TMO - GE And GE HealthCare Technologies: Separation Paves Way For Tremendous Value Creation

Summary

- General Electric successfully spun off GE HealthCare Technologies, resulting in one publicly-traded company turning into two.

- Though the transformation for General Electric is not complete, this does set up investors for tremendous upside potential.

- GE HealthCare Industries looks significantly undervalued and will likely fare well long-term.

Jan. 4 marked a major day for investors in industrial conglomerate General Electric ( GE ). As the company signaled last year, Jan. 4 proved to be the first day that GE HealthCare Technologies ( GEHC ), the former healthcare segment under General Electric, would be operating as a standalone, publicly-traded enterprise. As I anticipated, shares of both firms rose in response to this development. Having said that, the movement higher was not what I anticipated, nor was the movement distributed in a way that I would have thought. What's clear right now is that both companies still offer some nice upside potential. In particular, GE HealthCare Technologies looks to be drastically undervalued following the spinoff. In response to these developments, I have decided to keep my "strong buy" rating on General Electric while establishing a "strong buy" rating on GE HealthCare Technologies as well.

A big day for investors

The market opened on Jan. 4 with shares of General Electric trading substantially lower than what they closed at the day before. But this was not because of some decline in share price caused by fundamental concerns. Rather, it was an adjustment made for the fact that, for every three shares of General Electric stock somebody owned, they would be given one share of GE HealthCare Technologies as part of that entity's spinoff. Immediately in response to this move, shares of both companies rose higher for the day. In aggregate, as of the time of this writing at least, the increase worked out to roughly 4%, taking the pre-split value of General Electric from $84.98 per share to $88.42.

It's worth remembering that while most of the healthcare business has been distributed to shareholders, the 19.9% that was not ended up being held by General Electric itself. At current prices, this translates to equity value of roughly $5.33 billion. This means that General Electric on its own, which includes all of its other subsidiaries, comes out to roughly $69.81 billion compared to its current market capitalization of $75.14 billion. Next year, the company is going to be spinning off its Power segment and other related assets, leaving the aerospace operations with the main firm.

I have written extensively about how undervalued General Electric as a whole would be. I also have performed, in the past, sum-of-the-part analyses to show what it would look like if it were broken up into distinct entities. But until now, there has been some uncertainty about how GE HealthCare Technologies would ultimately be perceived as a standalone enterprise. The current market capitalization of that business, which includes the 19.9% stake that General Electric stove owns, comes out to $26.81 billion. With net debt of $8.44 billion, we end up with an enterprise value of $35.25 billion.

In one prior article , I discussed a range of pricing scenarios for GE HealthCare Technologies on its own. And frankly, what I thought would happen was that its shares would rise nicely on the day that the spinoff was completed, while shares of General Electric itself would fall materially since that is where a lot of the baggage exists in the eyes of shareholders. But this is not what came to pass. The end result, in my opinion, is that shares of GE HealthCare Technologies are now drastically underpriced to the point that they warrant a "strong buy" rating.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| GE HealthCare Technologies |

| 14.3 |

| 10.7 |

| 9.3 |

| Danaher ( DHR ) |

| 29.5 |

| 23.7 |

| 19.4 |

| Thermo Fisher Scientific ( TMO ) |

| 31.8 |

| 27.5 |

| 20.7 |

| Agilent Technologies ( A ) |

| 36.6 |

| 34.9 |

| 23.4 |

| Illumina ( ILMN ) |

| 40.5 |

| 61.1 |

| 79.8 |

| Mettler-Toledo International ( MTD ) |

| 40.7 |

| 42.8 |

| 28.8 |

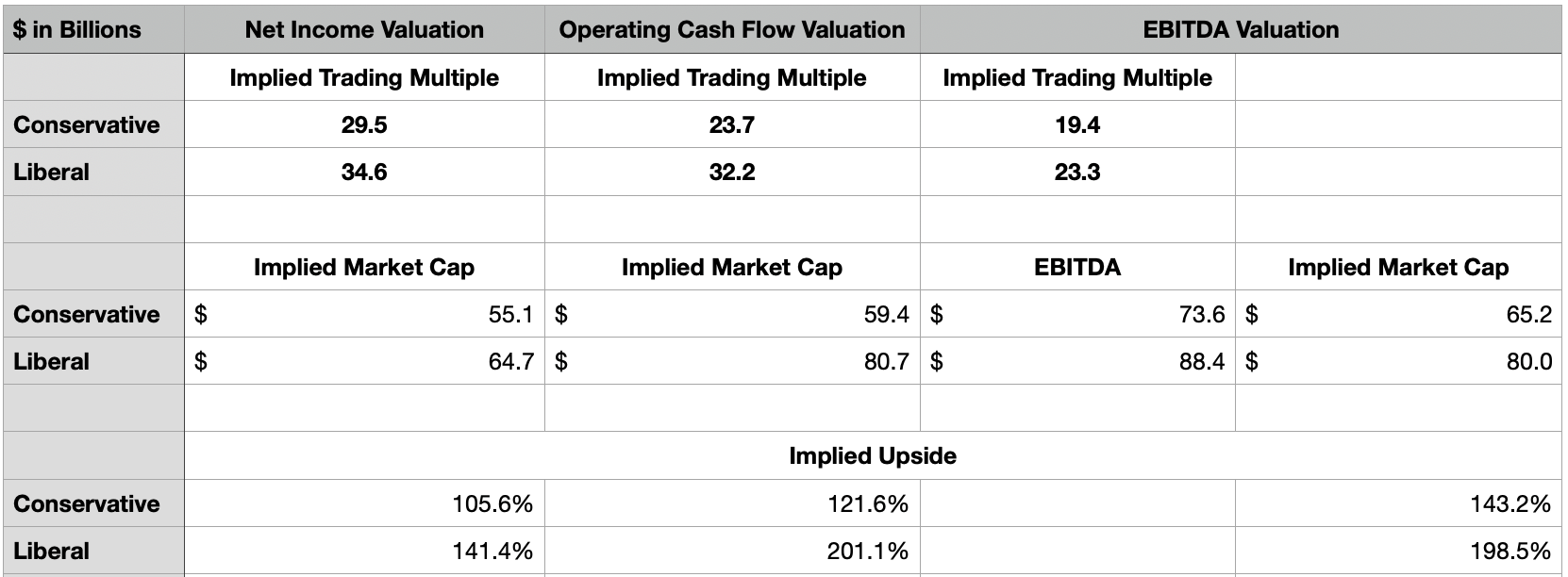

To understand why this is, I previously used the most recent data available by the company to calculate that net income for GE HealthCare Technologies on its own should be $1.87 billion. Adjusted operating cash flow should be $2.51 billion, while EBITDA should come out to nearly $3.80 billion. Based on the data we have at our disposal today, this implies that the company is currently trading at a price-to-earnings multiple of 14.3, a price to adjusted operating cash flow multiple of 10.7, and an EV to EBITDA multiple of 9.3. To most investors, this pricing should be indicative of a company that's at least marginally undervalued. But it's also important to keep in mind that this particular space tends to see the companies in it trade at high multiples.

In the first table in this article, you can see the trading multiples associated with five similar firms. For the price-to-earnings approach, these companies range from a low of 29.5 to a high of 40.7. Using the price to operating cash flow approach, the range is between 23.7 and 61.1. And when it comes to the EV to EBITDA approach, the range would be from 19.4 to 79.8. In order to appropriately value GE HealthCare Technologies, I looked at two different scenarios. The more conservative scenario assumes that it should trade at the multiples of the cheapest firm on the list. The more liberal scenario strips out the most expensive firm and averages out the multiples of the other four. It then assumes that GE HealthCare Technologies should trade at that level instead.

Utilizing this scenario, I calculated that GE HealthCare Technologies should be trading Somewhere between $55.1 billion and $65.2 billion using the conservative approach. Using the liberal approach, the range should be between $64.2 billion and $80.7 billion. What this implies is that the company should have upside potential, even in the worst case, of 105.6% compared to the $58.95 that shares are currently going for. On the high end, we're looking at upside of 201.1%. Naturally, the market is behaving cautiously because of the track record of General Electric as a whole. But assuming that GE HealthCare Technologies performs well from a fundamental perspective over the next couple of quarters, I think a nice increase in price will be warranted. What we can say is that the firm does currently have a good catalyst for growth moving forward. Based on data from the 2021 fiscal year, the combined global market opportunity for the industries that the firm operates in came out to $84 billion. That market, according to management, is expected to grow by between 4% and 6% per year. That would take the size of the industry up to between $98.3 billion and $106 billion by 2025. Even achieving growth close to that rate without experiencing any meaningful margin contraction would go a long way to proving the bullish case to shareholders.

{kind=link}

Takeaway

Right now, I understand why some investors may be worried about GE HealthCare Technologies and its former parent General Electric. For years, a combination of factors, ranging from company-specific problems to problems related to major customers, to economic issues, all played a role in bringing harm to General Electric. In my opinion, though, investors should view this as a new era for the firm, with distinct management teams able to focus on distinct enterprises in order to create as much value for the shareholders of each firm as possible. It will take a bit of time, but in the case of GE HealthCare Technologies, I believe that tremendous upside is on the table from here. And because of that, I happily rate the company a "strong buy" while retaining the "strong buy" rating I previously assigned General Electric itself.

For further details see:

GE And GE HealthCare Technologies: Separation Paves Way For Tremendous Value Creation