FNKO - Funko: Run For The Exits (Rating Downgrade)

2023-10-25 17:24:24 ET

Summary

- Funko's stock has declined by ~25% year to date due to a decimation of its business, driven by the behavior of its resale partners.

- The company's top line has deteriorated further, leading to a reduction in its full-year revenue outlook by $140 million (or roughly 10% y/y).

- Red flags include a potential decline in sales due to partners pulling back, declining gross margins, and limited liquidity with high levels of debt.

It's no secret that this year has been quite painful for investors in small and mid-cap stocks, as higher interest rates have dramatically devalued the prospect of future profits. In most cases, however, many of the underlying businesses have continued to showcase strong fundamentals, with their stock price moves largely uncorrelated to quarterly results that have more or less defied the macro recession.

Funko ( FNKO ), however, is in a quite different boat. The collectibles and toymaker has seen a decimation of its business, largely driven by the behavior of its resale partners. Today, the stock sits down ~25% year to date - and even that, in my view, is generous.

I last wrote a neutral opinion on Funko in June of this year. Since then, the company's top line has deteriorated further, and the company has instilled a board member as interim CEO while it looks for permanent leadership. Simultaneously, the company has laid off 18% of its headcount while also planning to shrink the diversity of its product offerings, hoping to focus on core products to minimize an inventory glut.

The outcome of these strategic moves is still unknown, but based on the sharp decay that we've seen in the company's top line, as well as Funko's recent guidance cut to the full year, I'm now rotating my viewpoint on the stock to bearish.

{kind=link}

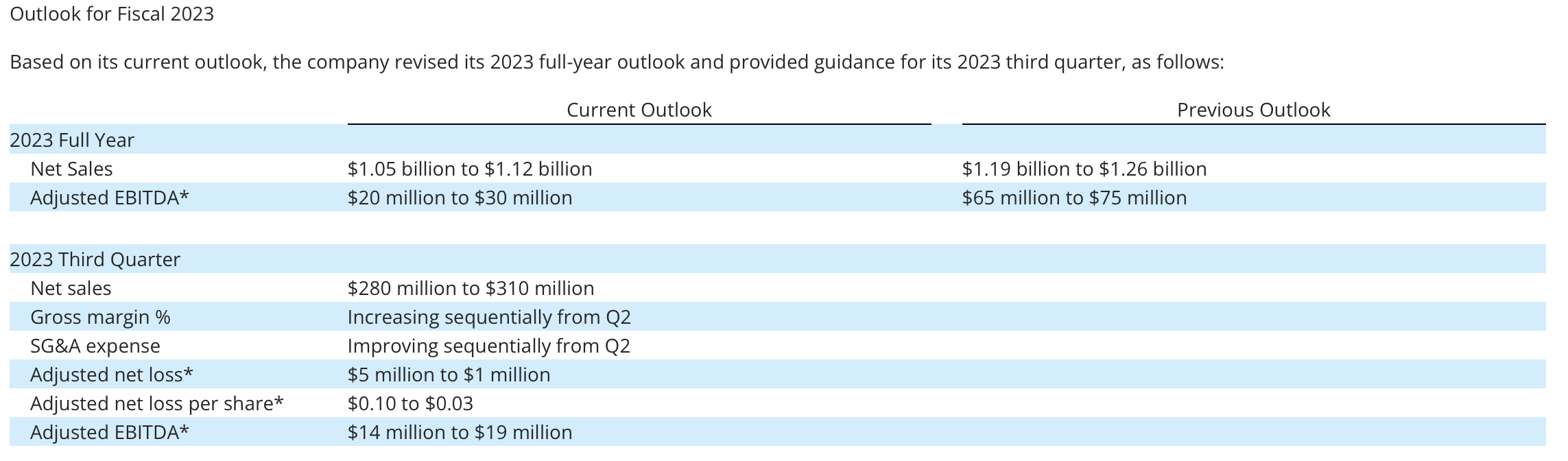

The above snapshot showcases the depth of Funko's dire straits. The company was always already planning for a contraction in revenue this year - its prior $1.19-$1.26 billion revenue range represented a decline range of -5% to -10% y/y. Now, however, its reduction of $140 million to the full-year revenue outlook puts growth at -15% to -20% y/y. At the same time, the company is expecting adjusted EBITDA at about a third of prior expectations, despite deep cost cuts.

To me, here are the core red flags to watch out for:

- If partners are pulling back, will Funko still generate meaningful sales? Funko relies heavily on reseller partners to move its products. In this macro crunch, partners are pulling back on ordering inventory, ultimately limiting the visibility of Funko products. If this becomes a long-term trend, Funko's sales reach will diminish tremendously.

- Gross margins are declining. Funko may be discounting to move product, which is reflecting in multi-point reductions in gross margins year over year. And especially as Funk's fad-based products continue to shift, inventory write-downs may become more of a "business as usual" phenomenon.

- Funk's liquidity is extremely limited, with the company down to critical levels of cash while also taking on more debt on its line of credit to finance current losses.

The bottom line here: there are a number of negative trends swirling in this business. Unlike many other small-cap stocks that have simply declined because the asset class is in competition with 5%+ interest rates, Funko is also facing sharply declining fundamentals. I'd recommend moving to the sidelines here and investing elsewhere.

Q2 download

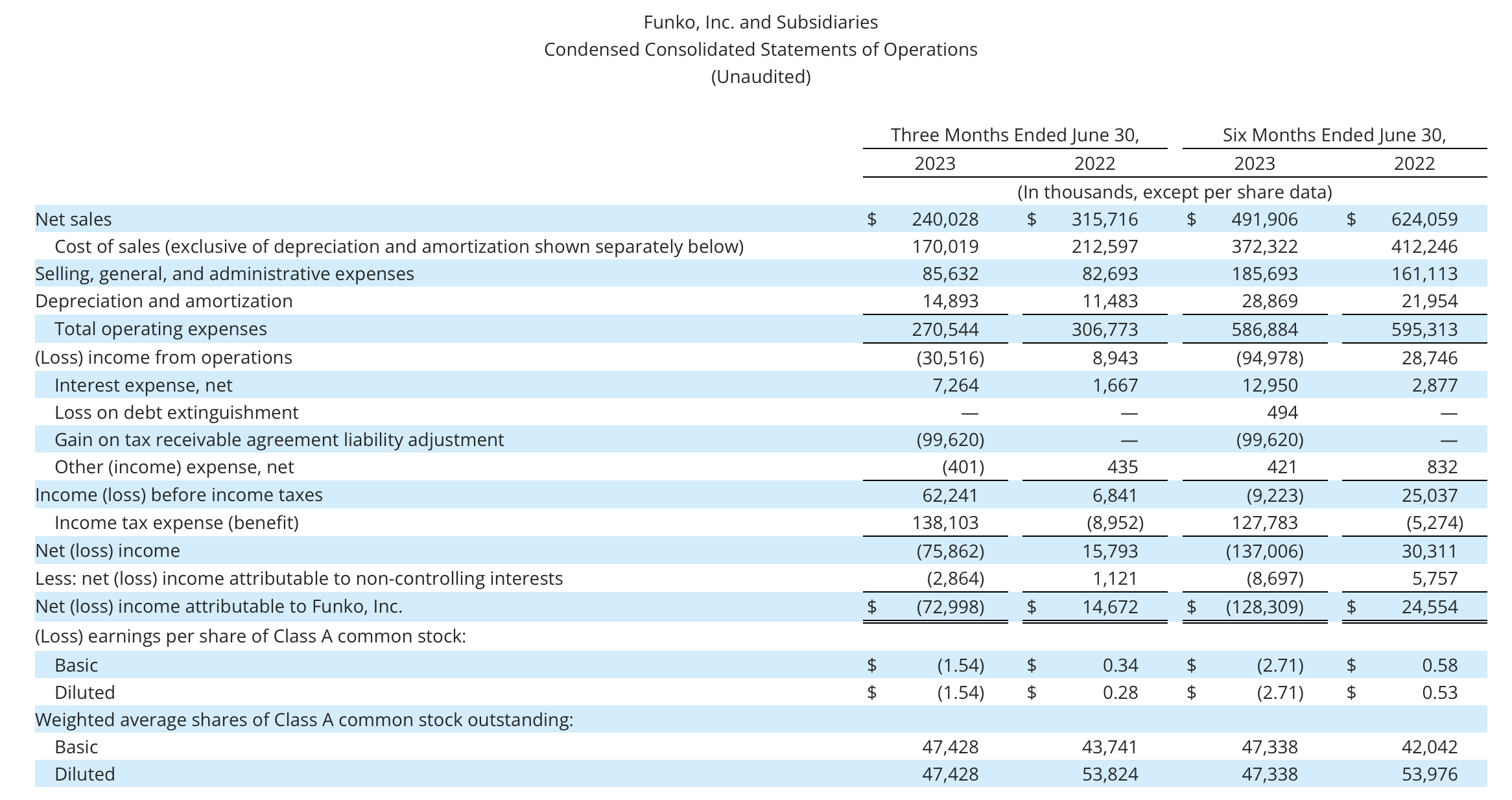

Let's now go through Funko's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Funko's revenue in Q2 declined -24% y/y to $240.0 million, missing Wall Street's expectations of $250.3 million (-21% y/y) and decelerating versus Q1's -21% y/y growth rate. Again, the core driver of the contraction here is reduced inventory shipments to resale partners, as Funko has a fairly limited DTC business. Stores, ranging from big-box to smaller retailers, have resorted to reducing inventory in order to minimize shrinkage and improve cash flow amid the tight macro environment.

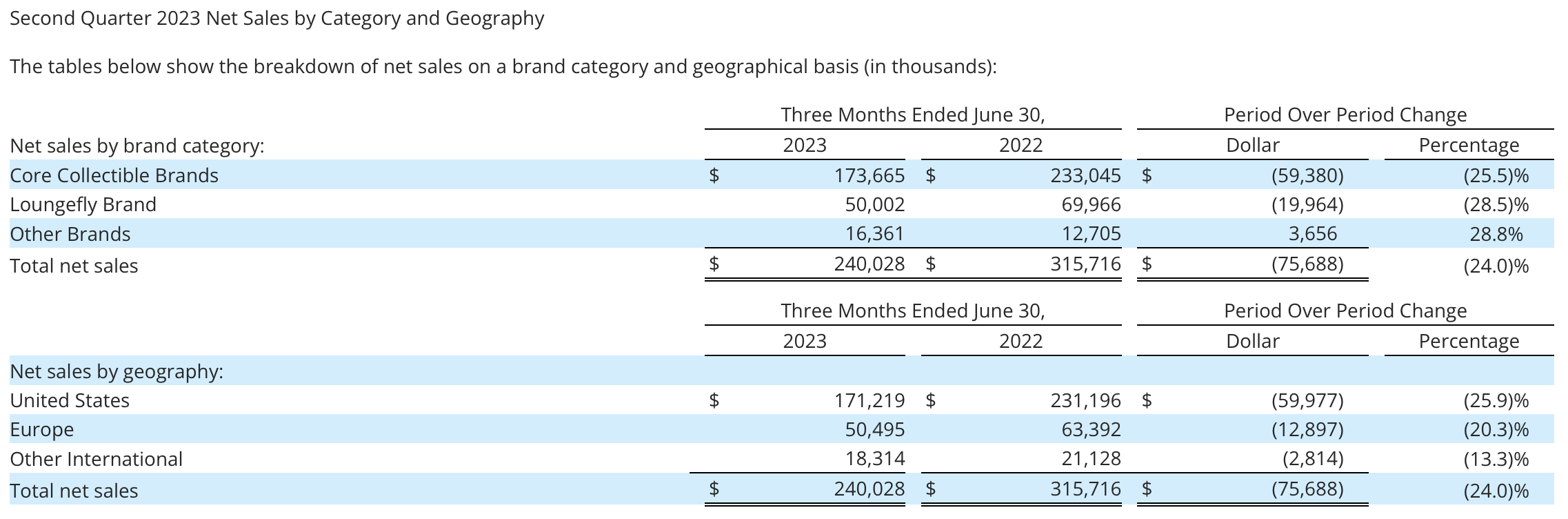

The snapshot below showcases Funko's top-line trends by geography and category:

{kind=link}

Core collectibles and the recently-acquired Loungefly (known for products such as backpacks) are both declining more than -20% y/y, while the company is seeing growth in the smaller other brands. By geography, the U.S. is seeing the sharpest -26% y/y decline, while other more emerging regions (probably helped by a lower prior-year base compare) are down "only" in the mid-teens.

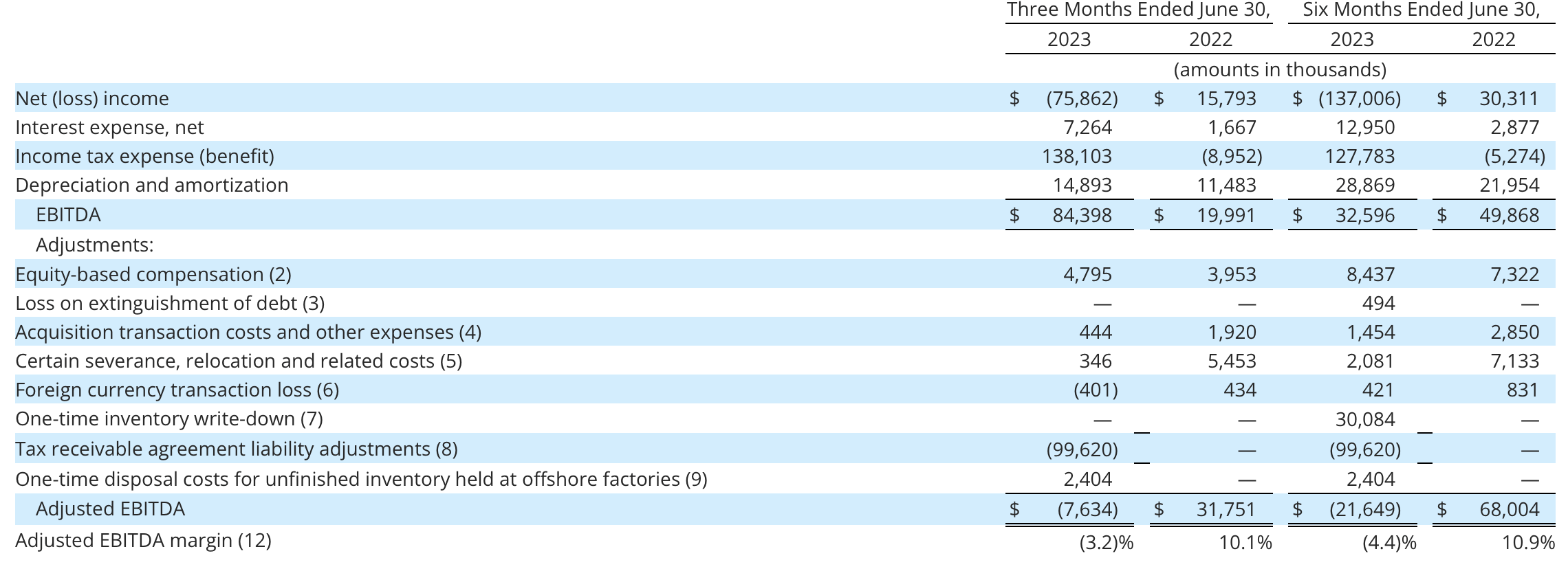

Adding insult to injury, Funko also suffered a drop in gross margins - down 350bps y/y to 29.2% in the quarter. Speaking to gross margin losses on the Q2 earnings call, CFO Steve Nave noted as follows:

Gross margin was 29.2%, which was below our expectations. This was primarily driven by two factors. One, the mix of our sales for the quarter included a higher than anticipated percentage of inventory that was received back when freight costs were much higher, resulting in higher amortization of capitalized inbound freight costs than we expected. And two, customer order cancellations during the quarter resulted in a formulaic increase in our inventory obsolescence reserve."

On top of operating de-leverage driven by sharp top-line losses, this caused Funko's adjusted EBITDA to slip to a -$7.6 million loss, or a -3.2% margin: thirteen points worse than the year-ago Q2.

{kind=link}

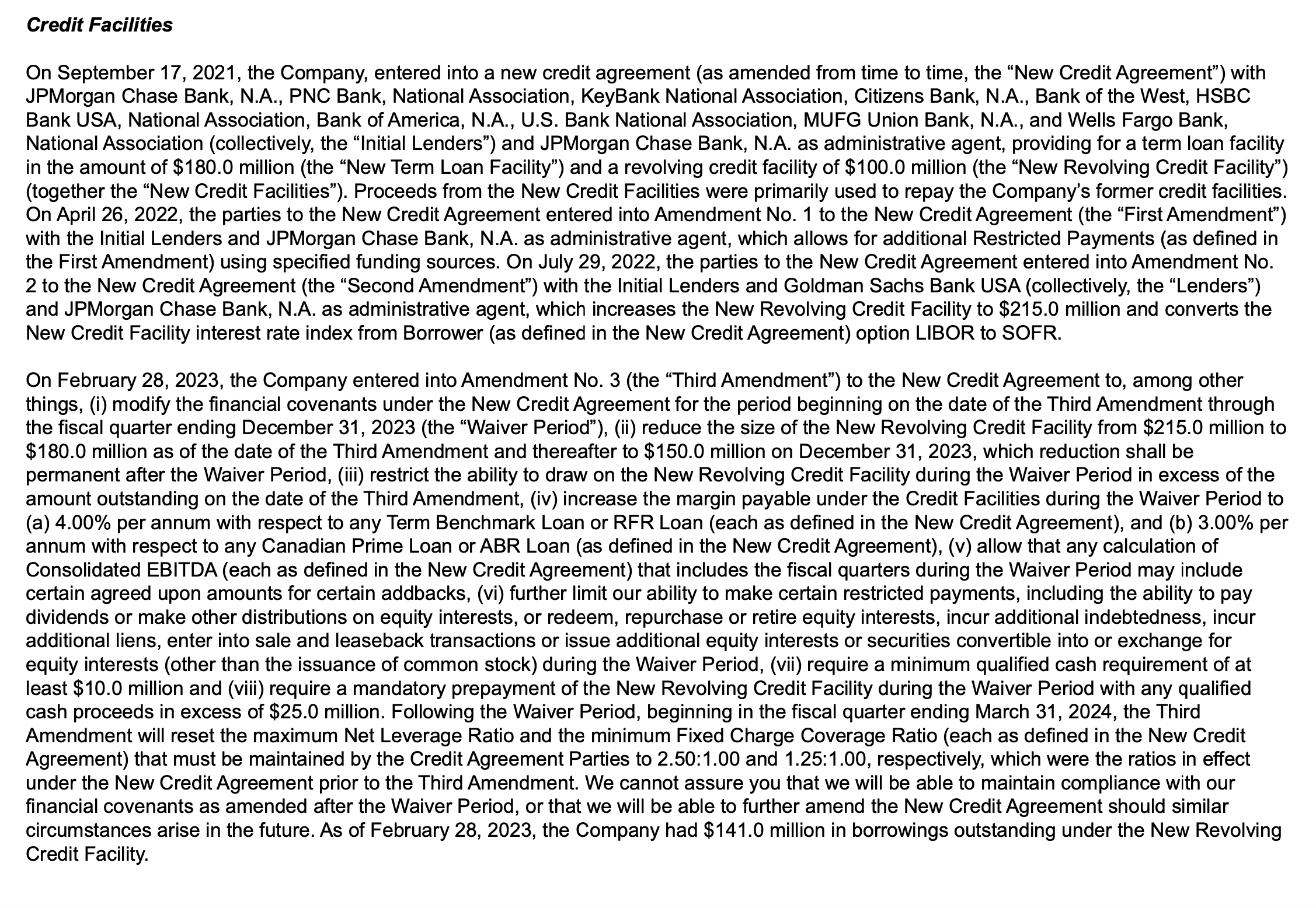

There's a direct concern here between growing losses and Funko's diminishing balance sheet. Free cash flow burn in the first half of FY23, including -$23 million of capex, was -$34.7 million. Meanwhile, Funko has only $36.8 million of cash left on its balance sheet, alongside total debt of $283.1 million.

Funko's liquidity lies almost entirely in its line of credit, of which $141 million was drawn as of the end of Q2. Parsing through its credit agreements in Funko's Q2 10-Q filing, we can see that this revolver has a max drawn capacity of only $185 million:

{kind=link}

And while the company can certainly draw down debt, note that it's punishingly expensive to do so, as this credit facility carries a premium of 4% above benchmark rates (SOFR is sitting at ~5.3% today) - which will push Funko's losses deeper.

Key takeaways

With a decimated top line, leadership turnover, a planned shrinkage of product lines, declining gross margins and deeper losses that are straining an already-tight balance sheet, there are a number of good reasons to stay away from Funko. Don't try to catch a falling knife here.

For further details see:

Funko: Run For The Exits (Rating Downgrade)