FNKO - Funko: Profit Compression Makes Me More Wary

Summary

- Shares of Funko have dropped a sharp 40% since reporting Q3 results in November, and the stock has only enjoyed a modest YTD recovery alongside other growth stocks in January.

- Though growth sustained well in Q3, guidance implies very little growth for Q4 amid reseller caution.

- Funko's infrastructure investments have also led to deep dents in profitability and liquidity that make it difficult to be gung-ho on the stock.

- I'd recommend moving to the sidelines here until fundamental headwinds clear.

Amid a potential rebound in 2023 and continued high volatility in the markets, investors have to be diligent about consistently reviewing the positions in our portfolios, especially where fundamental stories have changed.

I'm putting Funko ( FNKO ) under this microscope. This collectibles and toymaker had been one of my favorite quirky, little-known small cap plays, but with fundamentals likely darkening heading into 2023, it's a good time to trim the position. The company reported dismal Q3 results, and immediately afterward announced a leadership transition that re-instated a former CEO as well as beginning the search for a new CFO .

Year to date, shares of Funko have made a modest ~12% bounceback, but is still far from recovering the ~$20 levels from pre-November earnings. In my view, the path to get there has become tremendously challenging.

I am downgrading my view on Funko to neutral and am recommending that investors move to the sidelines. I now view this company as a relatively balanced grab bag of positives and negatives.

On the bright side for Funko, I'm still holding onto these longer-term bullish drivers:

- Unparalleled ability to source and monetize the best content. From Fortnite to Pokemon to Marvel and other brands, Funko's ability to nab the best content is unrivaled. No single brand dominates Funko's revenue, so it's well-diversified to be the beneficiary of a general rise in entertainment and pop culture.

- International growth push. Though primarily a U.S. company now, Funko is driving strong growth overseas, where it is growing revenue at a 30-40% y/y clip.

- New potential revenue stream in NFTs. Funko recently acquired a company called TokenWave, which enabled it to finally get its skin in the NFT craze that kicked up amid the pandemic. Funko notes that its first few token offerings have "sold out in minutes," potentially opening the door to an entirely new and fast-growing revenue stream going forward.

The near term, however, looks murkier with these red flags to watch:

- Profitability is waning. The company reported declines in gross margin, while at the same time its investments in infrastructure have dramatically boosted SG&A expenses at the expense of operating margins.

- Liquidity stretched. As a result of decaying profitability, Funko's liquidity has also dropped to razor-thin levels

- Macro impacts uncertain. Needless to say, Funko products are not consumer staples. Especially as the company's reseller partners pull back, the company's path to growth in 2023 and beyond is unclear.

In my view, the best move here is to migrate to the sidelines.

Worrying trends will leave an overhang throughout 2023

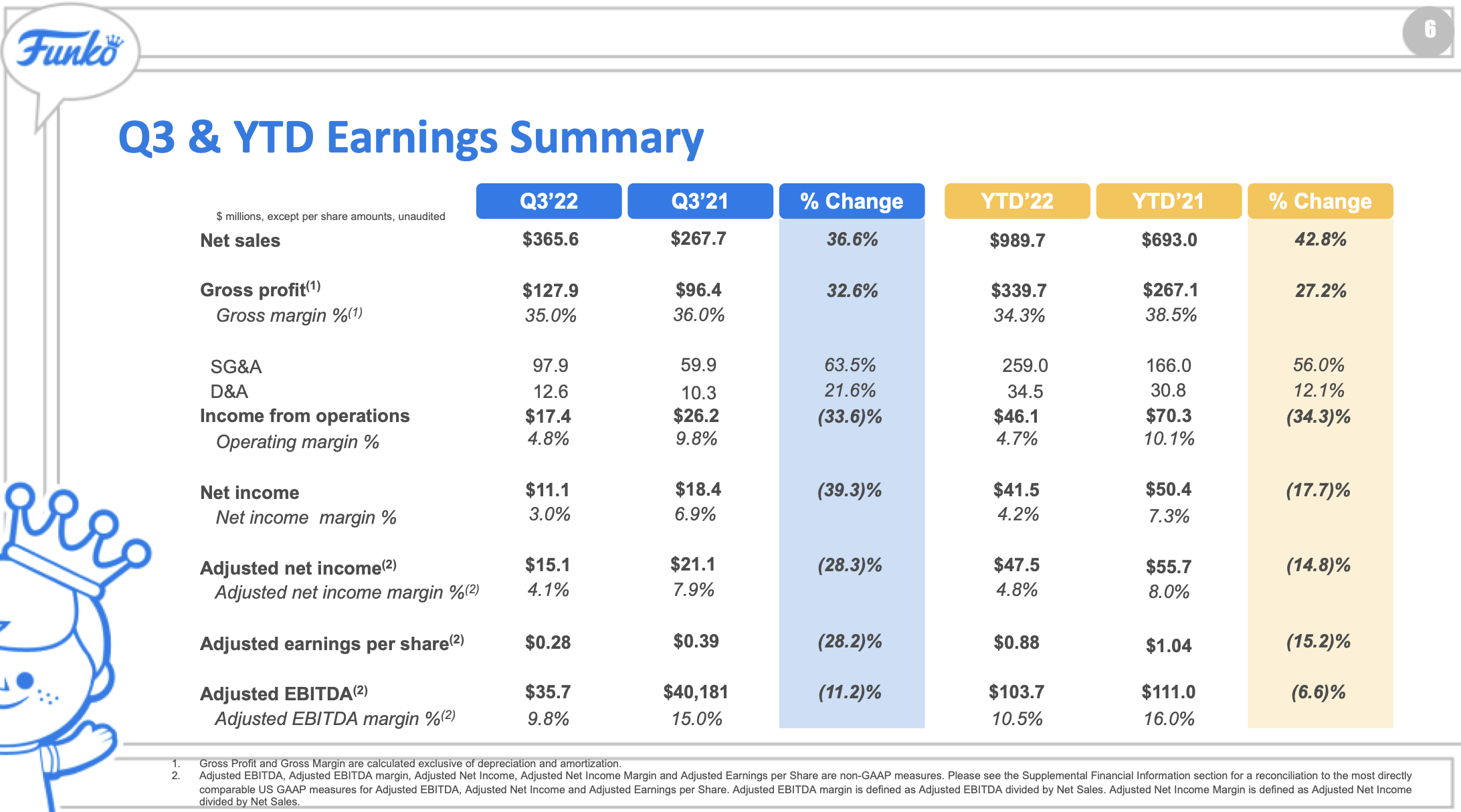

Let's zoom into what happened in the business in the third quarter (reported in November) to understand what risks are ahead for Funko. A summary of the Q3 results is shown below:

{kind=link}

Growth was fine, so far. Funko grew revenue at a 37% y/y pace to $365.6 million, coming in well ahead of Wall Street's expectations of $319.6 million (+19% y/y) despite decelerating sharply from 63% y/y growth in Q2.

Guidance, however, was a bit more worrying. The company's FY22 revenue range of $1.29-$1.33 billion implies $300-$340 million in revenue for the fourth quarter, which is a range of -4% y/y to 1% y/y growth.

Per CEO Andrew Perlmutter's remarks on the Q3 earnings call :

Turning to channel highlights. Within wholesale, we saw strong growth from our mass partners despite broadly high levels of inventory at retail. While Funko products continue to be traffic drivers for our retail partners, we have seen some order delays or reductions given the broader economic climate.

Our results in direct-to-consumer, which I'll speak to you shortly, highlight the continued strength of the Funko brand. However, we do expect these wholesale order reductions and delays to persist in the short term given the current macro environment. These expectations have been reflected in our full year guidance.

Our DTC channel saw another quarter of strong double-digit growth exceeding 30% and representing what we like to call our single largest customer by net sales. Average order value and traffic across our e-commerce sites were both up strong double-digits."

In other words - Funko moves a lot of product through its reseller channel. If partners are feeling pressure and end up de-stocking Funko products / not replenishing inventory to standard levels, end-customer sell through could end up getting hurt.

The other concern is on profitability. Gross margins declined by 100bps y/y, though the company noted that there was some impact from timing of freight costs that should correct in future quarters.

However, we do note that SG&A costs expanded by 64% y/y. The company notes that this was driven by investments in infrastructure, particularly around warehouse management, to support growth. This has taken a huge bite out of operating income, which declined -34% y/y to $17.4 million, while operating margins shrunk in more than half (500bps) to just 4.8%. Adjusted EBITDA margins, meanwhile, also slipped 520bps to 9.8%.

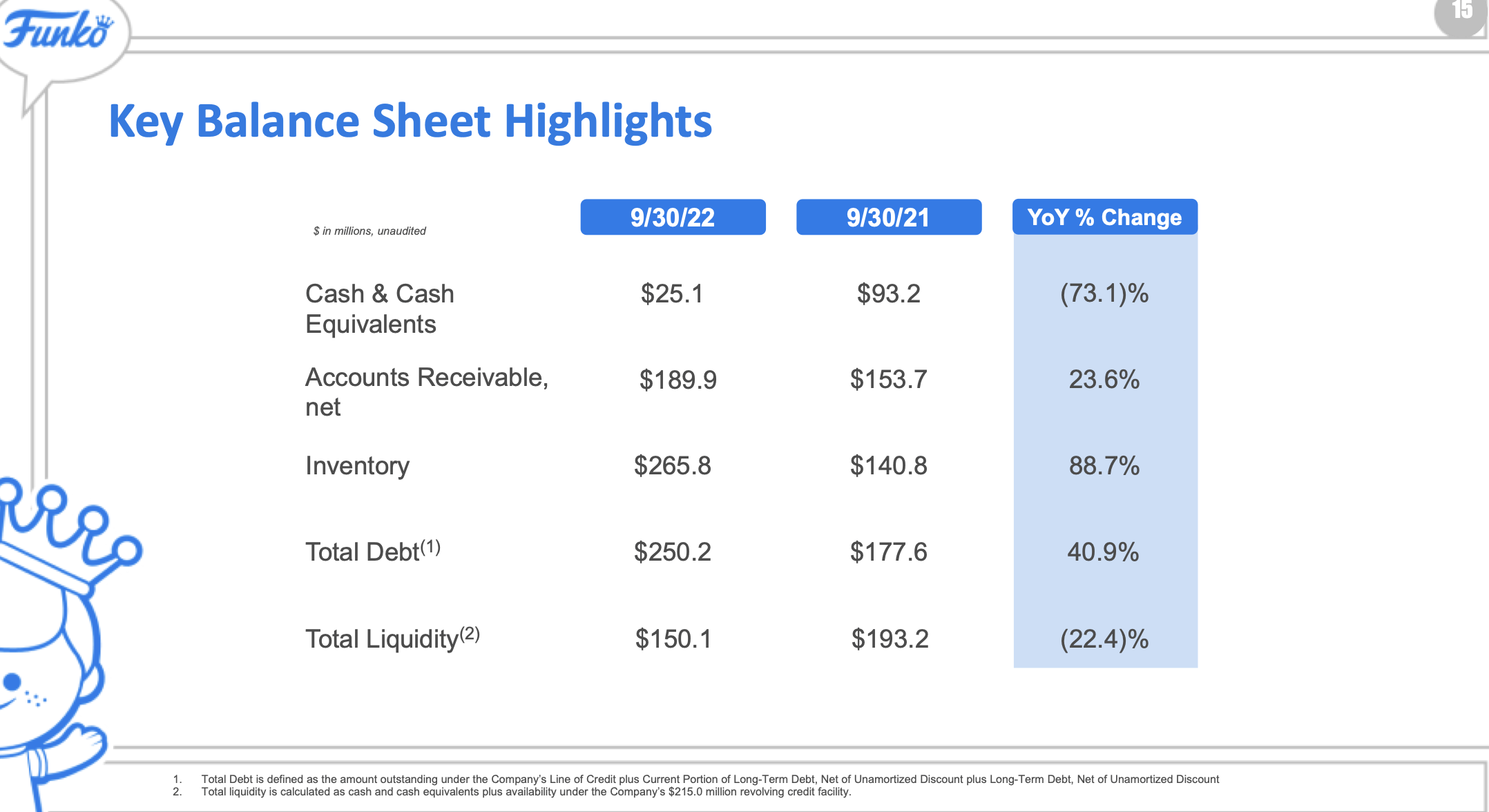

We also need to watch the impacts to liquidity. Funko's cash balances dropped to a dangerously low $25 million as of the end of Q3, while debt also rose to $250 million. The company does have a lot of inventory to unwind heading into Q4 - and in a fad-driven consumer products business, this could be a dangerous position for Funko to be in as 2023 unfolds.

{kind=link}

Key takeaways

With giant downward swings to profitability and no line of sight to recovery, as well as potential risks to growth as channel partners take a cautious stance on ordering inventory from Funko, there is a lot of room for trends to turn south for the company in 2023. With so many other great growth names still on sale after last year's decline, I'd recommend moving to the sidelines on Funko.

For further details see:

Funko: Profit Compression Makes Me More Wary