CA - Galiano Gold: Turnaround Thesis Remains Intact

Summary

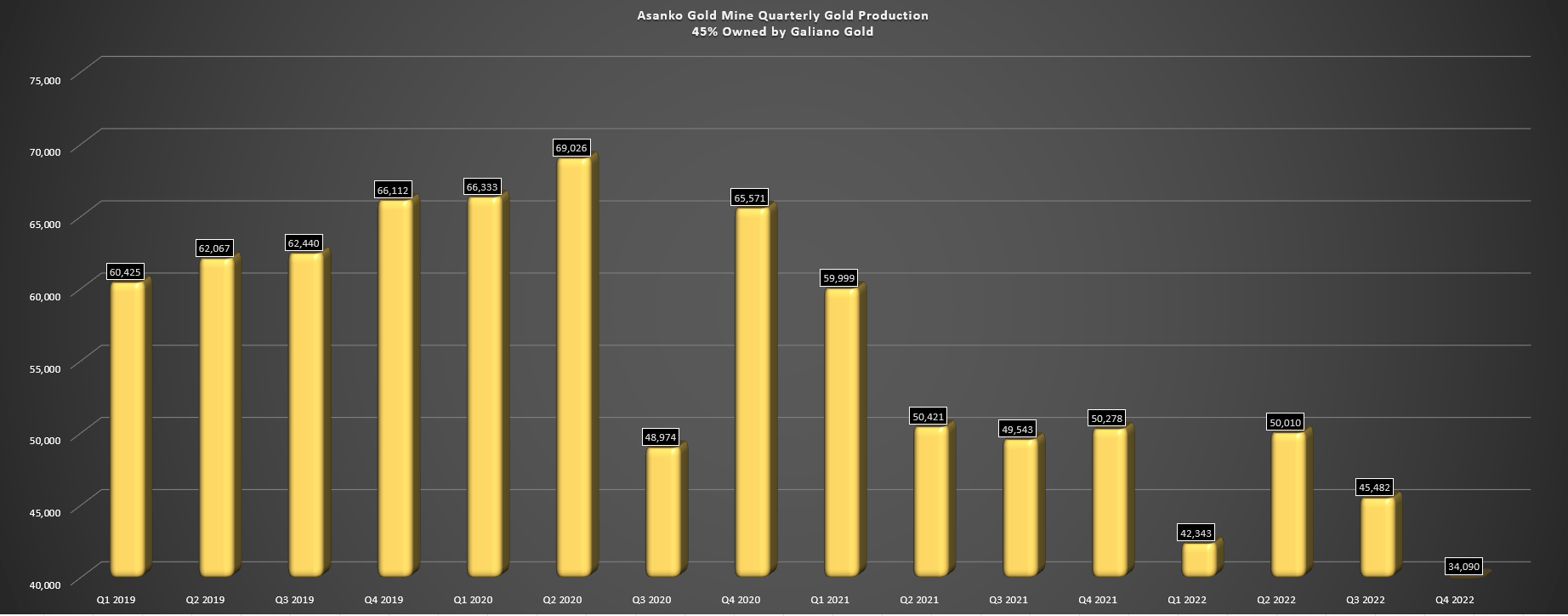

- Galiano Gold released its Q4 and FY2022 results last month, reporting quarterly production of ~34,100 ounces and annual production of ~170,300 ounces at the Asanko Gold Mine.

- This represented a significant beat vs. the top end of its updated guidance of 160,000 ounces, and a 55% beat vs. its initial guidance mid-point of 110,000 ounces.

- Notably, costs came in only slightly above the industry average despite inflationary pressures and a lower grade year helped by cost-cutting initiatives under new management.

- That said, while GAU is cheap at a sub $140 million market cap, I prefer to buy stocks sharply off their highs, not chase rallies, so I have little interest in chasing the stock here at US$0.58.

Just over two months ago, I wrote on Galiano Gold ( GAU ), noting that while I saw better value in other names in the small-cap producer space, I saw Galiano as a Speculative Buy at US$0.43. Since that update at US$0.56, Galiano has underperformed its peer group with just a 3% return since November 13th vs. a 9% return for the Gold Miners Index ( GDX ) and a more than 50% return for other names highlighted in the same period . This underperformance may be related to Galiano being overbought heading into mid-November, with it needing some time to digest its July through October gains.

Despite the recent underperformance, the Galiano turnaround thesis remains intact, and the company just delivered another solid quarter on the back of what was already a much better year than planned. In fact, FY2022 gold production at the Asanko Gold Mine came in 54% above Galiano's initial guidance mid-point of 110,000 ounces, with the production of ~170,300 ounces. This bolstered Galiano's already strong balance sheet and left the Asanko Gold Mine joint venture in strong financial shape as well. Given that the turnaround thesis remains intact, I continue to see GAU as a Speculative Buy at US$0.43. Let's take a closer look at the preliminary Q4 results below:

{kind=link}

Unless otherwise noted, all production/sales figures are on a 100% basis for the Asanko Gold Mine JV. The Joint Venture is split 50/50 for the 90% economic interest, with Ghana holding 10%. Therefore, all figures are attributable on a 45% basis to Galiano.

Q4 & FY2022 Production

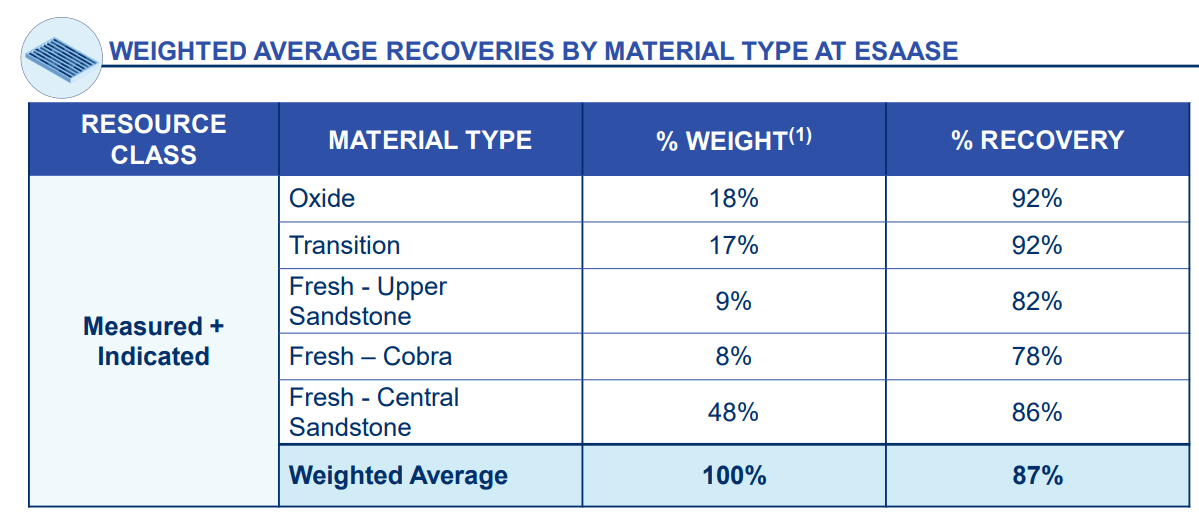

Galiano Gold released its Q4 and FY2022 results last month, reporting quarterly production of ~34,100 ounces and annual production of ~170,300 ounces at the Asanko Gold Mine. This represented a significant beat vs. its initial guidance mid-point of 110,000 ounces (provided in late March). For those unfamiliar, the company was ultra-conservative with its forecast due to weaker-than-expected metallurgical recoveries in Q1 2022 and the cessation of mining starting in Q3 2022 while technical work to support a mineral reserve was in progress. Fortunately, metallurgical test work completed last year confirmed historical gold recoveries at its Esaase deposit, and test work confirmed recoveries ranging from 78% (fresh ore) to 92% (oxide/transitional ore), with a weighted average of 87% on all types of mineralized material.

{kind=link}

Digging into the Q4 results, production was much lower sequentially (~34,100 ounces, with this directly impacted by the fact that mining was completed at Akwasiso in the previous quarter and the company was only processing stockpiles in Q4. This resulted in a much lower head grade to the mill, with grades of 0.84 grams per tonne of gold in Q4 vs. 1.10 grams per tonne of gold in Q3. Meanwhile, recovery rates were also much lower sequentially (79.7% vs. ~88% in Q3), related to the much lower grades processed in the period. Still, despite the Q4 production dip, the better-than-expected performance in Q1 through Q3 when Galiano was mining allowed the company to trounce its FY2022 forecasts.

Galiano Gold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

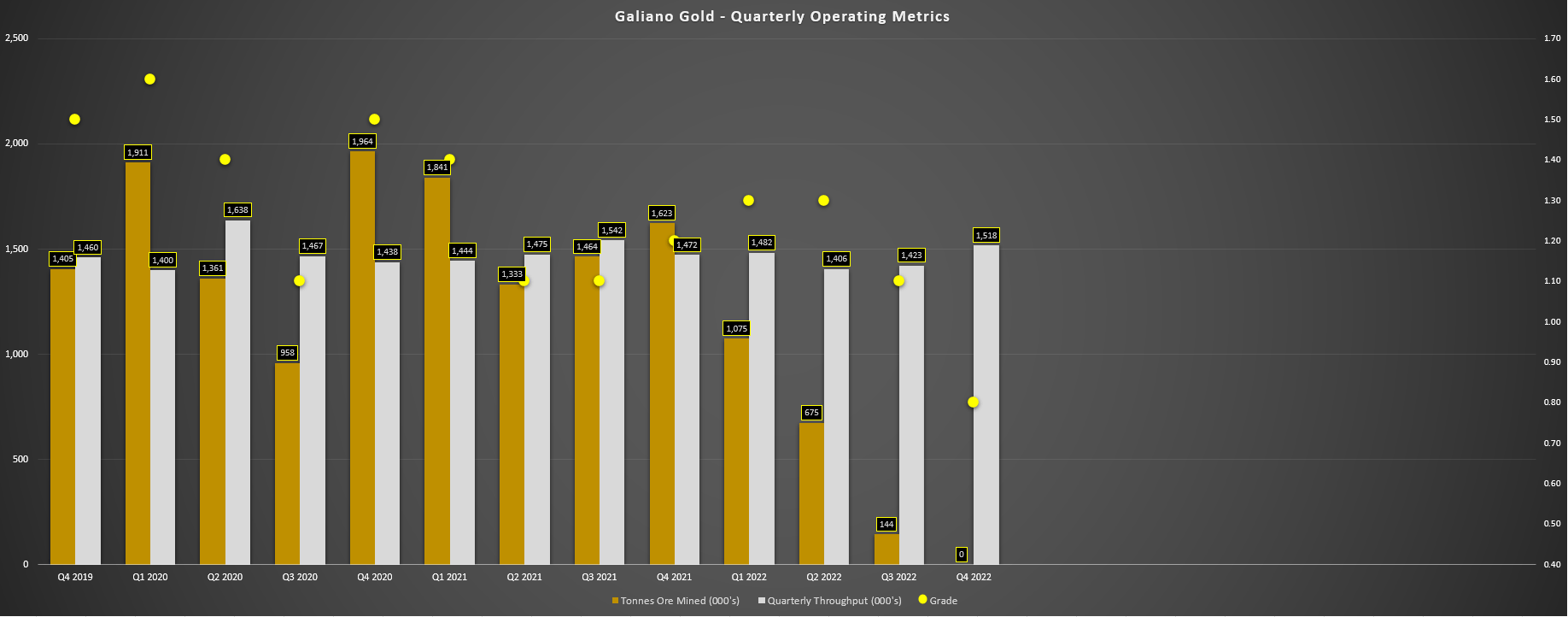

Galiano Gold - Quarterly Operating Metrics (Company Filings, Author's Chart)

{kind=link}

Looking ahead to FY2023, we still don't have a concrete forecast for expected production and costs, given that Galiano is in the process of releasing a new Technical Report later this quarter and reinstating reserves at the Asanko Gold Mine. However, regardless of where production and costs come in, the company has begun 2023 in a great position (despite a modest year of production with low gold prices in 2022), with the AGM joint venture with Gold Fields ( GFI ) holding ~$97 million in cash and Galiano holding $56 million in cash with no debt.

This represents one of the strongest balance sheets among small-cap and mid-cap producers and gives Galiano lots of flexibility to spend on near-mine, regional, and even greenfield exploration at its Asumura Project on the Sefwi Gold Belt. This project is 65 kilometers southwest (and along strike) of Newmont's ( NEM ) massive Ahafo Mine, which hosts ~6.1 million ounces at 0.90 grams per tonne of gold (Ahafo South) and ~3.57 million ounces at 2.40 grams per tonne of gold at its robust Ahafo North Project that's under construction. Galiano's Asumura Project is also northwest of the currently producing Chirano Mine, which Kinross ( KGC ) originally bought in its Red Back acquisition and sold last year. Hence, I certainly wouldn't rule out a meaningful discovery here.

Costs & Margins

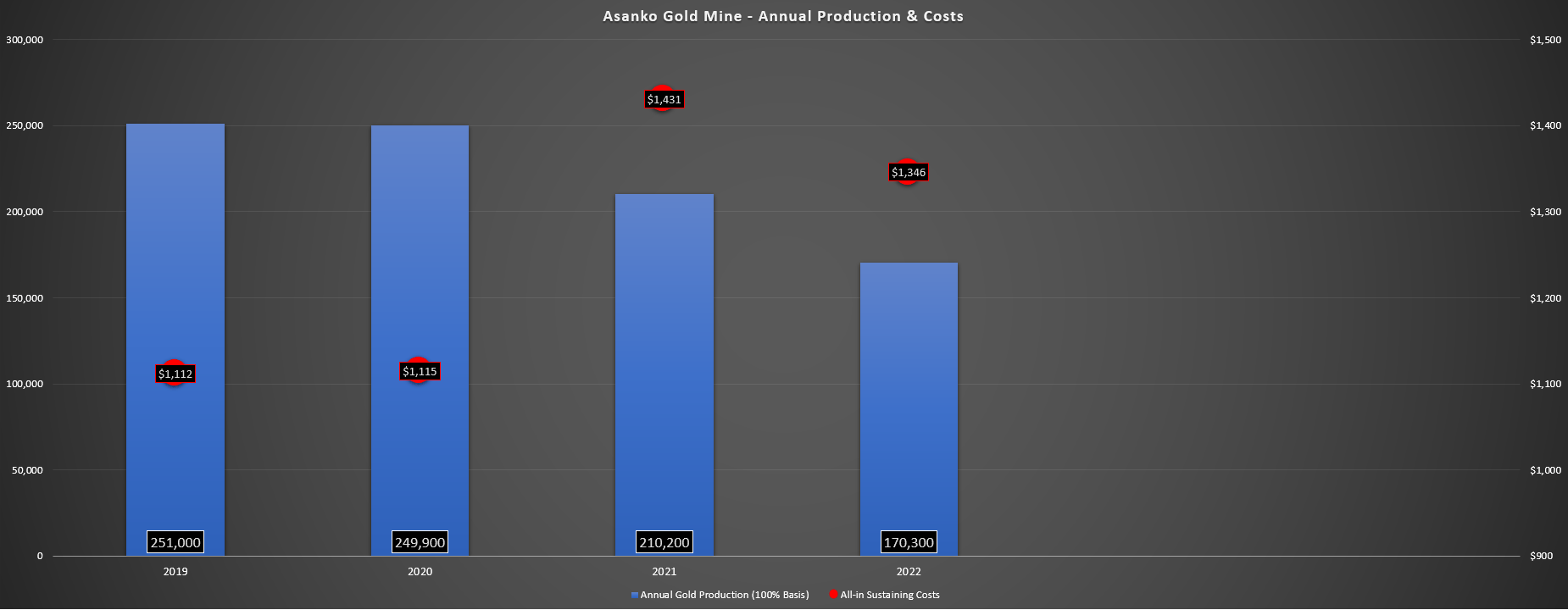

Moving over to costs and margins, it was a tough year for the gold sector, with inflationary pressures taking a sizeable bite out of producer's margins. This was especially true for those companies with high-volume and low-grade operations that don't benefit from lower-cost hydroelectricity. In Galiano Gold's case, the company did call out electricity, diesel, and higher consumables costs being a headwind this year. Still, cost performance was respectable, with all-in-sustaining costs [AISC] estimated to come in at $1,346/oz for the year, only 4% above the estimated industry average (~$1,290/oz).

Asanko Gold Mine - Annual Production & AISC (Company Filings, Author's Chart)

{kind=link}

Looking at the quarterly results, Galiano noted that it expected all-in-sustaining costs of $1,191/oz in Q4 and reported an average realized gold price of $1,686/oz, translating to AISC margins of $495/oz. This is a material improvement year-over-year (though it benefited from no mining costs in the quarter and simply processing). We should see another quarter of margin expansion in Q1 2023, with the gold price averaging $1,895/oz quarter-to-date. Although these margins are still well below FY2020 levels (~$600/oz), these margins aren't bad by any means, and costs are performing better than I had anticipated due to the rationalization of the AGM workforce, which resulted in $7.0 million in cost savings from Q1 to Q3 2022 alone.

The other piece worth noting is that while the Asanko Gold Mine is running at a cost profile of ~$1,350/oz based on processing average grades of ~1.1 grams per tonne in FY2022 after relying on stockpiles and mining at lower-grade deposits such as Esaase and Akwasiso, we should see a significant improvement in unit costs once mining heads to Nkran Cut 3, especially combined with the workforce restructuring that has led to a more streamlined operation. Mining at Nkran Cut 3 could begin in 2024, and grades here are much better than at other deposits and closer to the plant, with an average grade north of 2.0 grams per tonne of gold. Hence, I expect solid margins once mining begins here, which appears to be the next priority.

Long-Term Potential

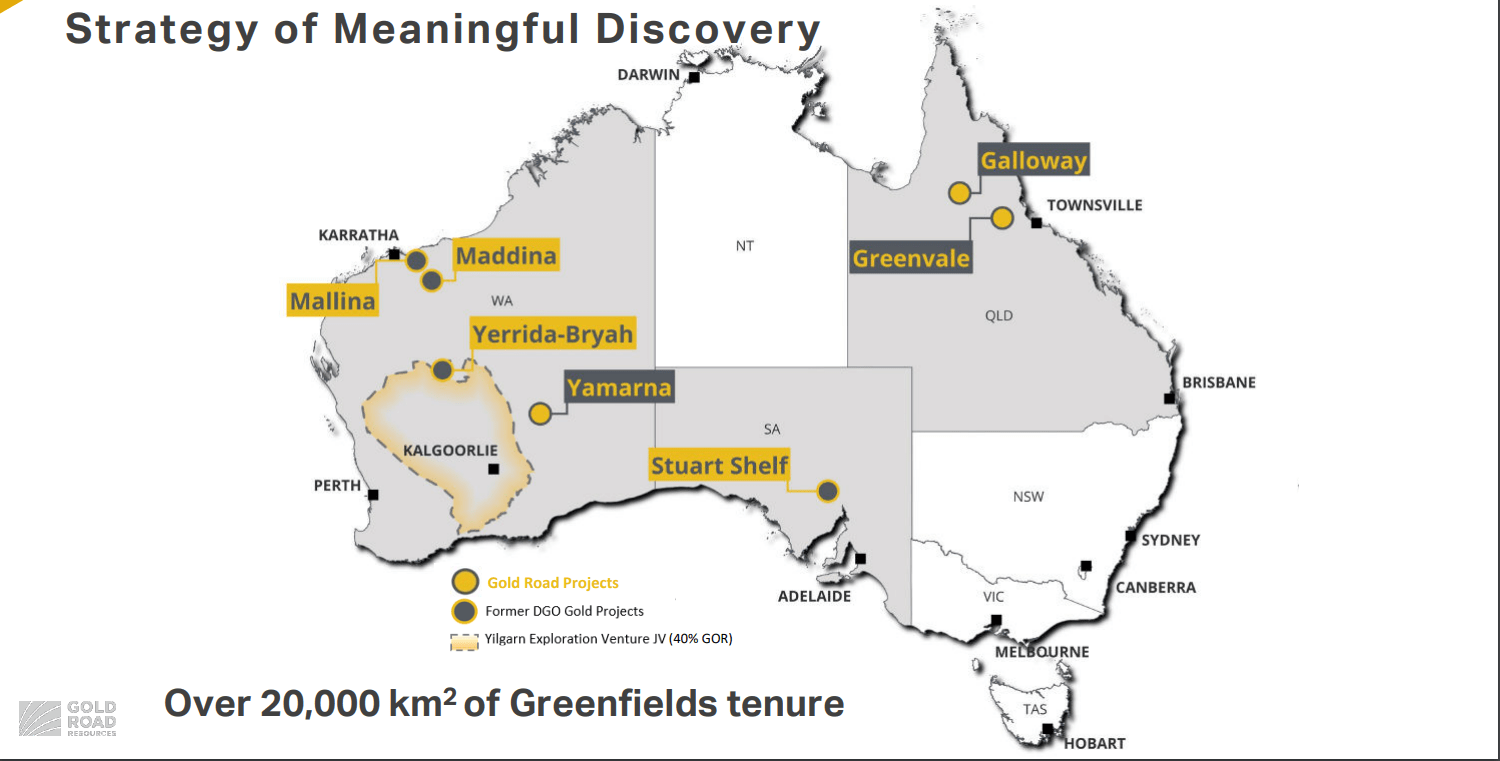

Looking at the big picture for Galiano Gold, one of the negatives is that it's a single-asset producer with attributable production of barely 100,000 ounces per annum at costs slightly above the industry average. However, with the company's strong balance sheet, I am surprised that the company hasn't explored opportunistic M&A to diversify itself or drilled more aggressively at 100% owned projects to look at setting itself up to add a second operation down the road and shed its single-asset producer status. This is what Gold Road Resources ( OTCPK:ELKMF ) has done, with it also sharing a mine with Gold Fields in Australia, but it is making strategic investments and drilling on 100% owned ground south of the Gruyere Mine.

Gold Road Resources - Gruyere Mine, 100% Owned Ground & Strategic Investments (Company Presentation)

{kind=link}

Gold Road's multiple is obviously helped by the fact that it's located in a Tier-1 jurisdiction with a larger attributable production profile vs. Galiano in Ghana, with a smaller attributable production profile. However, if Galiano were to delineate a 1.0+ million ounce resource at the Asumura Project and advance it, this could help with a re-rating of Galiano long-term. The reason is that it would add another component to the story vs. simply being the operator of a relatively small mine in Ghana. Another option would be to acquire an advanced project that already has resources. Normally, this wouldn't be an option for a junior producer, but with Galiano's strong balance sheet, either drilling aggressively at Asumura or acquiring prospective land/resources elsewhere is an option.

Until we see another dimension to this story, I would be surprised to see Galiano trade back above US$1.00 per share without much higher gold prices, even if the company looks to have a better year ahead post-2023 assuming it begins mining Nkran Cut 3. So, while it's certainly worth keeping an eye on the underground potential at Nkran and near-mine targets at the Asanko Gold Mine, I am more interested in the exploration results on its 100% owned ground at Asumura, where we may begin to see some results in 2023. Let's take a look at the valuation:

Valuation & Technical Picture

Based on ~235 million fully-diluted shares and a share price of US$0.57, Galiano trades at a market cap of ~$134 million and an enterprise value of US$78 million. This is a very reasonable valuation for a company with an attributable measured & indicated resource of ~1.45 million ounces of gold, especially when there looks to be an upside to this figure medium-term as the joint venture is well capitalized to drill new and existing targets on its large land package (20,000+ hectares). That said, unless capital is being returned to shareholders as dividends/buybacks, I believe it's best to use a market cap figure vs. an enterprise value figure for valuing companies.

Using what I believe to be a conservative multiple of 3.50x cash flow and FY2023 cash flow per share estimates of $0.19, this points to a fair value of US$0.91 (when adding in $0.24 in cash per share). However, I prefer not to place any value on cash unless it's being returned to shareholders, meaning the more conservative fair value for GAU is US$0.67 (18% upside). Some investors might argue that a cash flow multiple of 3.50 is too low. I would disagree. While Ghana is certainly a better jurisdiction than Guatemala and South Africa, I wouldn't consider it a low-risk jurisdiction. Besides, Galiano is a single-asset junior producer, placing it in arguably the highest-risk and most volatile class of gold producers.

Looking at the technical picture, my most recent update noted that Galiano Gold would become a Speculative Buy at US$0.43 or lower , and the stock touched this level on December 16th (low of US$0.42) and has rallied more than 30% off this low. However, this rally has left the stock back in the upper portion of its expected trading range where risk is elevated, with resistance at US$0.61 and no strong support until US$0.42. So, with the stock trading at US$0.58, which translates to a reward/risk ratio of ~0.25 to 1.0, I don't see any reason to pay up for the stock here, and I see far more attractive bets elsewhere in the sector currently.

{kind=link}

Summary

Galiano continues to be one of the most reasonably valued producers in the market, especially if we consider its cash position, which leaves the stock trading at an enterprise value of just ~$78 million. This leaves the stock trading at a deep discount to net asset value and just ~$52/oz on attributable M&I resources, an attractive valuation even for a junior producer in a Tier-3 jurisdiction like Ghana. That said, I prefer to buy when stocks are well off their recent highs, and I require a much larger margin of safety when it comes to single-asset producers to adjust for their elevated risk. So, while there's no disputing GAU stock is cheap, it would need to dip below US$0.43 to head into a low-risk buy zone.

For further details see:

Galiano Gold: Turnaround Thesis Remains Intact