CA - Frontera Energy Management Is At It Again

2023-04-04 16:53:34 ET

Summary

- Frontera Energy Corporation has a cash flow source.

- Financing a successful commercial discovery in Guyana through to production will be a difficult task for Frontera Energy Corporation.

- The limited number of neighboring operators who might be interested in this situation could instead lead to a war of attrition.

- The Frontera Energy Corporation balance sheet ratios look decent.

- South America is a risky place to do business. Companies present there often have discounted valuations.

(Note: This is a Canadian company reporting in United States dollars that does business basically in South America.)

Frontera Energy Corporation ( FECCF ) and its partner CGX Energy Inc. ( CGXEF ) are going to be drilling yet another exploration well in Guyana. Frontera Energy does have cash flow from continuing production. That definitely helps. However, Frontera Energy is an awfully small company to be doing this kind of very expensive offshore development. Adding to the risk of this plan is the fact that the larger companies in the industry do not always play nice (or some would say fair). It is more like the "law of the jungle" when it comes to this industry. Only those who can handle a lot of risks should consider this issue.

Even the continuing production has got some risks. Colombia frequently has blockades and other interruptions that make projecting cash flow difficult. That is before the recent elections turned the country in a leftward directio n. The company does have a decent history of operating in South America. But investors should not expect a valuation improvement given the hurdles that exist on that continent.

Frontera Energy Key Debt Ratio Presentation (Frontera Energy Fourth Quarter 2022, Earnings Conference Call Presentation)

{kind=link}

Frontera itself appears to have adequate ratios shown above. Personally, I prefer a debt-free balance sheet when a company operates in a place like South America because I believe political risk and the operating risk are higher than it is in the United States and Canada.

If a company is going to get into the offshore business as this one is, then the presence of a cash flow source is essential. This keeps the need to head to the capital market repeatedly down somewhat until exploration results in a discovery.

The majority-owned CGX Energy has no such cash source. So, there is a constant need for financing until there is some production to provide cash flow. This points out the main risk for both companies. Whenever a project is so large as to be a "game changer" or "once in a lifetime," the risk of dilution is such that the dilution may keep investors from realizing the benefits of that discovery.

The other risk of an offshore project is often the limited number of operators in the area that may be interested in the project. Oftentimes, that may limit the number of bidders and result in a bargaining advantage to the larger companies operating in the area. It is usually very hard to talk another company into an offshore project if they do not have a presence in the area already. A lack of competitive bidding for a successful find can turn instead into a war of attrition for a smaller company.

The benefit of a large discovery can be that a lot of growth can be accomplished by one discovery, instead of the years it takes for the steady progress shown above.

Cash Needed

Normally, companies that participate in offshore projects are much larger than Frontera. Hess Corporation ( HES ), for example, is the smallest company involved in the Exxon Mobil Corporation ( XOM ) partnership that has discoveries and is now beginning to produce those discoveries.

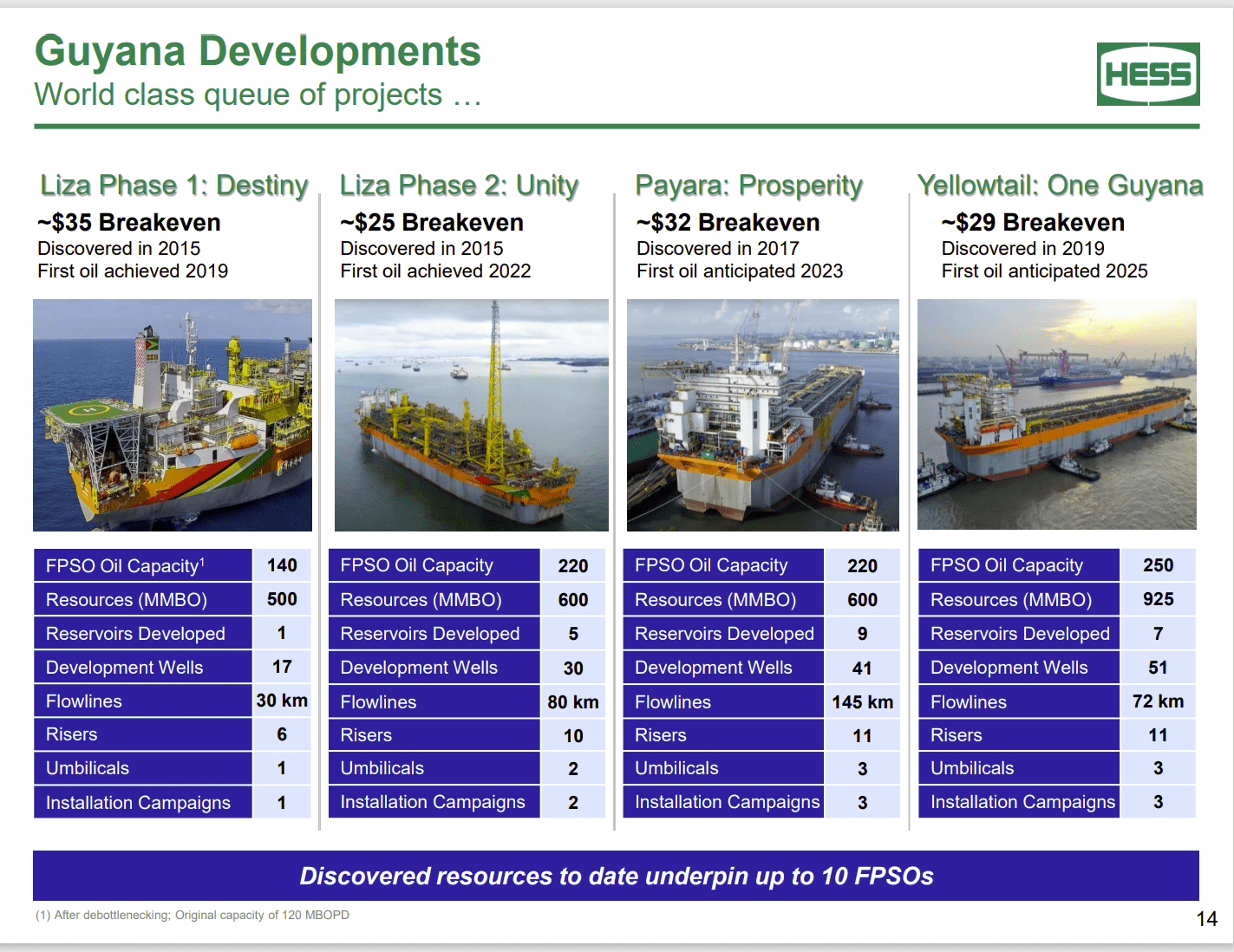

Hess Corporation Description Of Approved Production Projects In Guyana (Hess Corporation February 2023, Investor Presentation)

{kind=link}

Based upon the Hess management presentation shown above and subsequent discussions in conference calls and "road shows," it would appear that an FPSO can cost anywhere from $6 to $12 billion, depending upon requirements. Since this slide came out, no more projects have been approved. However, the latest project submitted to the government of Guyana for approval is likely to prove more (not less) costly. Even more costly is all the offshore wells shown above for each FPSO combined with all the connections required. Offshore well costs in excess of $100 million are not uncommon. That is especially true when one considers (midstream type) hookups or other transportation from the well to market.

For a company the size of Frontera, the cash flow is clearly not there to take on a project of this size. Majority-owned CGX clearly will not be a lot of help in this situation, either. This does not include unexpected challenges and setbacks like dry holes on the way to successful production.

There is also the time value of money. Hess has on several slides the date of the discovery and then the actual date of production for the approved projects. A typical time period lag is 5 to 7 years. So, not only does a lot of money have to be raised; but there is also a long time between a successful commercial discovery and actual production. Any borrowings have to be funded for that period of time. Then there is the risk that an FPSO begins producing during a time of low commodity prices (which increases the payback period).

There is also the risk that a discovery on the Frontera acreage would not be commercial, but had the lease been part of one of the other operator holdings, that well may have been connected to a commercial project nearby that warranted an FPSO. So, there is a lot between a discovery and "success" that may derail a successful future.

The Future

Frontera has the ongoing South American business. That alone can be considered risky, even though countries like Colombia have in the past heavily supported the industry. Nonetheless, there is a cash flow source to fund future growth that does not include Guyana.

Management needs to balance that growth against large projects like Guyana, or there may not be steady progress. Instead, the result would be a future based on the success or failure of Guyana. The Guyana project may cause significant stock price swings based on market-perceived progress or lack of progress. Each step in Guyana appears to have a lot of money involved. Therefore, quarterly earnings swings could be potentially large when one project like this is involved.

Furthermore, success even with a commercial discovery is far from assured. There is a potential risk of excessive dilution on the way to a lot of production. Trying to find a partner large enough to fund a success is definitely not guaranteed (nor are the terms of such a partner always acceptable).

The likely volatility of the future Frontera Energy Corporation stock price could involve some substantial trading opportunities for those that know when to walk away and not look back. But this stock is going to be highly speculative, even if it is acceptable to some investors. The roller coaster ride is likely to exceed the tolerance of a lot of investors. Frontera Energy Corporation is one of those "coffee money only" type stocks until there is some assurance of the outcome of the Guyana project.

For further details see:

Frontera Energy Management Is At It Again