FNKO - Funko: Expect Pressure On Revenue Growth And Margins Hold

2023-09-04 23:52:34 ET

Summary

- According to the results of 2Q 23, Funko's revenue decreased by 24% YoY, while operating loss (% of revenue) reached 12.7%.

- The company continues to reduce the range and implement initiatives to reduce operating costs.

- I expect pressure on both revenue growth and operating margin to continue in the coming quarters.

Introduction

Funko (FNKO) shares have fallen 35% YTD. Despite the fact that the quotes are down a lot and the company is valued relatively cheaply by multiples, I think it's still not the best time to go long.

Investment thesis

In my personal opinion, revenue and operating margin growth will continue to be under pressure in the second half of 2023. First, I don't expect we can see a quick recovery in consumer spending, even if inflation slows down, because consumers continue to face higher everyday spending. Secondly, the company's management has lowered the guidance for 2023. Third, I don't expect cost-cutting initiatives to be of significant support to financial results in the coming quarters, while operating margins continue to be in negative territory.

Company overview

Funko designs and distributes toys (vinyl figures, action toys, etc.), clothing, housewares, and accessories. The main revenue segments are wholesale and direct to consumer. The main markets are the USA (71% of revenue) and Europe (21% of revenue).

2Q 2023 Earnings Review

The company reported worse than investors expected . The company's revenue decreased by 24% YoY . The segments of the USA and Europe made the greatest contribution to the decline in sales, where revenue decreased by 26% YoY and 20% YoY, respectively.

Revenue by geography (%) (Company's information)

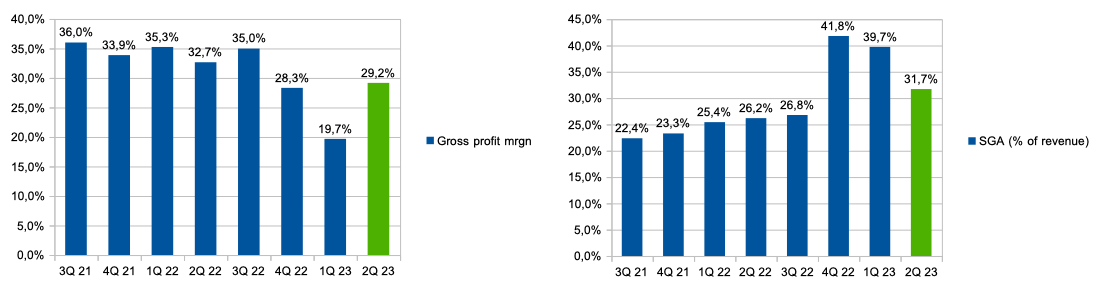

Gross profit margin decreased from 32.7% in Q2 2022 to 29.2% in Q2 2023 due to an increase in the amount of inventory that was received back, while the company faced increased freight costs. SGA spending (% of revenue) increased from 26.2% in Q2 2022 to 35.7% in Q2 2023 due to reduced economies of scale. However, SGA spending (% of revenue) improved compared to the previous two quarters due to cost optimization for distribution centers and strict cost control.

Gross profit margin and SGA (% of revenue) (Company's information)

{kind=link}

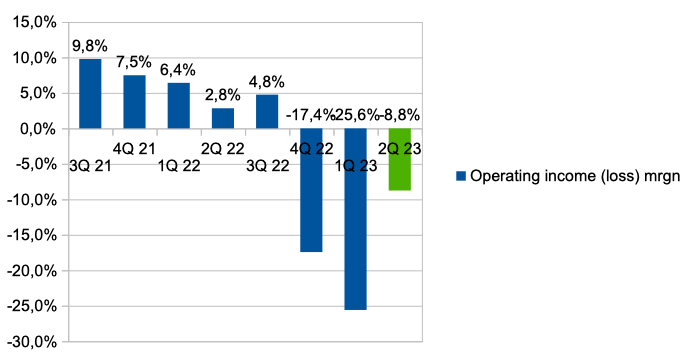

Thus, the operating loss (% of revenue) increased to 12.7%, while in the 2nd quarter of 2022 the company showed an operating profit of 2.8%.

{kind=link}

According to the results of the 2nd quarter of 2023, short term debt amounted to $141 million (about 46% of the total debt). In accordance with the New Revolving Credit Facility , which regulates the company's short-term debt, at the moment the limit on the credit line has been fully used. Although the cash balance is about $37 million, I believe that there are risks of increasing leverage.

In addition, the company has published guidance for 2023. Thus, management expects revenue to be around $1,050 - $1,120 million, which implies a decrease in revenue by 15% -21% compared to 2022. If we look at the second half of 2023, then management expects a decrease in revenue by 10% -20% compared to the second half of 2022. You can see the details in the chart below.

Guidance 2023 (Company's information)

My expectations

On the one hand, I like the fact that the company continues to reduce the number of SKUs (planning to cut about 30%) and optimize operating costs, however, on the other hand, I do not expect that we can see a significant improvement in the second half of 2023. First, I don't think we can see much support from the demand side in view of the ongoing pressure on consumer real incomes and the ongoing inventory destocking process among the company's main customers.

Our second quarter performance was impacted by ongoing inventory destocking by our larger wholesale customers. We anticipate this softness will continue in the second half of the year.

Secondly, I do not expect that we may see an increase in the prices of the company's products during 2023, as this may lead to a decrease in market share. If we look at management's comments during the Earnings Call after the release of financial results, we can see that the company expects support from rising prices only in 2024.

Separately, I would like to draw attention to the company's initiatives to reduce operating costs. In the 2nd quarter of 2023, management continued to reduce staff (about 17%), so we can see additional savings of about $38 million in annual terms. Of course, this initiative will have a positive effect on the operating profitability of the business, however, in my personal opinion, it will not allow the company to significantly improve financial performance. So, if we assume that the benefit from the reduction in staff will be evenly distributed over the next 4 quarters of $9.5 million, then in the example of 2Q 23 we can see that the savings will be just over 10% of SGA, while the cost of SGA ( % of revenue) will continue to be significantly higher than during 2021 and the first half of 2022.

In addition to the $20 million in savings from last week's workforce reduction, we've identified another $18 million in non-headcount related annualized cost savings, for a total of approximately $38 million of annualized cost savings related to the most recent workforce reduction

Risks

Margin: rising logistics costs and declining economies of scale could put pressure on a business's operating margins.

Macro (general risk): higher inflation and pressure on real incomes could lead to lower consumer spending in the discretionary segment, which could have a negative impact on business revenue growth.

Drivers

Revenue: a normalization of inventory levels at major wholesalers such as Walmart (NYSE: WMT ) and Target (NYSE: TGT ), an effective marketing campaign, new product and collaboration launches, and rising real consumer incomes could support the company's revenue growth in the future.

Margin: increasing prices for the company's products, reducing production and supply chain costs can have a positive impact on the dynamics of the operating profitability of the business.

Valuation

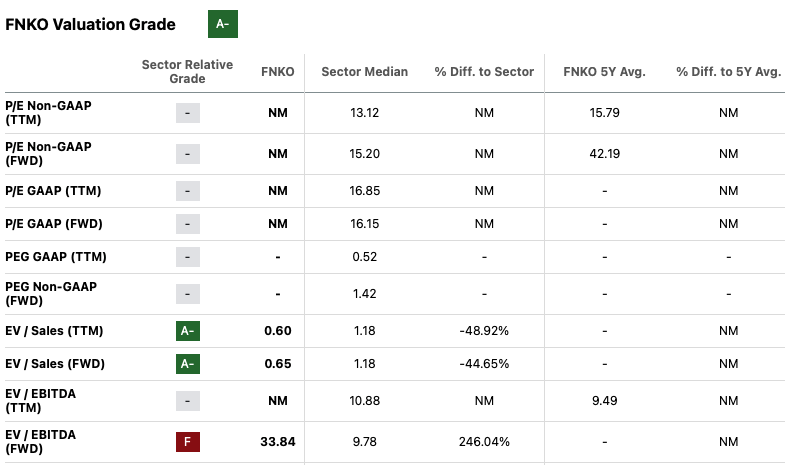

The current Valuation Grade is A-. On an EV/Sales ((FWD)) multiple, the company trades at 0.65x, implying a discount to the sector median of around 45%. I believe that investors should not make a decision to buy shares based only on a low valuation in accordance with the multiple, as stock quotes can be under pressure for a long time in the absence of growth catalysts or data on improving fundamental trends (revenue dynamics, profitability level).

{kind=link}

Conclusion

Thus, at the moment my recommendation is HOLD. Although the company's stock is not expensive, I don't see any additional growth drivers/catalysts for the stock in the coming quarters. I believe that investors need to wait for financial results for the next quarters before making a purchase decision. I will gladly change my recommendation to buy if I see signs of a normalization in demand for the company's products and an improvement in the profitability of the business.

For further details see:

Funko: Expect Pressure On Revenue Growth And Margins, Hold