CA - Gear Energy: Watch Out For The 12% Dividend Yield Sustainability

2023-05-11 17:44:37 ET

Summary

- Gear Energy is amongst the oil and gas companies with the highest dividend yields.

- Q1’23 results indicate that Gear has been hit by cost inflation, and management updated guidance downwards.

- WCS spread narrowing is a positive, partially offsetting the WTI price decline into Q2’23.

- In the current price environment, the dividend sustainability may be questionable and done at the expense of additional debt.

Back in January, I wrote an article about Gear Energy ([[GXE:CA]], [[GENGF]]), highlighting it as a good bet on shrinking price differential between Western Canada Select (WCS) to the WTI oil benchmark. As the company released its Q1'23 results recently, it's worth taking another look at the situation. It appears that Gear was not spared by cost inflation, hurting its margins. In addition, management reduced its 2023 guidance, reflecting the recent market developments. Oil prices have weakened into Q2'23, providing additional challenges. On the positive side, the WCS spread is indeed narrowing since the beginning of the year, which partially offsets the headwinds. I estimate that in the current price environment, dividends may not be fully funded through cash flows from operations, after reflecting the CAPEX budget. While the relatively low debt profile of Gear could allow for the remainder part of dividends to be funded through borrowings, the rising interest rates environment put a question on the viability of such strategy. Overall, I think that management will maintain the dividend into H2'23 and then take a decision, based on the market environment.

Operational overview

Q1'23 highlights (Gear Energy)

{kind=link}

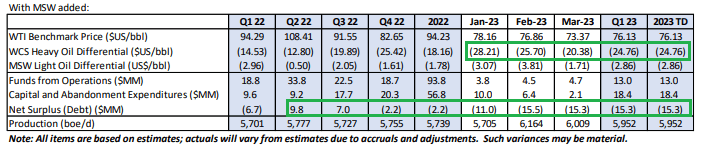

The overall market environment in which Gear Energy operated in Q1'23 was challenging as oil prices were trending downwards. In addition to that, the historically high WCS spread to WTI, which averaged at US$24.76/barrel dealt an additional blow to revenue. Average realized price for the product mix was CAD$62.86/boe (-29.2% YoY). At the same time, production advanced 4.4% YoY to 5,952boe/day, which was not enough to compensate for the hit on revenue from oil and gas sales, which amounted to CAD$33.7M (-26.0% YoY). It has to be noted that Gear Energy recorded a gain of CAD877k from hedging, compared to a loss of nearly CAD$9.5M a year ago.

{kind=link}

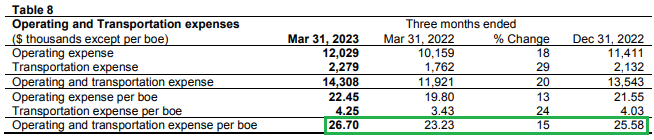

On the costs side, the company was hit by inflationary pressures as operating expenses surged 13.4% YoY to CAD$22.45/boe, which was also 4.2% higher compared to the figure from Q4'22. Transportation costs surged 23.9% YoY to CAD$4.25/boe, which resulted in total OPEX (including transportation) of CAD$26.70/boe (+14.9% YoY), significantly exceeding the 2023 initial guidance of CAD$23/boe. In total CAD$ amount, operating and transportation expenses came at CAD$ 14.3M (+20.0% YoY). Depletion, depreciation, and amortization charge was also higher at CAD$10.6M (+9.3% YoY). Net income for the quarter fell to CAD$2.0M (-68.0% YoY), or EPS of CAD$0.01.

At the same time, Gear Energy recorded CAD18.0M cash outflow, related to CAPEX and paid CAD$7.8M of dividends. This resulted in an increase of the net debt to CAD$15.3M from CAD$2.2M in the beginning of the year.

WCS-WTI spread is narrowing

WCS-WTI spread (BNN Bloomberg)

{kind=link}

Despite the overall negative market environment in which Gear Energy operated in Q1'23, there's one very positive development - the narrowing of the WCS-WTI spread. After reaching multi-year highs in 2022, the price differential began to shrink in 2023. The latest figures indicate that it stands around US$14.5/barrel, so it's about 50% off its highs in 2022. This positive development partially offsets the overall decline in oil prices, reducing the pressure on Gear's revenue. I see two primary reasons behind the WCS-WTI spread shrinkage - the halt of the US SPR releases and normalization of the previously low levels of the Mississippi river, allowing for more barging.

Updated guidance

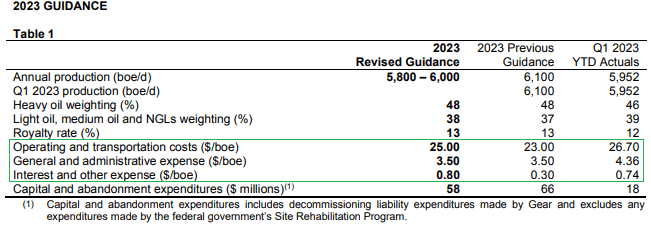

In light of the recent events, management updated its 2023 guidance. The new figures indicate reduced expectations as midpoint production projections were lowered to 5.9kboe way, compared to 6.1kboe/day in the previous guidance, while OPEX (including transportation) forecast is raised to CAD$25.0/barrel from CAD23.0/barrel. The rise in indebtedness as well as higher interest rates environment has prompted 166.6% increase in interest expense guidance to CAD$0.8/barrel. CAPEX projections were decreased from CAD$66M initially to CAD$58M of which CAD$18M was already spent in Q1'23.

Updated 2023 guidance (Gear Energy)

{kind=link}

Within the management's message to shareholders in the Q1'23 release , I noted the following:

The goals for 2023 remain the same: to strike a balance between strong returns on capital, production and reserves stability, continued dividends, and balance sheet strength.

I think that such wording indicates management's intention to continue with its CAD$0.01 monthly dividend, but not at all cost, as balance sheet strength is also mentioned. So a question arises of how sustainable is the dividend in the current environment.

Dividend sustainability

Stepping on management's guidance and adding assumptions of WCS spread of US$14.5/barrel and WTI price of US$73/barrel as well as average realized price of CAD$5.00/boe below the WCS price, holding working capital unchanged and ignoring the minor effects of hedging, I got the following:

| Quarterly results scenario |

| unit |

| production |

| boe/day |

| 5900 |

| WTI price |

| US$ |

| 73 |

| WCS-WTI spread |

| US$ |

| 14.5 |

| realized price/boe |

| CAD$ |

| 73.0 |

| Revenue |

| CAD |

| 39.2 |

| royalties |

| CAD |

| 5.1 |

| opex |

| CAD |

| 13.4 |

| G&A |

| CAD |

| 1.9 |

| interest |

| CAD |

| 0.4 |

| Depletion |

| CAD |

| 10 |

| net income |

| CAD |

| 8.4 |

| FCF |

| CAD |

| 18.4 |

| CAPEX |

| CAD |

| 13.3 |

| dividend |

| CAD |

| 7.8 |

| surplus/shortfall |

| CAD |

| -2.8 |

* Author's own assumptions

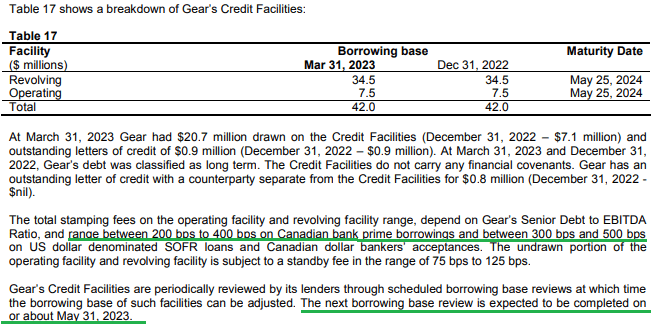

So it seems that in the current environment, Gear will have to use some debt to fully fund its dividend. While the amount is not high, such a strategy is not sustainable in the long term. Especially given that interest rates are rising, and the company's cost of borrowing should be close to 10%, given the surge in Canada's prime rate.

Credit facilities and costs (Gear Energy)

{kind=link}

Despite this, the estimated shortfall is small enough, that management could live with it in the short-term and I expect the dividend to be maintained into H2'23. After that, depending on the market environment an adjustment of policy may be made.

Notes on valuation and risks

At current market prices, the annualized dividend yield of Gear Energy is around 12%, which is amongst the highest in the oil and gas sector. The monthly distributions make it especially attractive for income oriented investors, who like frequent cash flows. In that regard, the stock appears to present a compelling opportunity. However, in order for this dividend yield to be sustainable in the long term, Gear Energy needs higher oil prices.

This also reveals the biggest risk in front of the company - a further fall in oil prices. This could come from two sources - lower oil prices in general, or expansion of the WCS-WTI spread. While I'm bullish on oil in general, short-term drop possibilities are not to be ignored, as the recession fears rage.

Conclusion

The 12% dividend yield of Gear Energy should not be taken for granted. The company may have trouble funding the monthly distributions to shareholders entirely through operating cash flows and may have to dip into debt financing. That being said, the shrinking of the WCS-WTI spread is a positive development and the balance sheet allows for the dividend to be maintained in the short term at the expense of some additional debt.

For further details see:

Gear Energy: Watch Out For The 12% Dividend Yield Sustainability