TMO - GE HealthCare: Recent Dip Provides A Good Entry Point

2023-04-27 18:03:18 ET

Summary

- Revenue should benefit from price increases and good end-market demand.

- Margins should benefit from volume leverage, moderating inflation, and price increases.

- Valuation is at a discount compared to the peers and the recent stock correction represents a buying opportunity.

Investment Thesis

GE HealthCare Technologies Inc (GEHC) is expected to benefit from price increases and volume growth due to good end-market demand for procedures, which should drive revenue growth. Additionally, on the margin front, GEHC is expected to expand its margins through price increases, volume leverage, and benefit from moderating inflation.

Although the stock price corrected post the recent Q1FY23 earnings release due to lower-than-expected Imaging segment margins, I believe it's more of a temporary issue, and the company's future growth and margin improvement prospects remain intact. Hence I believe the recent dip represents an attractive entry point for investors.

Q1FY23 Earnings

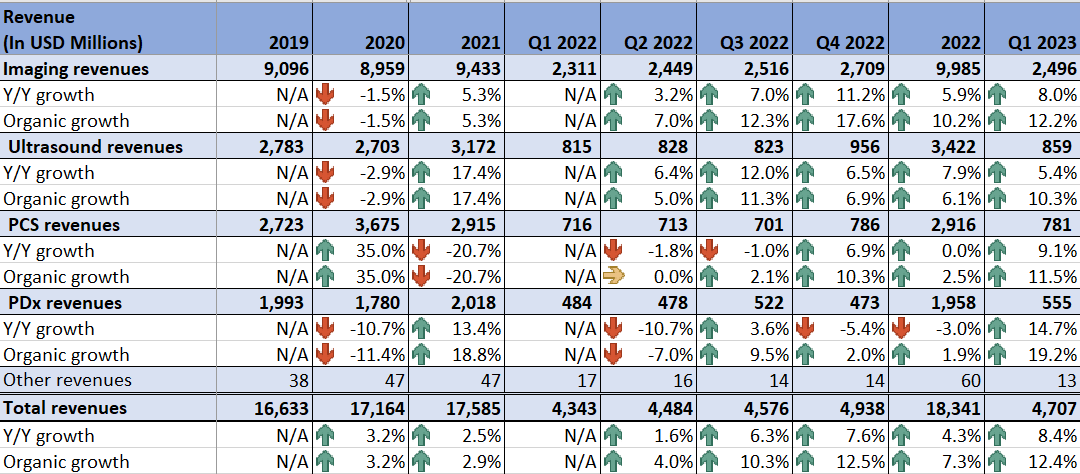

GE HealthCare recently reported better-than-expected results for the first quarter of 2023. The company's revenue increased by 12.4% organically or by 8.4% Y/Y on a reported basis to $4.7 billion, which exceeded the consensus estimate of $4.63 billion. Adjusted EPS grew by 34.92% Y/Y to $0.85 on a stand-alone basis and was higher than the consensus EPS estimate of $0.79. Stand-alone adjusted EBIT margin increased by 150 bps Y/Y to 14.1%. The revenue growth was driven by volume and price increases, good demand, and a healthy backlog. Adjusted EPS and adjusted EBIT margin increased due to volume leverage, productivity, cost-saving initiatives, and price increases.

Revenue Analysis and Outlook

In my previous article on GE HealthCare, I discussed the growth drivers that could help the company increase revenue in the coming years. Since then, the stock price had a good run-up until the earnings release, but it corrected post-earnings due to lower margins in the Imaging segment, which is GEHC's largest segment.

However, despite the recent correction, I remain bullish on the stock. In Q1FY23, revenue increased by 8.4% Y/Y to $4.7 billion, benefiting from good volume growth, as product revenue increased by 12.3% due to healthy demand across all segments. Additionally, price increases and a healthy backlog also contributed to revenue growth. Excluding a 4 percentage point FX headwind, organic revenue increased by 12.4%.

GE HealthCare's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I believe the company can continue to deliver revenue growth as it benefits from price increases and good demand across all the segments globally.

GEHC, like many industries, has been taking price increases to cover inflationary costs. These price increases have helped the company in supporting revenue growth. The company plans to take additional price increases in the coming quarters and targets a 2-3% Y/Y price increase for the current year. I expect these incremental price increases and the carryover impact of prices increases from last year to help the company's revenue growth.

In addition, I believe that the end market demand should continue to remain healthy as there is still pent-up demand from the pandemic for procedures around the globe. Following COVID, there is a high number of delayed procedures that require more follow-up in all the markets around the world, and most of those follow-up involves imaging. This should continue to drive demand for GEHC's imaging and ultrasound products.

Moreover, I mentioned in my previous article about China reopening and the pent-up demand for procedures, which were delayed for the last three years, along with government medical stimulus funds being a good tailwind for GEHC's sales growth in the near term. China's sales grew 18%Y/Y in the first quarter due to good volume growth as anticipated. The economic reopening has just begun, and I believe as China's market further normalizes, we should continue to see significant volume growth moving forward as well. This should be a good tailwind for the company's sales growth in the near term.

Margin Analysis and Outlook

In the first quarter of 2023, GEHC benefited from volume leverage and price increases, which contributed to Y/Y margin expansion. The company's productivity initiatives also helped in margin expansion for the quarter, offsetting inflationary raw material costs, planned investments, and unfavorable product and service mix. These headwinds were more pronounced in the Imaging and Pharmaceutical Diagnostics segment. Fortunately, these headwinds were offset by more pronounced pricing and volume tailwinds in the Ultrasound and Patient Care System segments, resulting in an adjusted EBIT margin growth of 30 bps Y/Y to 14.1% for the company. The stand-alone adjusted EBIT margin on a like-by-like basis (which includes standalone company costs that were not factored in the previous year) increased by 150 bps Y/Y to 14.1% from 12.6% standalone adjusted EBIT margin in the prior quarter.

However, one thing which disappointed investors was the segment EBIT margin of Imaging, which is GEHC's biggest segment. Imaging's EBIT margin was 7.7% versus 8.9% for the prior year, as planned investments and mix outweighed the volume leverage. The company's medium-term goal is to improve the segment margin to the high teens and the margin improvement in this segment is key to the company's medium to long-term margin improvement thesis. So, investors weren't happy to see margins declining in this segment and, as a result, the shares sold off.

I believe this correction is not justified. The margin decline was a result of management shipping more hardware/equipment in the quarter which increased equipment's share in the revenue mix compared to services. Since services carry higher margins, there was a negative impact from this mix shift. However, this is not necessarily bad from a medium to long-term perspective. These equipments will eventually require associated services from GEHC and the company's margins should benefit in the medium to long term. Here is what the company's CFO Helmut Zodl said on the earnings call,

So I'll start with Imaging margins. So obviously, we are very focused on expanding the EBIT margins in the high teens in the medium term for Imaging. And if you look at in the first quarter, our margins were at 7.0% or 8% for imaging both were slightly lower than what we saw in the fourth quarter, but there was a clear reason because we were shipping a higher and a component of hardware versus services in the quarter. But as we expect the services pull-through, we expect those margins to improve. "

Looking ahead, I anticipate continued margin growth for the company. As mentioned earlier in the revenue outlook, GEHC plans to continue implementing incremental price increases, which, along with the carryover impact of last year's price increases, should support margin expansion. The margin growth should be further supported by volume leverage given the good demand outlook. Additionally, inflationary pressures are moderating, and the company is experiencing a reduction in input costs which have decreased ~20% compared to the inflationary peak in mid-2022. As the company sells out high-cost inventory purchased during peak inflation last year in 1H2023, the second half of the year should see margin benefits from moderating inflation and lower-cost inventory.

Valuation and Conclusion

At present, GEHC is trading at a 21.35x FY23 consensus EPS estimate of $3.75 and an 18.78x FY24 consensus EPS estimate of $4.27. The current valuation of GEHC stock is lower than most of its peers despite similar growth prospects.

| Peers |

| FY23 P/E |

| FY24 P/E |

| FY25 P/E |

| FY23 EPS growth |

| FY24 EPS growth |

| FY25 EPS growth |

| Danaher Corporation (DHR) |

| 24.41 |

| 21.67 |

| 19.92 |

| -13.03% |

| 12.66% |

| 8.75% |

| Thermo Fisher Scientific Inc. (TMO) |

| 22.46 |

| 19.98 |

| 17.50 |

| 2.12% |

| 12.42% |

| 14.21% |

| Mettler-Toledo International Inc. (MTD) |

| 33.29 |

| 29.76 |

| 26.83 |

| 10.75% |

| 11.84% |

| 10.93% |

| Boston Scientific Corporation (BSX) |

| 26.77 |

| 23.66 |

| 21.34 |

| 11.61% |

| 13.14% |

| 10.91% |

| GE HealthCare Technologies Inc. |

| 21.35 |

| 18.78 |

| 16.19 |

| 10.95%* |

| 13.66% |

| 15.99% |

Source: Consensus Estimates (* GE FY23 EPS growth is versus FY22 standalone EPS of $3.38 provided by management)

Based on the company's strong fundamentals and the positive revenue and margin growth prospects for the upcoming years, I believe that the stock offers a good buying opportunity post recent correction.

For further details see:

GE HealthCare: Recent Dip Provides A Good Entry Point