RTX - General Dynamics: A Top-Tier Dividend Stock With Improving Tailwinds

2023-10-18 15:00:12 ET

Summary

- General Dynamics is one of America's top defense contractors with a market cap of nearly $70 billion.

- The company has a diverse business portfolio, including aerospace, military hardware production, and shipbuilding.

- GD has a strong dividend growth history and has consistently outperformed the market, making it an attractive investment option.

Introduction

It's time to talk about General Dynamics Corporation ( GD ) . With a market cap of almost $70 billion, it's one of America's five defense contractor giants. On July 9, I wrote an article titled General Dynamics Is Poised For Growth And Way Too Cheap . Since then, the stock has returned 13%, beating the S&P 500 (SP500) by roughly 14 points.

Now, it's time to look ahead, as the company is scheduled to report its earnings on October 25 before the market opens.

In this article, I'll walk you through new developments, the company's most recent comments and results, and what to make of the longer-term risk/reward.

So, let's get to it!

The Benefits Of General Dynamics

Earlier this week, I wrote an article covering RTX Corporation ( RTX ), formerly known as Raytheon Technologies. In that article, I updated readers on new investments in the defense space.

In my 20-stock dividend growth portfolio, I hold four defense contractors. These account for roughly 27% of my total exposure.

Leo Nelissen (Portfolio Top 5 Holdings)

That's a lot, and based on my belief that defense companies are a great way to benefit from long-term dividend growth with a favorable risk/reward.

After all, most defense sales are anti-cyclical.

General Dynamics is the only major defense contractor I don't own.

As I often say, this is not based on GD being a bad company. It's only based on overlapping exposure. As I own four defense companies, there's really no need to add a fifth. I would even make the case that owning four contractors is a bit much, but I have my reasons, which I often communicate with readers.

GD is a fascinating company for a number of reasons.

One reason is its diversification.

Roughly a fifth of its sales are generated in its Aerospace segment, which is mainly commercial aviation through its Gulfstream business. So, ultra-high-end travel, one might say.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Technologies | ||||

| 12,457 | ||||

| 32.4 % | ||||

| 12,492 | ||||

| 31.7 % | ||||

| Marine Systems | ||||

| 10,526 | ||||

| 27.4 % | ||||

| 11,040 | ||||

| 28.0 % | ||||

| Aerospace | ||||

| 8,135 | ||||

| 21.1 % | ||||

| 8,567 | ||||

| 21.7 % | ||||

| Combat Systems | ||||

| 7,351 | ||||

| 19.1 % | ||||

| 7,308 | ||||

| 18.5 % |

The company is also the largest producer of military hardware. It produces the Abrams Main Battle Tank, the Stryker wheeled vehicle, light armored vehicles, and other tactical vehicles that are the backbone of various military operations and logistics operations.

General Dynamics

Several companies that I invest in supply General Dynamics with electronics, weapons, and whatnot for these vehicles, which is why I don't need to add GD to my portfolio to get this kind of exposure.

For example, Northrop Grumman ( NOC ) produces protection systems for the Abrams tank - among many other things.

On top of the increasing importance of its Technologies segment, the company is also one of two companies that dominate the production of major Navy ships and submarines.

General Dynamics produces the Virginia-Class submarine, the Columbia-class submarine, and the Arleigh Burke-class destroyer - among other ships.

Having said that, GD is also known for its dividend, maybe more than any of its peers.

While its 2.2% yield isn't something to write home about, the dividend has been hiked for 29 consecutive years, making General Dynamics a dividend aristocrat.

Furthermore, the dividend is protected by a 42% payout ratio, which paved the way for a 5-year dividend CAGR of 7.5%.

On March 9, the company hiked its dividend by 4.8%.

Additionally, the company is known for buying back stock. Over the past ten years, it has bought back 23% of its shares, which added to its strong performance on the stock market.

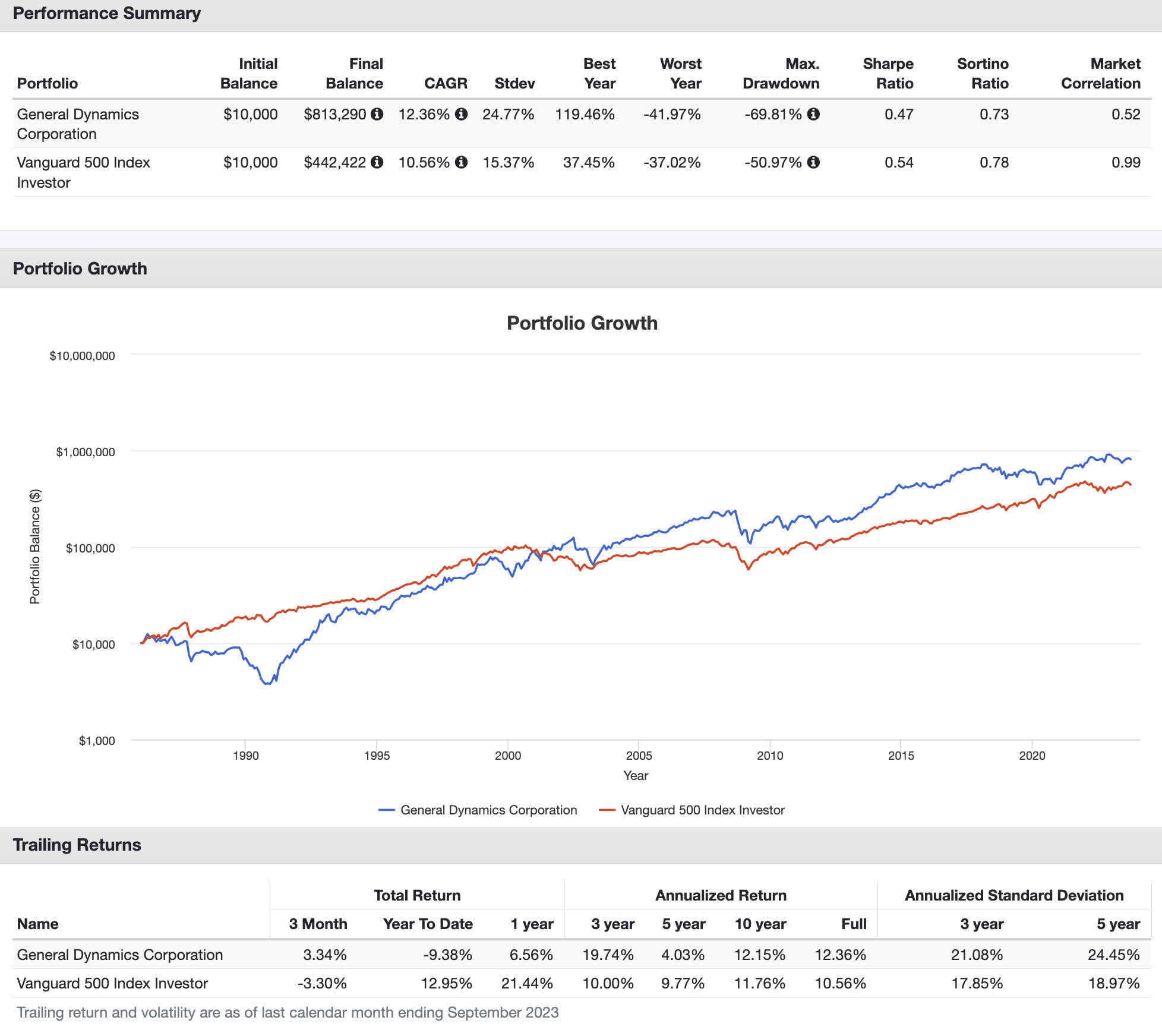

Since 1986, GD shares have returned 12.4% per year, beating the S&P 500 ((SP500)) by almost 200 basis points per year. As the lower part of the chart below shows, the company has consistently outperformed the market. The only interval listed below with underperformance is the past five years. This is due to the pandemic, which hit commercial aviation and the supply chain problems that followed. Especially high-tech defense companies like GD suffered from these issues.

{kind=link}

Overall, GD is a fantastic dividend growth stock for conservative investors.

It's a true sleep-well-at-night company.

Having said that, there's more to discuss!

GD Is Seeing Improving Revenue Growth

Since my article in early June, a lot has happened.

The two most important things are:

- The company's earnings results.

- The war between Israel and Hamas.

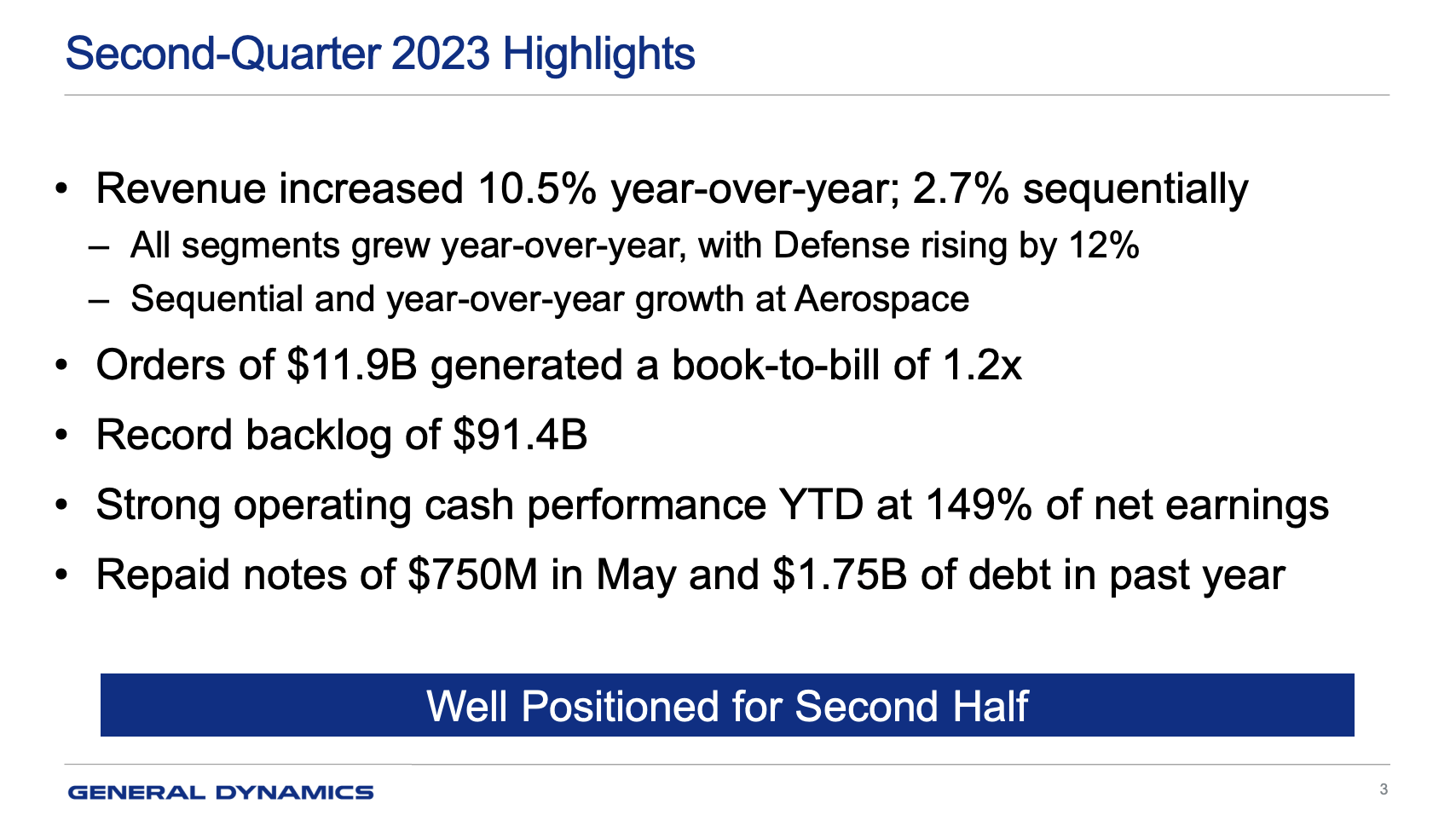

With regard to the second-quarter earnings , it seems the company is in a new growth uplift, which is likely to be confirmed in its Q3 2023 earnings call.

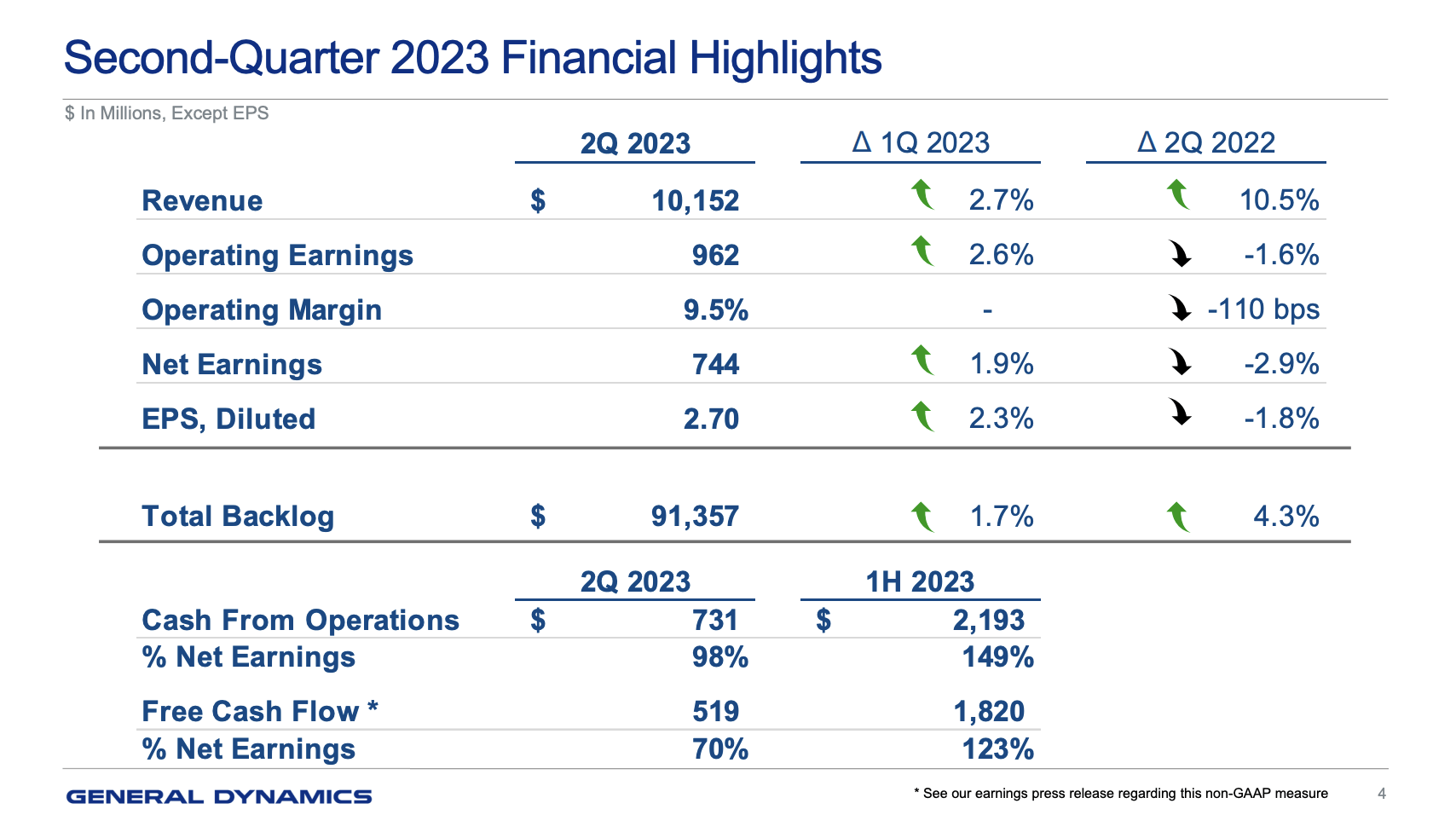

In the second quarter, GD reported earnings of $2.70 per diluted share on revenue of $10.2 billion. The defense segments experienced a notable 12% revenue increase, while Aerospace saw a 4.6% increase.

{kind=link}

Despite the revenue surge, operating and net earnings were lower compared to the year-ago quarter. However, they surpassed consensus estimates by $0.14 per share, largely due to operational efficiencies.

{kind=link}

The operating difficulties have been an issue in the entire sector since the pandemic. Year-to-date, GD sales are up 7.8%. Operating earnings are up less than 1% during this period.

However, orders are strong - especially in light of ongoing geopolitical challenges that I expect to last for many years - if not decades.

The company achieved a book-to-bill ratio of 1.2x, showcasing strong order activity across all segments. In other words, for every dollar worth of finished work, the company gets $1.20 in new orders, which is indicative of higher future growth.

- Combat Systems and Aerospace stood out with book-to-bills of 1.4x and 1.3x, respectively.

- The quarter ended with a record-level backlog of $91.4 billion, up 1.7% from the previous quarter.

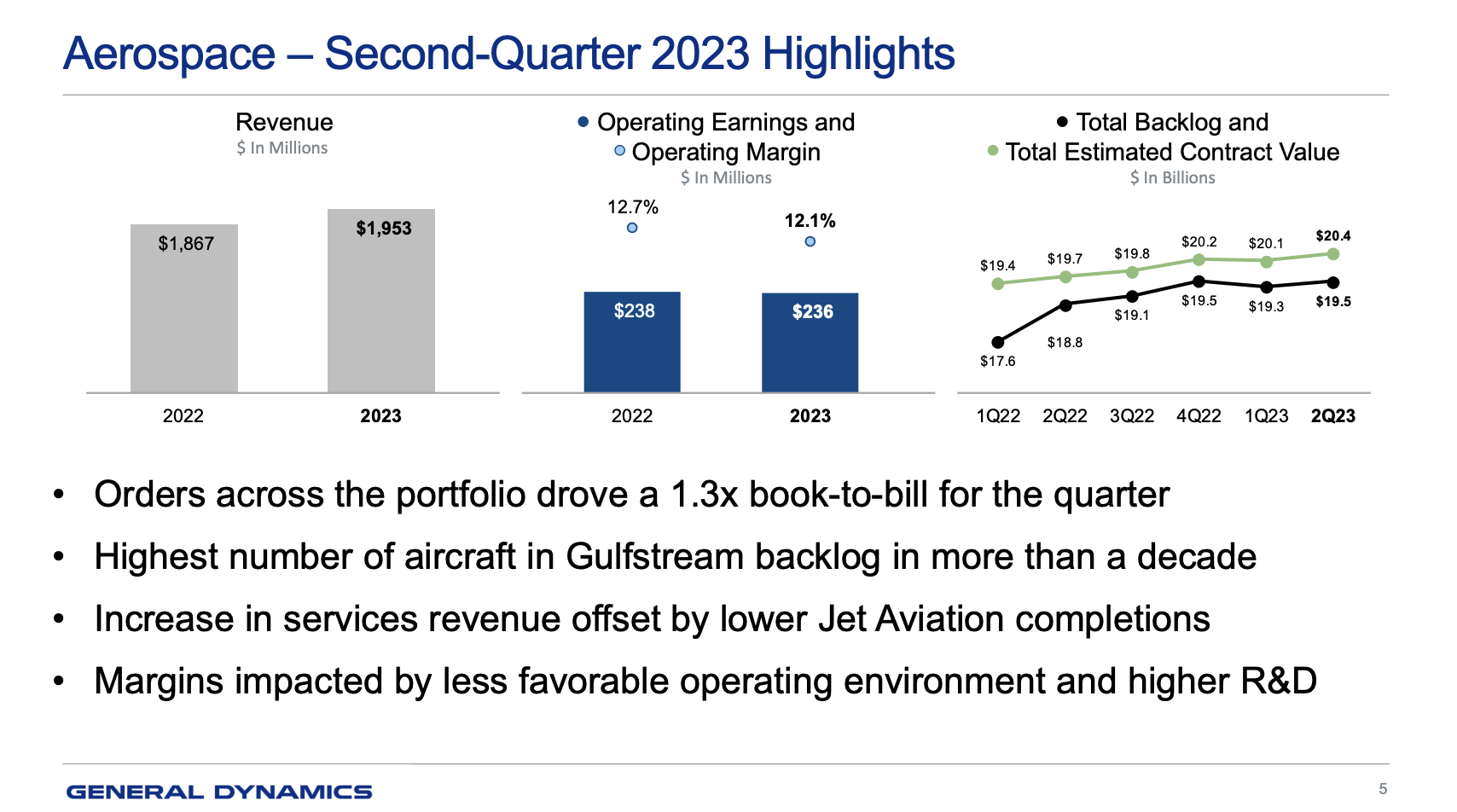

The Aerospace sector reported revenue of $1.95 billion and operating earnings of $236 million, boasting a 12.1% operating margin.

{kind=link}

The revenue increase of $86 million from the previous year's second quarter was attributed to additional new aircraft deliveries and heightened Gulfstream service center volume, slightly offset by reduced volume in Jet Aviation's completion center.

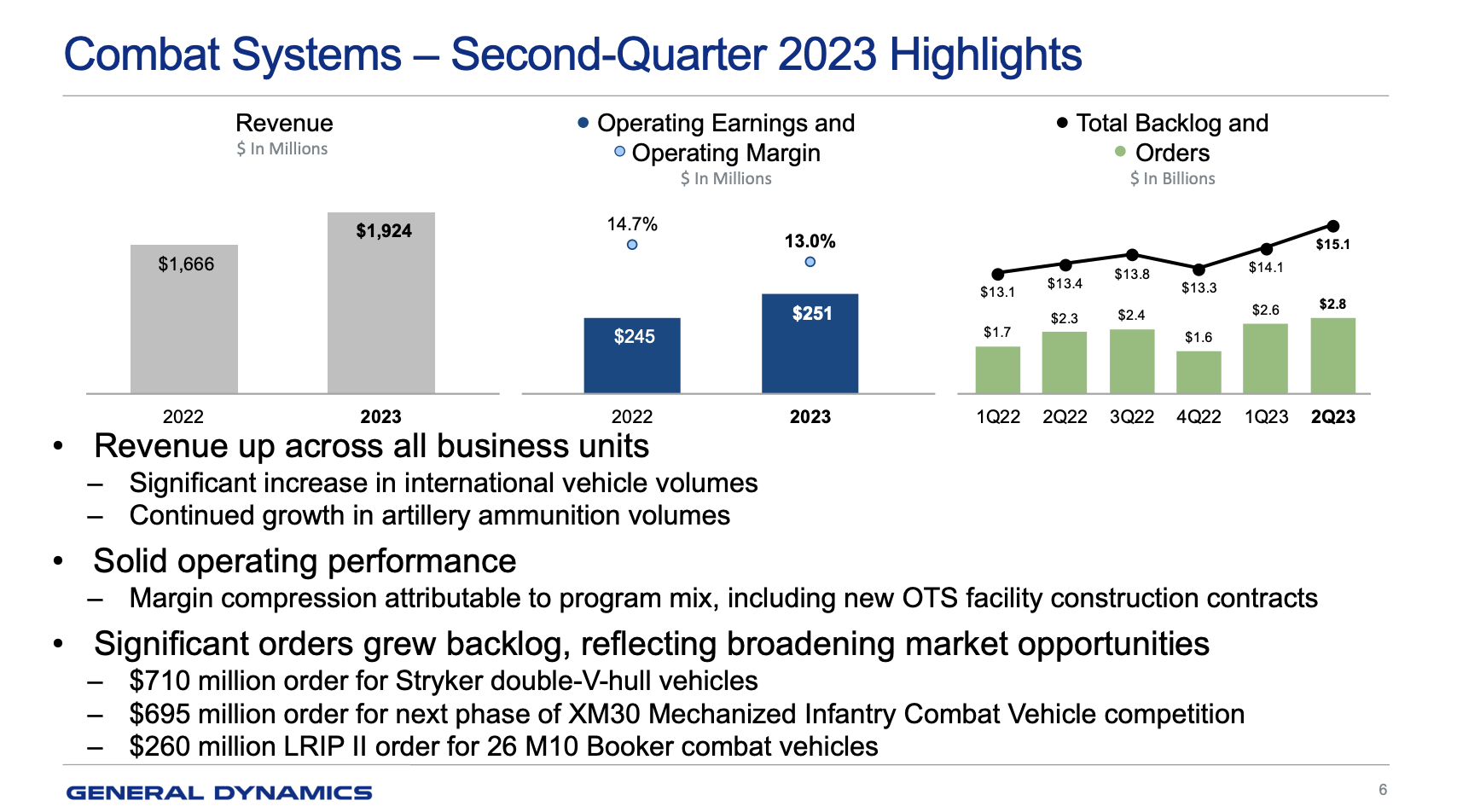

Combat Systems revenue surged by 15.5% over the year-ago quarter, amounting to $1.92 billion.

Noteworthy increases in revenue were fueled by international vehicle programs, particularly in Land Systems and European Land Systems.

This makes sense in light of the Ukraine war and increased defense spending in Europe. This segment alone has more than $15 billion in backlog orders.

{kind=link}

Marine Systems showed robust revenue growth as well, with a staggering 15.4% increase against the year-ago quarter, amounting to $3.1 billion. This growth was primarily attributed to Columbia class construction and engineering volume.

Future Expectations & What To Expect In Q3 2023 Earnings

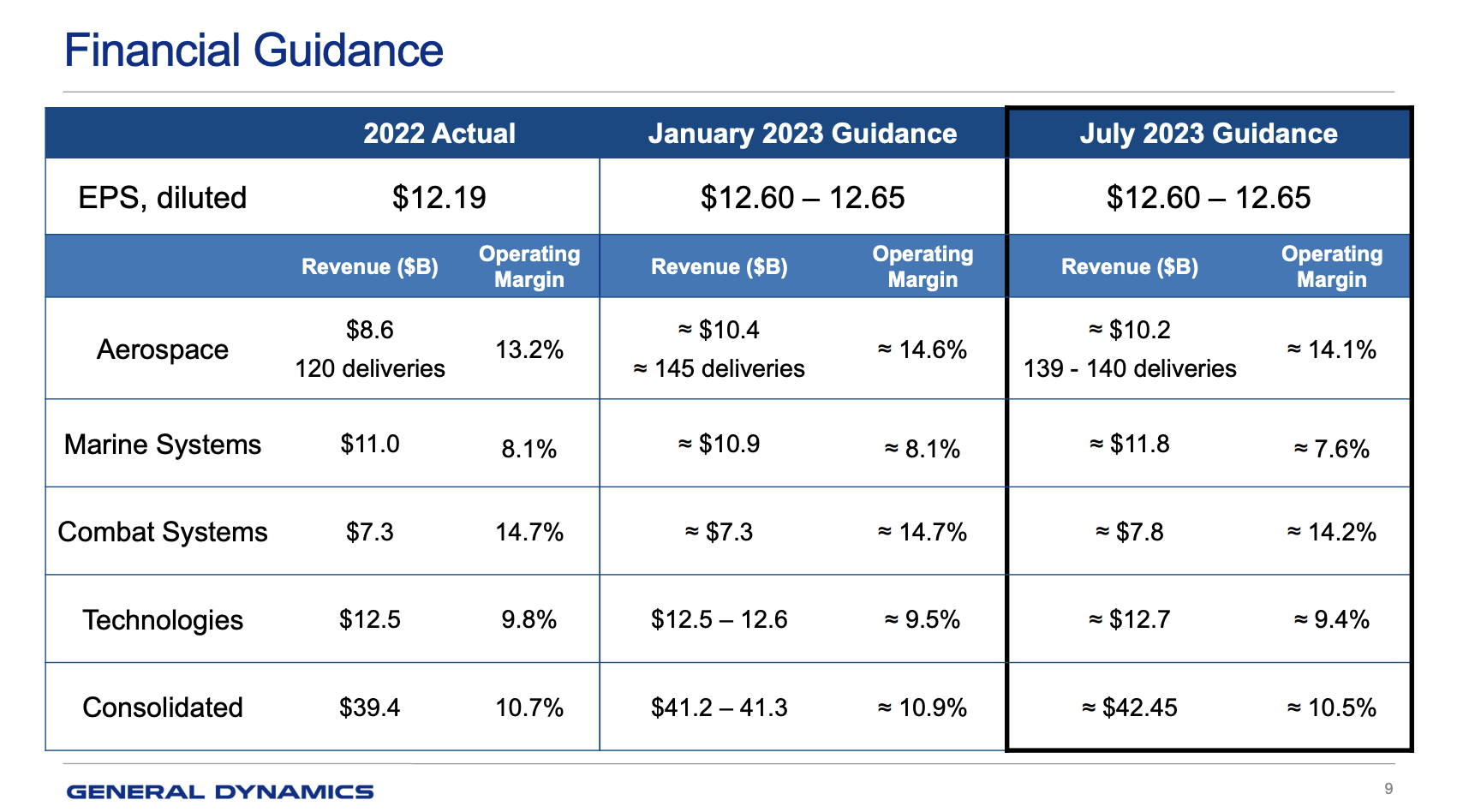

When the company updated its full-year guidance in July, its wide outlook indicated higher revenue than initially expected, although with a slightly lower operating margin.

This is the usual issue facing defense contractors: strong revenue growth but the inability to turn this into strong earnings growth.

{kind=link}

Note that revenue expectations were higher in every segment but Aerospace. This is due to lower deliveries, nothing serious. After all, this segment's backlog is at a decade-high.

Margin expectations were lower in every single segment.

Having said that, I expect the company to beat Q3 2023 earnings. Using Nasdaq data, the company is expected to report $2.87 in EPS, which is based on nine estimates. The company has seen one downgrade and one upgrade over the past four weeks.

In Q3 2022, the company reported $3.26 in EPS, which was $0.10 higher than expected.

{kind=link}

The bar is clearly very low for GD, which is one of the reasons why I expect the company to beat expectations. I also expect that the odds are favorable for a post-earnings rally if the company is able to show that operating issues are fading.

Even a hint that the company is becoming more efficient could cause analysts to boost future earnings expectations.

I also expect the company to comment on the changing geopolitical environment, which emphasizes defense spending.

However, I do not expect that GD will give us specific longer-term expectations. It's unlikely that defense companies will do this, as it's still unclear which defense areas Washington will prioritize.

We'll likely have to wait until early 2024 for these comments.

This is what Lockheed Martin ( LMT ) said this week in its Q3 2023 earnings call (emphasis added):

We are also reaffirming our full year 2023 financial outlook for sales , profit, EPS and free cash flow. Given the current status of the 2024 U.S. defense budget, global geopolitical tensions and the macroeconomic environment, we will provide our expectations for our 2024 financial outlook during our full year 2023 earnings call in January .

On the U.S. budget, though the specific trajectory of the future U.S. defense budget is still in process between the administration and Congress, the global threat landscape is increasingly elevated . Our robust backlog reflects the relevance and importance of the Lockheed Martin portfolio and elevating deterrence to great power conflict involving the United States and its allies and the solid positioning of our business to serve our domestic and international customers.

The only way I see a potential post-earnings selloff is if the company mentions prolonged operating efficiencies, which would come as a shock to investors.

However, given my view on supply chains and the demand environment, I'm bullish going into earnings.

Needless to say, this is not an encouragement to get anyone to bet on earnings! Earnings provide us with valuable intel. They are not a way to make a quick buck. At least not for most investors like me.

GD Stock Valuation

The valuation is a bit tricky. For two reasons:

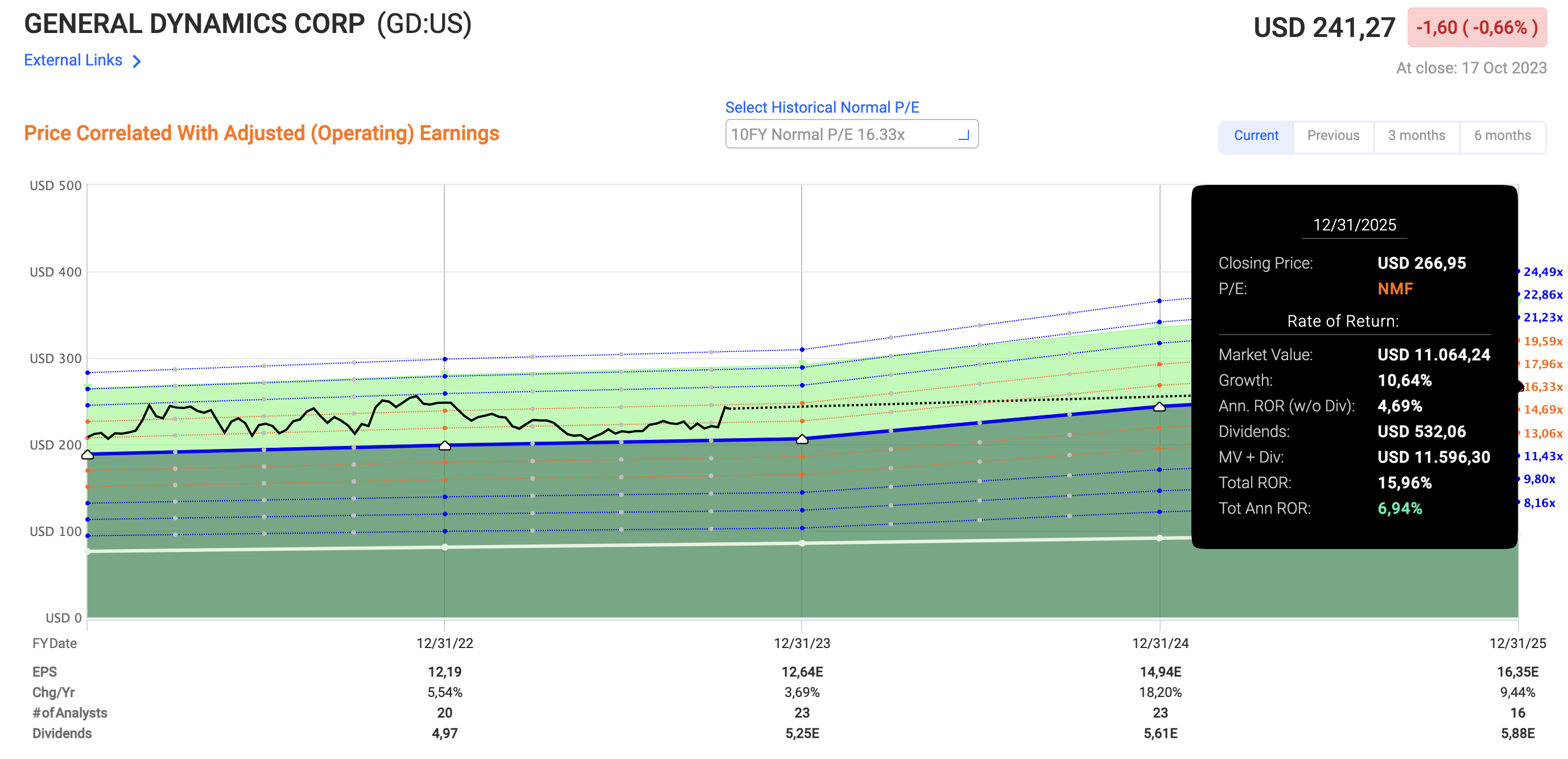

- GD is trading at 19x earnings. The 10-year average valuation is 16.3x earnings. A return to that valuation by 2025 would result in a theoretical annualized total return of 7%, as seen in the chart below. This is based on 3.7% expected earnings growth in 2023, 18.2% expected earnings growth in 2024, and 9.4% expected earnings growth in 2025.

{kind=link}

In light of high expected growth, the valuation may remain above 17x earnings, which would suggest annual returns between 7% and 12%.

That's not bad. However, here's reason 2.

- GD is somewhat stuck in the middle. While it is rapidly growing, there are defense players like L3Harris Technologies ( LHX ) and RTX Corp that trade at much more favorable valuations. Even Northrop is expected to double its free cash flow by 2028.

GD is a solid stock. I'm bullish on it, and I believe that it will continue to beat the market on a long-term basis.

However, I wouldn't chase this stock after rallies. Investors should wait for pullbacks.

The next earnings call may provide a buying opportunity, although my bet would be an earnings beat and higher prices.

I stick to the price target I gave the stock in my prior article, which is $280.

Takeaway

General Dynamics presents a promising investment prospect characterized by diverse business segments, robust dividend growth history, and consistent market outperformance.

The Q2 2023 earnings report indicated a positive growth trajectory, underlined by a substantial backlog and strong order activity, particularly in light of ongoing geopolitical challenges.

The upcoming earnings call is crucial and may serve as a catalyst for potential post-earnings market movements, especially if GD showcases improving operational efficiencies, which is what investors will care mostly about.

While GD's current valuation exceeds its historical average, the anticipation of sustained growth suggests the possibility of substantial returns.

However, competition from defense players with more attractive valuations poses a challenge, at least from an investors' point of view.

Prudent investors may opt to wait for potential market corrections before entering a position, although this may come with missing more upside if the company beats earnings expectations.

For further details see:

General Dynamics: A Top-Tier Dividend Stock With Improving Tailwinds