 15% and R&D 16%.

The tripling in SG&A (60% of cash burn) reflects many contributors including Consumer brand launches and the inclusion of air freight expenses in the SG&A category until 2023 when it will be moved to COGS. These items will be discussed in the next section.

Capital spending at 15% of Cash burn in the last 5 quarters increased as expected beginning in late 2021, peaking in Q2 of 2022 as construction of the Barra Bonita fermentation facility suffered from inflation and Consumer finishing plants were being completed. Cap ex is scheduled to increase in the next 6 months for downstream processing facilities as planned and in our forecasts.

R&D was 16% of cash burn but not a contributor to the surge in cash burn as it has grown at a steady and moderate rate.

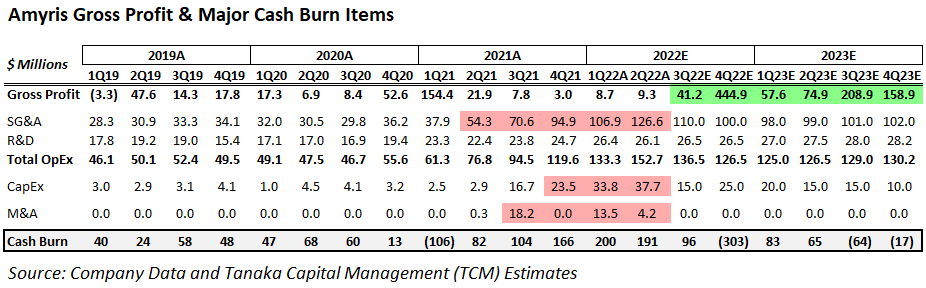

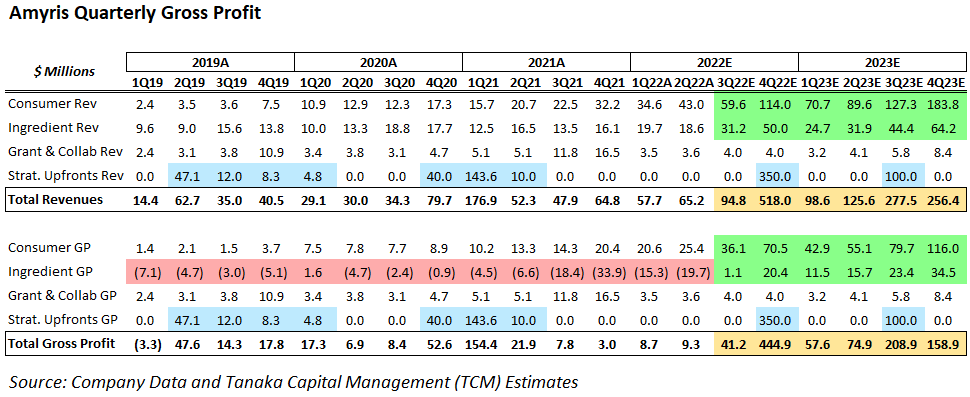

Total Gross profits were barely positive most of the last 5 quarters from Q3 of 2021 through Q2 of 2022 (first line in table below) and did not help much in offsetting cash burn.

However, you can take a sneak peek at what we estimate gross profits can generate in the next 6 quarters as Amyris benefits from its investments of the last two years (shaded green in table below). (Please note that there are so many moving parts making quarterly forecasting unusually difficult given the timing of: (1) the flow though of lower cost of goods sold (COGS) from new plant startups replacing higher cost outside contractors; (2) revenue from new Consumer Brand launches and new retailer stocking; (3) Amyris' "Fit To Win" cost saving initiatives; and (4) the reinventing of Amyris' new low cost AI and influencer-based marketing model.)

Source: Company data and Tanaka Capital Management estimates

{kind=link}

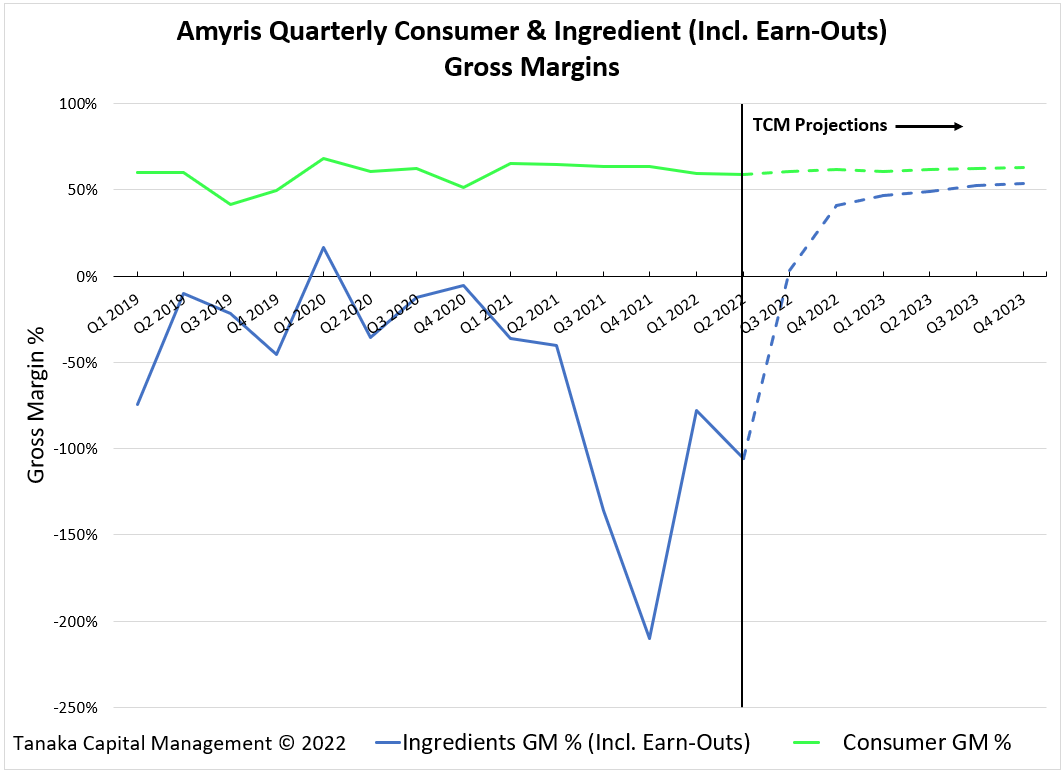

Ingredient Gross Margins Can Rise Higher Than Many Expect in the Next 6 Months And Help Accelerate the Transition to Positive Cash Flow

Low gross profit resulted from Ingredients outsourcing and out of necessity, an increasing reliance on outside CMOs (contract manufacturing organizations). Higher CMO costs were exacerbated by supply chain issues with the CMOs passing on 3-5 times energy costs as well as the Consumer segment suffering from a lack of bottles & caps and shutdowns in China.

Gross profits in the Ingredients business have never been broken out in company reporting. However, we deduced that Ingredient gross margins have been negative for the last few years -- we believe ever since Amyris sold its Brotas fermentation facility to DSM in 2017 for $58 million and has had to rely on DSM and CMOs for its growing volumes and increasingly diverse ingredients.

The above analysis was performed by Ben Bratt at Tanaka Capital Management and independently by Phil Schaeffer at Scott's Cove and was described in our August 8, 2022 Seeking Alpha article Amyris' Vertically-Integrated Business Model Transitioning From Investment Mode To Payoff Mode and subsequently confirmed by management.

Importance of the Brand New Barra Bonita Fermentation Facility

To totally understand the importance of the successful June 2022 startup of Amyris' $135 million state of the art fermentation facility at Barra Bonita, Brazil, it is critical to realize that Amyris' original Brotas fermentation facility was designed and optimized to do one thing very efficiently, ferment farnesene (the largest chemical family) and it still does.

However, Amyris has had to turn to other outside CMOs in Spain and elsewhere to ferment not only much greater volumes of farnesene due to its faster than expected growth of Consumer Brands using farnesene derivatives like Squalane and other molecules in the farnesene family labelled in red below, but also Amyris' growing portfolio of non-farnesene molecules labelled in blue below:

Source: Wiffle1 from r/Amyris Reddit June 2022

{kind=link}

Shortages of precision fermentation facilities (a bit more complicated than brewing beer or wine) have made it critical for Amyris to build a new fermentation facility not only to meet demand growing over 100%/year, but designed with flexibility to switch production lines efficiently for its rapidly diversifying portfolio of ingredients.

COO Eduardo Alvarez has made this point on numerous conference calls, but we believe investors will not appreciate this "efficient flexibility" feature until they see Ingredient margins expanding rapidly.

It is important to see how much Ingredients have been a drag on profitability in order to appreciate how big a jump to profitability could contribute materially to a reduction in cash burn and the generation of positive and growing cash flow in the next 4 quarters.

If we are correct, Ingredient gross margins will expand in the next 6 quarters (blue line below) but not likely to approach the 60-70% Consumer gross margins which have been encouragingly steady (green line) the last few years:

Source: Company data and Tanaka Capital Management estimates

{kind=link}

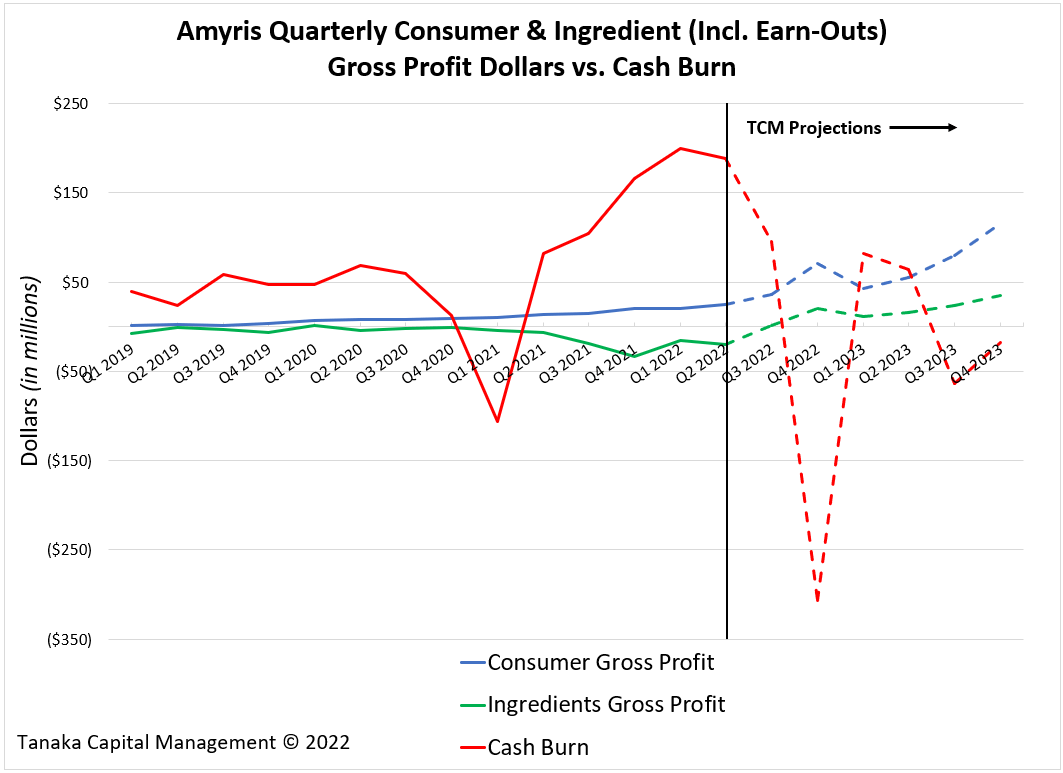

In the graph below we show how in the next 6 quarters we estimate Amyris can go from burning cash to positive cash flow with help from both Ingredient gross profits swinging from a loss over the last few years to a significant positive as well as a surge in Consumer gross profits as its newest brands pass breakeven and into profitability and earlier brands move into more stores and more geographies.

Our estimate of reaching positive cash flow is shown below as a reduction of "cash burn" in this graph in the next 6 quarter estimates. The blue and green lines are separate and not stacked, so you should add the two lines to see how together we expect they will pull the "cash burn" red line down in the next 6 months.

The sharp drop in cash burn in Q4 2022 assumes receipt of the $350 million molecule exclusivity sale that management has projected to occur in Q4 2022, though we can never be sure of timing. However, we are encouraged that we estimate that the cash burn drops towards breakeven and then becomes cash flow positive regardless of the timing of the $350 million cash infusion.

Source: Company data and Tanaka Capital Management estimates

{kind=link}

What Is "Fit to Win" and How Is Amyris Reducing Cash Burn in 2023 and Beyond by a Whopping $170 million/year?

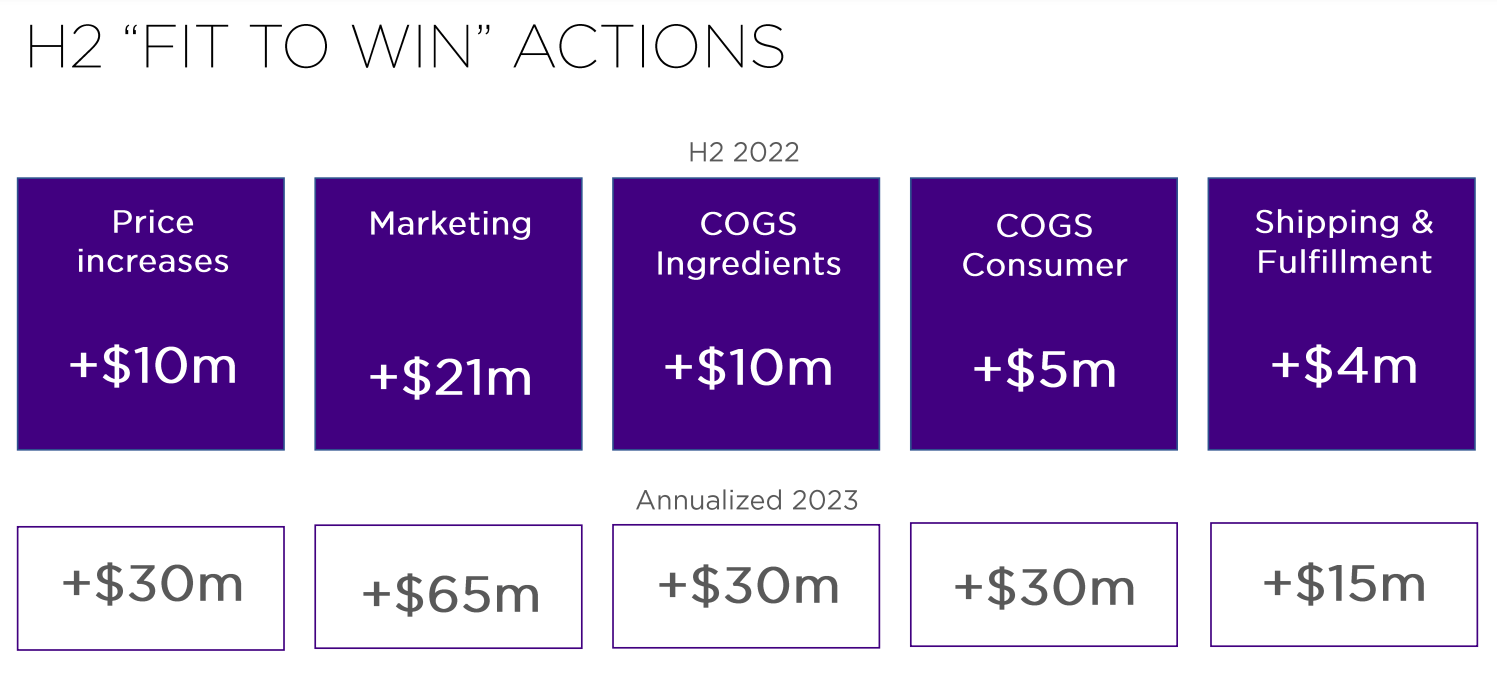

In the August 9, 2022 Q2 2022 conference call , CFO Han Kieftenbeld discussed Amyris' program to reduce spending and make the company more efficient for its next phase of growth. The slide below from the August 9, 2022 Q2 Earnings Call slide deck shows "five new business actions" in the program which we will discuss.

Note that the targeted savings totals $50 million in the 2nd Half of 2022 and an annual rate of $170 million of savings beginning in 2023 and each year thereafter.

These Fit To Win savings are very large and equivalent to about 19% of our estimate of $263 million of sales for H2 2022 (excluding $350 million estimated upfront revenues) and about 26% of our estimate of $658 million sales in full year 2023 (excluding a $100 million estimated upfront revenues in 2023).

These are HUGE cost savings as a percent of ongoing revenues and a direct improvement in operating margins, sounding almost too good to be true.

Two questions might come to mind. (1) How can Amyris have spent so much "extra" in the past 12 months and (2) going forward, how can Amyris cut so much spending while attempting to grow product revenues by what we estimate to be +104% in 2022 and +70% in 2023?

2/3 of Extra Cash Burn Was Unplanned

To answer these questions we asked how much of Amyris cash burn was unexpected and management characterized the spending surge in the last year as about 2/3 unplanned and only 1/3 from management's decision to accelerate investing in marketing for new Consumer brand launches.

We note that the majority of the large cash burn was unexpected and relatively short term, temporary and ironically addressable by the company's capital investment programs which were already underway and about to be completed.

These unexpected expenses included supply chain shortages and delays necessitating the hiring of expensive CMOs to fulfill faster than expected consumer demand and ship with expensive air freight.

Management's expansion of marketing spend was related to the launch of 8 new brands and the acquisition of social media and internet-based marketing companies. Amyris is expecting to continue to connect with consumers and add customers at rapid rates but with much less media advertising spend.

"Fit to Win" Is More a "Return On Investment" Rather Than a Typical Corporate Downsizing"

While we are encouraged that management has commented that Fit To Win is doing well, we had to find out more about these "five new business actions." We have concluded that "Fit To Win" is not a series of cost cutting programs that most investors are accustomed to.

While we expect many companies will be cutting employees over the next 6-9 months to achieve cost savings in a weaker economic environment, we expect Amyris to be growing while at the same time benefitting from cost savings resulting from investments already made in more efficient facilities and marketing methods.

Source: Amyris Q2 2022 Conference Call slides

{kind=link}

The Five "Fit To Win" Business Actions:

1. Price Increases:

CFO Kieftenbeld said on the August 9, 2022 Q2 2022 conference call that price increases were already in place for some ingredients in H2 and Amyris would raise prices on consumer products. My understanding is that 70% of planned price increase for Consumer Products have been implemented with "zero drop off in sales." We are not surprised as many of Amyris' Consumer Product SKUs have unique ingredients, consumers accept some inflationary adjustments in today's economy and several of the items benefit from the "Lipstick Effect" which was coined by Leonard Lauder of Estee Lauder in 2001 who noted that they sold more lipstick than usual after the terrorist attacks and was a contrary economic indicator.

It is important to note that various members of management have commented to me that the discounting that has been occurring with some regularity for their Consumer Brands over the years has been normal and customary.

However, we also understand that inflation in bottles, caps, paper, packaging and shipping costs has been unusually high in the constrained supply chain environment of the last 12 months, particularly from China. So price increases are to be expected, with some lag, and we will discuss how "Consumer COGS" (4th business action) are being reduced significantly from the levels of the last 12 months to offset much of these cost pressures.

2. Marketing:

CFO Kieftenbeld said on the August 9, 2022 Q2 2022 conference call that he expects "marketing cost reductions...to capture the benefits of our growing economies of scale...$21 million in the second half (of 2022) and $65 million for the full year '23 and beyond." We note that $21 million would equate to a very healthy 12.1% margin improvement in H2 2022 on our estimate of $173 million of Consumer revenue , and a $65 million savings would equal a 13.4% margin improvement on our 2023 estimate of $471 million of Consumer revenue .

To get $65 million per year of marketing cost reductions, by far the biggest component of the Fit To Win program, CFO Kieftenbeld "identified substantial opportunities to reduce our marketing spend as a result of the rapidly changing digital media landscape and through portfolio leverage."

We asked for examples and CEO Melo responded that "we are as scientific in marketing as we are in the lab... we reduced the size of our Meta/Facebook spend, removed Agency Advertising and 3rd party creators totaling about $20 million per year."

Asking how could they reduce advertising spend without losing growth and the response was "We invented new ways to create using AI, data algorithms and influencers. It took quite a bit of work, how we measure efficiency, etc. and we have people that know Beauty. We innovate in marketing, brands and how we go to market..."

I asked what it meant for Amyris' customer acquisition costs and he responded, "our customer acquisition costs in the new model we developed are now 10% of what they were at the beginning of the year." In the world of marketing, this is impressive.

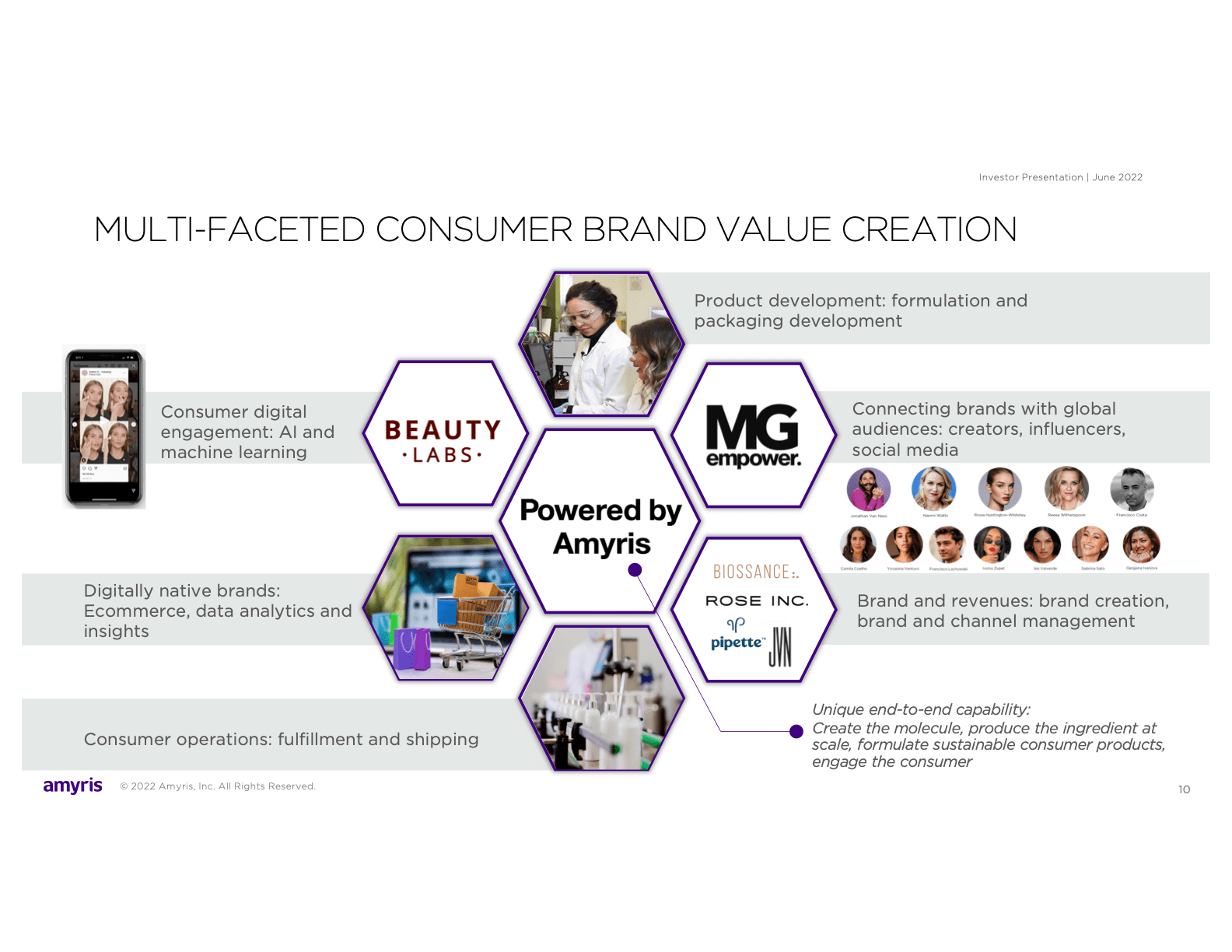

Amyris Is Innovating Again Using Artificial Intelligence and Data Analytics Along With Well Respected Personalities and Influencers To Reinvent Its Marketing Strategies

Now we know why the slide below was presented in the June 14, 2022 Amyris slide deck and have a better appreciation of why Amyris acquired MG Empower for "Connecting brands with global audiences, creators, influencers, social media" and Beauty Labs for "Consumer digital engagement, AI and machine learning."

It appears Amyris has been reinventing marketing of its Consumer brands that has already met with great success in the "Direct to Consumer" sales channel and has only recently begun to expand its omni-channel approach with multiple retailers in the US and overseas.

We hope to learn more about Amyris' innovative marketing approach to digital media-based marketing with influencers:

Source: Amyris Website June 2022 Slide Deck

{kind=link}

Influencers and Brand Ambassadors

We have asked how Amyris is able to attract and partner with such accomplished personalities as ambassadors for its new consumer brands and the answers we get are that these ambassadors are seeking clean and sustainable products which really work. They also actually want to make a difference, consistent with Amyris' corporate mission and culture.

{kind=link}

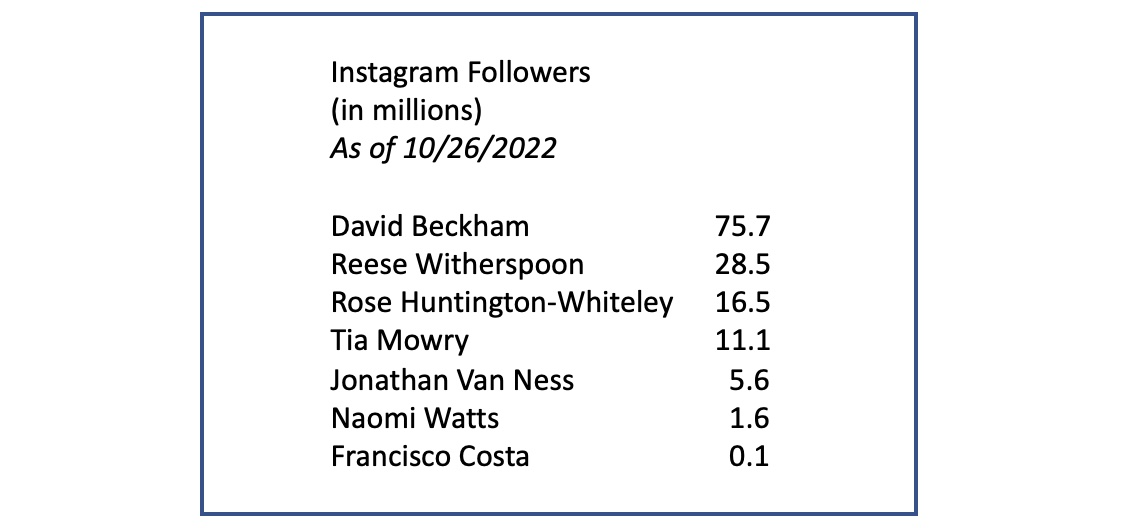

We note that the three newest ambassadors to be joining Amyris' All-Star cast are Naomi Watts, Tia Mowry and soccer star David Beckham. The last two have very large number of followers which should help the new brand launches.

Tia Mowry is helping to launch "4U by Tia" a brand of personal care products for Millennials this quarter and is expected to team up with Walmart. CEO Melo said on the Q2 call that he expects the 4U brand to launch in Q4 and be immediately profitable.

David Beckham is expected to help launch a men's care brand next year. We would not be surprised to see some of Amyris' Terasana CBG and CBD hero ingredients used for pain and inflammation applications for athletes, but just a guess.

Source: Randy Baron, Pinnacle Advisors

{kind=link}

We Believe Stripes With Naomi Watts Could Become At Least As Large As Biossance or JVN

Actress Naomi Watts is helping to launch the Amyris brand "Stripes" for menopause. From Town & Country article on October 3, 2022: Naomi Watts is Taking on The Change. The article cites a huge potential commercial market: "The menopause market is estimated to be a potential $600 billion, with 1 billion women worldwide poised to be in the life phase by 2025. And here's a thought to make us all feel old: Millennials, now ticking past 40, are entering that era of hormonal capriciousness we now know to call perimenopause."

Stripes is positioned to include Ectoine, a new clean and sustainable ingredient coming out of the Amyris R&D pipeline that helps skin retain moisture and is complementary with Amyris' squalane, nature's emollient that provides moisture. We believe that ectoine can become Amyris' next "Hero Ingredient" which will differentiate Amyris' Stripes product line from others that have struggled to address this nascent but potentially large market in need of effective solutions.

3. COGS Ingredients:

To reduce Ingredients COGS (cost of goods sold) by $10 million in H2 2022 and by $30 million per year in 2023 and beyond, CFO Kieftenbeld said on the August 9, 2022 Q2 2022 conference call "we will leverage our Barra Bonita precision fermentation capability to reduce production and shipping costs."

A $10 million reduction in expenses would equate to about 12.3% margin improvement on our estimate of $81.2 million in H2 2022 Ingredients revenue, and a $30 million reduction for next year would deliver a very healthy 18.2% margin improvement on our estimate of $165 million of Ingredients revenues for 2023 (excluding upfront exclusivity revenues).

Source: Amyris website June 2022 New Barra Bonita Fermentation Facility

{kind=link}

Our prior Seeking Alpha articles went into some detail describing the benefits of the state of the art Barra Bonita fermentation facility started up in June of this year: "Amyris Vertically-Integrated Business Model Transitioning From Investment Mode to Payoff Mode" published on August 8, 2022 and "Recurring Marketing Exclusivity Deals Accelerate Amyris On Path To Profitability" on October 1, 2022.

Our estimates of how Ingredients have suffered from negative gross margins over the last few years are shown in the data table below shaded in red:

Source: Company data and Tanaka Capital Management estimates

{kind=link}

In the last 12 months, apparently there were unusual shortages of farnesene due to the Covid-induced surge in demand for Vitamin E (derived from farnesene) which utilized much of DSM's supply of farnesene. This required Amyris to seek supply from CMOs in Europe which were then hit by soaring energy costs and elevated air freight costs to be able to secure supply of farnesene to make squalane to meet the greater than expected demand from Biossance, JVN, Rose and Pipette.

Barra Bonita Changes Everything

CEO Melo has told me that all Amyris capital projects are expected to have a two year payback period or better. This would equate to a very high 50% cash on cash return on investment. Based on a $135 million capital cost for Barra Bonita, we would expect about a $60-70 million/year in cash returns on this plant when fully operational. Barra Bonita is also expected to double the output of the original Brotas facility, providing much needed capacity for growth.

In answer to our question on the August 9, 2022 Q2 2022 Conference Call management commented that the new Barra Bonita facility will reduce the COGS of fermenting farnesene by 2/3 versus what Amyris has had to pay contract manufacturing organizations [CMOs] this year due to shortages of capacity.

Longer term, even as CMO costs normalize with fewer supply chain issues and lower energy costs, we would estimate based on our prior research on Amyris' 17 year learning curve, IP, proprietary equipment and unpublished know-how that Barra Bonita would be able to maintain a cost advantage of 30-60% vs. CMOs depending on the complexity of the final ingredient, some of which have more downstream processing costs.

This advantage could last for years to come, and we would characterize a durable 30-60% cost advantage as the equivalent of "fermenting money."

Note that we estimate the startup of Amyris' Barra Bonita state of the art facility will boost Ingredient gross profits dramatically from a loss of about $19.7 million in Q2 2022 to what we estimate to be a profit of about $20.4 million by Q4 this year due to the start up of farnesene fermentation in addition to the production of tons of vanillin per day as well as Reb M and another unnamed ingredient.

Amyris is a tech company and we would fully expect that Amyris has developed new processes and equipment over the last few years to reduce Ingredient COGS at least 10% below even the cost at the older Brotas plant -- and will likely continue to reduce COGS per unit every year in the future as Amyris scales production and tweaks its science and processes.

COO Eduardo Alvarez has commented publicly that Barra Bonita is running smoothly and we have not heard of difficulties that often plague fermentation startups. So we are very comfortable with the Fit To Win targets for Ingredient COGS savings (returns on investment) and suspect that the targets might be conservative.

4. COGS Consumer:

Amyris' Fit To Win aims to reduce Consumer Products COGS by $5 million in H2 2022 and by $30 million in 2023 by "driving scale, consolidating production and simplifying components and packaging into two new consumer finishing plants" in Reno and Sao Paulo.

Both of these target savings seem very low relative to the $173 million we estimate for Consumer revenues for H2 2022 and the $471 million in Consumer revenues we estimate for 2023, equating to a 2.9% improvement in Consumer margins for H2 2022 and a 6.3% margin improvement for 2023 . Given the extent of supply chain disruptions and delays over the last few quarters we would have expected greater savings for Consumer COGS and we think the targets are conservative .

We expect Amyris to be replacing several CMOs scattered around the US which apparently at times have been inconsistently fulfilling orders as reported by the Amyris Discord and Reddit communities.

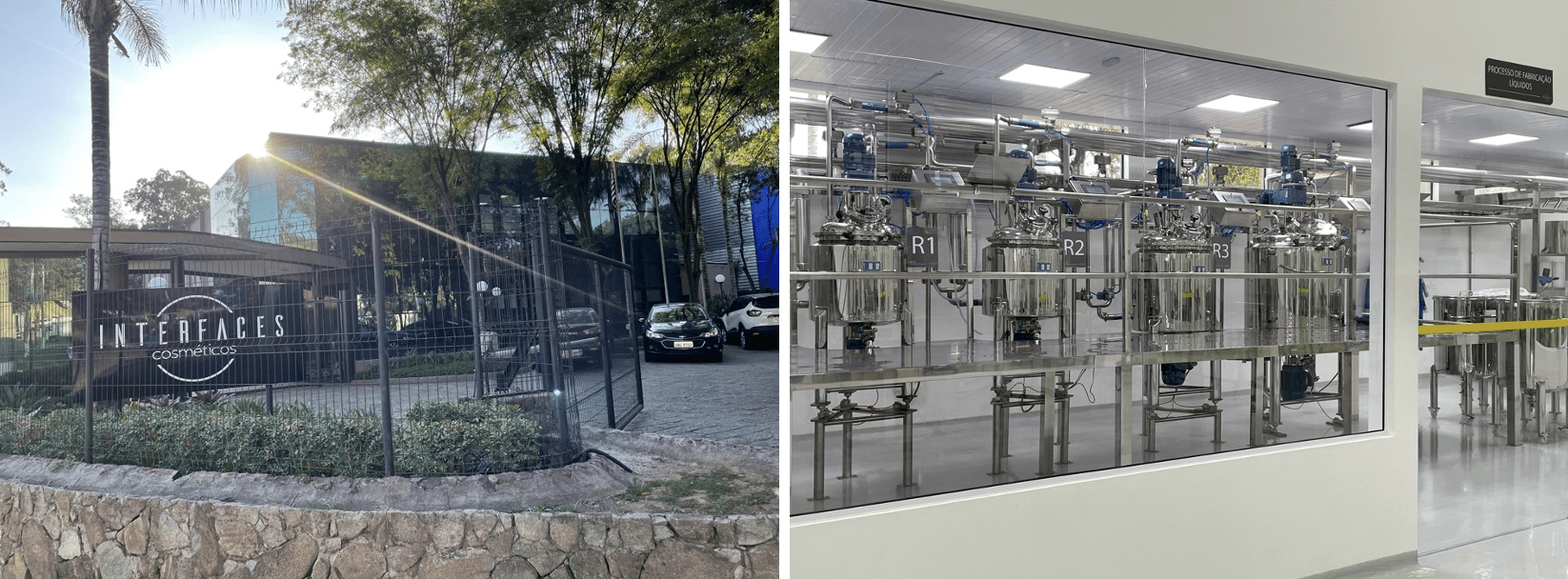

This too will change. E.g., CEO Melo informed us that Amyris' Sao Paulo "Interfaces" cosmetics finishing plant is already making 16-20 SKUs and that it is expected to deliver a 6 month payback on its $10-12 million all in capital cost. This would imply a cash flow return on investment of 200% or $20 million/year , suggesting to us that the savings for Consumer COGS in 2023 could be more than $30 million. We note that savings are related to lower cost components in Brazil at attractive exchange rates and that these kinds of savings can scale with the expected rapid growth in Consumer volumes.

Source: Amyris November 2022 Interfaces Sao Paulo Consumer Finishing Plant

{kind=link}

Our understanding is that Amyris chose to locate a consumer finishing plant in Sao Paulo not only because it would be closer to the Barra Bonita Ingredients facility but also because Brazil already has a sizable cosmetics industry with experienced workers at an attractive cost and an ability to ship to Europe exempt from import duties.

Ironically, Amyris has opportunities to reduce costs and become more multi-national in its manufacturing at a time when many companies are near-shoring and doing the reverse.

5. Shipping & Fulfillment:

In the August 9, 2022 Q2 2022 conference call CFO Kieftenbeld cited "shipping and fulfillment, optimize, simplify and drive scale across our consumer brands and cost structure. We expect $4 million (savings) in the second half...and $15 million full year 2023...this is predominantly a cost for our consumer business and DTC, direct-to-consumer in particular.

Our understanding is that most of the anticipated savings are from a 30% reduction of pick, pack and shipping costs from economies of scale and a new shipping provider.

To Maintain Minimum Cash Balances, Two of Three Financings Have Been Put In Place and a $350 Million Molecule Exclusivity Deal Is Expected To Close By The End of 2022.

Note, we have assumed that Amyris will receive $350 million upfront fees in Q4 2022 as previously predicted by management for the sale of exclusivity for two molecules.

With the 2 recent debt financings and declining cash burn, we project 12/31/22 yearend cash of $117 million even if the anticipated $350 million is delayed into 2023.

Details on the two loan arrangements totaling $180 million secured in September and October are provided below compliments of Randy Baron of Pinnacle Associates and Phil Schaeffer of Scott's Cove:

"On September 13th, Amyris entered into a new loan with John Doerr, via two tranches, of $80 million in total. The notes have a 7 percent coupon and mature in 2023 and 2024, respectively. In lieu of prepayment and upfront fees, the notes included warrants representing $2.0 million shares at an exercise price of $3.91 per share. Based on our fully diluted share count, we calculate this dilution to represent roughly half of one percent of shares outstanding.

On October 11th, Amyris entered into a $75 million loan with DSM, with the potential for an additional $25 million to be drawn in the future. The 9 percent loan amortizes in 2023 and 2024, respectively, but shall be reduced by the value of Amyris' earn-out with DSM related to its 2021 asset monetization. Because Barra Bonita is up and running, Amyris is operating above original expectations for this earn out. As such, we do not foresee Amyris needing to repay this paper except from the earnout, though of course it could once this year's asset monetization is complete. Also, it's good that there was no dilution included as part of the transaction, but there was an upfront fee of $5.1 million."

Our understanding is that there is more borrowing capacity available from these two sources if needed in the future.

We believe that these two financings were at favorable terms and relatively covenant light for Amyris considering that borrowing spreads have widened and high yield financings are being executed at much higher rates today. E.g., Carnival Cruise borrowed $2 billion at 10.375% but had to collateralize 12 ships, junk bonds yields averaged 12.25% in October and AMC borrowed $400 million at 15.1%.

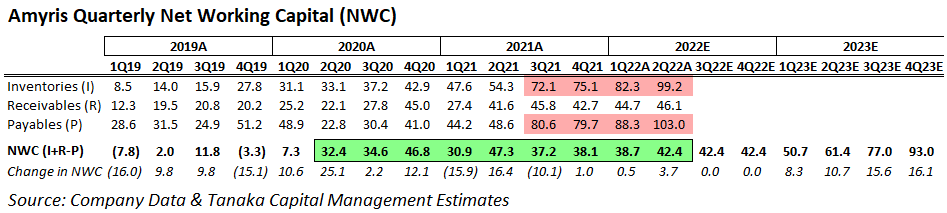

Working Capital Balances Did Not Rise As Quickly As We Expected, But We Anticipate a Rise in 2023 As Revenues Ramp and Amyris Reduce Payables

To complete our analysis of Amyris' cash flow history and outlook we are presenting a net working capital table below which shows the last 5 quarters growth in inventory for the fast growing Consumer business as well as to build safety stock due to an unreliable supply chain.

While inventory growth has been largely financed by extending payables, we would expect payables to moderate and have modeled for a faster ramp in working capital through 2023:

Company data and Tanaka Capital Management estimates

{kind=link}

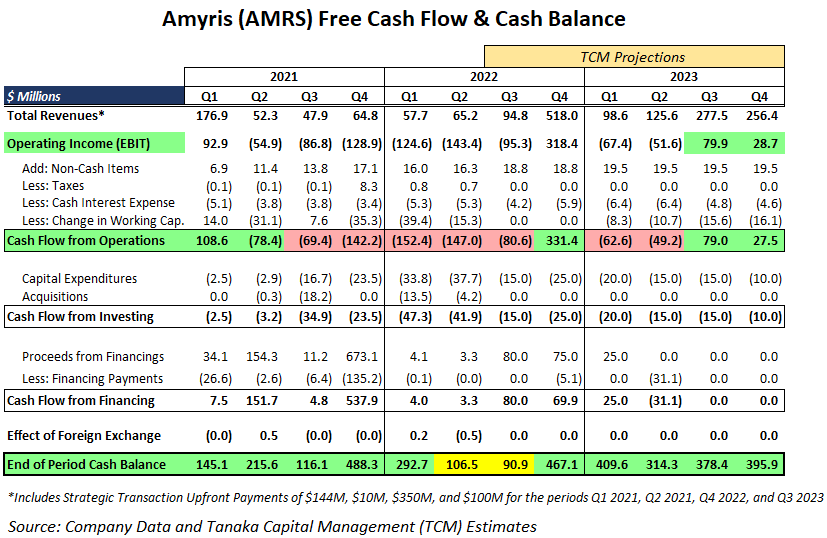

With the Projected Decline In Cash Burn From Returns on "Fit To Win," Estimated Growth in Operating Income and the Two Recent Debt Financings, We Expect Cash Balances To Remain Healthy Over the Next Few Quarters Even with a Rise in Net Working Capital.

A reminder that timing is difficult to predict on a quarterly basis with so many changes underway at Amyris. However, it is encouraging that the many moving parts of the Amyris Integrated Business Model are now scaling simultaneously , from the lab to the plants to the consumer brands and new retailers, and things are moving in the right direction as the company is approaching positive cash flow:

Company data and Tanaka Capital Management estimates

{kind=link}

As noted earlier, even if the large $350 million upfront fees on the two molecule exclusivity sales are delayed from being received in Q4 2022, we forecast cash at an estimated $117 million at year end 2022 which would remain over CFO Kieftenbeld's minimum ongoing target cash balance of $100 million.

Short Term Problems With Long Term Fixes Bring Amyris Closer to Positive Cash Flow and Earnings.

While the majority of the causes of the cash burn over the last 5 quarters were mostly unplanned short term hits to the cash flow and income statements from global supply chains under duress, the fixes will inure to the benefit of Amyris for many years as its high ROI capital investments inject more permanent efficiencies into the Amyris vertical business model with more Amyris-owned and controlled assets.

While this article is focused on the road to positive cash flow in 2023, we should point out that our earnings model projects operating income of $28.7 million on $256.4 million in revenues for the 4th Quarter of 2023 and an 11.2% operating margin. (This can be seen in the table above on the second line labelled "Operating Income" and shaded in green for Q4 2023.)

Our forecast of $28.7 million of operating profit for Q4 2023 gets Amyris close to positive GAAP net earnings depending on whether Amyris uses its cash to pay down debt and reduce interest expense. We should point out that Q4 is normally Amyris' seasonally strongest quarter.

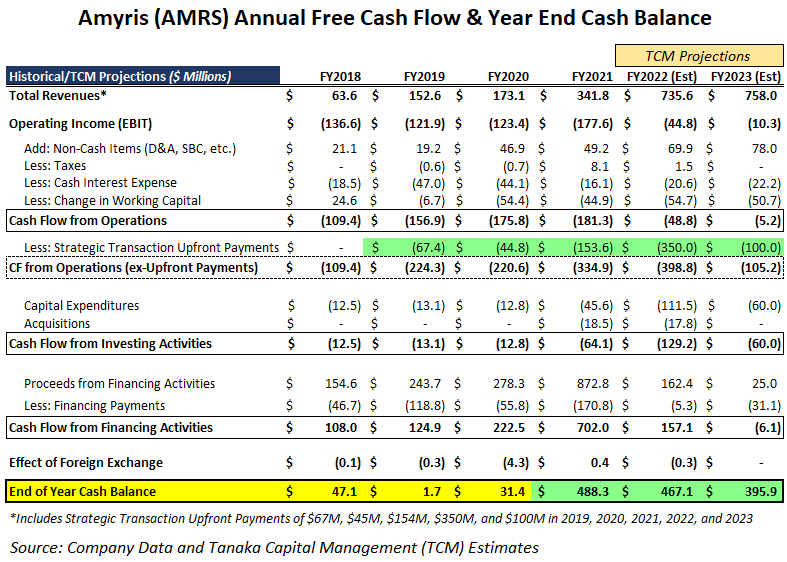

The table below of annual cash flow shows how far Amyris has progressed financially over the last few years:

Company data and Tanaka Capital Management estimates

{kind=link}

Amyris Can Go From Spending Cash To Fermenting Money

As Amyris investors begin to benefit from declining costs and rapidly rising gross profits and cash flow, we believe it is important to be aware that none of this comes easily and growth doesn't come in a straight line.

However, Amyris is an always-innovating, science-based technology company now fortified with an above average profit margin business model. If it continues to make the right decisions on the big decisions and executes on the little things, we believe the odds are increasing that Amyris can leverage its leadership position in the nascent Bio-manufacturing industry to capitalize financially on a potentially very large commercial market opportunity in the early stages of what we believe will be the Next Big Industrial Revolution as clean and sustainable biology replaces much of society's chemically produced products.

In our next Seeking Alpha article we will discuss our revenues and earnings model outlook through 2025, the significant potential for upside from Bluebird opportunities and appropriate valuations.

Risks To Our Thesis

1. Fit To Win program does not deliver anticipated savings although management has said it is ahead of schedule.

2. Barra Bonita encounters some difficulties fermenting at anticipated yields although it has already started up 3 of 5 production lines smoothly.

3. Delays or difficulties in closing on the two Molecule Exclusivity sales by the end of the year.

4. A slowdown in Consumer Product revenue growth due to a more severe recession than is generally anticipated.

5. Difficulties in scaling Amyris' new approach to AI and Influencer-based marketing.

Credit: Tables and Graphs created by Benjamin Bratt

For further details see:

From Spending Cash To Fermenting Money: Amyris Is Fit To Profit From High ROI Plants And Innovative Marketing