FNKO - Funko: Beware Of Rising Debt And Profit Holes

2023-06-21 03:29:26 ET

Summary

- Funko, a toymaker known for its Pop! figurines, has seen its share price recover.

- Despite a raised profit outlook for FY23, investors should be cautious due to uncertain macro impacts, declining gross margins, and limited liquidity.

- Funko's channel partners are squeezing inventory, which may limit the brand's shelf visibility to end customers.

Investor interest in small-caps and taking on risk has soared since the start of May, and many relatively unknown stocks have seen massive leaps in valuation over the past few months. Amid buoyant sentiment for a near-term end to interest rate hikes and a relatively short-lived recession, investors should be careful not to assume that a rising tide will lift all boats: as fundamental performance is widely disparate between individual stocks.

Funko ( FNKO ), a toymaker best known for its Pop! figurines that revolve around pop culture brands, has seen its share price recover ~12% year to date, while also nearly doubling from a YTD low near $7 that the stock hit in March. The big question here: what's driving the upside?

Broadly speaking, investors are encouraged that the company's sales declines are not as bad as expected (driven both by strong category performance of the company's Loungefly line, a backpacks/accessories company that Funko acquired in 2017; as well as unusually strong performance in Europe while most other markets saw double-digit declines), as well as a raised profit outlook for FY23 following recent cost cuts and a beat to EBITDA expectations in Q1.

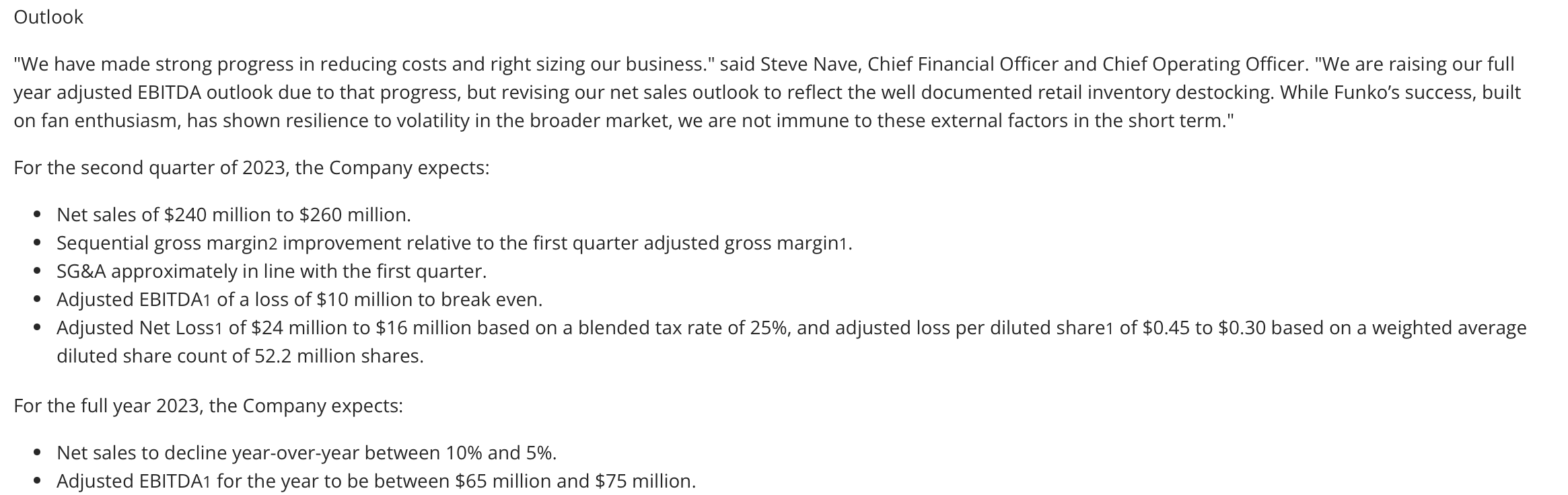

Now for FY23, Funko is guiding to $65-$75 million in adjusted EBITDA, versus a prior view of $50-$75 million:

{kind=link}

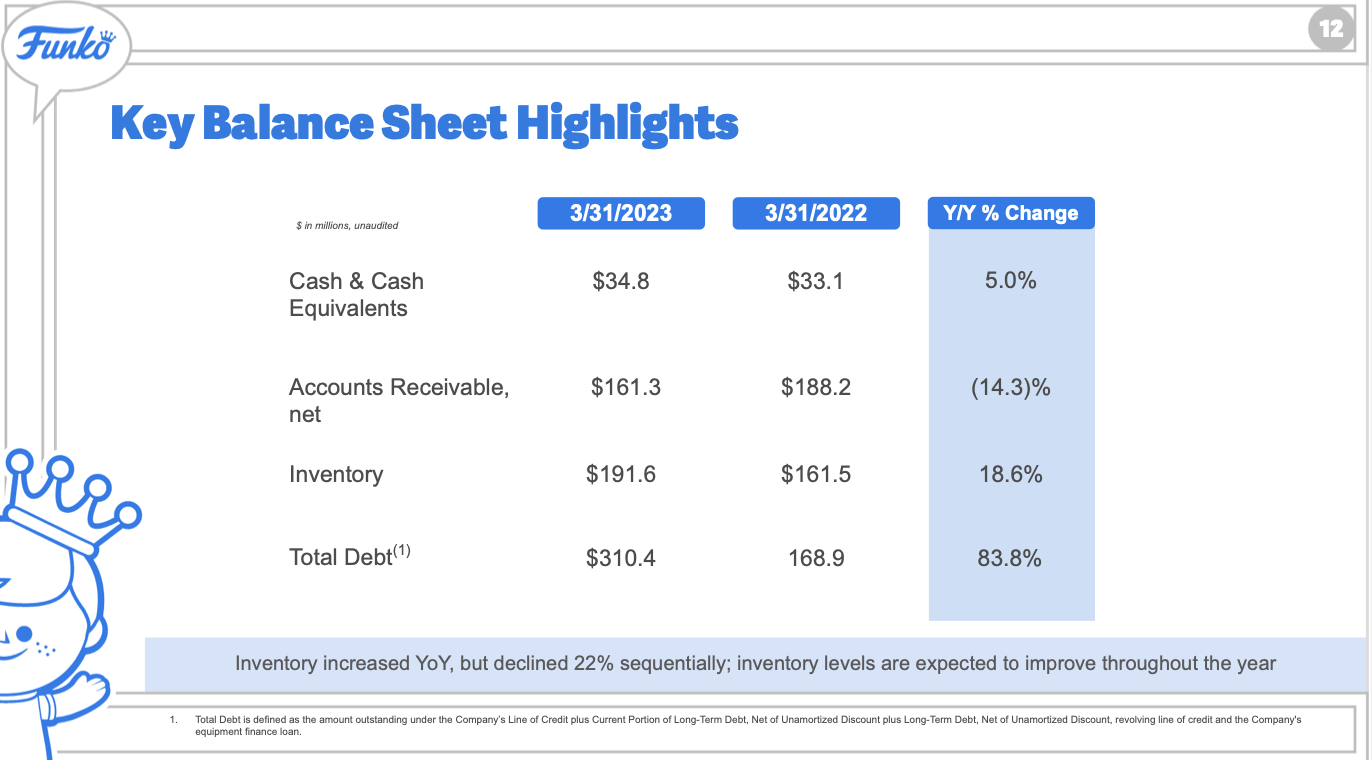

Funko's valuation has responded to the midpoint of adjusted EBITDA shifting upward. At current share prices near $12, Funko trades at a $626.6 million market cap. After netting off the $310.4 million of debt and $34.8 million of cash on the company's most recent balance sheet, the company's resulting enterprise value is $902.2 million, putting the stock's valuation at 12.9x EV/FY23 adjusted EBITDA .

While Funko can be considered cheap against a "trough year" EBITDA in FY23, we still can't forget a number of red flags that are working against this company's favor:

- Macro impacts uncertain. Needless to say, Funko products are not consumer staples. Especially as the company's reseller partners pull back, the company's path to growth in 2023 and beyond is unclear.

- Gross margins are declining. Funko may be discounting to move product, which is reflecting in multi-point reductions in gross margins year over year. And especially as Funk's fad-based products continue to shift, inventory write-downs may become more of a "business as usual" phenomenon.

- Funk's liquidity is extremely limited, with the company down to critical levels of cash while also taking on more debt on its line of credit to finance current losses.

More on the last point above: you can see in the chart below how dramatically debt levels have expanded year over year:

{kind=link}

All in all, I remain neutral on Funko. I'm not sure that the company's slight boost to its adjusted EBITDA estimates warrant the sharp rise in stock prices that we've seen over the past month, nor do I think opex cost cuts will necessarily be enough to combat gross margin declines and revenue decay. I'm more comfortable staying on the sidelines here until we either get better fundamental visibility or Funko's share price retreats back down.

Q1 download

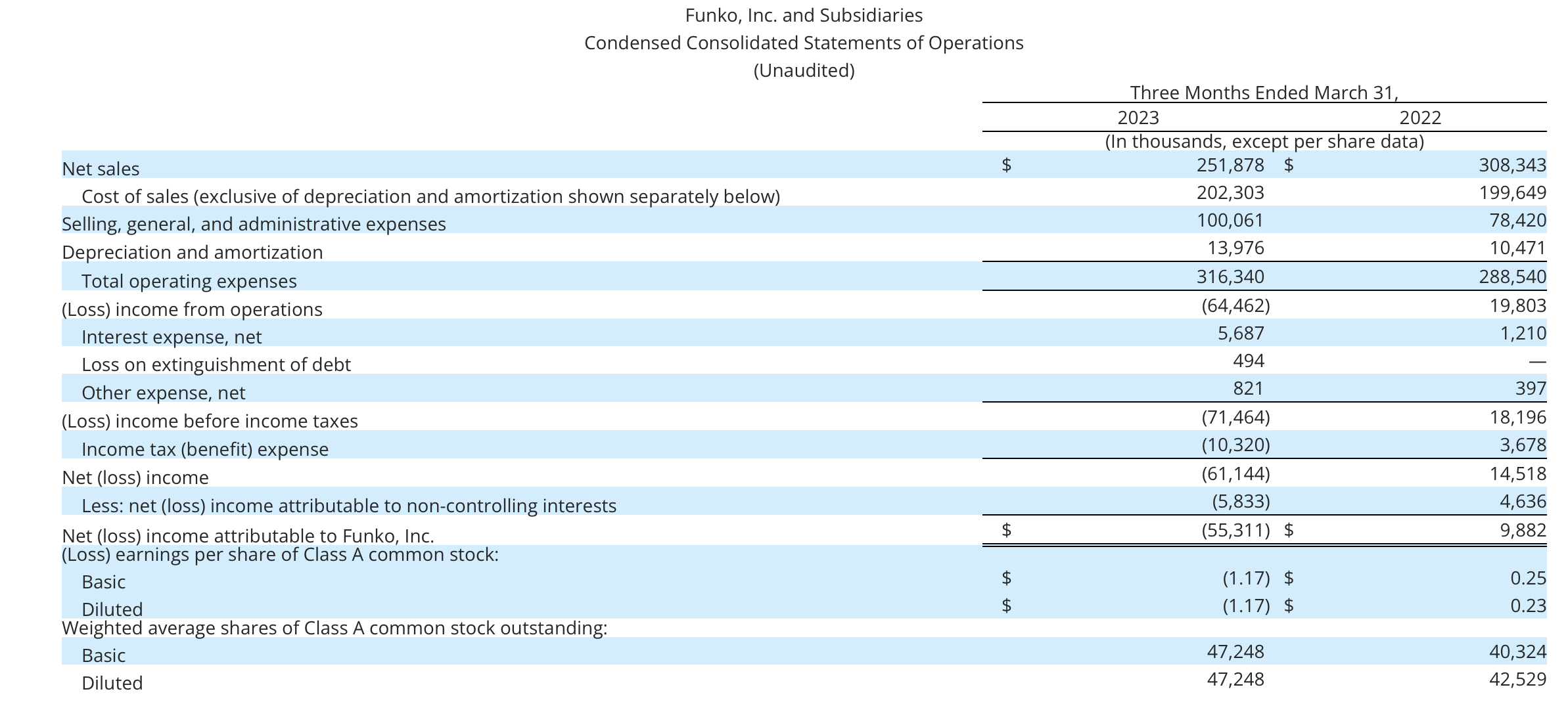

Let's now go through Funko's latest quarterly results in greater detail. The Q1 earnings summary is shown below:

{kind=link}

Funko's revenue declined -22% y/y to $251.9 million, though this came in higher than Wall Street's expectations of $235.6 million (-26% y/y). The company is dealing with a double-whammy of weaker end-customer demand as consumer spending softens, plus retail partners being more cautious on ordering inventory (which, if this ends up reducing Funko products' prominence on retail shelves, may hurt end-customer demand even more).

From a geographical basis, the U.S. declined -23% y/y, matching international markets ex-Europe. Europe, strangely, was the only geo that saw growth at +4% y/y.

Margins were another red flag. Adjusted gross margins declined 370bps y/y to 31.6%, down from 35.3% in the year-ago quarter.

{kind=link}

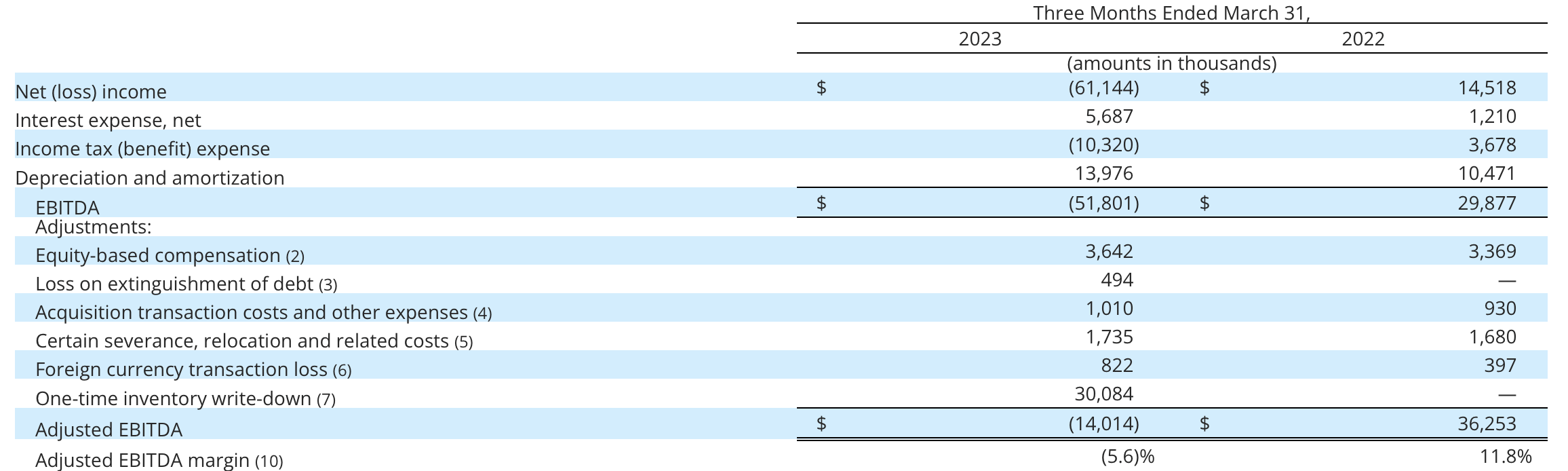

The company made a big one-time adjustment here for inventory write-downs worth $30.1 million (12 points of gross margin added back for the quarter). I'd argue here, however, that write-downs are going to be a very normal part of Funko's business (though the magnitude may not always be this high). As the company always invests in fad-based recent trends, the company is continually running the risk of producing excess inventory that ages and becomes obsolete very quickly.

This being said, the company is working on several levers to improve gross margin, including reducing container storage needs and increasing pricing. Per CFO Steve Nave's remarks on the Q1 earnings call :

I'll start with our efforts to improve our gross margin. Last quarter, we described the container rental charges we were paying, which peaked at just over a $100,000 per day. This was our most immediate action item and I'm pleased to report that as of the end of the quarter, we've eliminated all excess containers. We were able to accomplish this work much more quickly than we originally anticipated. The introduction of a price increase on our exclusive products is the second gross margin lever we've been focused on. In Q1, we successfully wrapped up negotiations on this action with our retail partners and we are on track to receive the full benefit of this pricing action by the third quarter of this year. Finally, we've made strides on our efforts to drive efficiency in our product costs. We've instituted a competitive bidding process with our manufacturers and are currently implementing design, cost, tracking and reduction initiatives."

And as shown in the chart below, last year's adjusted EBITDA profits swung to a loss of -$14.0 million, representing a -5.6% margin - down 17 points from the year-ago Q1.

{kind=link}

The company is expecting adjusted EBITDA to improve to a single-digit loss margin in Q2, and to swing positive in the second half of the year as opex cost takedowns kick in.

Key takeaways

Though arguably a value stock, I see plenty of risk in Funko as channel partners continue to pull back their orders and as the company works through gross margin challenges. Maintain caution here, especially after the recent rally.

For further details see:

Funko: Beware Of Rising Debt And Profit Holes