RTX - General Electric: Not For Me Anymore

2023-05-10 08:30:08 ET

Summary

- General Electric has had a great run in recent months, with shares soaring as the market comes to realize the firm's value and potential.

- This is great, but the stock does not seem to offer much additional potential to make it worth holding onto for me.

- This is based on an assessment of its core aviation business that certainly comprises the rest of its remaining value.

- The company is still a solid firm that should achieve nice upside in the long run, but the easy money has probably been made.

As a long-oriented value investor, my ultimate goal when buying a stock is to purchase it with the idea in mind that, over a span of three to five years, that stock can generate attractive annualized returns that comfortably exceed with the broader market should. However, I do not pigeonhole myself to this. If shares of a company rise enough, I have no problem divesting them. And with the recent movement seen by industrial conglomerate General Electric ( GE ), I do believe that now is that moment to sell my stake and move on. Make no mistake; I do believe that the company has done some remarkable things over the past couple of years. Recently, it has drastically outperformed the broader market. And I still do believe that it is a strong enough prospect to warrant a ‘buy’ rating. But I am no longer of the opinion that it offers enough upside to justify the ‘strong buy’ rating that I assigned the company last year. This assessment was based on my own view of the value of what remains within the enterprise. In particular, my emphasis was on its aviation operations under what management now calls GE Aerospace.

A great ride

No matter how you stack it, things have been going quite well for investors in General Electric. Since spinning off GE HealthCare Technologies ( GEHC ) into a separate publicly traded company earlier this year, General Electric has seen almost nothing but upside. Since that spinoff, shareholders have seen upside of roughly 44%. Given this awesome trajectory, I felt it was time to take a step back and reassess the picture. After all, even the best opportunities are only worth so much. The way I did this was to see what kind of value would likely exist for GE Aerospace as a whole once it and the rest of the company's operations, currently called GE Vernova, are separated early next year. When I initially purchased General Electric late last year, part of my investment thesis was that the healthcare subsidiary was worth a significant amount of capital compared to what the conglomerate as a whole was trading for. Sticking with that approach, I wanted to see if, by buying General Electric, I could pay for GE Aerospace while getting GE Vernova for free or something close to it.

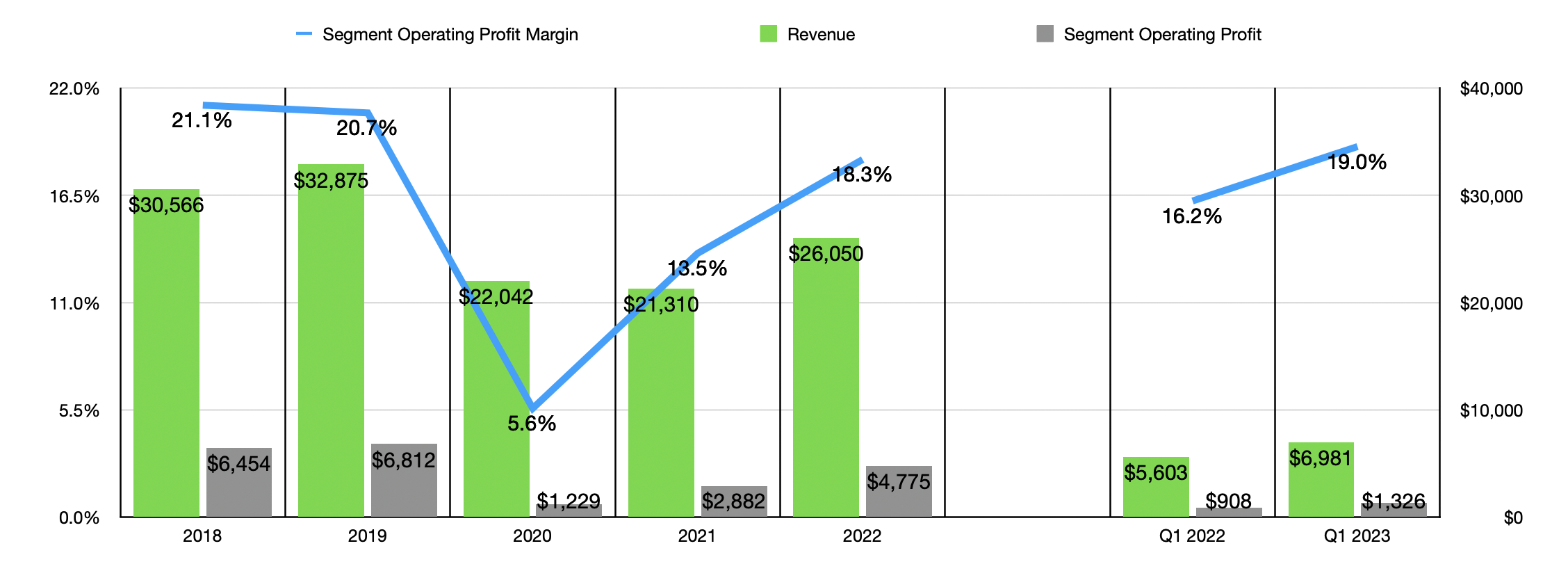

Sadly, I think the answer to this is no. For those who might be somewhat new to the conglomerate, GE Aerospace is the portion of General Electric that designs and produces commercial and military aircraft engines, as well as related parts and systems. It also provides services to its customers in the aviation space, such as maintenance and repair work. When you look at the overall financial picture of this portion of the enterprise, you see a rather interesting track record. The window of time in question that I have decided to focus on is from 2018 through the present day. In 2018, revenue for the unit came in at $30.57 billion. This popped to $32.88 billion in 2019 before falling over the next two years to hit $21.31 billion in 2021.

{kind=link}

This is not the kind of trajectory that you typically want to see. But there were good reasons for this decline. For starters, the COVID-19 pandemic caused air travel to more or less grind to a halt. This resulted in fewer orders for aircraft, as well as a reduction in shop visits. There were also other factors, largely ones that were outside of the control of the parent company. The most noteworthy was the 737 MAX grounding debacle. Produced by Boeing ( BA ), the 737 MAX aircraft saw some significant issues that culminated in two fatal crashes and a subsequent global grounding of the aircraft for well over a year. Given that GE Aerospace is responsible for the production of the LEAP engine that is used by the 737 MAX, it's not a surprise that the unit would suffer materially as a result.

Although I didn't own shares of the company during these times, I remained optimistic about its potential because I viewed these issues as transitory in nature. And sure enough, the company did experience an eventual rebound. Revenue hit $26.05 billion in 2022 as backlog shot up from $303.4 billion one year earlier to $352.6 billion by the end of last year. And so far this year, financial performance is even stronger. During the first quarter of the 2023 fiscal year, revenue for the unit totaled $6.98 billion. That's up 24.6% over the $5.60 billion generated one year earlier. Bottom line performance achieved by GE Aerospace has followed a very similar trajectory over the past few years. After bottoming out at $1.23 billion in 2020, segment operating income jumped to $4.78 billion last year.

For the current fiscal year, management expects revenue for the unit to climb at a rate between the mid-teens and the high-teens. For the purpose of valuing the company, I assumed this meant 17.5%. This would translate to revenue of $30.61 billion. And management has said that segment operating income would be between $5.3 billion and $5.7 billion, with a midpoint of $5.5 billion. This would translate to an operating profit margin of around 18%. For context, that number last year was 18.3%. And if you ignore the two weak years of 2020 and 2021, the number has ranged between a low of 18.3% and a high of 21.1% over the past five years.

| Company |

| Price / Sales |

| Price / Operating Profit |

| Honeywell International ( HON ) |

| 3.55 |

| 20.39 |

| Northrop Grumman ( NOC ) |

| 1.75 |

| 18.65 |

| Raytheon Technologies ( RTX ) |

| 1.94 |

| 25.73 |

| Lockheed Martin ( LMT ) |

| 1.74 |

| 13.68 |

| General Dynamics ( GD ) |

| 1.40 |

| 13.78 |

When you consider that GE Vernova is forecasted to generate negative segment profits this year, it becomes clear that General Electric derives most of its value from its GE Aerospace operations. Although I couldn't find a pureplay competitor to compare it to, I did find firms that were very similar to it from a structural perspective. For these five companies, I calculated that they are trading at a forward price to sales ratio of between 1.40 and 3.55. Meanwhile, their price to operating income ratio ranged between 13.68 and 25.73.

{kind=link}

To see what kind of upside potential, if any, might exist for shareholders of General Electric at this point, I decided to look at two different scenarios for both of these valuation metrics. The first was to assume that it would be worth the low end of what the range of these companies happens to be. The second, more aggressive, scenario, is to strip out the most expensive of the group, and then average out the other four to find an appropriate comparable multiple. Using the more conservative approach, I estimated that GE Aerospace should be worth between $42.85 billion and $75.24 billion. Meanwhile, using the more liberal approach, we get a range of between $52.34 billion and $91.47 billion. I would caution when it comes to relying on the higher end of this range. This is because the difference between segment operating profits and actual operating income for the competitors is that the segment operating profits don't factor in unallocated corporate expenditures. It would be wise to reduce the upper end of these ranges by around 10% to 15% or so. Regardless, General Electric on as a whole is worth around $109.16 billion.

| Company |

| EV / Sales |

| EV / Operating Profit |

| Honeywell International |

| 3.88 |

| 22.35 |

| Northrop Grumman |

| 2.04 |

| 21.78 |

| Raytheon Technologies |

| 2.34 |

| 31.36 |

| Lockheed Martin |

| 1.94 |

| 14.92 |

| General Dynamics |

| 1.60 |

| 15.74 |

It is important to keep in mind that, as of the end of the most recent quarter, General Electric technically is in a position where, on a net basis, that is negative. This means that the enterprise value of the company is around $107.94 billion. In the table below, I decided to repeat this analysis, swapping out the market capitalization of the company and swapping in its enterprise value. But as you can see, the numbers are not all that significantly different than what I calculated previously.

{kind=link}

Takeaway

Based on the data provided, I do believe that General Electric is still a great prospect for long term, value-oriented investors. Having said that, I do think that it is trading a lot closer to fair value than it was earlier this year. The market realized, with the spinoff of GE HealthCare Technologies, that the stock had been mispriced for some time. I would make the case that this has largely been rectified. Of course, GE Vernova likely is worth enough to at least make up the difference between the value of General Electric as a whole and what I estimate GE Aerospace to be worth (at least if GE Aerospace is worth near the high end of the range). But to me, having an attractive margin of safety is incredibly important and I feel like that has been eroded by the increase in stock price for the conglomerate. Because of this, I have decided to sell off my position in General Electric. I am submitting this article for publication in the early morning of May 10th. I do not know if it will be published before the market opens. But I likely will sell my shares some time in the late morning of May 10th.

For further details see:

General Electric: Not For Me Anymore