LMT - General Dynamics: Positive Risk/Reward Going Into Q4 Earnings

Summary

- General Dynamics Corporation is a major U.S. Defense Contractor with visible earnings, a strong competitive position, and strong '23 earnings growth.

- The company has a strong backlog and the current global threat environment suggests major upside is possible, if not likely.

- The company has a strong management team that has splendidly navigated past and recent challenges.

- General Dynamics has many superior characteristics to peers, and its aerospace sector has excellent exposure to easing financial conditions.

- Much of the company's future revenue is the most solid kind of defense revenue, that from "sacred cow" projects.

So far, 2023 markets have been much more positive than many suspected. However, trouble likely lurks just around the corner. The consensus is that this will be a tough earnings season, and growth will become increasingly scarce throughout the year. Indeed, the earnings season is not off to a good start. According to FactSet , the magnitude and number of earnings surprises are below their 5-year and 10-yr averages. The total of companies reporting as of Friday beat estimates by 3.3%, which is well below the 5-year average of an 8.6% differential between expected and reported earnings.

{kind=link}

The other thing about this quarter is that it will consist of a great deal of sandbagging from management teams. The uncertainty that pervades early 2023 gives management teams little incentive not to lay out worst-case scenarios in hopes of outperforming them within reasonable and legal bounds. This is just the nature of the beast when you are a public company. This can add another layer of uncertainty to earnings in a time already fraught with uncertainty, apprehension, and fears of a potential recession or Fed policy error.

Despite this uncertainty, one sector where there is slated to be some of the most robust earnings growth in the coming year is Industrials. My favorite part of this favored sector is Defense & Aerospace because of the industry's defensive characteristics and secular tailwinds; both help mitigate uncertainty during difficult times for markets. General Dynamics Corporation ( GD ) is one of my favorite companies in the industry. Defense and Aerospace, as a sector, provides investors a unique profile of the potential for above consensus earnings growth mixed with the acyclical revenue drivers that give the industry its defensive characteristics.

{kind=link}

The Defense & Aerospace Industry is considered more defensive than most industries because it primarily depends on the U.S. government and foreign government spending on Defense. This is generally easier to predict than fickle economic activity dependent on the activity of billions of people. Uncle Sam and what he's got to spend to counter mounting threats is the main thing driving revenue instead, and the Defense budget tends to grow steadily. This is the case during regular times. However, in times like we are currently experiencing, where uncertainty around and severity of the geopolitical threats are more in flux than it's been in decades, I suspect that many estimates for earnings over the next few years are light. This is because the spending of the U.S. and our allies on Defense over the coming years is possibly going to increase a lot more than most currently expect.

In a previous piece on Raytheon ( RTX ), I argued why the current War in Ukraine would almost certainly demand far more assistance from the U.S. and allies than is possible to imagine at this point. The rising threat from China will continue to play out over the coming years and will require ever-increasing spending to maintain two-front nuclear deterrence. General Dynamics has the contract for the next generation of Nuclear Submarines, one of the essential elements of the U.S. nuclear triad. This is known as a "sacred cow" project due to its strategic significance and deterrent factor.

Bloomberg, DoD

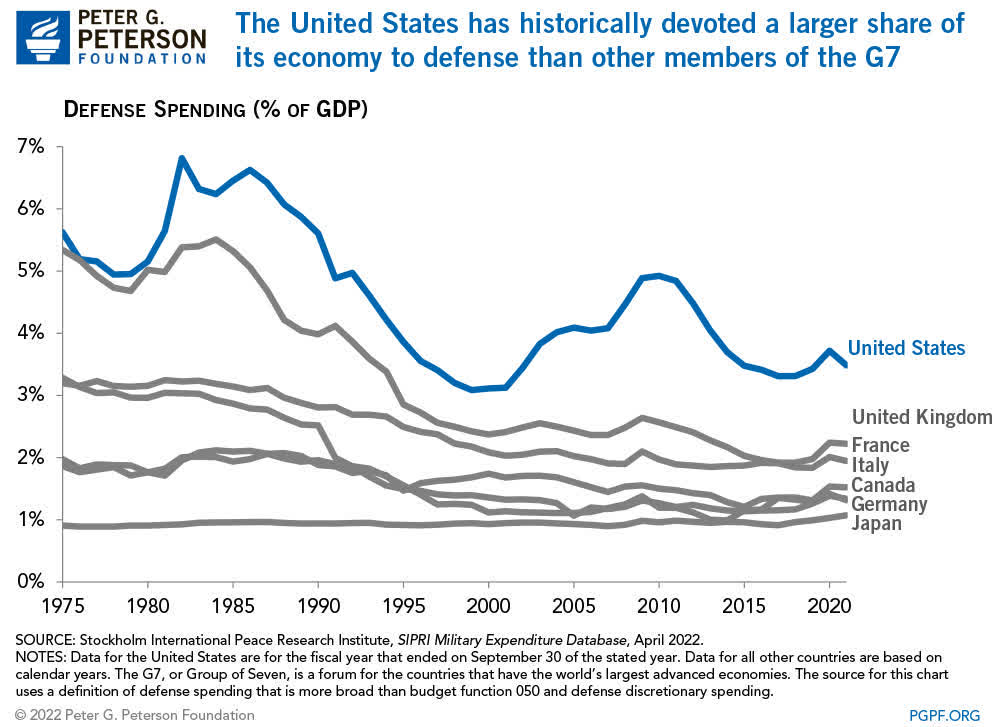

While the current numbers being thrown around with regards to the U.S. Defense budget seem extraordinarily high, the aggregate levels of spending as a share of GDP are historically low, especially compared to times when the United States has been postured toward confronting another major global power. There are a lot of unknowns going into the year 2023. However, given current information, one pretty sure thing is that the War in Ukraine (the "War") likely won't end anytime soon. The demands of a high-intensity conflict like that unfolding in Ukraine simultaneously with increasing needs to counter Chinese capabilities almost necessarily means the Defense Spending will likelier move closer to the proportions of GDP seen during the 1980s.

{kind=link}

General Dynamics is the most critical company for shipbuilding, the most significant portion of the defense budget that is still growing (unlike aircraft). It's also a leader in C4I, whose growth potential may be underappreciated by current estimates, given the real-world importance it's been shown to have on the ground in Ukraine. The War has demonstrated in real-life what defense wiz kids have been theorizing over the past few years. Warfare constantly evolves, and there's a constantly shifting balance between offensive and defensive armaments.

Ukraine has shown that new technological capabilities have upended the 20th Century's focus on offensive combined arms operations. It will be a direct beneficiary of the changing focus in military spending that is likely to follow in a way that may very well exceed the current estimates of the sell-side analysts. Russia's unprecedented losses of equipment and personnel attest to this. Russia's failure has also shown that the types of command and control systems (like encrypted communications ) that General Dynamics specializes in are not only nice-to-have but absolutely essential. European allies with frontiers near or bordering Russia have certainly taken note.

General Dynamics Has an Advantageous Competitive Position and Strong Management

In a crisis there's nowhere for weakness to hide- Phebe Novakovic, General Dynamics CEO

Phebe Novakovic is one of the most competent and qualified CEOs that you've never heard about. Don't be surprised if she maintains a bit of a low profile, she is a former spook (Central Intelligence Agency). She is focused, believes in the mission of her company, and has admirably led it through the unprecedented challenges of the pandemic. She shone through the process. However, what I really like is her experience. She's given a lot of her life to public service through the military and the Agency.

Even more importantly for her current role, though, she had firsthand experience, which distinguishes her among her peers, of working not just at the Pentagon but also managing the Defense Budget for the Clinton Administration while at OMB. She's a seasoned manager with the right experience. She's a proven and capable steward of shareholder capital and also understands her business and its mission thoroughly. The company has a demonstrated track record of being a real compounder that outperforms peers over the long term.

{kind=link}

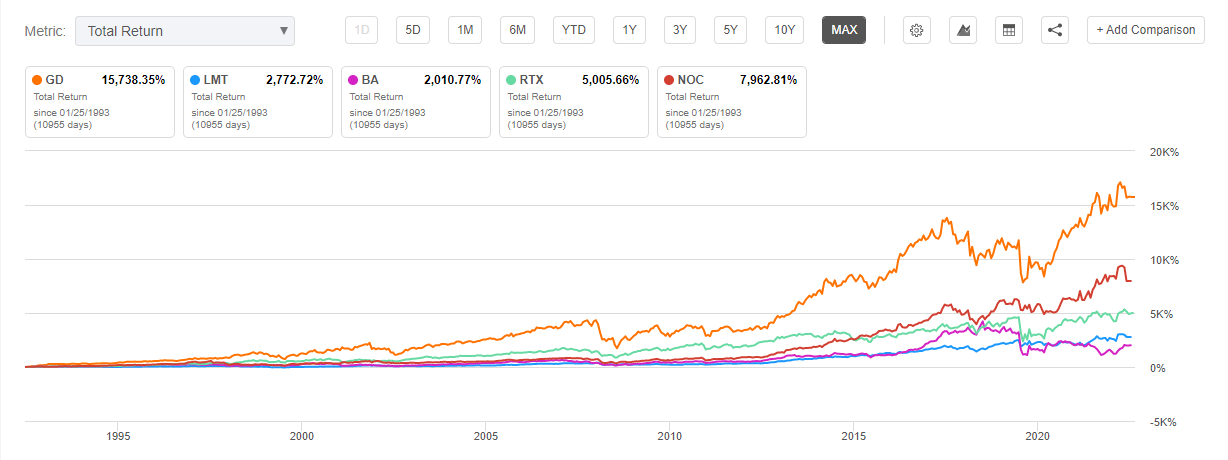

General Dynamics is in a unique and enviable position within the Aerospace & Defense Industry. I'd refer to it as the "biggest of the little guys." It is large enough to compete for some of the largest and most lucrative contracts, yet it can afford to be leaner and more focused than some of its lumbering big brothers, like Lockheed Martin ( LMT ) and Boeing ( BA ). For example, the scrappy Defense Manufacturer secured the $22.2 multi-year contract for nuclear powered attack submarines, which was the largest contract in the history of the U.S. Navy. It has a duopoly in shipbuilding with Huntington-Ingalls ( HII ).

{kind=link}

General Dynamics Corporation has a healthy product mix and a massive backlog of $126 billion of the potential contract value on a market cap that is about half of that. It is concentrated on "sacred cow" projects like nuclear submarines and may also benefit from the growing discussions about the need for main battle tanks in the worsening Ukraine War. Poland has already ordered more Abrams tanks from the firm, and this likely won't be the last order from allies.

The company produces the Abrams Tank, the main battle tank of the United States Army. However, one of the most promising areas for future growth is the area of command systems, known as Command, Control, Communications, Computers and Intelligence, or C4I. This segment has been plagued by supply disruptions, particularly in chips, but the demand is not only existing but increasing.

General Dynamics not only has a specialty in C4I, but growth in this area should be particularly robust as the realities on the ground in Ukraine have demonstrated the supreme importance of having a cutting-edge ability in this area. The Ukrainians have relied on a better implementation of modern technology, satellites, and encrypted communications into their military structure, and militaries worldwide have seen this superiority deployed to devastating effects against the Russians.

Why I'm Comfortable Recommending General Dynamics A Day Before Q4 Earnings

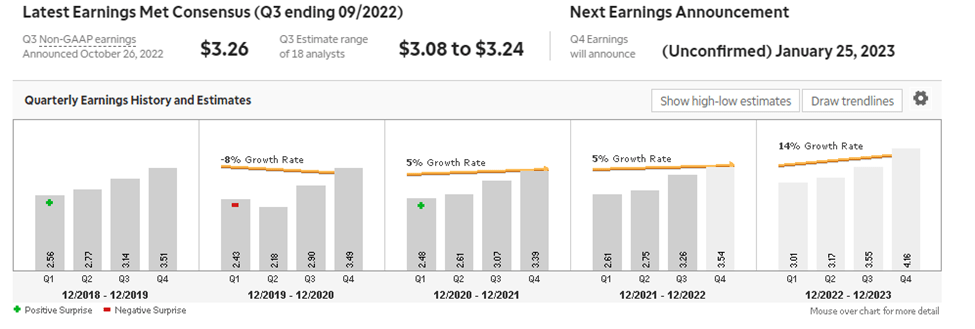

I'll let you in on a little secret. Of us poor folks who have tried to make a living providing equity research, it is often common practice to not recommend a stock right before an earnings report, for obvious reasons. As I mentioned, this is a sandbag quarter if there's ever been one given all the uncertainty and mounting pressures on the consumer, earnings, and margins. However, General Dynamics has a long track record of being a "no-drama" earnings name for the most part, and it's current backlog make this a trend that likely endures in the short and medium term.

{kind=link}

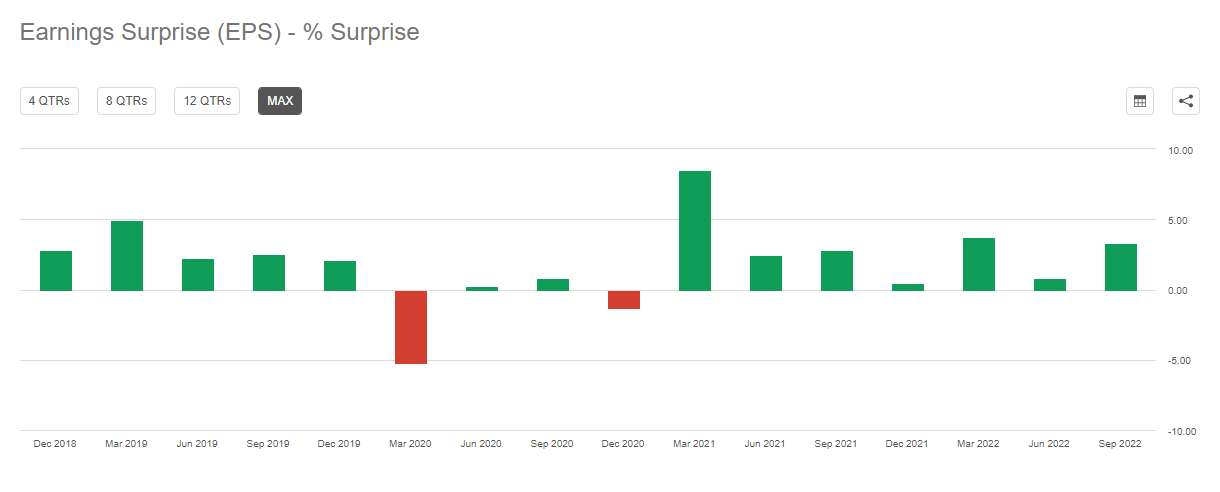

Take a look above and you can see that the company has only missed expectations on EPS twice in the last sixteen quarters, and one of those was in March 2020. I think they can have a pass for that one. The four segments are pretty evenly diversified which likely contributes to the company's stability. The company's Aerospace segment, which produces the cherished Gulfstream Jet, has had one of its best years in a decade which helped bolster the weakness occurring in the largest Defense Segment, Technologies.

Company Reports

However, the supply chain issues are being dealt with, and as I mentioned in my article on Raytheon Uncle Sam will likely be providing some help here as well. General Dynamics was a leader in rectifying these problems and keeping the ship running during COVID. It advances billions to key suppliers experiencing problems and made the situation less acute than it could have been. I expect growth to pick up significantly in coming quarters across the three defense segments.

Company Reports

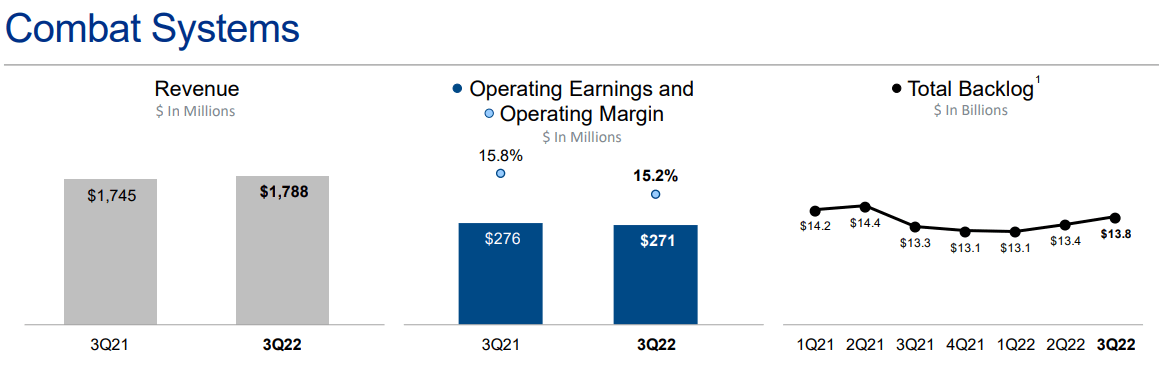

Last quarter's growth was a bit lackluster in Combat Systems and Technologies. However, I've already mentioned that the Abrams Tank is going to become much more sought after. There is mounting pressure from many sources for the Germans to allow their allies to supply Leopard Tanks . Many allies who deplete their Leopard stocks may be keen to replace them with the well-laureled Abrams, as fickle and difficult to maintain as it may be. The mere prospect of open armored warfare in the coming spring offensive likely launched by Russia will likely increase demand. Many nations who might have thought armored warfare was a thing of the past will hurriedly re-adjust to a world where it is again occurring in a way that sways the outcomes of conflict.

{kind=link}

The other thing is this. General Dynamics has a lot of institutional ownership and a lot of long-term holders because of its status as a dividend aristocrat (has raised every year for the last quarter century). About 80% of the float is held by institutions. This helps support the price at a time where there's a lot of bearishness across Wall Street. However, and quite sadly, I suspect the course of events in the globe will likely make the case for owning the premier defense manufacturer more and more self-evident as the War in Ukraine progresses and as a bi-partisan consensus to oppose China's military buildup continues to coalesce. It also has great metrics relative to peers on profitability.

The company's metrics

Seeking Alpha

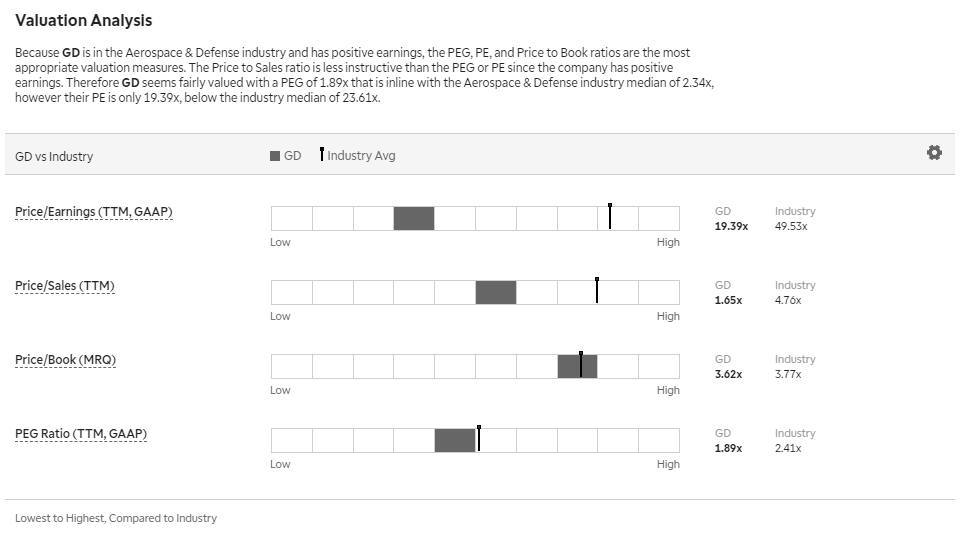

There's a lot of other metrics where the firm has superior metrics to peers as well. This is always supportive of a premier valuation, which the firm has had at times, but I frankly view it as a bargain after the recent pullback. I think you should buy General Dynamics Corporation stock even in the event a small earnings miss occurs, particularly if it is because of supply chain issues that should be more than midway through resolving.

{kind=link}

As you can see, across several metrics, the valuation of General Dynamics is more attractive than the industry averages. I think the recent price weakness is definitely an opportunity to raise exposure to a well-managed name with projected earnings momentum and attractive valuation going into 2023. As I mentioned before, General Dynamics Corporation stock is a great mix of a traditionally defensive area benefitting from a generational rise in defense spending and a new geopolitical environment marked by great power competition.

General Dynamics Meets My Criteria for Long Recommendations as 2023 Begins

The Fed and the bond market are engaged in a high-stakes game of poker that will significantly impact the ultimate path of markets in 2023. As I said in my outlook for this year, I tend to sympathize with the position that the bond market will ultimately prove correct and the Fed will be forced to reverse direction earlier than its members' projections would infer. This is not a conclusion I am by any means certain of. Thus my strategy for long picks this year involves stocks with the following attributes.

- Strong competitive position and strong management teams

- High visibility into future earnings is less cyclical than most of the market and preferable earnings that are accelerating through 2023.

- Favorable track recorded and stated management intent of providing risk mitigation and price support through dividends and buybacks.

- Companies that are direct beneficiaries of transformational or secular trends have a high likelihood of holding steady regardless of what happens with the Fed and recession.

I think I've demonstrated how the stock qualifies for most of these points but I'd like to highlight one of the most important criteria. The company is expected to have accelerating and above-trend earnings for 2023. In a market where earnings growth will be increasingly hard to find, this is one of the main characteristics I seek in my long recommendations for early 2023. Earnings are currently projected to grow at a rate of 16% in Q1 and Q2, then slow to 9% in Q3, and then grow 18% in the fourth quarter. These forecasts quite possibly could be light.

{kind=link}

Things change fast in high-intensity conflicts. At the beginning of WWII, the United States produced very few planes, but by 1944 it turned nearly 100,000 of the assembly lines. Orders have a higher likelihood of breaking to the upside of targets given the threat environment. While there's a lot of reasons to love this stock, that doesn't mean there aren't plenty of risks.

Risks to My Bearish Thesis for General Dynamics

Recently there were rumors that the House GOP made a dramatic cuts in defense spending a condition of allowing Kevin McCarthy to rise to the speakership. Since then, the Republicans have made clear that they want to see no cuts in defense. One of the things that mitigates risk to defense spending even when the budget of the United States, and proposed spending cuts, become front and center is that the industry has years of experiencing in making it very difficult for many politicians to kill certain defense programs. Look at the footprint of F-35 production below to illustrate this concept.

Business Insider

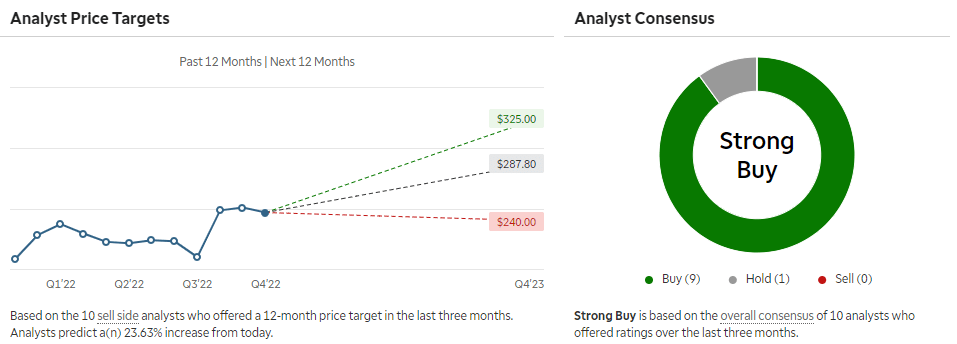

This old trick is even more effective in a heightened threat environment like we are facing in 2023. So, I think there's certainly a possibility that Defense spending faces some difficult decisions and debates as the debt ceiling crisis progresses, but ultimately it will likely be spared. The stakes are too high, and despite a vocal minority in the Republican Party, much of the establishment is proud of and committed to the support for Ukraine. Another source of comfort for those buying General Dynamics Corporation stock is that after the recent selloff, it is below all the major analyst targets and is almost unanimously recommended by the sell-side.

{kind=link}

I think the biggest single risk continues to be the supply chain. General Dynamics' largest defense segment is currently vexed by supply shortages particularly of high-end chips. The risk from Congress, I believe, was overstated by Goldman Sachs in their recent downgrade of Defense & Aerospace names. They think there is risk that the U.S. Defense budget will contract. I am plainly stating that I think that risk is much lower than the consensus seems to think. However, if these analysts are right and U.S. Defense spending contracts in a significant way, then there is definitely downside for the industry including General Dynamics.

{kind=link}

The firm also has labor issues in the high-touch shipbuilding business which has emerged. This could impede the realization of key revenue on important contracts, including for nuclear submarines. However, as I mentioned before, the "sacred cow" nature of this project and the budding nuclear buildup of the Chinese make augmentations to the contracts more likely than cuts in my estimation. A great thing about the business is that it's steady, even if growth comes in lighter than expected as a result of legislative negotiations. Take Combat systems. Even if there's a cutback in Naval Spending or continuing supply chain issues, this segment's specialization in munition and ordnance, which are increasingly scarce by the day, gives a potential upside kicker as the War in Ukraine intensifies and allies drain their ammunition stocks.

One of the other characteristics of General Dynamics Corporation I like that mitigates risk is that it has a better balance sheet than a lot of peers. Again, this appears a chronic symptom of good management that is always a good check against risk.

Conclusion

General Dynamics Corporation is one of my favorite Defense & Aerospace names and I recommend them without reservation on the eve of their Q4 earnings report. The firm's full year results should provide additional information to inform your decision, but even if they fall short and the stock sells off, I believe this will be a great buying opportunity.

General Dynamics Corporation is benefitting from transformational and secular trends, it has a strong competitive position in an oligopolistic industry, superior profitability, a great product mix for a world with evolving defense needs, and a solid management team. A strong dividend and buyback policy add a margin of safety for General Dynamics Corporation investors who want a stock you can buy and hold for the brave new world we find ourselves in the perilous year of 2023.

For further details see:

General Dynamics: Positive Risk/Reward Going Into Q4 Earnings