SFL - Frontline: Up 57% YTD With More To Come

Summary

- Frontline's EPS trending higher, thanks to a big jump from LR2 vessels.

- Fundamentals do look positive over the next couple of years.

- Higher average time charter equivalent earnings will result in higher dividends.

Frontline Ltd logo (Frontline)

Investment Thesis

In my last article on Frontline Limited (FRO), I upgraded it to a buy in June, not at the bottom of the market, but the share price has since gone up by 21%.

On August 25th, they came out with their 2022 Q2 results. As such, it is a good time to revisit the thesis and see what is going on in the market in which they operate.

2022 Q2 financial results

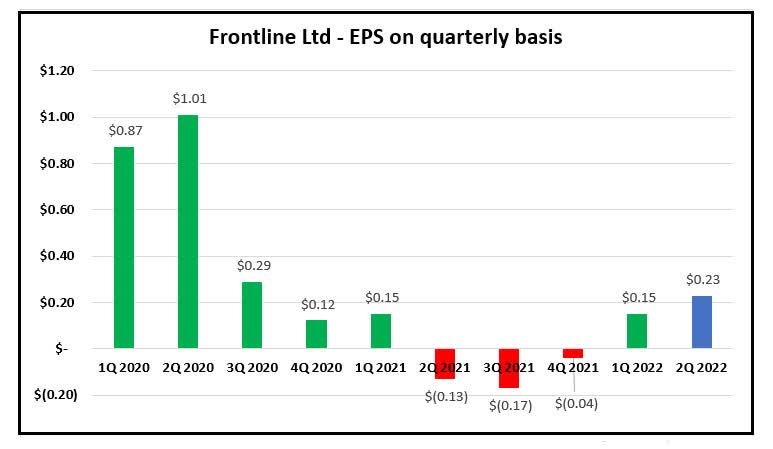

FRO reported a net income of USD 47.1 million or USD 0.23 per share. From this, the board decided to pay out a dividend of USD 0.15 per share. That is a payout ratio of 65%.

FRO - EPS on a quarterly basis (Data from Frontline. Graph by author)

{kind=link}

The adjusted net income came in at USD 42.5 million, after accounting adjustments from gains or losses on non-cash items such as derivatives, results of associated companies, amortization of acquired time charters, insurance claims, and changes to values of marketable securities.

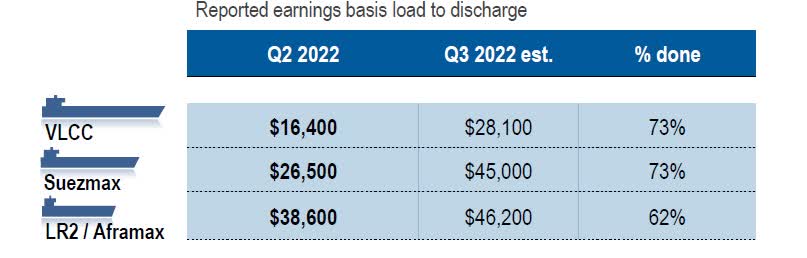

The average cash cost breakeven rates for the remainder of 2022 are about USD 24,900 per day for the VLCCs, USD 20,000 per day for the Suezmax tankers, and USD 17,200 per day for the LR2 tankers.

We can see that it was the smaller Suezmax vessels, and particularly the LR2/Aframax vessels which pulled in the profit.

Average earnings basis load to discharge ports (FRO 2022 Q2 presentation)

{kind=link}

With regards to their balance sheet, the total amount increased by $304 million as FRO took delivery of 2 new buildings VLCCs, "Front Alta" and "Front Tweed".

It also increased with the acquisition of the Euronav (EURN) shares in exchange for Frontline shares, in addition to regular debt repayments and depreciation.

Long-term net debt is USD 1,626 million and the book value of the fleet is USD 3.531 million, which means that its gearing is 46%. That is a reduction from a gearing of 52% one year earlier.

At the end of Q2, they held USD 286 million in cash and marketable securities.

FRO's merger with Euronav

A definitive combination agreement has been reached for a stock-for-stock combination of FRO and EURN where the exchange ratio is 1.45 FRO shares for every 1 EURN share.

A tender offer is expected to be launched in Q4 of this year. Should FRO get above 75% acceptance amongst the Euronav shareholders, they will go directly to a merger with EURN.

In the event the acceptance ends up between 50.1% and 75%, EURN will become a subsidiary of FRO.

What is important to shareholders of FRO is that the combined group will have a fleet of 146 vessels. They do anticipate delivering synergies of at least USD 60 million yearly from this.

Market outlook

During the Q2 presentation to analysts and investors, FRO informed that Castor Analytics described the market development for the VLCCs as "the most impressive summer rally in the sector on record". From early June until the middle of August, time charter equivalents for non-eco tonnage rose by USD 65,000 per day.

The global oil demand slipped by 700,000 barrels per day in Q2 compared to Q1, averaging 98.4 million barrels. The oil supply came in at 99.1 million barrels per day.

In my last article on one of FRO's competitors DHT Holdings (DHT), I highlighted some of the effects in the market of major oil-consuming countries like China and the U.S. releasing parts of their strategic petroleum reserves in order to reduce the price of oil.

A large importer, like China, obviously imports less when they release inventory sitting in their storage at home. It is less relevant to the U.S., as it is more of a net exporter of oil these days, so it could in fact boost shipping if more cargoes were released.

It was interesting to learn what one of the experts in the crude oil market had to say about the development of the oil price going forward.

At the recent ONS energy conference in Norway Jarand Rystad , founder of Rystad Energy, made a bold prediction that the oil price will stay around the levels we see now, or up and down between 100 to 130 dollars a barrel this year and in 2023. But he predicts that the oil price will collapse in 2024 and that the prices could fall to levels as low as USD 20 per barrel.

The reason, he claimed, is that we are now mobilizing a lot of new capacity. One example is that the number of new wells has fallen from 40,000 to 30,000; however, the average productivity on those wells has increased by 50 percent.

It is hard to predict anything.

Especially the longer out on the time horizon you go. I have high respect for Rystad Energy's work, but I believe there are too many factors that can shift the supply and demand balance. Nevertheless, if we do see a much lower oil price, it would in theory lead to higher demand which is good for all tankers, both crude and clean.

With regard to the market for shipping clean oil products, we saw a big improvement for FRO's LR2 tankers. Bear in mind that these are not only able to carry crude oil, but can also trade clean products such as gasoline.

In my article on SFL Corporation ( SFL ) back in March this year, I stated that I was bullish on that sector, as there is a shift taking place with oil majors consolidating their refineries and shutting down many of them. One such example is Australia. They have now become very dependent upon importation to cater to their demand. As we have learned this year, which is not a good idea when war breaks out.

We have seen a dramatic change in demand and trading patterns for refined products developing during Q2 this year" - Lars Barstad CEO of Frontline Ltd

He also went on to say that some of the improvement in the market can be attributed to the volatility the war in Ukraine has created, as this results in longer voyages which reduces the number of available vessels in the market.

On the VLCC side, Russian crude oil that earlier was exported to countries in Europe is now heading to Asia. This has created this inefficient trading pattern.

The present order book is 47 vessels to be delivered. After a drought of one year for the shipyards with no new VLCC orders, Japan's Mitsui OSK Lines have just ordered two LNG dual-fuel VLCC newbuildings. These will be built in China by Dalian COSCO KHI Ship Engineering.

The total fleet of VLCCs is 861 vessels with about 10% of these being older than 20 years.

The big movers in the crude oil trades are the large oil majors like Shell (SHEL), Exxon Mobil (XOM), TotalEnergies (TTE), and so forth. They have been absent for several years in taking any kind of interest to secure VLCC on multi-year charters.

According to FRO's management, what has changed in the last quarter is that several of them have now started looking at chartering in such tonnage for 3, even 5 years time charter. That is positive news.

Risks to the thesis

I would say that the biggest risk to the thesis is the fact that it is a very volatile spot market.

We have seen many spikes in earnings in the past, but the biggest problem with them is that they generally do not last very long.

{kind=link}

The spikes can go very high, as can be seen above. However, those high rates lasted two to three months, with long periods of rates way below USD 50,000 per day.

In order to hedge against a possible fall in the market, FRO does from time to time secure some long-term charters.

It was just revealed on 25th August that they have secured a 3-year time-charter to Trafigura for one of their LR2/Aframax tankers. The rate was USD 31,500 per day.

Final thoughts and conclusion

Analysts covering the shipping sector at Sweden's largest bank SEB came out on 2nd September with a bullish call on the tankers. They think that this time it is different than the graph above, showing the short duration with elevated rates. They believe that we are going to see two to three years of elevated rates for VLCCs. For what it is worth, their favorite pick was also FRO in that space.

What we know, with a high degree of certainty, is that if and when the market improves to rates north of the USD 50,000 level, FRO will generate a lot of cash.

How much?

FRO estimates that on the base of historical Clarkson TCE rates for non-eco vessels in the period 2021, adjusted for premiums on scrubber and eco vessels, FRO delivers a free cash flow per share of USD 2.34 for the year. Furthermore, the free cash flow yield obviously increases should the average time-charter earnings go higher in 2023.

It is quite likely that they will distribute at least 60%, but probably more, of this in the form of dividends to the shareholders.

The present yield going forward is based on USD 0.15 per quarter and a share price of USDD 11.90 would be 5%. Should the dividend payout ratio stay at 65% and they achieve a free cash flow of USD 2.34 per share, it would be well covered even if they were to double it from here to USD 0.30 per quarter.

The merger will also add more to the cash flow despite an increase in shares outstanding.

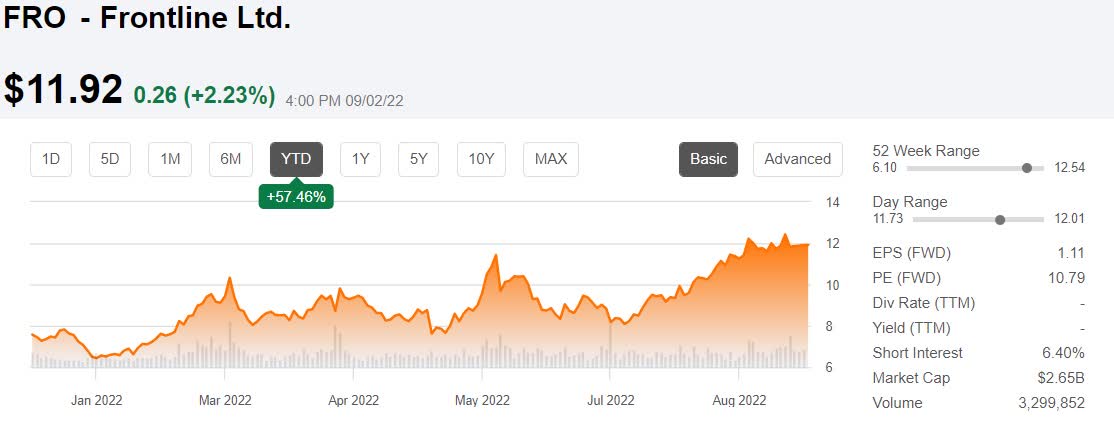

FRO's stock has gone up by 57% so far this year.

{kind=link}

I believe the risk/reward seems favorable as I expect more good news to come from FRO in the next one to two years.

It remains a Buy for me.

For further details see:

Frontline: Up 57% YTD With More To Come