FNKO - Funko: A Turnaround Plan Is In Place But It May Not Pan Out

2023-12-15 00:24:50 ET

Summary

- Funko's stock has fallen over 30% this year due to retrenchment among its channel partners and lower revenue.

- The company is implementing a complete overhaul of its business, including a headcount reduction and SKU count pull-in.

- These efforts may help to eliminate cost in the short-term, but in the long run, Funko's biggest problem remains its sales decline.

- With limited liquidity (~$30 million in cash on top of nearly $280 million in debt), Funko is in a relatively precarious position.

The stock market has been in rally mode for the past few months, fueled by hopes for lower interest rates in 2024. Amid the recent bonanza, however, there have been a few holdouts, and prominent among them is Funko ( FNKO ), the beleaguered pop culture toymaker.

Shares of Funko have slipped more than 30% year to date. The core issue here is retrenchment among Funko’s channel partners, which move a considerable amount of product for the company and are responsible for the lion’s share of the firm’s top line. With retailers looking to optimize inventory and purchasing much more carefully in a weaker consumer spending environment, Funko has seen drastically lower revenue - which creates a vicious cycle, as its product visibility suffers and further deteriorates the brand.

I last wrote a bearish article on Funko in October, when the stock was trading closer to $8 per share. Since then, two factors have emerged: first, the company has released mixed Q3 results. While its top line continued to suffer, the company is seeing stronger DTC (direct to consumer) results, which suggests that there’s a lot of noise right now from channel partner retrenchment which may not fully represent end-customer demand.

The company is working on a complete overhaul of its business (which I’d argue is quite necessary for a company suffering double-digit revenue declines and is in such a strapped cash position). Among the many levers that the company has put into motion is a sharp headcount reduction that aims to bring annual operating expenses down by $150 million (for sizing purposes, roughly half a quarter’s worth of revenue) relative to 2022 levels, as well as a pull-in of its SKU count.

Funko had long prided itself on having a wide diversity of offerings to attract fans of all kinds of pop culture trends. Its new corporate strategy, however, is to rely more on “evergreen” content that is less cyclically driven and less on newer releases - which would allow the company to use more of its existing molds and gain operating leverage in its manufacturing process. Carrying fewer SKUs will also necessitate less inventory for the company, freeing up cash at a time when Funko needs it most.

These are admirable efforts. In spite of this as well as continued devaluation in the stock, I remain bearish on Funko. I find it difficult to believe that Funko can reverse its sales declines while channel partners are draining their inventory. And while Funko’s SKU reductions may help its margin profile in the near term, it may cap the company’s ability to return to sales growth.

The other core concern is liquidity. As of the end of the most recent quarter, Funko had only $32 million of cash left on its balance sheet - which is more than offset by $277 million of debt. In other words, inventory shrinkage may not just be a choice for Funko - it may be necessary for the company to corral as much cash together as possible.

All in all, I continue to worry about poor top-line trends for Funko amid retrenching consumer demand. There are some pockets of hope (which I view as upside risk for the stock), but in my view, it will be difficult for Funko to surmount revenue pressure with its limited resources.

Q3 recap

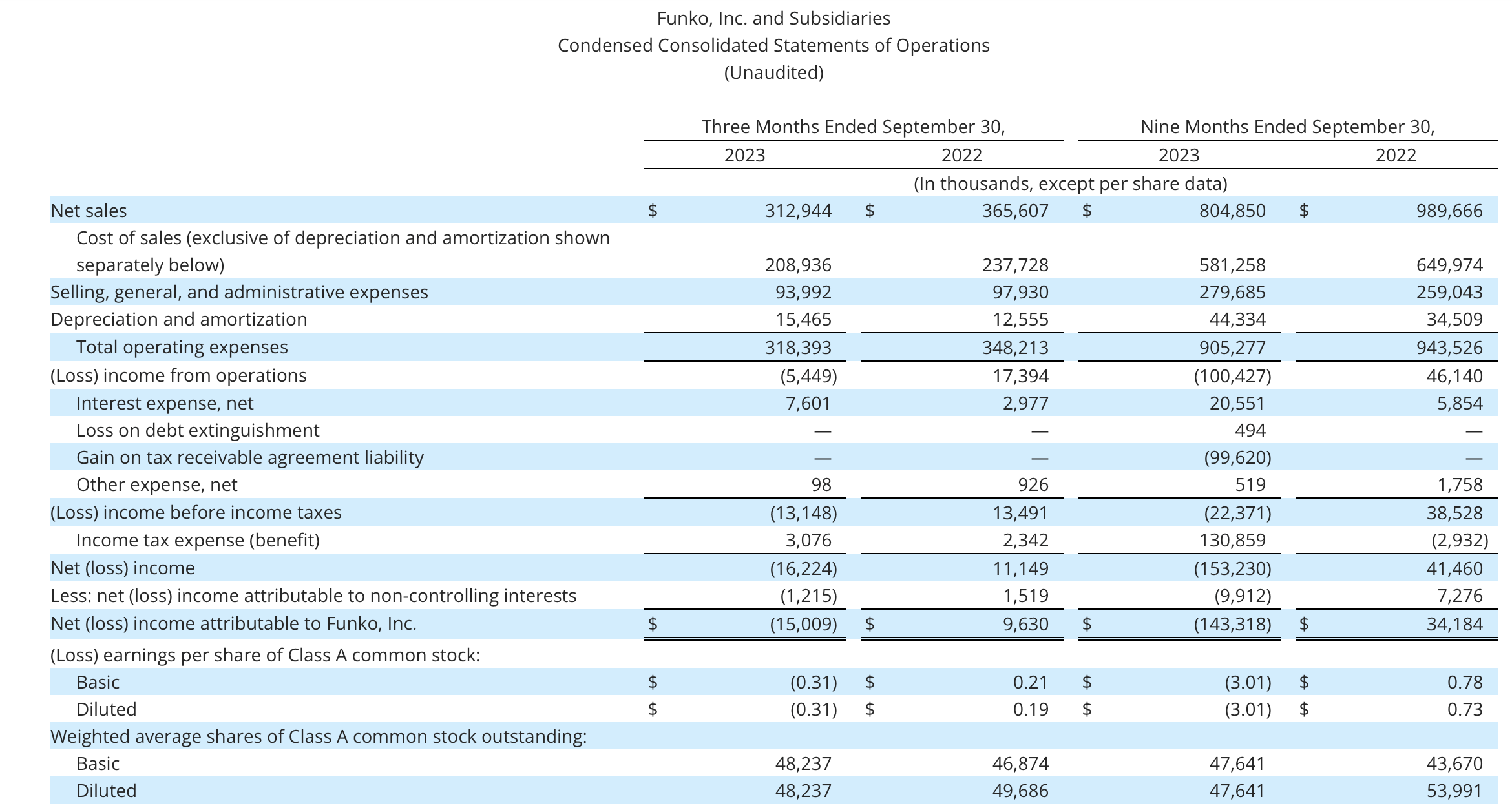

Let's now go through Funko's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

Funko's revenue declined -14% y/y to $312.9 million. The bright way to spin this is that revenue did come in ahead of Wall Street's much more modest expectations of $289.6 million (-21% y/y), and the company also improved sequentially relative to -20% y/y decline in Q2.

Management has pointed to stronger DTC sales as evidence that the brand isn't really in decline. In Q3, Funko noted that DTC sales grew 32% y/y. However, this is only 17% of the company's overall sales mix (up from 11% in the year-ago Q3) - showcasing how reliant Funko is on retail partners to drive sales.

Here's additional commentary from interim CEO Mike Lunsford's prepared remarks on the Q3 earnings call, detailing sales momentum as well as the company's new lower-SKU count strategy going forward:

We believe our fans and customers are excited and engaged that our brand is strong. So how do we quantify this? First, we grew direct-to-consumer sales 32% year-over-year, with D2C sales in Q3, representing 17% of our sales mix versus 11% in the third quarter of last year [...]

In the third quarter, we also made progress focusing on fewer products done extremely well. On the fewer product side, we have stopped development of lower value product lines and SKUs.

We believe this will ultimately help us expand gross margin and improve inventory management. On the done extremely well side, Loungefly won the Innovation Award at The Licensing Awards in September for its McDonald's French Fries Crossbody Bag and Loungefly’s Disney Nightmare Before Christmas toy, Undead Duck Crossbody Bag, one of the fastest selling lines of Q3 saw 100% sell through within the first week of sales."

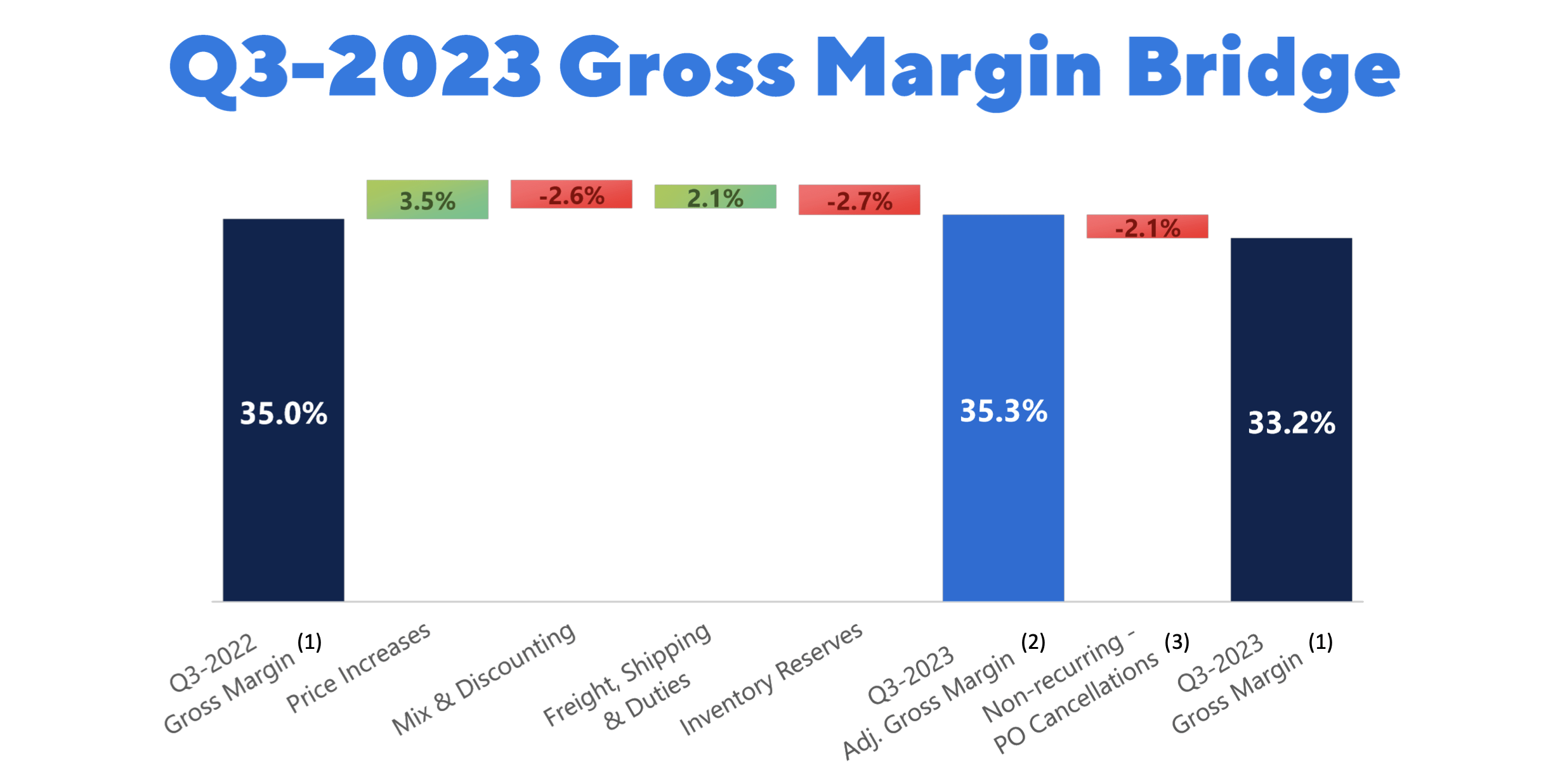

We haven't yet seen the benefits to gross margin, however - which clocked in at 33.2% in Q3, down 180bps y/y . The company is chalking up $6.4 million of cost (2.1% margin) to a one-time factory purchase order cancellation; but even after adjusting for that, Funko's ~35% gross margin is still much weaker than gross margins in the 37-38% range in prior historical years.

{kind=link}

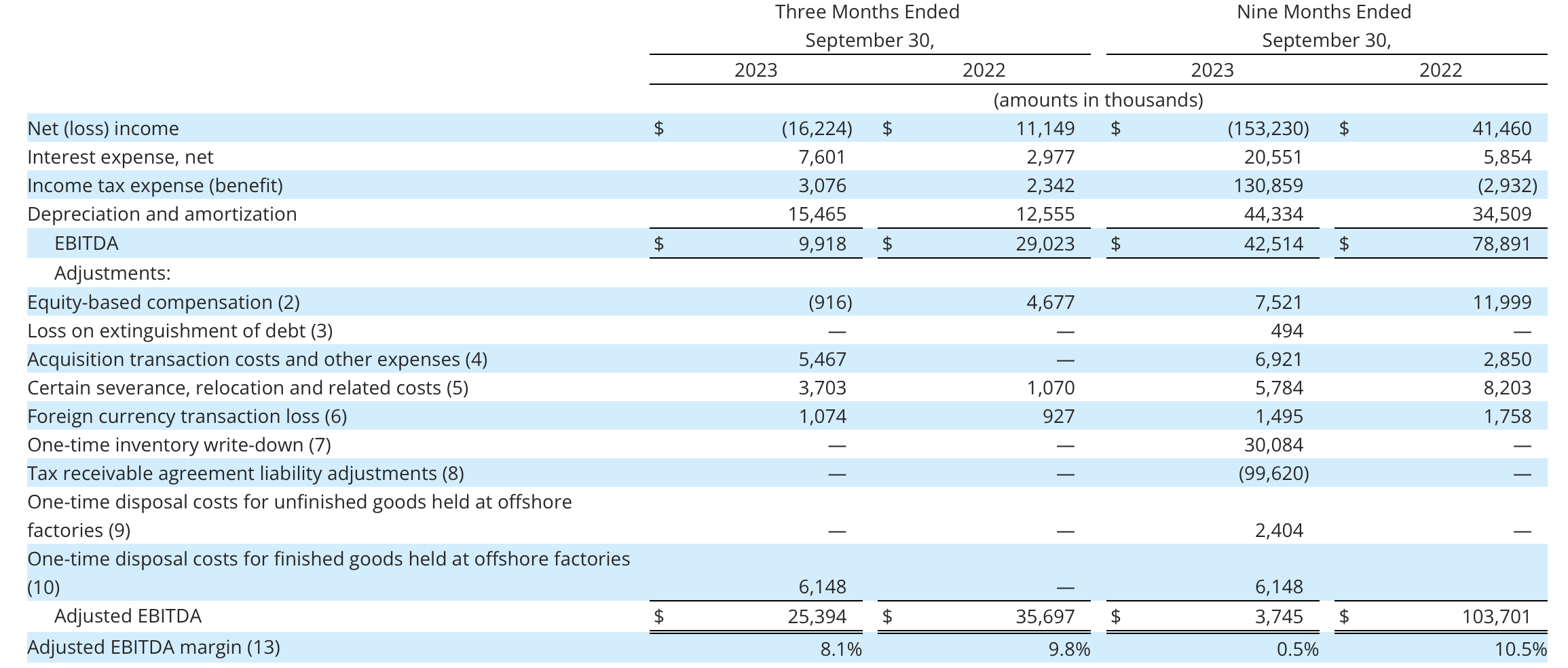

From an overall profitability standpoint, adjusted EBITDA also shrank -28% y/y to $25.4 million, while adjusted EBITDA margins declined 170bps y/y:

{kind=link}

As previously noted, the company has executed several rounds of layoffs with an eye toward removing $150 million in annual cost, but even this may not be enough to offset double-digit revenue declines if they are sustained.

Key takeaways

I continue to find little incentive for staying invested in Funko. In my view, the company's plan to reduce SKU count won't support what should be its top goal: returning to sales growth. Steer clear here and invest elsewhere.

For further details see:

Funko: A Turnaround Plan Is In Place, But It May Not Pan Out