CA - Frontera Energy: In A Buy Zone At Current Prices

2023-09-30 08:00:00 ET

Summary

- Frontera Energy Corporation, a Canadian E&P company, has faced challenges due to oil price fluctuations, political adversity, and increasing capital outlay in Guyana.

- The company's troubled outlook in Colombia is offset by its stake in CGX Energy and the potential for a big payday in Guyana's Corentyne Block.

- Frontera's Q2 financials showed increased production and strong cash generation, but risks remain, including funding for future appraisal wells in the Corentyne block.

- We rate Frontera as a buy for risk-tolerant investors.

Introduction

The last few months have been hard on Frontera Energy Corporation (FECCF), a Canadian based E&P company with principal operations in Latin America. We have discussed them previously , and I will commend you to that for a deep dive. We gave them a buy recommendation in March of 2022, when everything oil was going up then, and FECCF seemed like a candidate to do the same.

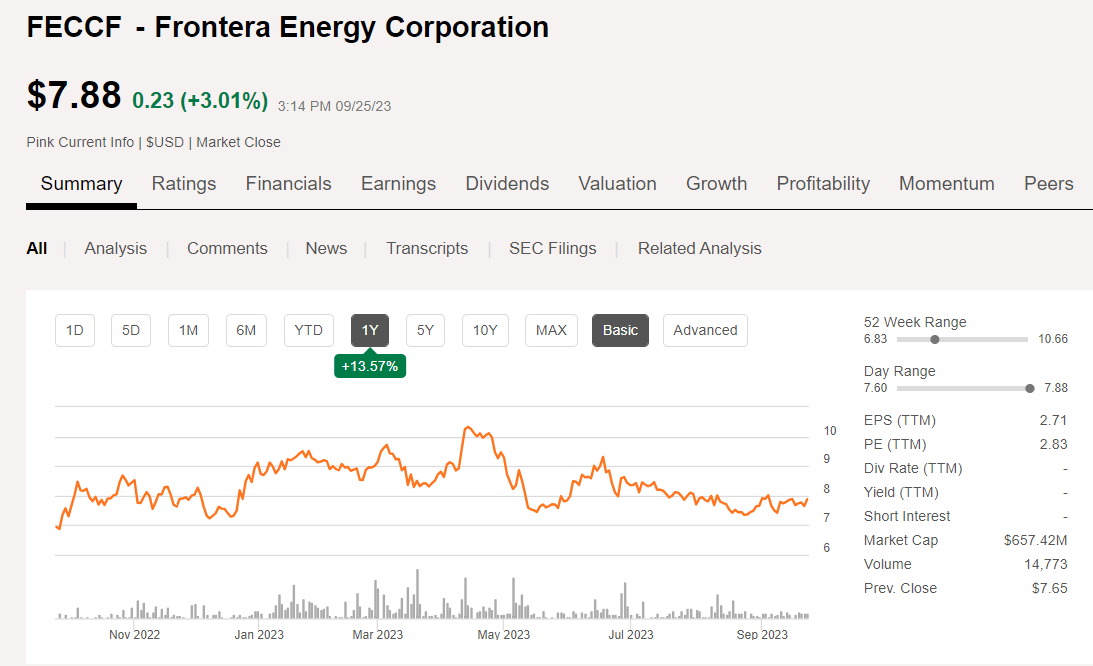

Frontera Energy price chart (Seeking Alpha)

{kind=link}

That recommendation hasn't aged well, as it came within a few weeks of a top set on April, 6th of 2022, and it's been largely downhill ever since. Oil price fluctuations, political adversity in-country, and increasing capital outlay on the Corentyne block, offshore Guyana, operated by CGX Energy. Anyone considering FECCF should also read my last article on CGX Energy ( OTCPK:CGXEF ), as the two companies are joined at the hip in the Corentyne Block offshore Guyana.

Here we sit nearing $8.00 for FECCF, down about 30% YoY from the last report. FECCF's largest shareholder has indicated an interest in selling its position , which totals about 40.84% of the company, and probably puts a drag on shares, of top of all the other lead weights dragging it down. This is well off the analyst's call for a low of $9.57 and a high of $11.88, leading perhaps to the conclusion that the market is mispricing FECCF. We will make that determination as we close out this review.

The case for Frontera Energy

The company has a troubled outlook in its principal operations in Colombia, as the country is turning its back on hydrocarbons. Late last year, the country's new president, Gustavo Petro was quoted in an AP article that suggested the industry's days were numbered in the country-

He has said Colombia will stop granting new licenses for oil exploration and will ban fracking projects, even though the oil industry makes up almost 50% of the nation’s legal exports.

There is a ray of hope for Frontera's current, widely distributed Columbian operations, as the Petro government is now making overatures to oil companies to continue investing in producing fields. A neat way of sidestepping the "no new" licenses dictum to address the country's compelling need for oil exports and the revenue they bring. It should be noted that the company is forging ahead on their current operations as noted in their Q-2, 2023 call. We will touch on this later in the article.

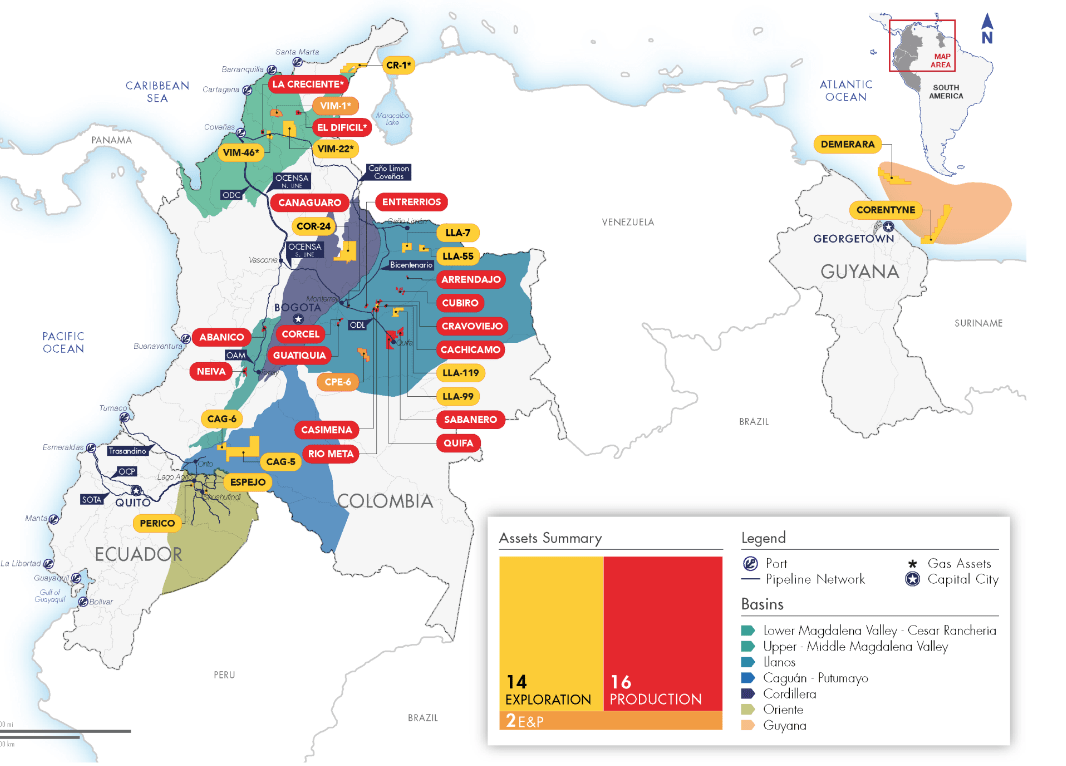

If you look at the right side of the company footprint, you will see the primary reason to be interested in Frontera. Of course, we are talking about the company's stake in CGX Energy and the potential for a big payday in Guyana's Corentyne Block.

Frontera Footprint (Frontera Energy)

{kind=link}

Not the least of the impetus for the interest in the FECCF/CGX two discovery wells is the success Exxon Mobil Corporation ( XOM ) has had a little farther to the north. XOM has made discovery after discovery and floated two FPSO projects, now cranking out 400K BOEPD, with a third sanctioned and on the way. Based on the 11 bn barrels of recoverable OIP discovered by XOM, the Guyanan deepwater blocks have been likened to West Africa twenty years ago.

As noted in the recent APA Corp article, the trend established by XOM's Stabroek discoveries, established a "fairway" for oil discoveries that now are proven to extend into Suriname.

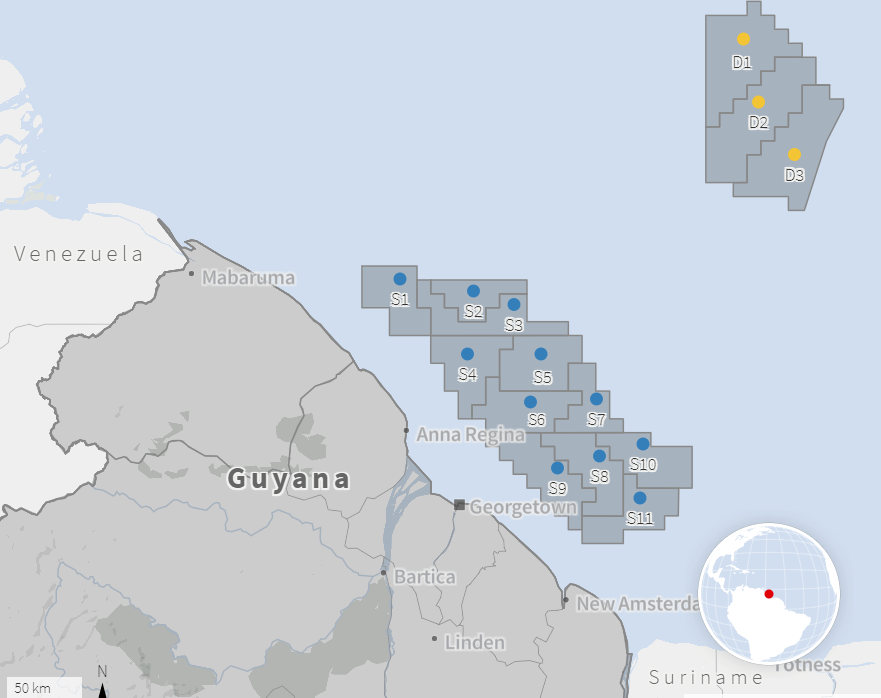

Dateline: Guyana, Corentyne Block

There are probably more people drumming their fingers, waiting for some news...that surely must come soon, on the eventual update from Frontera and CGX on the outcome of the analytical work be done on the Santonian samples, and news that shopping the project to potential "Big Daddies," able to bear the cost of development is finally bearing fruit, than any other project in the world. The suspense is killing us, but there is total radio silence about testing results. Christine Guerrero, whom we interviewed in the last CGX article, was on the call, and pushed FECCF management for information -

On the potential of the block and how to move into the forward basis to say something more, I mean, say something more than that is going to be difficult at this point in time. And as I said, I mean as we have indicated before we normally, permanently looking into strategic options for the current team for the Corentyne result. But that is where we are concentrated right now. And any potential move after this space will be subject to the analysis that we are conducting to the results of the analysis that we are conducting today.

Like I said, radio silence. Nice try, Christine.

Although CGX is nominally the operator, Frontera has a lot to say as it is largely their capital on the line. CGX with no revenues has needed Frontera to advance costs of drilling these two wells-Kawa#1, and Wei#1, and in so doing has ceded 72.7% of the project to them. Worth noting is that Frontera owns nearly all of the common stock of CGX, estimated at 76.05%.

There is also other activity in the area. XOM has spud the Haimara#2, targeting the same gassy sand package found in Haimara #1. Guyana is determined to begin monetizing gas discoveries, and the XOM may need to install infrastructure that could end up advantaging other operators, like Frontera and CGX. A confirmation of further reserves in the area would be supportive of CGX's/Frontera's positive stance toward the eventual development of the block.

Repsol and partners are evaluating next steps on the Kanuku Block, following poor drilling results. Some of this could revolve around the Guyanese governments approach to renewing their license , now expired for the block.

Finally, awards for the just concluded offshore bid round in Guyana are pending, with the awards due November, 1st. This round attracted global interest in the 14 blocks, eight of which received offers.

Guyana 2022 bid round (Guyana ANP)

{kind=link}

I think we are fairly well updated on Guyana now, let's have a look at FECCF's ongoing operations and financials.

South American operations

Frontera upped daily production by 1% to approximately 42,000 BOE per day for the quarter. At CPE-6, they recently achieved daily record production of 6,177 barrels per day. Capex of approximately $155 million was deployed primarily to drill 19 development wells at Quifa, CPE-6 and Cubiro, improve flow lines, build a storage tank and other facilities to double water handling capacity at CPE-6, drill two exploration wells in Colombia and complete Wei-1 exploration drilling activity.

In Ecuador, Frontera’s net was 613 barrels per day of medium crude oil for the three months ended June 30 compared to 1,005 barrels in the prior quarter. On the Perico block, Frontera drilled the G2 appraisal well in July, discovering 48 feet of net pay in the Lower U sand and 24 feet net pay in the Hollin main formation. The well has been successfully completed with initial production rates of approximately 1,200 barrels or 30.5-degree API crude oil. Preparations are underway for the of drilling the Jandiayacu exploration well, which the company expected to spud in August.

Frontera also has a midstream business that is constructing a link between their liquids terminal in Puerto Bahia, and EcoPetrol's refinery in Reficar. Construction of the connection is expected to begin in the second half of this year and take approximately 12 to 18 months to complete a unanticipated total cost of approximately $30 million, and a capacity of 84K BOPD.

Q2 2023 financials and guidance

In Q2 the company recorded net income of roughly $80 million, which compared with a net loss of $11.3 million in the prior quarter. The company's second quarter net income included $35.5 million of a net recovery from asset retirement obligations and impairment expenses, resulting mainly from the company's sale of its interest and asset in the Z1 block and the corresponding reduction in asset retirement obligations related to such block.

EBITDA for the quarter was $116.5 million compared to $92 million in the first quarter. This represents a 27% increase in quarter-over-quarter operating EBITDA, primarily as a result of higher sales volumes during the quarter and the realized gain on their asset risk management contract.

On the cost side, production and transportation cost per barrel totaled approximately $14 and $11.40, respectively. This compares to $12 and $11.20 in the first quarter. The increase in costs quarter-over-quarter was primarily a result of foreign exchange impact related to the almost 10% appreciation of the Colombian peso during the quarter, also impacting higher energy and internal transportation costs and additional costs related to additional activity for services.

Cash generation for the quarter was strong with cash from operations totaling $184 million compared with approximately $1 million in the prior quarter. From an investment standpoint, the company spent $154.9 million in capital expenditures during the second quarter, including $72.8 million related to the Guyana Wei-1 exploration well. The company expects to be in the lower end of the capital guidance of approximately $190 million to $195 million for the full year.

Frontera reported cash on the balance sheet of $214 million compared to $183 million as of the first quarter of 2023. Frontera also uses derivative instruments to manage exposure to oil price and foreign exchange volatility. As of Q2, the company had placed new put hedges totaling roughly 2.1 million barrels or roughly 40% of their production for the year, at prices between $70 and $79 per Brent barrel. Frontera has also entered into FX rate hedges totaling roughly $120 million or approximately 40% of their estimated peso exposure for the second half of 2023.

Source .

Risks for Frontera

Other than the flux induced by the potential for sale of Catalyst Capital's Frontera's shares, the key risk revolves around continued funding of appraisal wells for the Corentyne block. Further delineation is required to establish the size of the reservoir as well as its quality. Frontera has been fronting these expenses and it's cut their cash reserves in half over the last couple of years. Higher oil prices in Q3 may mitigate this somewhat, but what is needed is an outside investor who can shoulder the burden. A burden that could run to another half a billion dollars based on sunk costs for two initial wells.

Your takeaway

Frontera is a largely well run E&P with more than the usual share of problems impacting the stock. The new government in Colombia has sent a chill through the investment community, at least with respect to oil and gas development. As noted there seems to be some recognition of that fact, but it's made people leery of investing there.

In spite of all the activity in the general area of Corentyne, none of the key players, TotalEnergies ( TTE ), Hess ( HES ), or Exxon Mobil ( XOM ) has stepped forward. It's a little disconcerting, as it could be easily had for a song. Frontera's market cap is $653 mm. Some of this could be explained by the fact they all have significant investments in the country currently. There are other companies coming into the picture, Malaysian operator, Petronas (PNAGF) as an example, or CNOOC (CEOHF) - which participates in the Stabroek block, and a number of others.

This is not to diminish the work Frontera and CGX have done. There's just more to do to pretty up Corentyne for "adoption" by a Big Daddy.

Frontera trades at attractive multiples. 1.3X- EV/EBITDA on a TTM basis, and $23K per flowing barrel. It has a solid balance sheet with LT Debt less than one net turn of EBITDA, meaning the company can easily repay it from cash flow. Particularly as Q-3, realizations should be at least 20% above Q-2 results.

My take is that for investors with a huge risk tolerance, and let's understand most of the risk comes from being stalled out on Guyana, FECCF is in a buy zone. I think the Colombian government is already trying to back away from the initial pronouncement about new petroleum licenses. I expect somebody with a ledger book elbowed his way into El Presidente's office and had brief chat about finances. Once a wall begins to crumble, it's not long until it tumbles down. That development could certainly boost the stock. The current 1.3X multiple is absurdly low and represents the present view of risk associated with Colombia.

News of a farm in by one of the big guys would also rocket the stock. I am long CGX and may consider taking a position in Frontera Energy Corporation. I think the positives for further development are strong enough that a white knight will eventually step, in causing a complete rerating for the stock.

For further details see:

Frontera Energy: In A Buy Zone At Current Prices