TMO - GE HealthCare Technologies: Still Significantly Undervalued

Summary

- The management team at GE HealthCare Technologies Inc. announced financial results covering the final quarter of the company's 2022 fiscal year.

- This release cleared up a lot of uncertainty regarding the company and established management's thoughts for the 2023 fiscal year.

- This news also reaffirmed, to me, that GEHC stock is drastically undervalued.

Following its spin-off from General Electric Company ( GE ), GE HealthCare Technologies Inc. ( GEHC ) has experienced a great deal of upside. Even though uncertainty existed about how the company would ultimately look and about what investors could anticipate moving forward, investor sentiment has been all-around positive for the firm. As a result, those who kept their shares and/or, like me, who purchased more after the spinoff, were rewarded handsomely. Moving forward, it does now look as though the uncertainty regarding the company is clearing up. After reporting financial results covering the final quarter of the company's 2022 fiscal year and offering guidance for 2023, shares of the business are looking cheap. They are, in fact, cheap enough to still warrant a "strong buy" rating in my book.

GE Healthcare is still a great prospect

On January 4th of this year, one day after GE HealthCare Technologies split off from General Electric, I wrote a very bullish article regarding the firm. In addition to reiterating my "strong buy" rating for General Electric, I assigned a "strong buy" rating for the new spun-off entity. This was based largely on a comparative analysis of the enterprise when stacked up against similar firms. It was also based on the fact that overall financial results for the company, while mixed, were still looking robust. So far, my rating on the company has turned out well. While the S&P 500 (SP500) is up 4.6% since the publication of that article, shares of GE HealthCare Technologies have seen upside of 15.6%.

Some of that increase came on January 30th, when the management team at the business announced financial results covering the final quarter of the company's 2022 fiscal year. When former parent General Electric announced its own results for the final quarter of 2022 earlier in the week, the company did touch on some of the data associated with GE HealthCare Technologies, only because that quarter was the final full quarter for which GE HealthCare Technologies was a wholly owned subsidiary of the industrial conglomerate. today, General Electric only owns 19.9% of the healthcare business.

{kind=link}

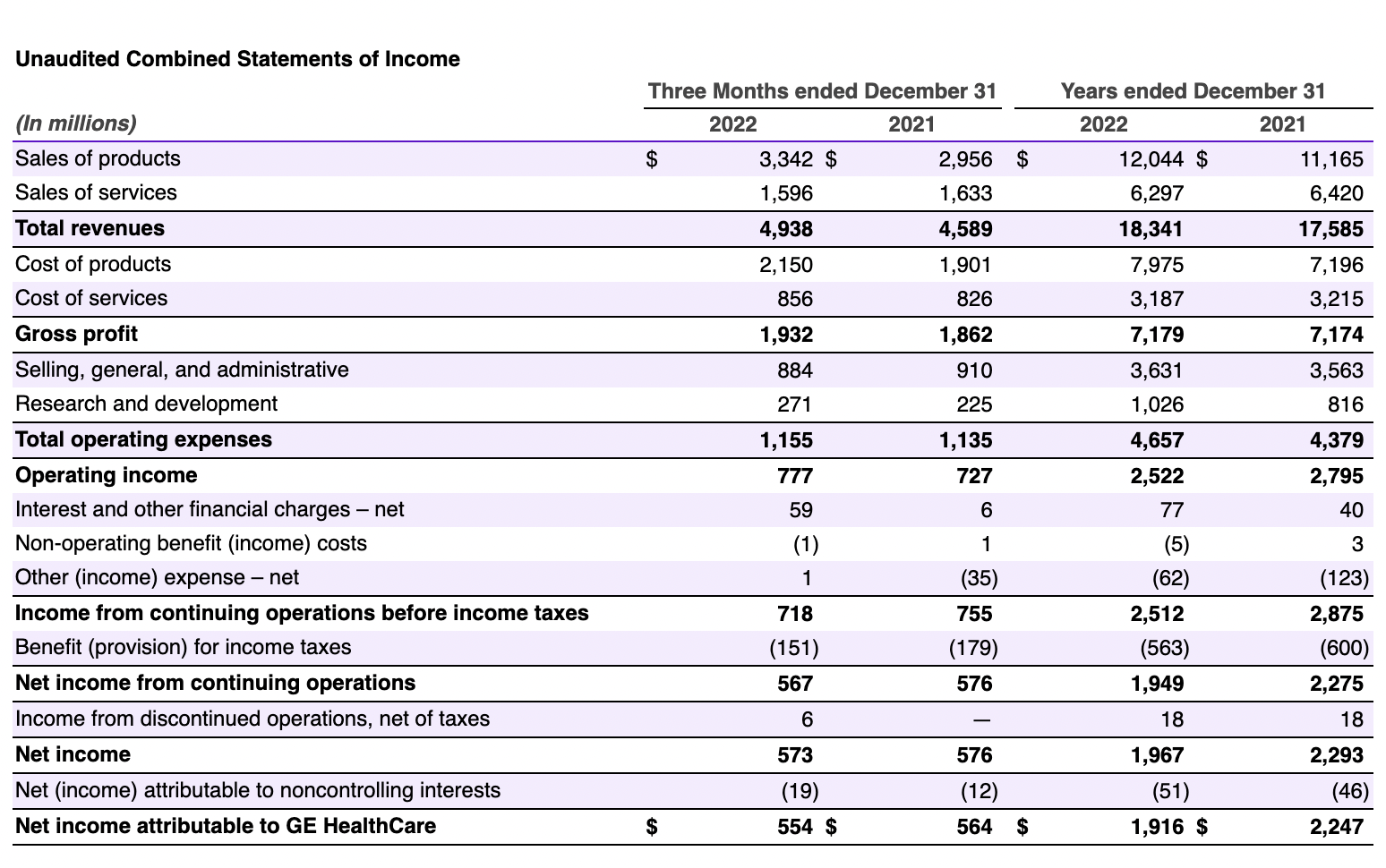

For the most part, financial results achieved by GE HealthCare Technologies looked positive. Revenue in the final quarter came in at $4.94 billion. That represents a year-over-year increase of 7.6% compared to the $4.59 billion the company reported in the final quarter of 2021. Actual organic revenue for the company was up an impressive 13%. Acquisitions also added 1% to the company's top line.

The pain, then, came from foreign currency fluctuations that hit sales to the tune of 6%. The greatest growth for the company came from its Imaging segment, with overall revenue up around 11% but organic revenue up 18%. The molecular imaging and computed tomography, magnetic resonance, and surgery categories all experienced robust upside thanks to strong demand. Patient Care Solutions also grew nicely, shearing up 7%, with organic growth of 10%. Management attributed the increase to improvements in supply chain resiliency and to pricing actions the company enacted. Ultrasound revenue jumped 6%, or 7% organically, thanks largely to strong demand across a variety of the company's product categories. The real laggard for the company was the Pharmaceutical Diagnostics segment, with revenue dropping 5%, or increasing only 2% on an organic basis, because of fewer procedures in China and the normalization of customer inventory in the U.S.

From a profitability perspective, things for the company were a bit mixed. Net income came in at $554 million. That's actually down from the $564 million reported one year earlier. A rise in interest expense, from $6 million to $59 million, really associated with the increased debt load of the company, negatively impacted results. The firm saw a 13.1% rise in the cost of products, with a combination of inflation, a change in product mix, and other factors all impacting the company. Research and development costs also rose, climbing by 20.4%.

For 2022 as a whole, revenue for the company came in at $18.34 billion. That stacks up nicely against the $17.59 billion reported one year earlier. Just as was the case in the final quarter, profitability for the company declined, dropping from $2.25 billion for 2021 down to $1.92 billion for 2022. We should also naturally pay attention to other profitability metrics. Operating cash flow for the company actually increased, rising from $1.61 billion to $2.13 billion. But if we adjust for changes in working capital, it would have fallen from $2.89 billion to $2.23 billion, while EBITDA shrank from $3.80 billion to $3.49 billion.

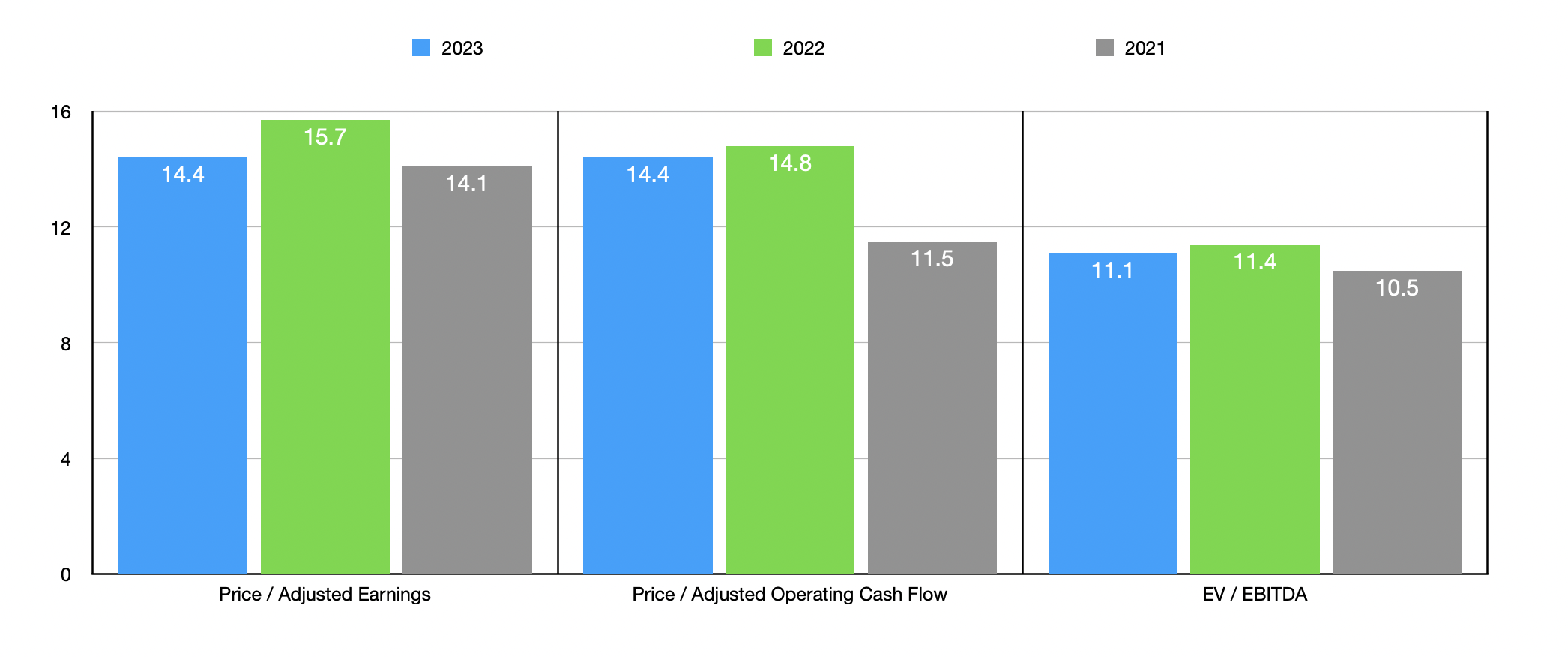

When it comes to 2023, GE HealthCare Technologies Inc. management has a rather rosy outlook for the company. Overall organic revenue should climb by between 5% and 7%. The company is also forecasting adjusted earnings per share of between $3.60 and $3.75. That compares to the $3.38 per share reported for 2022. This would translate to adjusted net income, at the midpoint, of roughly $2.29 billion. The company also said its EBIT margin should range between 15% and 15.5%. Taking the midpoint there, we can anticipate a reading of nearly $3.60 billion. If we assume that other profitability metrics will change at the same rate, then we would get adjusted operating cash flow for 2023 of just under $2.30 billion.

{kind=link}

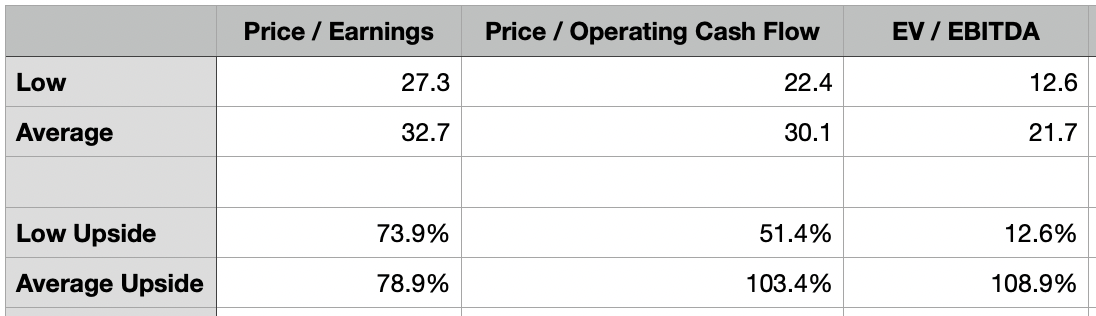

Based on these numbers, the company would be trading at a forward price to adjusted earnings multiple of 14.4. That matches the forward price to adjusted operating cash flow multiple, while the forward EV to EBITDA multiple would come in at 11.1. As you can see in the chart above, the company does look cheaper than if we were to use data from 2022. But it is more expensive than if we were to use the data from 2021. As part of my analysis, I did compare the company to six similar firms. On a price-to-earnings basis, these companies ranged from a low of 27.3 to a high of 41.3. Using the price to operating cash flow approach, the range would be from 22.4 to 62.8. And when it comes to the EV to EBITDA approach, the range would be from 12.6 to 79.8. In each case, GE HealthCare Technologies was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| GE HealthCare Technologies |

| 15.7 |

| 14.8 |

| 11.4 |

| Danaher Corporation ( DHR ) |

| 27.3 |

| 22.8 |

| 19.5 |

| Thermo Fisher Scientific ( TMO ) |

| 31.7 |

| 27.4 |

| 21.4 |

| Agilent ( A ) |

| 36.3 |

| 34.6 |

| 25.1 |

| Illumina ( ILMN ) |

| 40.5 |

| 62.8 |

| 79.8 |

| Mettler-Toledo International ( MTD ) |

| 41.3 |

| 43.3 |

| 30.1 |

| Siemens Healthineers ( SMMNY ) |

| 27.6 |

| 22.4 |

| 12.6 |

To value the company, I decided to look at two different scenarios. In the first scenario, I assumed that fair value for GE HealthCare Technologies would match the trading multiples of the cheapest of the six companies I compared it to. Doing this for the price-to-earnings approach would imply upside for investors of 73.9%. Using the price to operating cash flow approach, upside would be 51.4%. And when it comes to the EV to EBITDA approach, it would be a more modest 12.6%. Though in this case, if we were to look at the second-cheapest company instead of the cheapest, implied upside would be more in line with the other two approaches, with a reading of 85.6%. In the second scenario, I took out the most expensive company from the six and averaged out the other five. I then assumed that GE HealthCare Technologies Inc. would trade at that multiple. Using this scenario, implied upside would be anywhere from 78.9% to 108.9%.

{kind=link}

Takeaway

Based on all the data at my disposal, GE HealthCare Technologies Inc. continues to look incredibly cheap. The company is clearly healthy, even if it does have some debt on its books. So long as management can deliver on guidance, I see no reason why shares shouldn't move higher from here. Because of this, I have decided to keep the "strong buy" rating I signed GE HealthCare Technologies Inc. previously with the idea that GEHC stock will likely significantly outperform the broader market moving forward.

For further details see:

GE HealthCare Technologies: Still Significantly Undervalued